Why do some states have no sales tax while you’re filing returns in 45 others? For e-commerce businesses navigating multi-state compliance, understanding tax-free states isn’t just interesting—it’s strategic.

Five states have opted out entirely: Alaska, Delaware, Montana, New Hampshire, and Oregon. No statewide sales tax. No collection systems. No monthly filing deadlines.

“Tax-free” doesn’t mean obligation-free. Alaska’s 100+ local jurisdictions impose their own sales taxes—remote sellers can trigger nexus in Anchorage or Juneau without state-level involvement. Oregon’s Corporate Activity Tax functions like gross receipts taxes elsewhere. Montana applies specific transaction fees.

Understanding where and how you pay sales tax is our expertise. Hands Off Sales Tax (HOST) helps in navigating sales tax obligations in all states, including the ones where “no sales tax” doesn’t mean “no obligations.”

What “Sales Tax-Free” Actually Means

A sales tax-free state doesn’t impose statewide sales tax on retail transactions. Customers don’t pay extra at checkout. Businesses don’t collect or remit to the state government.

The label can be misleading. Alaska allows over 100 local jurisdictions to impose their own sales taxes—rates from 1% to 7%. New Hampshire charges 9% on meals and lodging. While Oregon has a Commercial Activity Tax triggering at $1 million in state revenue.

Understanding what each state does—and doesn’t—tax keeps you ahead of surprise obligations.

The Five States That Skip Sales Tax

Oregon—Progressive Income Tax Replaces Sales Tax

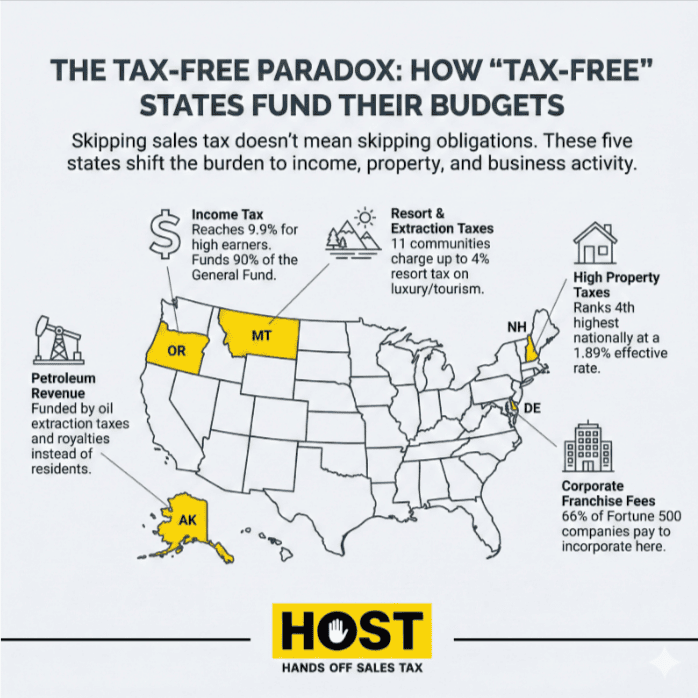

Oregon funds operations through progressive income taxes reaching 9.9% for high earners—among the highest in the nation. The state has rejected sales tax proposals ten times since 1910, most recently defeating Measure 118 in 2024 by a margin exceeding 75%.

Oregon’s anti-sales-tax stance runs deep. Voters consistently oppose sales taxes by overwhelming margins, viewing them as regressive and contrary to Oregon values. This pattern spans nine decades, making sales tax adoption essentially impossible without constitutional amendment.

Oregon added a major complexity in 2020: the Corporate Activity Tax (CAT). This gross receipts tax applies to businesses with over $1 million in Oregon commercial activity, calculated as:

$250 + [(Taxable Commercial Activity – $1 million) × 0.57%] = CAT Due

The CAT is particularly tricky because it operates differently than income tax. It’s based on gross receipts sourced to Oregon, minus a 35% deduction for either cost of goods sold or labor costs (whichever is greater). Unlike sales tax, the CAT pyramids—taxing products at each stage of the supply chain.

Registration is required at $750,000 in Oregon commercial activity, though no tax is due until hitting $1 million. Penalties for failing to register within 30 days: $100 per month, up to $1,000 annually.

For e-commerce businesses, this means two separate nexus analyses for Oregon: traditional income tax nexus and CAT nexus. You can owe CAT even if you’re not profitable, and you can owe CAT even if you have no physical presence in Oregon—economic activity alone triggers the obligation.

This is why HOST offers comprehensive nexus analysis services—we analyze your sales data to determine where you’ve met thresholds for any tax obligation, not just sales tax. Oregon’s CAT is precisely the kind of hidden obligation that catches businesses by surprise.

