Understanding Wisconsin sales tax nexus requirements keeps your e-commerce business compliant while avoiding costly audit surprises. Since the 2018 Wayfair decision transformed remote seller obligations, crossing economic thresholds in Wisconsin triggers registration, collection, and filing responsibilities whether you maintain physical presence in the state or not.

That’s where Hands Off Sales Tax (HOST) helps. With over 25 years managing multi-state compliance, we analyze your Wisconsin nexus status, handle registrations, file returns, and respond to notices so you can focus on sales instead of decoding Wisconsin Department of Revenue requirements.

What Is Wisconsin Sales Tax Nexus?

Wisconsin sales tax nexus is the connection between your business and Wisconsin that creates a legal obligation to collect and remit sales tax. Once you establish nexus, you must register with the Wisconsin Department of Revenue, collect 5% state sales tax (plus applicable county and stadium taxes), and file returns on schedule.

Nexus operates on two principles: physical presence and economic activity. Physical nexus triggers when you maintain offices, employees, inventory, or property in Wisconsin. Economic nexus activates when your Wisconsin sales exceed specific dollar thresholds, regardless of physical presence.

The Wisconsin Department of Revenue enforces these requirements aggressively. Missing nexus obligations leads to back taxes, penalties, interest, and potential audits. Those are liabilities that compound the longer they remain unaddressed.

