Texas sales tax nexus determines whether your business must collect and remit sales tax in the Lone Star State. Cross the $500,000 threshold, and you’re in, being responsible for collecting tax across one of America’s largest consumer markets.

This is about knowing where you stand. Texas generates nearly $50 billion annually from sales tax, and the Comptroller’s office actively tracks remote sellers. Whether you crossed the threshold yesterday or you’re planning Texas expansion, clarity protects your business from expensive surprises.

Hands Off Sales Tax (HOST) handles the complexity by analyzing your footprint, managing registration, filing returns, and ensuring accurate collection. With over 25 years focused exclusively on sales tax, we navigate Texas’s requirements so you can focus on growth.

What Is Sales Tax Nexus in Texas?

Nexus is the connection between your business and Texas that triggers collection obligations. The Texas Comptroller recognizes two types: physical nexus (offices, warehouses, employees, inventory) and economic nexus (revenue thresholds, regardless of physical presence).

Once nexus exists, you register with the Comptroller, collect 6.25% state tax plus local rates (up to 8.25% combined), and file returns monthly, quarterly, or annually. Texas uses origin-based sourcing for in-state sellers but destination-based for remote sellers, meaning you calculate tax based on your customer’s location.

Non-compliance brings serious consequences: back taxes, penalties reaching 50% of tax due, and interest at 10% annually. The Comptroller conducts regular audits and has intensified pursuit of online sellers since Wayfair.