Alaska—Oil Revenue Replaces Everything

Alaska funds operations primarily through petroleum extraction taxes and royalties. The Alaska Permanent Fund, established in 1976, captures oil revenue and distributes annual dividends to residents—$1,702 per person in 2024, though amounts vary.

This resource-rich approach means Alaska can afford to skip sales tax at the state level.

But over 100 Alaskan municipalities impose their own sales taxes. Juneau charges 5%. Anchorage has no local tax. Kenai Peninsula Borough charges 3%.

Alaska has no economic nexus law requiring remote sellers to collect local taxes. However, physical presence in taxing municipalities triggers obligations. You’ll need address-level validation to determine which local tax applies.

Delaware—The Corporate Tax Haven

Delaware generates massive revenue from corporate franchise taxes and incorporation fees. Over 66% of Fortune 500 companies incorporate in Delaware because of favorable business laws, specialized Court of Chancery, and tax advantages.

Delaware also leans on gross receipts taxes for businesses and higher personal income taxes. For consumers and online sellers, this creates a genuinely tax-free shopping experience. No state sales tax. No local sales taxes.

Montana—Tourism and Income Taxes

Montana funds state government through a mix of individual income tax (with a top bracket of 6.75%), natural resource extraction taxes from coal, oil, and gas production, and tourism-related taxes. The state collected $246.8 million from natural resource extraction in 2016, though this revenue has become less reliable as coal and oil production has declined in recent years.

Tourism provides another revenue stream through specialized local taxes. Montana allows certain resort communities and areas to levy local option sales taxes—but only in specific tourist-dependent locations with limited populations.

Currently, 11 Montana communities impose resort taxes: Big Sky, Whitefish, Red Lodge, Virginia City, West Yellowstone, Cooke City, Craig, Gardiner, St. Regis, Wolf Creek, and Columbia Falls. All levy the maximum 3% rate (Big Sky actually charges 4% after voters approved an additional 1% for infrastructure in 2020).

These taxes apply to lodging, restaurants, bars, destination recreational facilities, and luxury goods—targeting tourists rather than residents. Under Montana law, only incorporated towns with fewer than 5,500 residents or unincorporated areas with fewer than 2,500 residents can implement resort taxes.

For e-commerce sellers, this creates a unique compliance challenge. Most of Montana remains genuinely sales tax-free. But if you’re selling taxable goods or services in these 11 resort communities, you need to track which local jurisdiction applies, register separately with each, and file local returns—all without state-level guidance or a unified system.

New Hampshire—”Live Free or Die” Tax Philosophy

New Hampshire operates under a unique revenue model: no sales tax, no personal income tax on wages. Instead, the state relies on property taxes (ranking 4th highest nationally by effective rate at 1.89% and 2nd highest by median annual payment at $6,372), business taxes, and industry-specific levies.

The Business Enterprise Tax (BET) charges 0.55% on a company’s “enterprise value tax base”—the sum of compensation paid to employees, interest expenses, and dividends. This applies to businesses with more than $298,000 in gross receipts or enterprise value. Unlike most business taxes, the BET taxes payroll and capital costs rather than profits, meaning companies can owe tax even without showing net income.

New Hampshire also imposes a Business Profits Tax at 7.5% on net income for businesses exceeding $92,000 in gross receipts. Together, these business taxes generate approximately 39% of state revenue—the highest percentage of any state in the nation.

Geographic advantage plays a role. New Hampshire borders Massachusetts, where sales tax hits 6.25%. A Massachusetts resident buying a $2,000 laptop in New Hampshire saves $125, driving significant cross-border retail traffic.

For e-commerce sellers, New Hampshire presents a paradox: no sales tax obligations to customers, but potential BET liability if your business reaches the $298,000 threshold and has nexus through physical presence, property, or exceeding 25% of your total property, payroll, or commercial activity in the state.

The Hidden Costs of “Tax-Free” States

Higher Taxes Elsewhere

Tax-free doesn’t mean low-tax. New Hampshire has property taxes among the top 3-7 highest nationally. Oregon’s income tax exceeds 9% at the top bracket. The tax burden shifts—high-income earners and property owners pay more.

Local Sales Taxes Create Compliance Chaos

Alaska has over 100 municipalities with local taxes. Montana allows limited resort area taxes.

This fragmented approach creates compliance complexity worse than statewide systems. You must research local ordinances, determine which jurisdictions apply, register and file in multiple localities—all without statewide guidance.

HOST handles these “special” local returns as part of our filing services—even tax-free states have filing obligations that catch you off guard.

Specialized Taxes That Function Like Sales Tax

New Hampshire’s 9% meals and rooms tax hits restaurants, hotels, and car rentals. Alaska charges lodging taxes. For businesses in affected industries, these create the same compliance burdens as sales tax—collection, reporting, remittance, audits.

What E-Commerce Businesses Need to Know

Nexus Exists Even Without Sales Tax

Physical presence creates a nexus. Economic activity creates a nexus. Nexus determines whether a state can impose any tax obligations on your business.