Wisconsin Economic Nexus: The $100,000 Threshold

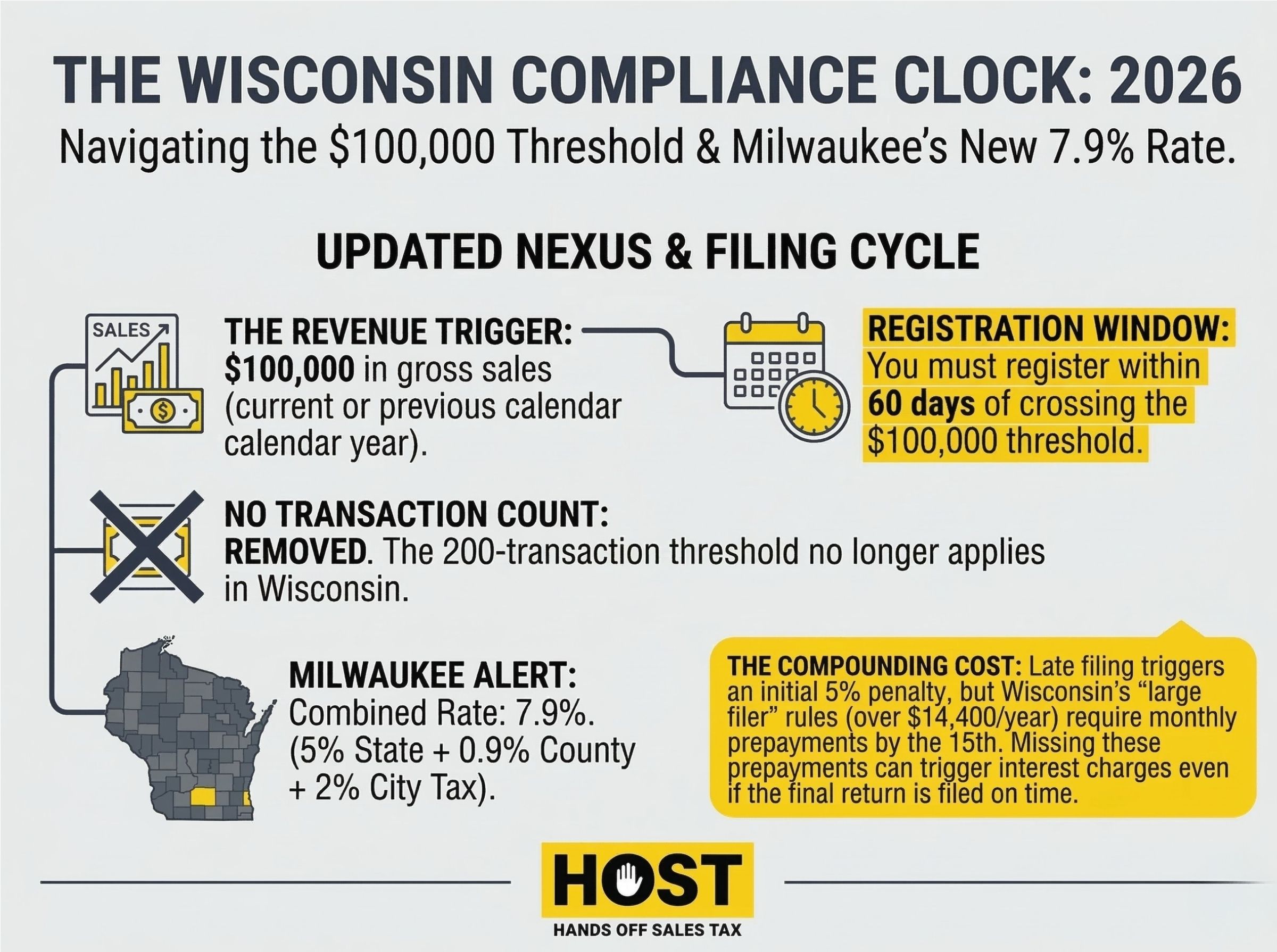

Wisconsin implemented economic nexus rules effective October 1, 2018, following the Supreme Court’s South Dakota v. Wayfair decision. Remote sellers meet Wisconsin economic nexus when gross sales to Wisconsin customers exceed $100,000 in the current or previous calendar year.

Unlike many states, Wisconsin uses a sales-only threshold with no transaction count requirement. Wisconsin originally required either $100,000 in sales OR 200 transactions when economic nexus began, but simplified compliance by eliminating the transaction count threshold in February 2021. Even businesses making relatively few high-value sales can trigger obligations quickly.

Calculation follows a calendar year basis. If you exceed $100,000 in Wisconsin sales during 2024, you establish nexus on January 1, 2025. However, if you exceed the threshold mid-year, Wisconsin requires registration within 60 days of crossing it.

Marketplace facilitator laws shifted responsibility for many sellers. Amazon, eBay, Etsy, Walmart Marketplace, and similar platforms collect Wisconsin sales tax on behalf of third-party sellers. If 100% of your Wisconsin sales occur through facilitator platforms, you typically don’t have independent nexus obligations. But any direct sales (through your own website, for example) count toward the $100,000 threshold.

Tracking becomes critical when you sell through multiple channels. Your Shopify sales plus direct Etsy checkout sales plus any other direct customer transactions must be aggregated to determine if you’ve crossed Wisconsin’s threshold.

Physical Nexus: Traditional Triggers That Still Matter

Economic nexus dominates discussions post-Wayfair, but physical nexus remains equally important, and often triggers obligations below economic thresholds.

Employees and Contractors: Remote workers living in Wisconsin while performing duties for your out-of-state business create nexus. Attending Wisconsin trade shows periodically can trigger nexus if you make sales or solicit orders.

Inventory and Fulfillment: Storing inventory in Wisconsin creates immediate nexus. This includes third-party warehouses, fulfillment centers, and FBA locations. If Amazon stores your products in a Wisconsin fulfillment center, you have physical nexus even if you never visit the state.

Drop Shipping Arrangements: Wisconsin takes a strict stance on drop shipping. If your supplier ships products to Wisconsin customers on your behalf, you may establish nexus through the supplier’s Wisconsin presence, depending on the arrangement’s structure.

Understanding exactly where you maintain physical presence requires careful analysis. HOST’s nexus analysis service reviews your complete operational footprint: employees, inventory locations, contractors, and affiliates to identify all Wisconsin nexus triggers, not just economic thresholds.

Wisconsin Sales Tax Rates: More Complex Than 5%

Wisconsin imposes a 5% state sales tax rate on most retail transactions. However, the total rate customers pay often exceeds 5% due to additional county and special district taxes.

County Sales Tax: Currently, 65 of Wisconsin’s 72 counties levy an additional 0.5%, bringing the combined rate to 5.5% in those jurisdictions.

Stadium Tax Districts: Milwaukee County imposes an additional 0.5% stadium tax to fund American Family Field, bringing the total rate to 6%. Five surrounding counties (Ozaukee, Washington, Waukesha, Racine, and Walworth) also collect the stadium tax. The City of Milwaukee adds an additional 2% city tax on top of state, county, and stadium taxes, creating Wisconsin’s highest combined rate of 7.9%.

