Understanding Utah sales tax nexus is the legal trigger that determines whether your business must collect and remit sales tax in the state. With economic nexus thresholds, marketplace facilitator rules, and aggressive audit enforcement, Utah has become a compliance priority for remote sellers nationwide.

This guide breaks down exactly when nexus is created, what activities trigger obligations, and how to stay compliant without disruption. If you’re already past the threshold or facing audit risk, Hands Off Sales Tax (HOST) provides full-service nexus analysis, registration, filing, and audit defense to keep your business protected.

What Is Sales Tax Nexus in Utah?

Sales tax nexus is the legal connection between your business and Utah that obligates you to collect and remit sales tax. It’s not about whether you’re “doing business” in the traditional sense, it’s about whether the state can enforce tax collection based on your activities or sales volume within its borders.

Under Utah law, nexus can be established through physical presence (like having an office or storing inventory) or through economic activity (crossing sales thresholds). Once nexus is triggered, you must register with the Utah State Tax Commission, collect the correct sales tax rate, and file returns on schedule.

A common misconception: “I don’t have an office in Utah, so I’m exempt.” That’s no longer true. Even remote sellers with zero physical footprint can trigger nexus through sales alone, and Utah actively enforces these rules.

Why Utah Sales Tax Nexus Matters More After Wayfair

The landscape shifted dramatically in 2018 with South Dakota v. Wayfair, Inc., which eliminated the physical presence requirement for sales tax nexus. Before Wayfair, states couldn’t compel remote sellers to collect tax without a physical connection. After Wayfair, economic activity alone became sufficient.

Utah wasted no time adopting economic nexus standards. The state now requires out-of-state sellers to collect tax if they exceed specific revenue thresholds regardless of whether they have employees, warehouses, or offices in Utah.

This decision also accelerated audit activity. States began sharing data through initiatives like the Streamlined Sales Tax Project, cross-referencing marketplace reports, 1099-K forms, and shipping records to identify non-compliant sellers. Penalties compound quickly: back taxes, interest, and failure-to-file penalties can accumulate over multiple years if nexus obligations are ignored.

For growing businesses, Wayfair transformed nexus from a theoretical concern into an operational imperative.

