Receiving a notification from the Texas Comptroller of Public Accounts is rarely the highlight of a business owner’s week. In the past, you might have felt like you were just a random number in a drawing. However, in 2026, audits are no longer just “bad luck.” With the state now using sophisticated IRS data-matching and real-time marketplace analysis, audits have become a precision tool used to ensure every dollar of the 8.25% is accounted for.

Navigating this process can feel like walking through a minefield of “60-day letters” and shifting legal standards. But here is the good news: the rules have changed in your favor, too. From the 2025 “Sufficient Records” standard to the newly established Fifteenth Court of Appeals, businesses now have more protections than ever—provided they know how to use them.

At Hands Off Sales Tax (HOST), we believe you should focus on scaling your business, not decoding the tax code. This guide demystifies the audit lifecycle from the first notice to the final assessment, giving you the “insider” knowledge needed to protect your revenue and maintain your peace of mind.

What is a Texas Sales Tax Audit?

A Texas sales tax audit ensures businesses comply with state tax laws by accurately reporting and remitting sales taxes. Conducted by the Texas Comptroller of Public Accounts, these audits are a key tool to maintain tax compliance and fairness across industries.

A sales tax audit examines a business’s financial records to verify if the correct amount of sales tax has been reported and paid. The goal is to identify discrepancies, whether due to unintentional errors or non-compliance. This process helps protect public revenue and ensures equitable taxation.

Texas sales tax audits operate under a 4-year statute of limitations from the tax due date (34 Texas Administrative Code 3.339). However, critical exceptions apply:

- If tax is understated by 25% or more, there is no statute of limitations

- In cases of fraud or failure to file, the Comptroller can assess taxes indefinitely

- Businesses participating in the Voluntary Disclosure Agreement program benefit from a capped 4-year lookback period, regardless of how long they’ve had nexus in Texas

The Texas Comptroller oversees the auditing process, issuing notices, reviewing records, and assessing taxes where discrepancies are found. The office also provides guidance and resources for businesses to better understand their obligations.

Triggers for a Sales Tax Audit

Sales tax audits don’t happen randomly; they’re often initiated by specific triggers that suggest potential non-compliance. Understanding these triggers can help businesses proactively address issues and avoid penalties.

| Trigger Type | Threshold / Red Flag | Unique Insight |

| Gross Receipts Mismatch | 15% variance vs. IRS | Often caused by “netting” sales (reporting only profit) instead of gross. |

| Exemption Ratios | > 40% of total revenue | Triggers an automatic request for “Certificate Verification.” |

| Digital Nexus | > $500,000 in sales | Remote sellers are now the #1 growth area for Texas audits. |

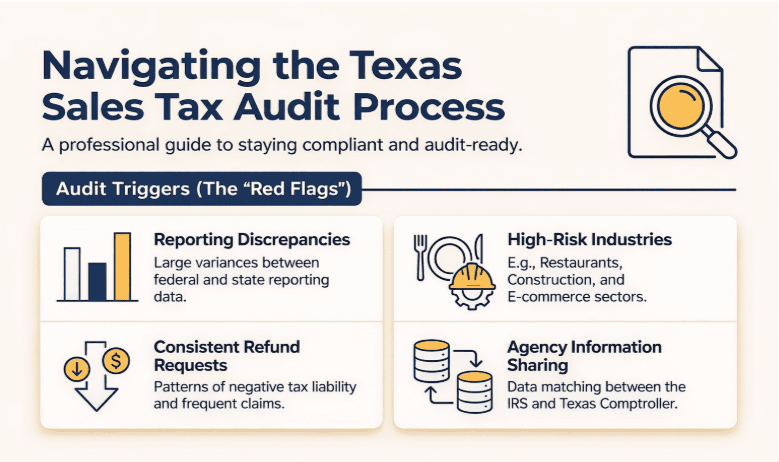

Key Factors That May Prompt an Audit

Significant Discrepancies in Reported Sales:

Large variances between reported sales and expected industry averages or patterns can raise red flags. Specifically, the Comptroller’s office looks for:

- Negative tax liability patterns: Consistently reporting negative amounts or requesting refunds quarter after quarter

- Sharp revenue drops: Year-over-year sales declines of 20% or more without clear economic explanation

- Local Rate Misalignment: With over 60 new local rate changes taking effect on January 1, 2026, businesses shipping to multiple Texas jurisdictions are at high risk for “under-collection” flags.

- Information Sharing (IRS Data): The Comptroller now uses real-time data matching between federal Form 1120 and Texas sales tax returns. A variance of 15% or more between federal gross receipts and Texas taxable sales is a primary audit trigger.