Texas Economic Nexus Threshold: $500,000

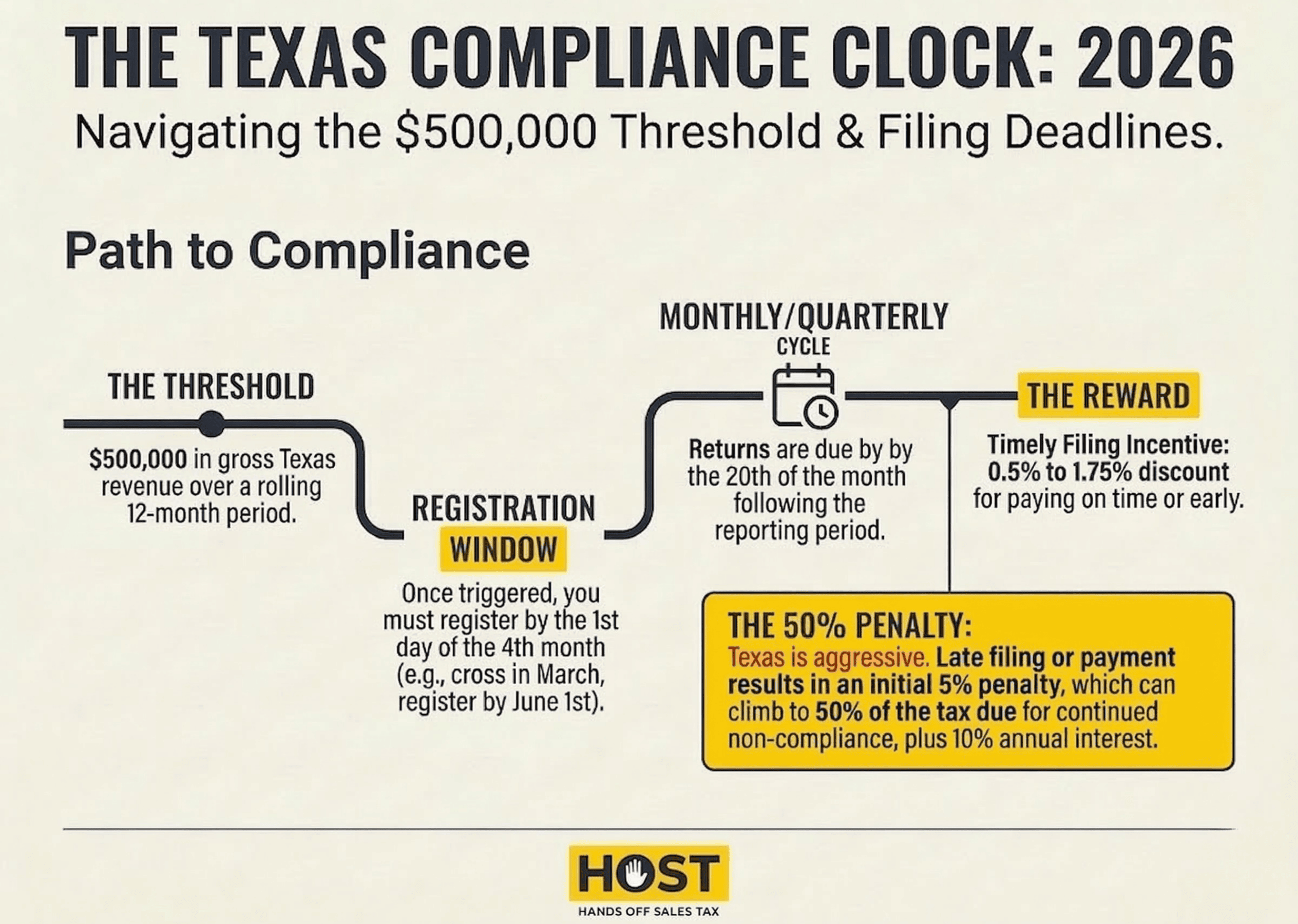

Texas established economic nexus in October 2019 following Wayfair. The threshold: $500,000 in total Texas revenue during any rolling 12-month period.

This includes everything: taxable sales, exempt transactions, wholesale revenue. Hit $500,000 in gross receipts from Texas customers over any 12-month window, and you’ve triggered nexus.

Unlike many states with $100,000 thresholds or transaction counts, Texas uses revenue alone. It’s straightforward: either you’re above $500,000 or you’re not.

The lookback is continuous, not calendar-based. Cross the threshold in March, and you have until the first day of the fourth month to register and begin collecting. For example, exceed $500,000 in March, and you must register by June 1st. You maintain nexus going forward until you stay below $500,000 for a full 12 consecutive months.

Important Exception: Remote sellers who only sell through marketplace facilitators (Amazon, Etsy, eBay) that certify they’re collecting tax on your behalf don’t need their own Texas permit. However, marketplace sales still count toward your $500,000 threshold. If you also make direct sales, you’ll need to register once combined revenue crosses $500,000.

Franchise Tax Warning: Obtaining a Texas sales tax permit also creates franchise tax nexus. Texas’s franchise tax is a separate tax on business gross receipts, potentially adding significant compliance obligations beyond sales tax alone.

HOST’s nexus analysis service examines your sales data to pinpoint exactly when you crossed Texas’s threshold, eliminating guesswork and preventing late registration penalties.

Physical Nexus in Texas: Beyond Economic Thresholds

Physical nexus extends beyond obvious presence. The Comptroller interprets it broadly, capturing activities many remote sellers overlook.

Inventory Storage: Warehousing product in Texas (even temporarily at third-party facilities) creates nexus. Use Amazon FBA and your inventory lands in a Texas fulfillment center? You have physical nexus, regardless of revenue.

Employees and Contractors: Remote employees working from Texas homes establish nexus for your entire business. A single sales rep calling from Houston triggers statewide obligations.

Trade Shows and Events: Displaying products at Austin’s SXSW or Houston trade shows creates temporary nexus. The Comptroller has pursued out-of-state businesses after discovering event participation.

Drop Shipping: Suppliers shipping from Texas locations can create nexus depending on your arrangement and control over inventory.

Affiliate Relationships: Texas-based affiliates generating over $500,000 in referrals annually establish nexus under click-through provisions.

Software Licensing: Licensing software to Texas customers creates nexus, with the receipts from licensing activity triggering obligations.

Event Promotion: Promoting flea markets, craft shows, trade days, or festivals selling taxable items in Texas establishes nexus.

Equipment Leasing: Leasing equipment or tangible personal property to Texas customers creates nexus.

Ownership Relationships: Having 50% or more ownership interest in (or being 50% owned by) another entity with Texas operations, particularly distribution centers, warehouses, or similar locations, can create nexus.

Disaster Relief Exception: Out-of-state businesses entering Texas solely to help with disaster recovery aren’t considered engaged in business and don’t need to register, provided they meet specific requirements under Texas law.

Physical nexus demands immediate collection regardless of revenue. Even $1 in sales combined with physical presence requires registration.

Many businesses discover physical nexus during audits, creating years of liability. HOST identifies all nexus-creating activities upfront, ensuring day-one compliance rather than audit-day surprises.

How to Register for Texas Sales Tax

Once nexus exists, registration is mandatory before collecting tax. Texas issues an 11-digit Texas Taxpayer Number (your sales tax permit identifier).

Registration Steps:

- Create a Webfile account on the Texas Comptroller’s website

- Complete Form AP-201 (Texas Application for Sales and Use Tax Permit) online

- Provide business details: legal name, DBA, structure, FEIN, activities, estimated monthly sales

- Receive your permit within 2-3 weeks

- Display your permit at business locations (though irrelevant for remote sellers)

Required Information:

- FEIN or SSN for sole proprietors

- Legal business name and DBAs

- Business structure (LLC, Corporation, Partnership, Sole Proprietor)

- Physical and mailing addresses

- Business activities description

- Estimated monthly taxable sales

- Owner information (names, addresses, SSNs for 10%+ ownership)

Common Mistakes:

- Misclassifying business type, affecting filing frequency

- Underestimating sales, leading to inappropriate schedules

- Failing to register all inventory locations

- Using entity names that don’t match bank accounts

HOST handles Texas registration completely. Accurate completion, appropriate frequency selection, and Comptroller follow-up to secure your permit quickly.