Economic Nexus in Utah: Thresholds You Must Monitor

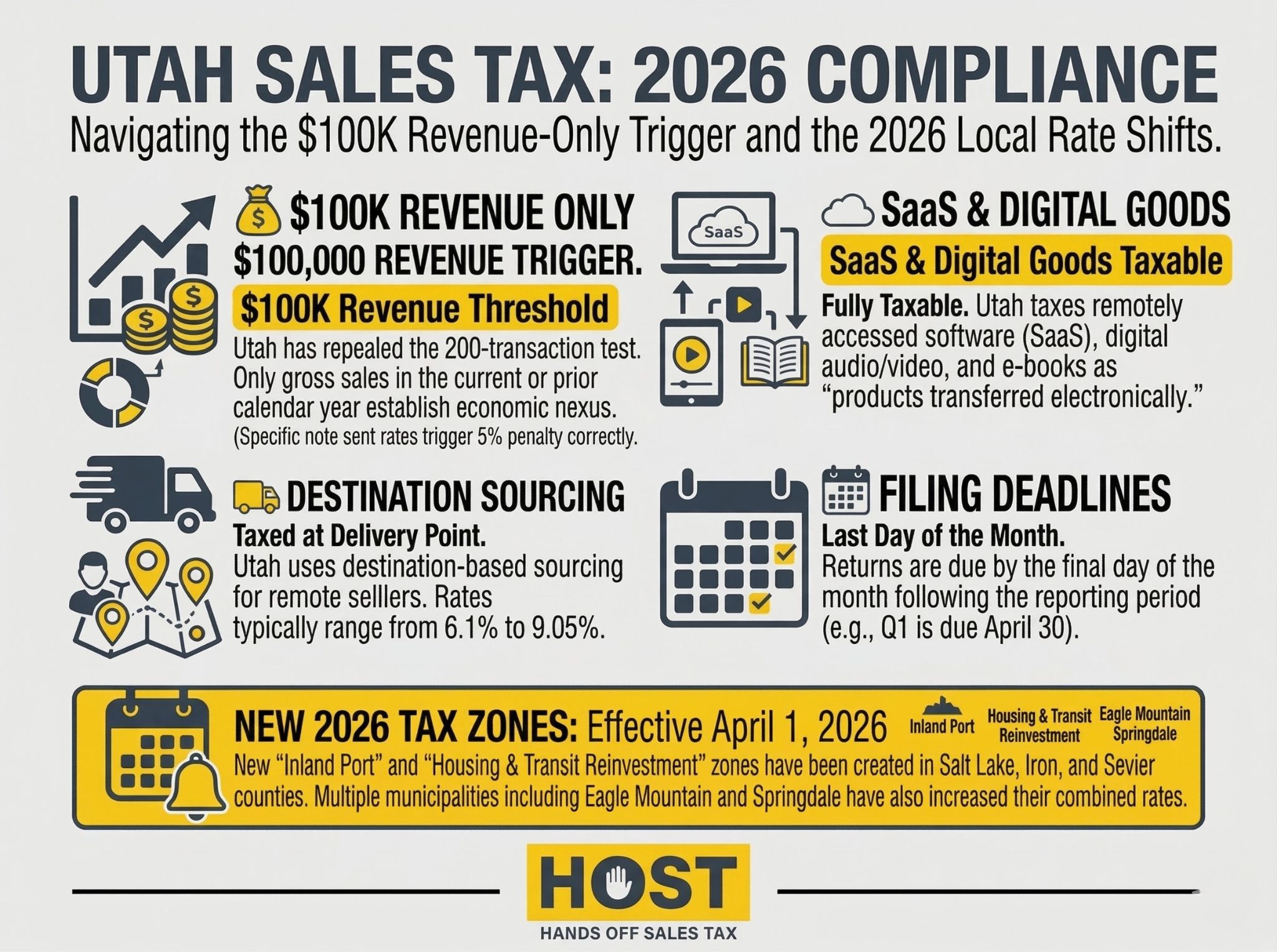

Utah’s economic nexus threshold is straightforward but unforgiving: $100,000 in gross sales into the state within the current or previous calendar year. There is no transaction count threshold. Only revenue matters.

What Counts Toward the Threshold?

Not all sales are equal when calculating your exposure. Here’s what Utah includes:

- Taxable sales: Retail sales of tangible personal property and specified digital products

- Exempt sales: Sales to entities with valid exemption certificates (these still count toward the threshold)

- Wholesale and B2B sales: These count, even if tax wasn’t collected due to resale certificates

- Digital goods and SaaS: Utah taxes specified digital products delivered electronically, including software, apps, and digital audio/visual works

What doesn’t count: sales through marketplace facilitators where the platform collects tax on your behalf may not always need to be included, depending on how Utah tracks reporting obligations. However, this is a gray area. It’s safer to monitor total sales volume.

When Nexus Is Triggered

Once you cross $100,000 in sales, nexus is established immediately. You must register with the Utah State Tax Commission and begin collecting tax on your next sale into the state.

Utah doesn’t offer a grace period. If you cross the threshold in July, you’re expected to register and collect tax starting in August or face penalties for late registration and uncollected tax.

Physical Nexus in Utah: More Than an Office

Physical nexus is the original nexus trigger, and it is still very much in play. Unlike economic nexus, which resets annually, physical nexus persists as long as the qualifying activity continues.

Here’s what creates physical nexus in Utah:

- Offices, warehouses, or storefronts: Any owned or leased space

- Inventory stored in Utah: This includes third-party logistics (3PL) warehouses and Amazon FBA fulfillment centers

- Employees or contractors: Even one remote employee living in Utah can trigger nexus

- Trade shows and conventions: Attending an event in Utah for more than a few days may create temporary physical presence

- Installation or service activity: Sending staff to install, repair, or service products in-state

The most overlooked trigger? FBA inventory. Amazon dynamically distributes inventory across its network, meaning goods you thought were in Nevada might land in a Utah warehouse, creating nexus without your knowledge. Sellers should regularly review Amazon’s inventory placement reports in Seller Central to track exposure.

Marketplace Facilitator Rules in Utah

Utah’s marketplace facilitator law shifts tax collection responsibility to platforms like Amazon, Etsy, Walmart, and eBay; but it doesn’t eliminate your obligations entirely.

When Marketplaces Collect on Your Behalf

If you sell through a qualifying marketplace, the platform collects and remits sales tax for those transactions. This covers the vast majority of e-commerce sellers using major platforms.

