Washington’s economic nexus threshold draws a clear line: cross $100,000 in sales to the state, and you’re obligated to collect sales tax. Even if you’ve never stepped foot in Seattle.

For e-commerce sellers expanding into Pacific Northwest markets, understanding where that threshold sits prevents costly surprises. Miss it, and you’re looking at audits, penalties stacking up monthly, and compliance gaps that compound with interest.

Hands Off Sales Tax (HOST) eliminates the guesswork. From nexus analysis determining where you’ve triggered obligations to handling registration and ongoing filings, our 25+ years of focused expertise keeps you collecting in the right states without drowning in compliance work.

What Economic Nexus Actually Means

Economic nexus establishes a state’s authority to require sales tax collection based on economic activity rather than physical presence. Before the 2018 South Dakota v. Wayfair ruling, states could only require collection from businesses with physical footprints: stores, warehouses, employees, or inventory within state borders.

Wayfair changed everything. The Supreme Court ruled that states can require out-of-state sellers to collect sales tax once they exceed state-defined thresholds. Modern e-commerce creates substantial economic connections without physical presence, and states wanted their cut.

For online sellers, this means monitoring sales into every state. Cross a threshold through revenue or transaction volume, and you’ve triggered collection obligations, regardless of whether you’ve ever operated physically in that state.