Texas Sales Tax Rates and Local Jurisdictions

Texas charges a 6.25% state sales tax rate on most retail sales of tangible personal property. However, local jurisdictions like cities, counties, special purpose districts, and transit authorities, can add up to 2% in local sales taxes, creating combined rates as high as 8.25%.

Unlike many states, Texas is an origin-based state for in-state sellers but destination-based for remote sellers. This creates an important distinction:

In-State Sellers: Collect based on business location (origin), charging the rate applicable at your Texas store or warehouse regardless of customer location.

Remote Sellers: Collect based on customer location (destination), charging the combined rate where your customer receives the product.

With 254 counties and hundreds of cities, determining correct rates demands address-level precision. Dallas customers pay 8.25%; someone 15 miles away in a different jurisdiction might pay 7.75%.

Single Local Use Tax Rate Option: Texas offers remote sellers a significant simplification. Instead of tracking hundreds of local jurisdictions, you can elect to charge a single statewide local rate—currently 1.75%—on all Texas sales. This means charging 6.25% (state) + 1.75% (simplified local) = 8% everywhere in Texas.

You must notify the Comptroller to use this election. In-state sellers cannot use this option; it’s exclusively for remote sellers. This dramatically reduces compliance complexity while ensuring you collect sufficient local tax.

Taxable vs. Exempt Items:

Texas taxes most tangible personal property but exempts:

- Groceries and most food items (prepared food is taxable)

- Prescription medications

- Medical devices prescribed by physicians

- Agricultural and timber items

- Manufacturing machinery used directly in production

Remote sellers must configure systems to calculate correct rates per address while applying product-based exemptions. Misconfiguration leads to overcharging (damaging relationships, violating Texas law) or undercharging (creating personal liability for uncollected tax).

HOST’s free Sales Tax Software Review audits your configuration to identify rate errors, incorrect exemptions, and double-taxation from system overlaps.

Texas Sales Tax Filing Requirements

Texas requires regular sales tax return filing based on your assigned frequency: monthly, quarterly, or annually. The Texas Comptroller assigns frequency during registration based on estimated tax liability. New taxpayers are typically assigned monthly or quarterly initially, and the Comptroller may adjust frequency based on actual reported taxes over time.

Filing Frequencies:

- Monthly: Businesses with higher tax liability

- Quarterly: Businesses with moderate tax liability (typically those collecting less than $1,500 in tax per quarter)

- Annually: Businesses with minimal liability (typically under $1,000 annual tax liability, granted to taxpayers with a history of timely filing)

Filing Deadlines:

- Monthly filers: 20th of the month following the reporting period (January sales due February 20th)

- Quarterly filers: 20th of the month following the quarter (Q1 due April 20th)

- Annual filers: January 20th for the prior calendar year

Texas requires electronic filing through Webfile. Report gross sales, taxable sales, exemptions, deductions, tax collected, and credits. Even zero-sales periods require zero returns, and failure to file a zero return triggers a $50 penalty per period.

Timely Filing Incentive: Texas rewards compliance. File and pay on time to claim a 0.5% discount on tax reported. Prepay taxes to earn an additional 1.25% discount, for a combined 1.75% discount. For businesses with significant liability, these discounts add up.

Local Jurisdiction Reporting:

Texas’s local tax structure demands additional complexity. While filing a single state return, you must break out local taxes by jurisdiction, tracking address-level data for every sale. A business with 1,000 monthly Texas transactions might span 50+ local jurisdictions, each requiring separate line-item reporting.

Penalties for Late Filing:

- Late Filing: 5% of tax due if 1-30 days late, plus 5% for each additional 30 days, up to 50% maximum

- Late Payment: 5% if 1-30 days late, plus 5% for each additional 30 days, up to 50% maximum

- Interest: 10% annually on unpaid tax, compounded daily

- Criminal Penalties: Intentional failure can result in criminal charges

The Comptroller aggressively pursues unfiled returns, conducting sweeps to identify unregistered remote sellers and sending assessment notices for estimated tax plus maximum penalties.

HOST manages all Texas filing requirements! Preparing returns on your schedule, ensuring accurate local jurisdiction allocation, and keeping you current without diverting time from your business.

Voluntary Disclosure Agreements in Texas

Operated without collecting Texas tax for months or years? The Texas Comptroller’s Voluntary Disclosure Program offers a compliance path with reduced penalties.

How Texas VDA Works:

Voluntary Disclosure lets businesses come forward before discovery. In exchange for registering and paying back taxes, Texas limits the lookback period and waives most penalties.