When Sellers Still Have Obligations

Even if marketplaces handle collection, you may still need to:

- Register with Utah: Some states require sellers to register even when marketplaces collect tax

- Report direct sales: Any sales made outside the marketplace (e.g., through your own website) are your responsibility

- File returns: Utah may require you to file “zero returns” or report marketplace sales separately, depending on your registration status

Common Marketplace Compliance Mistakes

The biggest error? Assuming “Amazon handles everything.” While marketplaces collect tax on facilitated sales, they don’t:

- Monitor your overall nexus status across channels

- Register your business with the state

- Handle audits or notice responses on your behalf

- Calculate local tax components if you have physical nexus requiring origin-based sourcing

If you sell both on and off marketplaces, or if you have physical presence in Utah, you can’t rely solely on marketplace collection.

Local Sales Taxes in Utah: State vs Local Jurisdictions

Utah operates a combined state and local sales tax system. The state base rate is 4.85%, but total rates vary significantly by jurisdiction due to local option taxes imposed by cities, counties, and special taxing districts.

Total rates in Utah can range from around 6.1% to over 9%, depending on the destination. Utah uses destination-based sourcing for remote sellers, meaning you must collect the rate applicable to the buyer’s location, not your warehouse or office.

Why does this matter? Incorrect rate calculation is one of the most common audit triggers. If you collect the state rate but ignore local components, you’ll owe the difference plus penalties and interest. Even worse, if you overcollect and remit the wrong local allocation, you may face reconciliation requirements during an audit.

What Happens If You Ignore Utah Sales Tax Nexus?

Ignoring nexus doesn’t make it disappear. In fact, it compounds. Here’s what businesses face when they fail to register or collect tax:

- Failure-to-register penalties: Utah assesses penalties for late registration, often calculated as a percentage of tax due

- Back taxes and interest: The state can pursue uncollected tax going back four years from the date of discovery, plus interest compounding monthly

- Audit triggers: Utah shares data with other states and receives 1099-K information from payment processors. Cross-referencing sales records makes non-compliance easy to detect

- Personal liability: In some cases, business owners or officers can be held personally liable for unpaid sales tax

Penalties don’t scale linearly, they accelerate. A $10,000 tax liability ignored for two years can balloon to $15,000+ with interest and penalties. Early action is always cheaper than delayed compliance.

Utah Sales Tax Audits: What Businesses Should Expect

Utah conducts audits to verify compliance, typically triggered by:

- Discrepancies in reported sales vs. 1099-K or marketplace data

- Failure to file returns after registration

- Tips or referrals from other states or agencies

- Random selection from high-volume sellers

During an audit, the Utah State Tax Commission will request:

- Sales records and invoices

- Exemption certificates

- Filing history and nexus documentation

- Proof of tax collected and remitted

Audits typically review a three-year period, though the state can extend this if fraud or willful neglect is suspected. Most audits result in assessments, but cooperative businesses often negotiate settlements or payment plans. Appeals are possible but require documented evidence and timely response.

The key? Treat audits as procedural, not adversarial. With organized records and professional representation, most issues can be resolved without severe penalties.

How to Register and Comply Once You Have Nexus

Once nexus is established, here’s your compliance roadmap:

- Register with the Utah State Tax Commission: File a Utah TC-69 Application for a sales tax license. Registration is free and can be completed online.

- Determine your filing frequency: Utah assigns filing frequency based on your tax liability: monthly, quarterly, or annually. High-volume sellers typically file monthly.

- Collect the correct rate: Use Utah’s Tax Rate Lookup Tool to determine destination-based rates for each transaction.

- File and remit on time: Returns are due by the last day of the month following the reporting period. Late filing triggers penalties even if no tax is owed.

- Monitor ongoing nexus: Track sales volume, inventory placement, and affiliate relationships to ensure you stay compliant as your business evolves.

Voluntary Disclosure & Penalty Relief Options in Utah

If you’ve already triggered nexus but haven’t registered, Utah’s Voluntary Disclosure Program may offer relief. The program allows businesses to come forward proactively, often resulting in:

- Reduced lookback periods: Instead of four years, Utah may limit liability to three years or less

- Waived penalties: Late-filing and failure-to-register penalties can be reduced or eliminated

- Anonymity during negotiation: You can explore options before formally identifying your business

However, timing is critical. Once Utah contacts you directly through an audit notice, inquiry, or assessment, you’re no longer eligible for voluntary disclosure. The window closes fast, so proactive action is essential.