Industries with High Non-Compliance Rates:

The Texas Comptroller targets certain sectors with historically higher instances of underreported taxes. Based on audit frequency data, these industries face elevated scrutiny:

- Restaurants and bars (audit rate approximately 1 in 8 businesses): Common issues include underreporting cash sales, improper handling of catering vs. dine-in taxes, and misclassifying alcoholic beverage sales

- Construction contractors (audit rate approximately 1 in 10): Frequent errors involve failing to collect tax on materials used in lump-sum contracts and misunderstanding the taxability of repair vs. improvement work

- Online retailers and e-commerce: With economic nexus rules, Texas actively audits remote sellers who may have crossed the $500,000 threshold but failed to register

- Auto repair shops: Often misapply tax to parts vs. labor or fail to collect tax on shop supplies

- Hair salons and spas: Commonly underreport retail product sales or misclassify service vs. product revenue

Random Selection:

While targeted audits dominate, approximately 5-10% of Texas sales tax audits are randomly selected to ensure overall compliance across all industries and business sizes. These statistical samples help the Comptroller maintain a baseline understanding of compliance rates.

Information Sharing Between Agencies:

The Comptroller receives data from multiple sources that can trigger audits:

- IRS data matching: Automatic comparisons between federal gross receipts (Form 1120 or Schedule C) and Texas sales tax returns

- Sales tax permit applications: New registrations from businesses that should have registered years earlier based on their incorporation date or business start

- Bankruptcy filings: Courts notify the Comptroller, prompting review of pre-bankruptcy tax compliance

- Other state revenue departments: Interstate data sharing reveals businesses operating in multiple states who may have Texas obligations

Public Tips or Complaints:

The Comptroller maintains a tax fraud hotline and online reporting system. Common complaint scenarios include:

- Competitor reports: A business notices a competitor not charging sales tax and reports them, triggering an investigation

- Disgruntled employees: Former staff members report cash-skimming or double-books to authorities

- Customer complaints: Shoppers notice they weren’t charged tax and report the business

- Whistleblower reports: Individuals with direct knowledge of tax evasion can file detailed complaints

A Houston electronics store faced an audit after multiple customers reported purchasing items without sales tax being collected. It was because the store owner had been pocketing the tax amounts instead of remitting them to the state.

By addressing these factors proactively, businesses can reduce their audit risk substantially. Regular internal reviews, accurate record-keeping, and proper tax calculation systems are your best defense.