Destination-Based Sourcing: Wisconsin uses destination-based sourcing for remote sellers. You charge sales tax based on where the customer receives the product, not where you ship from. This requires address-level tax calculation accuracy.

With over 70 counties and multiple special districts, manually calculating correct Wisconsin rates creates significant error risk. Sales tax automation software handles this complexity, but only when properly configured. HOST offers a Free Sales Tax Software Review to audit your configuration and prevent costly calculation errors.

How to Register for Wisconsin Sales Tax

Once you determine you have nexus, registration must happen quickly. Wisconsin requires registration within 60 days of establishing nexus.

Online Registration Process: Register through the Wisconsin Department of Revenue’s My Tax Account portal. You’ll need:

- Federal Employer Identification Number (FEIN) or Social Security Number

- Business legal name and trade names

- Physical business address and mailing address

- Business structure (LLC, corporation, sole proprietorship, etc.)

- Estimated Wisconsin sales volume

- Date you established nexus

Wisconsin issues a Sales and Use Tax Certificate immediately upon approval. This certificate displays your Wisconsin Tax ID number, which you’ll reference on all returns and correspondence.

HOST handles Wisconsin registration completely completing paperwork, navigating state systems, responding to follow-up requests, and ensuring you receive proper credentials. Through our Sales Tax Registration service, we’ve registered thousands of businesses across Wisconsin and all other states.

Wisconsin Sales Tax Filing Requirements and Deadlines

Wisconsin assigns filing frequency based on your annual sales tax liability: monthly, quarterly, or annual returns.

Monthly Filers: Businesses owing more than $1,200 annually file monthly returns due by the last day of the month following the reporting period. January sales are due February 28th.

Quarterly Filers: Businesses owing between $300 and $1,200 annually file quarterly returns due by the last day of the month following the quarter.

Annual Filers: Businesses owing less than $300 annually file annual returns due January 31st of the following year.

Prepayment Requirements: Large filers (those remitting over $14,400 annually) must make prepayments by the 15th of each month for the previous month’s collections, in addition to filing returns by month-end. This accelerated remittance schedule catches many businesses by surprise.

Late filing penalties start at 5% of tax due and increase monthly. Interest accrues daily at variable rates. These penalties compound quickly, turning small oversights into significant liabilities.

Managing Wisconsin filing requirements alongside 44+ other states creates overwhelming administrative burden. HOST’s Sales Tax Filing service handles Wisconsin returns automatically, ensuring deadlines are met, prepayments submitted on schedule, and your compliance record remains clean.

Voluntary Disclosure Agreements: Fixing Past Wisconsin Nexus

Discovering you had Wisconsin nexus for months or years creates a difficult situation. Ignoring it compounds liability through accumulating penalties and interest. Wisconsin offers a solution: Voluntary Disclosure Agreements (VDAs).

VDAs allow businesses to come forward voluntarily, register, and pay back taxes while limiting the look-back period and often abating penalties. Wisconsin typically limits VDAs to 4 years of back taxes rather than the 10-year statute of limitations.

VDA Benefits:

- Reduced look-back period (typically 4 years vs. 10 years)

- Penalty abatement in most cases

- Structured payment plans for large liabilities

- Anonymous filing option until terms are agreed upon

HOST manages Voluntary Disclosure Agreements across Wisconsin and all states, filing anonymously on your behalf, negotiating favorable terms, and minimizing your total liability.

What to Do If You Receive a Wisconsin Sales Tax Notice

Wisconsin Department of Revenue notices arrive for many reasons: unreported sales, late filings, underpayments, nexus questionnaires, or audit notifications. Many businesses panic and either ignore notices or respond without understanding implications.

Common Wisconsin Notice Types:

- Nexus Questionnaires: Wisconsin asks about your business activities to determine if you have filing obligations

- Filing Reminders: Notices when returns are overdue

- Discrepancy Notices: When reported sales don’t match third-party data Wisconsin receives

- Assessment Notices: Proposed tax liabilities based on Wisconsin’s calculations

Each notice type requires specific responses with tight deadlines. Typically 30 or 60 days. Missing response deadlines allows Wisconsin to finalize assessments, making them much harder to dispute.