How Hands Off Sales Tax Helps Businesses Stay Compliant in Utah

Sales tax compliance doesn’t have to derail your operations. Hands Off Sales Tax (HOST) provides end-to-end support for businesses navigating Utah’s nexus rules, including:

- Nexus analysis: Pinpoint exactly where you have obligations based on your sales, inventory, and business activities

- Registration and filing: Handle Utah registration, rate calculation, and timely filing across all jurisdictions

- Marketplace reconciliation: Ensure your marketplace sales are properly reported and separated from direct sales

- Audit defense: Professional representation during audits, with documentation review and settlement negotiation

- Voluntary disclosure support: Navigate Utah’s VDA program to minimize liability and secure penalty relief

With over 25 years of experience, HOST manages compliance so you can focus on growth without the distraction of tracking thresholds, filing deadlines, or audit notices.

Don’t Let Utah Nexus Catch You Off Guard

Utah sales tax nexus is broader than most businesses expect, and the state enforces it aggressively. Whether you’ve crossed the economic threshold, stored inventory in-state, or sold through marketplaces, understanding your obligations is the first step toward avoiding penalties.

Hands Off Sales Tax makes that possible. From nexus analysis to audit defense, we provide the expertise and systems you need to stay compliant across Utah and beyond. If your business is selling into Utah, now is the time to get proactive before a notice shows up in your inbox.

Utah Sales Tax Nexus FAQ

Do remote sellers need to collect Utah sales tax?

Yes. Remote sellers must collect and remit Utah sales tax if they establish economic nexus or physical nexus in the state. Physical presence is not required. Once nexus is triggered, registration and ongoing compliance are mandatory.

What is Utah’s economic nexus threshold?

Utah economic nexus is triggered when a business has $100,000 or more in gross sales into Utah during the current or previous calendar year. There is no transaction-count threshold.

When does the obligation to collect Utah sales tax begin?

The obligation begins immediately after the economic nexus threshold is exceeded. Businesses are expected to register promptly and begin collecting sales tax on taxable Utah sales from that point forward.

What types of sales count toward Utah’s nexus threshold?

All gross sales delivered into Utah count toward the threshold, including:

- Taxable and non-taxable sales

- Retail and wholesale transactions

- Online, marketplace, and direct sales

Returns and exempt transactions generally still count toward gross sales calculations.

Does selling through Amazon or Etsy create Utah sales tax nexus?

Selling through a marketplace does not automatically create nexus, but marketplace facilitator laws apply. Marketplaces like Amazon and Etsy are required to collect and remit Utah sales tax on behalf of sellers for marketplace transactions. However, sellers may still have registration or filing obligations if they also make direct sales.

Do marketplace sellers still need to register in Utah?

In many cases, yes. Businesses with Utah nexus may still be required to register and file returns, even if all tax is collected by a marketplace facilitator. Filing requirements depend on the seller’s overall activity and sales channels.

Does inventory stored in Utah create sales tax nexus?

Yes. Storing inventory in Utah in a warehouse, fulfillment center, or through Amazon FBA creates physical nexus, even if the seller has no employees or offices in the state.

Do services or SaaS products create Utah sales tax nexus?

They can. Nexus depends on sales activity, not taxability. Even if a service or SaaS product is partially or fully exempt from Utah sales tax, the revenue may still count toward the economic nexus threshold, triggering registration and filing obligations.

What happens if I fail to register after establishing Utah nexus?

Failure to register triggers a cascade of penalties:

- Back taxes owed for all periods where nexus existed

- Interest compounding monthly on unpaid amounts

- Failure-to-file and failure-to-remit penalties

- Multi-year lookback periods during audits, potentially going back four years or more

The longer noncompliance continues, the worse the exposure becomes. If you’ve crossed the threshold but haven’t registered, HOST’s nexus analysis service can help you assess liability and take corrective action before the state contacts you.

How far back can Utah assess unpaid sales tax?

Utah generally enforces a three-year lookback period for registered filers who miss returns or underreport. However, if you never registered despite having nexus, the lookback period may extend indefinitely, significantly increasing your liability. This unlimited lookback applies when the state determines willful neglect or fraud.