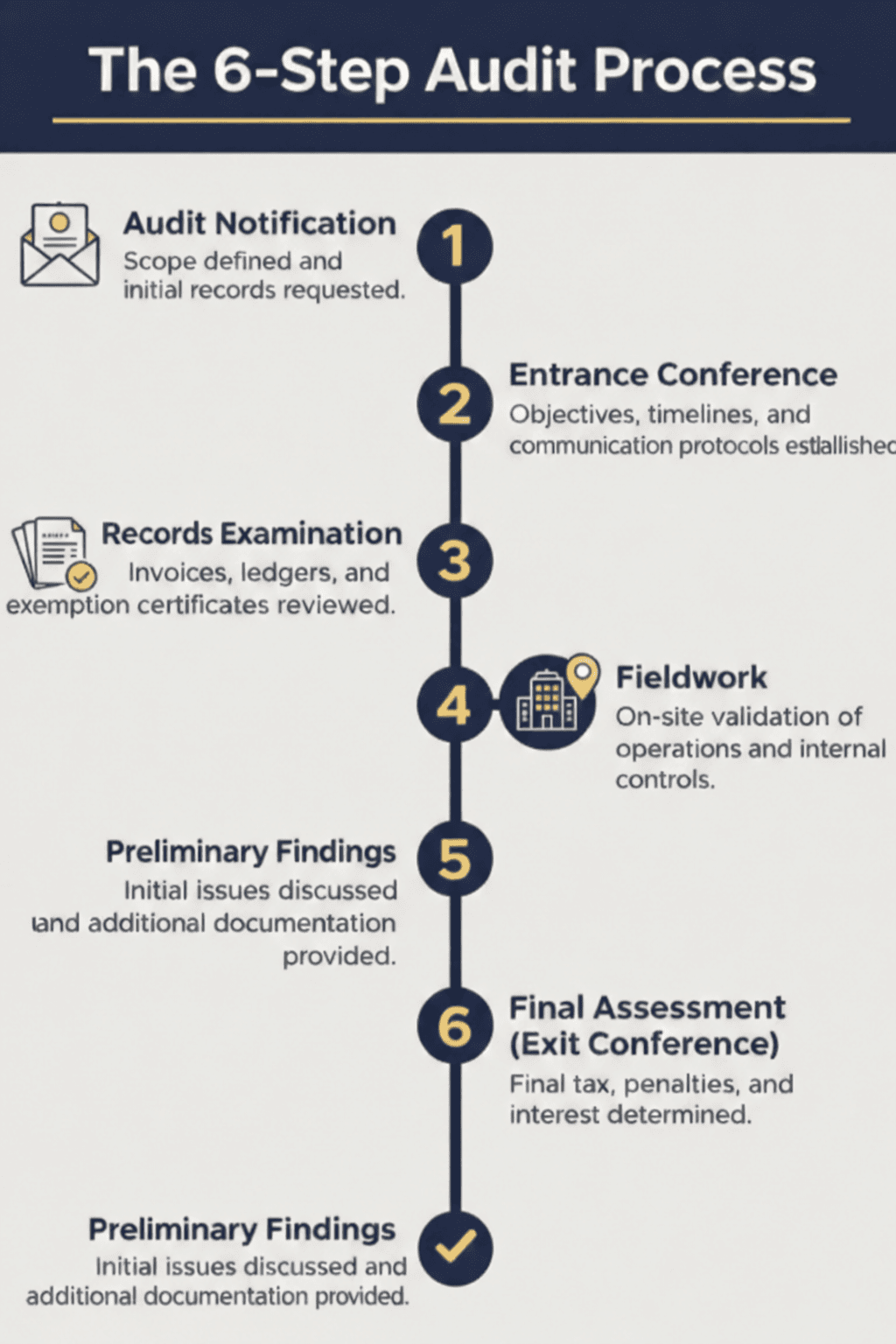

The Texas Sales Tax Audit Process: A Step-by-Step Guide

The Texas sales tax audit process is a structured evaluation conducted by the Comptroller of Public Accounts. For 2026, the process places a heavier emphasis on digital documentation and formal preliminary conferences.

- Notification & Initial Setup

- The Audit Notice: You will receive a formal “Notice of Routine Tax Audit.” This letter identifies the tax types (Sales/Use/Franchise), the period under review, and the assigned auditor.

- The Audit Questionnaire (Form 00-750): This is now a critical first step. You must complete and return this questionnaire within 30 days. It asks about your accounting software, business locations, and key personnel.

- Statute of Limitations: Standard audits cover 4 years, but auditors may ask you to sign a Statute Extension Agreement. Use caution here—consult with a pro before waiving your limitation rights.

- Entrance Conference (Initial Meeting)

- Defining the Audit Plan: This meeting is no longer just an introduction. The auditor will present a formal Audit Plan detailing whether they will perform a “detail audit” (every transaction) or “sampling” (statistical projections).

- Internal Control Review: Expect deep questions about your POS system and how you handle tax-exempt sales. This is your chance to explain any unique business nuances before the state begins pulling data.

- Examination of Records: The “Sufficient” Standard

- The 2025 Standard Shift: Under Texas Tax Code § 111.0041, the state can no longer demand “contemporaneous” records (those created at the exact time of the transaction). You only need to provide “sufficient” evidence. If original invoices are missing, you can now use bank statements, ledgers, or third-party reports to prove tax was paid.

- Standard Document List:

- Sales invoices and purchase receipts.

- Valid Exemption/Resale Certificates.

- Federal Income Tax Returns (Forms 1120 or 1065).

- General Ledgers and Bank Statements.

- Fieldwork & Sampling Notification

- Sampling Procedures: If the auditor uses sampling, they must issue a formal Notification of Sampling Procedures, usually after testing roughly 25% of the sample. You have the right to challenge the “representativeness” of their sample at this stage.

- Data Verification: Auditors now prefer electronic data (Excel/CSV) over paper files to speed up the reconciliation with your filed returns.

- Preliminary Findings & The “60-Day Letter”

- Reviewing Schedules: The auditor will provide “Audit Schedules” listing every transaction they believe is taxable.

- The 60-Day Rule: If you are missing exemption certificates, the state will issue a 60-Day Letter. This is a hard deadline. You have exactly 60 days to hunt down missing certificates from customers. Anything received after day 60 is legally inadmissible in a later hearing.

- Exit Conference & Final Assessment

- The Final Report: The auditor presents the final tax, penalty, and interest amounts.

- Penalty Waivers: You can request a “Penalty Waiver” at this meeting. Success usually depends on your past filing history and how cooperative you were during the audit.