Oregon’s CAT triggers at $1 million in Oregon sales. Delaware’s gross receipts tax applies to businesses with substantial state revenue. Both operate independently of sales tax.

Since 2018, when the Wayfair decision changed everything, HOST has helped businesses understand exactly where they have obligations—in all states, including the “tax-free” ones.

Simplified Sales Tax Compliance, Hidden Complexity Elsewhere

No sales tax means no collection systems, no monthly filings, no rate updates. For businesses managing compliance across 45 states, eliminating five provides real relief.

Keep in mind, hidden complexities lurk. Alaska’s local taxes require address-level validation. New Hampshire’s industry-specific taxes catch hospitality businesses by surprise. Oregon’s CAT creates unexpected obligations.

HOST’s team manages these frequently confusing state notices so you don’t have to decipher them yourself.

Could More States Eliminate Sales Tax?

The Fiscal Reality

Eliminating sales tax in states that currently depend on it would crater budgets. Sales tax typically generates 30-40% of state revenue—funding for schools, roads, public safety, healthcare.

Replacing this revenue requires dramatic tax increases elsewhere or severe spending cuts. States with existing sales tax infrastructure have built decades of budgets around this revenue stream. Elimination is highly unlikely—bordering on impossible.

Post-Wayfair Competitive Dynamics

The 2018 South Dakota v. Wayfair Supreme Court decision gave states authority to require out-of-state sellers to collect sales tax based on economic nexus—customer location, not seller location.

This doesn’t directly affect tax-free states. But it eliminated their competitive advantage for online shopping. A Massachusetts resident buying from a New Hampshire online retailer still pays Massachusetts sales tax.

This post-Wayfair complexity is exactly why HOST exists. Through our parent company TaxMatrix, we’ve helped some of the largest companies in North America manage sales tax requirements. Now we bring that expertise to small e-commerce businesses navigating the same multi-state compliance challenges.

HOST: Your Partner for Navigating Tax-Free State Complexity

Sales tax compliance across 45 states creates complexity. Add local obligations in Alaska, industry-specific taxes in New Hampshire, and business-level taxes in Oregon and Delaware, and you’ve got a compliance landscape demanding expertise.

What HOST Delivers:

- Nexus Analysis: We analyze your sales data to determine where you’ve met thresholds for economic or physical nexus—including gross receipts taxes.

- Sales Tax Registration: We apply for registrations with every applicable state taxing jurisdiction, handling all paperwork.

- Sales Tax Filings: HOST offers filing plans to meet your needs. We file your returns—including local and “special” returns—so everything stays current.

- Notice Management: We handle confusing notices from states, interpreting what they mean and responding appropriately.

- Audit Defense: We’re your trusted, battle-tested partner in resolving your sales tax audit, organizing documentation and defending your position.

- VDA Support: We file voluntary disclosure agreements to limit look-back periods and abate penalties.

We’ve been 100% focused on sales tax since 1999—that’s 25 years managing compliance so you can keep your hands on your business. Co-founded by Mike Espenshade, with parent company TaxMatrix serving the largest companies in North America.

Contact HOST today to discuss your multi-state compliance needs. Let’s ensure you’re collecting in the right states, handling local obligations correctly, and staying ahead of tax-free state complexities.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Why do some states have no sales tax?

States without sales tax fund operations through alternative revenue models—higher income taxes, property taxes, natural resource extraction fees, corporate taxes, and industry-specific transaction taxes. Alaska, Delaware, Montana, New Hampshire, and Oregon each leverage unique economic advantages.

Do I collect any taxes when selling to customers in tax-free states?

Generally no, but exceptions exist. Alaska has over 100 local jurisdictions with their own sales taxes. New Hampshire charges 9% on lodging and restaurant meals. Oregon and Delaware have gross receipts taxes based on business revenue thresholds. If unsure, HOST offers consultation services.

Can tax-free states still impose other business taxes on my company?

Absolutely. Tax-free states can impose income taxes, franchise taxes, gross receipts taxes, business license fees, and transaction taxes on businesses with nexus. A comprehensive nexus analysis helps identify all obligations.

Are tax-free states actually lower-tax overall?

Not necessarily. New Hampshire has property taxes ranking among the top 3-7 highest nationally. Oregon’s income tax exceeds 9% at the top bracket. Alaska and New Hampshire rank among genuinely low-tax states overall, but others land closer to national averages.

Could states with sales tax eliminate it like these five states did?

Highly unlikely. Sales tax generates 30-40% of state revenue for most states that collect it. The five tax-free states never established sales tax infrastructure—different path entirely.

How does the Wayfair decision affect tax-free states?

Wayfair doesn’t directly impact tax-free states since they have no sales tax to collect. However, it eliminated their cross-border shopping advantage for online purchases, leveling the competitive playing field for e-commerce.