Never Ignore Wisconsin Notices: Ignoring notices doesn’t make them disappear. Wisconsin can assess taxes unilaterally, freeze bank accounts, and file tax liens.

HOST’s Notice Management service interprets confusing Wisconsin correspondence, determines appropriate responses, and handles communications with the Department of Revenue—protecting you from penalties while resolving issues efficiently.

HOST: Your Wisconsin Sales Tax Compliance Partner

Wisconsin sales tax nexus represents just one piece of your multi-state compliance puzzle. Between monitoring economic thresholds across 45+ states, managing registrations, calculating rates correctly, filing returns on time, and responding to notices, sales tax consumes time that generates no revenue.

What HOST Delivers:

- Nexus Analysis: We analyze your Wisconsin sales data and operational footprint to determine exactly where you’ve triggered nexus

- Sales Tax Registration: We handle Wisconsin registration completely, navigating the My Tax Account portal and managing all Department of Revenue correspondence

- Sales Tax Filing: We prepare and file Wisconsin returns, including prepayments and local returns, keeping you current

- Sales Tax Consultation: Schedule 15, 30, or 60-minute consultations to discuss Wisconsin-specific scenarios or compliance strategy

- Audit Defense: We’re your trusted partner in resolving Wisconsin sales tax audits, organizing documentation and defending your position

- Voluntary Disclosure Agreements: If you’ve been selling into Wisconsin without collecting tax, we file VDAs to limit look-back periods and abate penalties

- Free Sales Tax Software Review: We audit your TaxJar, Avalara, or other automation setup to identify Wisconsin rate calculation errors

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping e-commerce businesses navigate Wisconsin and all other state requirements. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise-level expertise to sellers of all sizes.

Ready to Get Wisconsin Compliant?

Whether you just crossed Wisconsin’s $100,000 economic nexus threshold, discovered FBA inventory stored in Wisconsin fulfillment centers, or received a nexus questionnaire from the Department of Revenue, professional guidance eliminates guesswork and prevents costly mistakes.

Every day you operate with Wisconsin nexus without collecting tax increases your liability. Every missed filing deadline adds penalties. Every incorrectly calculated rate creates audit exposure.

Contact HOST today to discuss your Wisconsin sales tax needs or schedule a free consultation. Let us handle Wisconsin compliance, along with all your other states, so you can focus on growing sales instead of tracking nexus thresholds.

Want to learn more about common pitfalls? Download our free eBook: “10 Sales Tax Mistakes E-Commerce Sellers Make”.

Frequently Asked Questions

What is the Wisconsin sales tax nexus threshold for remote sellers?

Wisconsin establishes economic nexus when your gross sales to Wisconsin customers exceed $100,000 in the current or previous calendar year. Wisconsin uses only a sales threshold with no transaction count requirement.

Do I need to collect Wisconsin sales tax if I only sell through Amazon?

If 100% of your Wisconsin sales occur through marketplace facilitators like Amazon FBA, the platform collects Wisconsin sales tax on your behalf. However, any direct sales through your website or other channels count toward Wisconsin’s $100,000 nexus threshold and may create independent collection obligations.

How long do I have to register once I establish Wisconsin nexus?

Wisconsin requires registration within 60 days of establishing nexus. If you exceed the economic nexus threshold mid-year, you must register within 60 days of crossing $100,000.

What Wisconsin sales tax rate should I charge customers?

Wisconsin’s base rate is 5%, but 65 of 72 counties add 0.5% county tax. Milwaukee County and five surrounding counties add an additional 0.5% stadium tax. Use destination-based sourcing and charge tax based on the customer’s location. Rates range from 5% to 6% depending on the specific county and district.

What happens if I’ve been selling in Wisconsin without collecting sales tax?

If you established Wisconsin nexus previously but didn’t register or collect tax, you have potential back-tax liability. Wisconsin offers Voluntary Disclosure Agreements (VDAs) that limit the look-back period to approximately 4 years and often abate penalties.

Does having FBA inventory in Wisconsin create nexus?

Yes. Storing inventory in Wisconsin (including Amazon FBA fulfillment centers) creates physical nexus regardless of where your business is located. Physical nexus triggers immediate registration and collection obligations, separate from economic nexus thresholds.