Dispute Resolution (The Pre-Appeal Path) If you disagree with the findings, 2026 protocols offer two internal “checkpoints” before you hit a formal courtroom:

- Reconciliation Conference: A meeting with the auditor’s supervisor to resolve factual errors.

- Independent Audit Review (IAR) Conference: A neutral third-party reviewer from the Comptroller’s office evaluates the dispute to avoid a formal hearing.

Taxpayer Rights and Responsibilities During an Audit

During a Texas sales tax audit, understanding your rights and responsibilities is vital for a smooth and fair process. These are governed by the Texas Taxpayer Bill of Rights and recent 2025 legislative amendments.

1. Your Rights

- Right to Fair and Equitable Treatment: You have the right to professional and courteous treatment. Auditors are legally prohibited from being rewarded or promoted based on the amount of tax they assess (See: 96-265 Texas Taxpayer Bill of Rights).

- Right to Privacy and Confidentiality: Your financial and operational data is protected. Unauthorized disclosure by Comptroller staff is a violation of state law.

- Right to Representation: You have the absolute right to engage a CPA, attorney, or tax consultant to represent you. In fact, most business owners prefer to have a “buffer” between the auditor and their daily operations.

- Right to Contest a Decision: If you disagree with an audit’s outcome, you have the right to request an Independent Audit Review (IAR) before the final assessment is issued, or file a formal protest (See: Contesting Disagreed Audits).

2. Your Responsibilities

- Obligation to Provide “Sufficient” Records: Per the 2025 amendment to Texas Tax Code § 111.0041, you are no longer strictly held to “contemporaneous” (created-at-the-time) records. However, you must provide sufficient documentation—such as bank statements or third-party reports—to substantiate your claims.

- Cooperation with Auditor Requests: You must provide requested access to your books and premises. Failure to cooperate can lead to the Comptroller estimating your tax liability, which is almost always higher than the actual amount due.

- Timely Communication: You must respond to the Audit Questionnaire and any “60-Day Letters” regarding missing exemption certificates within the legal timeframes to avoid losing your right to claim those exemptions.

Preparing for a Sales Tax Audit

Proactive preparation is your best defense against “audit creep”—where an auditor begins expanding the scope of their investigation because of messy records.

- Maintain Digital Accessibility: Texas auditors now prioritize electronic data. Ensure your general ledgers and sales journals can be exported in Excel or CSV format (See: Comptroller Records FAQ).

HOST Tip: Need to export 4 years of messy data? HOST’s automated systems do the heavy lifting for you, ensuring your files are auditor-ready in minutes. - Validate Exemption Certificates: Every sale you didn’t charge tax on must be backed by a valid Resale or Exemption Certificate. If you are missing these, you have a 60-day window once the audit begins to retrieve them.

- Retain Records for 4 Years: While the standard lookback is 48 months, keep records longer if an administrative hearing or refund claim is pending.

- Reconcile Sales to Tax Returns: Monthly reconciliations between your POS system and your filed tax returns are the easiest way to spot “Tax Collected but Not Remitted” errors—a major red flag for auditors.

- Update Tax Rates for 2026: Ensure your systems reflect the January 1, 2026 local rate changes for any jurisdictions where you have physical or economic nexus.

- Perform Internal “Mini-Audits”: Spot-check 10% of your exempt sales each quarter to ensure the certificates on file are filled out correctly and haven’t expired.

- The “One Point of Contact” Rule: Designate one person to speak with the auditor. This prevents conflicting information from being given by different employees.

Partner with HOST: When you use HOST’s Audit Defense, we become your “One Point of Contact,” insulating your team from the stress of direct auditor questioning. - Document Handling: Train staff never to give original documents to an auditor to take off-site. Auditors may view originals at your office or take copies, but the originals should remain in your possession.

The Managed Audit Program: An Alternative Approach

The Managed Audit Program allows businesses to conduct a self-review of their tax compliance under the guidance of the Texas Comptroller.

- Request Timing: You must request a managed audit within 60 days of receiving your Audit Notification Letter (See: Managed Audit Policy).

- Statute Waiver: You will likely be required to sign a statute waiver extending the audit period by 90 days beyond the completion timeline.

- Incentives: If no fraud is found, the Comptroller may waive 100% of penalties and a significant portion of interest.

- Eligibility: Your business must be current on all filings and have a “clean” history (no excessive estimated returns).

Common Pitfalls and How to Avoid Them

- Misclassification of Digital Services: With 2026’s new Ancillary Test for SaaS, misclassifying software maintenance vs. data processing will be one of the main causes of assessments this year.