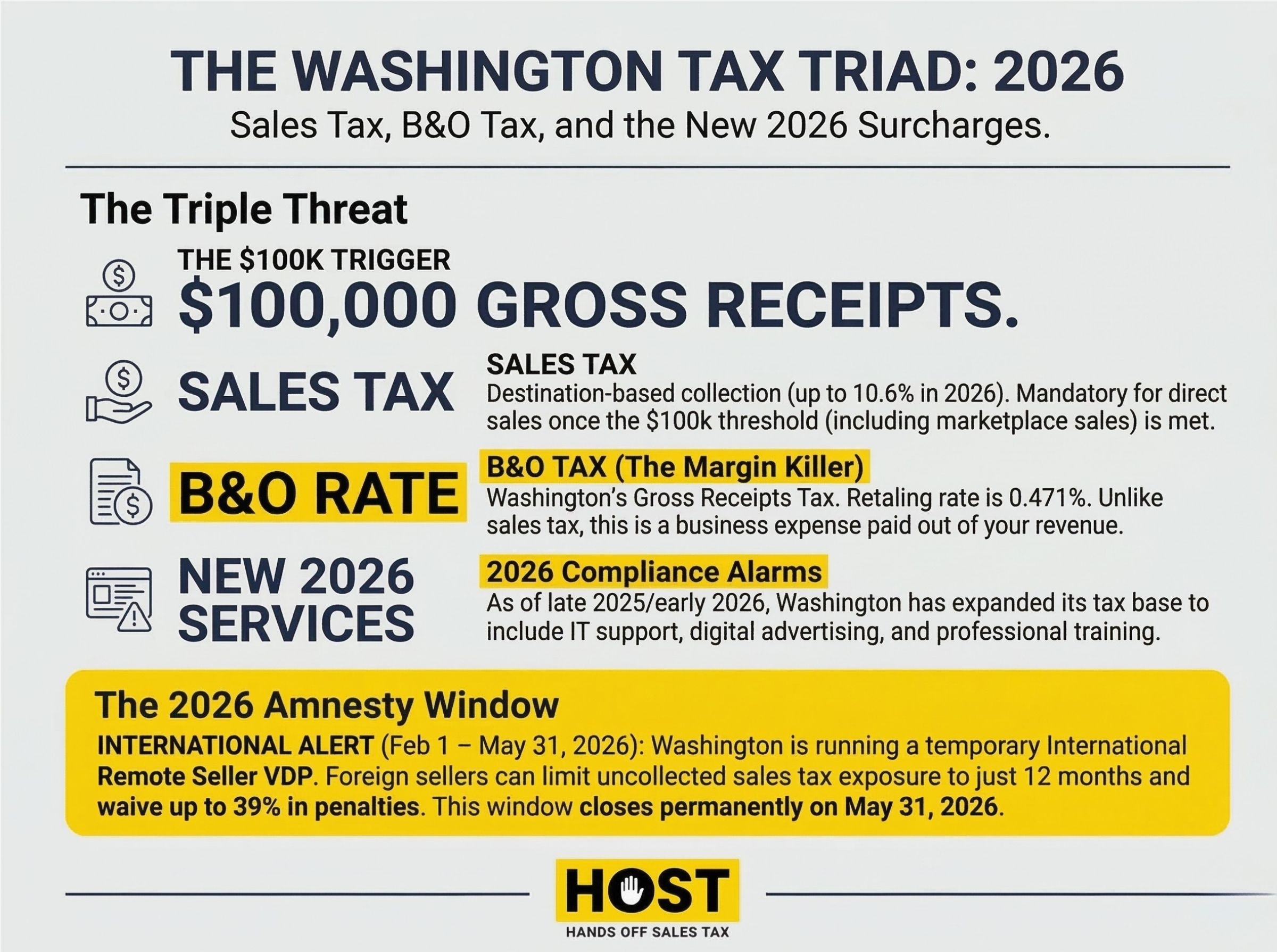

Washington’s $100,000 Threshold

Washington State Department of Revenue implemented economic nexus rules October 1, 2018, shortly after Wayfair. The threshold is straightforward: $100,000 in gross receipts from Washington sales in the current or prior calendar year.

That’s it. No transaction count to track. Unlike states that also count order numbers (like 200 transactions), Washington focuses exclusively on dollar volume. Washington originally included a 200-transaction threshold but eliminated it March 14, 2019, simplifying compliance for remote sellers.

“Gross receipts” means total sales sourced to Washington customers. Retail sales of tangible personal property, digital goods, digital codes, digital automated services, and certain taxable services. Shipping charges included in the sale price count if the sale itself is taxable.

The B&O Tax Surprise Most Sellers Miss

Here’s what catches e-commerce sellers off-guard: crossing Washington’s $100,000 threshold creates Business & Occupation (B&O) tax liability.

Since January 1, 2020, any business exceeding $100,000 in cumulative gross receipts owes B&O tax on those Washington sales. For retailers, that’s 0.471% of gross receipts with no deductions for costs or expenses.

Example: $200,000 in Washington sales means you collect approximately $13,000-$21,000 in sales tax from customers (which you remit to the state) AND you pay approximately $942 in B&O tax out of your revenue to Washington.

Unlike sales tax (which customers pay), B&O tax comes directly from your margins. Most sales tax advisors focus exclusively on collection obligations and never mention this additional tax layer. HOST’s comprehensive nexus analysis identifies both obligations, ensuring you understand your complete Washington tax footprint.

The Lookback Provision That Catches People

Washington uses a calendar year measurement period with a lookback. If you exceeded $100,000 during the current calendar year, register immediately once you cross that line. If you exceeded $100,000 in the prior calendar year, you have nexus for the entire current year, even if current year sales haven’t reached $100,000.

Sell $120,000 to Washington customers in 2024? You have economic nexus for all of 2025 regardless of 2025 sales volume. This lookback provision means hitting the threshold once creates ongoing obligations until your sales drop below $100,000 for an entire calendar year.

What Counts (And What Doesn’t)

Washington counts ALL retail sales toward the threshold, including tax-exempt items. Selling groceries, prescription drugs, or other exempt products? Those sales still count toward your $100,000 nexus determination.

Marketplace sales create a tricky tracking requirement: Even though Amazon or Etsy collects tax on your behalf for those sales, you must still count that revenue when determining if you’ve crossed the $100,000 threshold. Hit $100,000 total (including marketplace sales), and you must register and collect tax on your DIRECT sales (through your website, at events, or other non-marketplace channels).

This distinction confuses many sellers. The marketplace facilitator handles collection and remittance for sales through their platform. You don’t owe tax on those specific transactions. But those sales DO count when calculating whether you’ve triggered nexus. Once you hit the threshold through any combination of marketplace and direct sales, you must collect on everything the marketplace doesn’t handle.