Standard Terms:

- Lookback Period: Limited to 4 years (instead of unlimited for unregistered businesses)

- Penalty Waiver: Texas waives penalties entirely for voluntary disclosure

- Interest: 10% annual interest still applies to back taxes

- Anonymity: Initial contact can be anonymous through a representative

- No Trailing Nexus: Texas eliminated trailing nexus requirements—once you properly terminate nexus, you’re not obligated to collect for an additional 12 months

Eligibility:

- Come forward before the Comptroller contacts you

- Must not have a current Texas sales tax permit

- Agree to register and file going forward

The Texas VDA has saved businesses tens of thousands in penalties. Without VDA, audit discoveries face maximum 50% penalties plus interest, potentially doubling liability.

HOST manages the entire Texas VDA process, maintaining anonymity during initial stages, calculating accurate historical liability, negotiating with the Comptroller, and ensuring smooth transition to compliance.

HOST: Your Texas Sales Tax Compliance Partner

Texas compliance demands precision. Every month without proper registration increases exposure. The Comptroller actively pursues remote sellers, and audits often uncover years of obligations.

What HOST Delivers for Texas:

- Texas Nexus Analysis: We analyze your sales data and physical footprint to determine nexus and calculate when obligations began

- Texas Registration: We complete your Texas Application for Sales and Use Tax Permit, ensuring accuracy and appropriate filing frequency

- Ongoing Texas Filings: We prepare and file returns monthly, quarterly, or annually, handling local jurisdiction allocation

- Rate Management: We ensure correct rate calculations for each Texas customer address

- Notice Response: We interpret and respond to Comptroller notices, resolving issues quickly

- Texas Audit Defense: We represent you during audits, organizing documentation and defending your position

- Texas VDA: We manage VDA applications to limit lookback periods and eliminate penalties

We’ve focused 100% on sales tax since 1999. That’s over 25 years helping businesses navigate compliance. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

Ready to Get Texas Compliant?

Whether you’ve just crossed $500,000, you’re unsure about FBA inventory creating nexus, or you need to come forward safely after operating without registration, professional guidance eliminates guesswork and prevents costly mistakes.

Every month without compliance increases exposure. The Comptroller pursues remote sellers aggressively.

Contact HOST today to discuss your Texas situation or schedule a free consultation. We’ll analyze your nexus, handle registration if needed, manage ongoing filings, and ensure correct collection across all Texas jurisdictions.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book to discover common compliance errors and how to avoid them.

Frequently Asked Questions

What is the Texas sales tax nexus threshold for remote sellers?

Texas’s economic nexus threshold is $500,000 in total Texas revenue during any rolling 12-month period. This includes all sales: taxable, exempt, and wholesale combined. Once you exceed this amount, you have until the first day of the fourth month after crossing the threshold to register and begin collecting. For example, cross $500,000 in March, register by June 1st.

Does storing inventory in a Texas fulfillment center create nexus?

Yes. Storing inventory in Texas, including at third-party warehouses or Amazon FBA facilities, creates physical nexus regardless of revenue. Physical nexus requires registration and collection even with minimal Texas sales.

Do I need a Texas permit if I only sell through Amazon or Etsy?

If you exclusively sell through marketplace facilitators that certify they’re collecting Texas tax on your behalf, you don’t need your own Texas permit. However, marketplace sales still count toward your $500,000 threshold. If you make any direct sales (through your own website, for example), you must register once combined revenue crosses $500,000.

How do I register for a Texas sales tax permit?

Register through the Comptroller’s Webfile system by completing Form AP-201. You’ll need your FEIN, business structure details, ownership information, and estimated monthly sales. Texas typically issues permits within 2-3 weeks.

What happens if I’ve had Texas nexus but haven’t been collecting sales tax?

You face back-tax liability plus penalties and interest. The Comptroller can assess up to four years of back taxes with penalties reaching 50% plus 10% annual interest. A Voluntary Disclosure Agreement can limit lookback periods and eliminate penalties if you come forward before contact.

How often do I need to file Texas sales tax returns?

Filing frequency depends on tax liability: monthly for businesses with higher liability, quarterly for those typically collecting less than $1,500 in tax per quarter, or annually for minimal liability (under $1,000 annually with timely filing history). The Comptroller assigns frequency during registration.

Is Texas an origin-based or destination-based state for sales tax?

Texas is origin-based for in-state sellers (charge tax based on your business location) but destination-based for remote sellers (charge tax based on customer location). Remote sellers must calculate tax using each customer’s specific address, including local jurisdictions.

Alternatively, remote sellers can elect to use Texas’s Single Local Use Tax Rate (currently 1.75%) instead of tracking individual jurisdictions, simplifying compliance significantly.