Wholesale sales don’t count. If you’re selling products for resale to retailers who provide valid resale certificates, those transactions are excluded from the $100,000 calculation. Only retail sales to end consumers factor into the threshold.

Registration Timing and Grace Periods

Once you meet Washington’s threshold, registration timing depends on when you crossed it:

Current year threshold: If you exceed $100,000 during the current calendar year, you must register and begin collecting sales tax on the first day of the month that starts at least 30 days after you cross the threshold. Cross $100,000 on June 15? You must begin collecting August 1.

Prior year threshold: If you exceeded $100,000 in the prior calendar year, you should have registered by January 1 of the current year. Discovering this mid-year? Register immediately and consider a voluntary disclosure agreement to address past liability.

Washington assigns filing frequencies based on estimated tax liability: monthly, quarterly, or annually. Most businesses meeting economic nexus start quarterly, though high-volume sellers may get monthly obligations.

Penalties for failing to register hit hard. Washington assesses penalties starting at 9% of tax due if not paid by the due date, increasing to 19% after the last day of the following month, and 29% after the last day of the second month following the due date. Interest accrues on top. An audit discovering unfiled returns can assess back multiple years with compounding penalties.

Destination-Based Rates Add Complexity

Washington has no uniform sales tax rate. The state base sits at 6.5%, and local jurisdictions pile on their own rates. Combined state and local rates range from 7.0% to 10.6% depending on customer location.

Washington uses destination-based sourcing for remote sellers. You must collect the rate applicable at the customer’s shipping address. With over 300 local tax jurisdictions in Washington, manual rate calculation is impractical.

Sales tax automation software integrates with e-commerce platforms to calculate correct rates based on customer addresses. However, misconfigured software overcharges customers or applies incorrect rates. Common errors HOST identifies through our Free Sales Tax Software Review.

When You’ve Already Crossed the Line

Discovered you already exceeded Washington’s $100,000 threshold? Whether recently or in past years? Don’t panic. Options exist to resolve past liabilities while minimizing penalties.

Register Immediately

Even if you should have registered months ago, register now. Continuing to operate without registration after discovering your obligation makes matters worse. You’ll need to register for both sales tax collection and B&O tax reporting.

Consider a Voluntary Disclosure Agreement

Washington offers a Voluntary Disclosure Program for businesses that failed to collect when required. Through a VDA, you can limit the lookback period (typically to 4 years instead of Washington’s standard statute), potentially reduce or eliminate penalties, and resolve past liabilities without extensive audit procedures.

VDAs require coming forward before Washington contacts you. Once the state initiates contact, VDA options typically disappear. Acting proactively demonstrates good faith and saves substantial penalty costs.

HOST manages the VDA process: preparing calculations, negotiating with states, and handling all communications. Our experience with Washington’s program ensures you get the best possible resolution while limiting liability exposure.

Start Collecting Going Forward

Once registered, begin collecting Washington sales tax immediately on all taxable sales to Washington customers. Configure your e-commerce platform to calculate and collect correct destination-based rates. If you’re unsure about your software configuration, HOST offers a Free Sales Tax Software Review to identify costly mistakes before they create audit problems.

Physical Nexus Creates Immediate Obligations

Economic nexus isn’t your only potential connection to Washington. Physical nexus creates independent obligations regardless of sales volume.

You have physical nexus in Washington if you have:

- Office, warehouse, or retail location in Washington

- Employees working in Washington (including remote workers residing there)

- Inventory stored in Washington (including FBA inventory in Amazon’s Washington fulfillment centers)

- Contractors or agents soliciting sales on your behalf in Washington

- Business organized or commercially domiciled in Washington (incorporated or LLC formed there)

Physical nexus existed long before Wayfair and operates independently from economic nexus. A business with even one employee in Washington has nexus regardless of whether Washington sales reach $100,000. Similarly, if your business is incorporated in Washington, you have automatic nexus even without any sales activity.

For B&O tax purposes, physical presence creates nexus immediately. You owe B&O tax on all Washington-sourced income from day one, regardless of volume.

HOST: Managing Washington and Beyond

Washington’s threshold is one of 45+ state frameworks you’re navigating as an e-commerce business. Each state sets its own thresholds, measurement periods, sourcing rules, and filing requirements, creating a compliance landscape that demands expertise and dedicated management.

What HOST Delivers:

Comprehensive Nexus Analysis: We analyze your sales data across all states, identifying exactly where you’ve met thresholds (including Washington’s $100,000 requirement) and where physical nexus might exist. We assess both sales tax AND B&O tax obligations, ensuring you understand your complete Washington tax exposure.

Washington Registration: We handle the entire registration process with Washington State Department of Revenue, completing applications for both sales tax collection and B&O tax reporting, selecting appropriate classifications, and ensuring you’re set up correctly from day one.

Ongoing Filing Management: We prepare and file your Washington sales tax returns and B&O tax returns on the assigned schedule, managing deadlines and ensuring accuracy. This includes local jurisdiction reporting and special district taxes.

Multi-State Compliance: Washington is rarely your only obligation. We manage sales tax compliance across all states where you have nexus, providing unified oversight that prevents any jurisdiction from falling through the cracks.

Software Configuration Review: Our Free Sales Tax Software Review identifies if your TaxJar, Avalara, or other automation tool is correctly calculating Washington’s destination-based rates and properly handling exemptions, preventing overcharging or undercollection.

VDA Support: If you’ve exceeded Washington’s threshold in the past without collecting, we file voluntary disclosure agreements to limit lookback periods and minimize penalties, resolving liabilities before they become audit assessments.

We’ve focused exclusively on sales tax for over 25 years. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

Ready to Get Compliant?

Understanding Washington’s threshold is step one. Managing compliance across Washington and dozens of other states while running your business is the real challenge.

Whether you’re approaching the $100,000 threshold, already exceeded it without registering, or simply want expert oversight of your multi-state obligations, HOST eliminates the complexity. We combine deep technical knowledge with transparent communication and personalized support, so you’re never left guessing about your compliance status.

Contact HOST today to discuss your Washington nexus situation and discover how we take sales tax off your plate.

You handle the sales, we handle the tax.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is Washington’s economic nexus threshold?

Washington’s threshold is $100,000 in gross receipts from retail sales to Washington customers in the current or prior calendar year. No transaction count requirement. Only the dollar threshold matters. This applies to all retail sales, including tax-exempt items.

Does crossing Washington’s threshold trigger any taxes besides sales tax?

Yes. Exceeding $100,000 in Washington sales triggers both sales tax collection obligations AND Business & Occupation (B&O) tax liability. B&O tax for retailers is 0.471% of gross receipts with no deductions for expenses. Most sellers focus only on sales tax and get surprised by B&O tax obligations.

Do marketplace sales count toward Washington’s threshold?

Yes, marketplace sales through Amazon, Etsy, eBay, and similar platforms count toward your $100,000 threshold calculation, even though the marketplace collects tax on those specific sales. Once you hit $100,000 (including marketplace sales), you must register and collect tax on your direct sales through your website or other non-marketplace channels.

When must I start collecting after crossing the threshold mid-year?

If you exceed $100,000 during the current calendar year, you must begin collecting sales tax on the first day of the month that starts at least 30 days after you cross the threshold. Cross the threshold June 15? Start collecting August 1.

Does Washington use origin or destination-based sourcing?

Washington uses destination-based sourcing for remote sellers. You must collect the sales tax rate applicable at the customer’s shipping address. With over 300 local tax jurisdictions, accurate rate calculation requires automation tools or expert management.

Can I have nexus in Washington without any sales?

Yes. Physical presence creates immediate nexus regardless of sales volume. Having an office, warehouse, employee, or inventory in Washington triggers both sales tax and B&O tax obligations. Additionally, if your business is incorporated or organized in Washington, you have automatic nexus.