- Expired Exemption Certificates: Accepting a certificate that hasn’t been updated since 2022 is an automatic “fail” in a 2026 audit.

HOST Defense: Avoid the 60-day trap with HOST’s proactive certificate management—we verify your customers’ certificates so you don’t have to. - Jurisdictional Errors: Using a flat 8.25% rate when shipping to a location with a new 2026 transit district overlay will trigger a discrepancy.

- Over-Sharing Records: Volunteering documents outside the requested period or “extra” spreadsheets can unintentionally lead an auditor to a new area of liability.

Closing the Audit Chapter with Confidence

Navigating a Texas sales tax audit in 2026 is no longer just about keeping paper receipts—it’s about staying ahead of digital nexus rules and aggressive data matching. Don’t leave your business’s financial health to chance.

Whether you’ve just received an audit notice or want a proactive 2026 Nexus Analysis, HOST is the trusted partner you need to make sales tax truly “hands-off.” Talk to a HOST Sales Tax Specialist Today

FAQ: 2026 Audit Edition

Q: What is the “Sufficient Records” standard?

A: As of September 2025, Texas has modernized its record-keeping requirements under Texas Tax Code § 111.0041. Previously, auditors often demanded “contemporaneous” records—meaning documents created at the exact moment of the transaction. The new “Sufficient” standard is more flexible; if original invoices are lost, you can now use “reconstructed” data such as bank statements, 1099s, or third-party vendor reports to prove tax compliance. This shift prevents businesses from being unfairly penalized for minor documentation gaps, provided they can substantiate their numbers through other verifiable means.

Q: Does the $2.65M Franchise Tax threshold affect me?

A: Yes, significantly. For reports due after January 1, 2026, the No-Tax-Due threshold has increased to $2.65 million. If your revenue falls below this, you no longer file a Franchise Tax Report. However, this creates a new challenge during a sales tax audit: because the auditor doesn’t have a Franchise Report to cross-reference, they will rely more heavily on your federal Form 1120 or Schedule C to verify gross receipts. Any discrepancy between your federal income and your Texas sales tax filings will likely become the primary focus of their investigation.

Q: What is the “Ancillary Test”?

A: The “Ancillary Test” is a critical 2026 update to 34 TAC § 3.330 regarding software and digital services. Instead of looking purely at the “essence of the transaction,” auditors now look at whether the software component is merely “ancillary” to a non-taxable service. For example, if you provide a professional consulting service that uses a proprietary platform to deliver data, the state may now tax the entire contract if the software isn’t proven to be secondary. This is the #1 audit risk for SaaS and tech-enabled service providers in 2026, as the “burden of proof” for non-taxability has increased.

Q: How does the “60-Day Letter” impact my audit?

A: The “60-Day Letter” is the most dangerous deadline in a Texas audit. If an auditor finds sales where you didn’t charge tax but lack a valid Exemption Certificate, they will issue this formal notice. You have exactly 60 days from the date on the letter to acquire missing certificates from your customers. This is a “hard” statutory deadline; certificates received on day 61 are legally inadmissible in any future appeal or hearing. If you fail to meet this window, the transactions become taxable by default, often resulting in massive assessments that could have been avoided with proactive document management.

Q: Can I get my audit penalties waived in 2026?

A: Penalty waivers are not guaranteed, but they are common for businesses that show “Reasonable Diligence.” The Comptroller reviews factors like your audit history, the complexity of the law, and whether you collected but failed to remit the tax (the latter is a “deal-breaker” for waivers). Under 2026 guidelines, being cooperative and having “sufficient” records significantly increases your chances. It is often best to request a waiver during the Exit Conference. If denied, you can still pursue it through an Independent Audit Review (IAR) or by showing you took immediate corrective steps, such as hiring a professional compliance service like HOST.

Q: What happens if my audit uncovers a “Gross Error”?

A: A “Gross Error” occurs when the tax you actually owe exceeds what you reported by 25% or more. This is a critical threshold because it triggers an exception to the standard 4-year statute of limitations, allowing the Comptroller to audit your records as far back as they choose—sometimes indefinitely. Additionally, a 25% error rate usually disqualifies you from interest waivers in a Managed Audit. If you suspect a significant reporting gap, participating in a Voluntary Disclosure Agreement (VDA) before an audit begins is the only way to cap your lookback period and avoid this “statute-free” exposure.

Q: Is there a way to settle my audit without going to court?

A: Yes. In 2026, the most effective “off-ramp” is the Independent Audit Review (IAR) Conference. This is a neutral review conducted by a non-auditor within the Comptroller’s office. It’s designed to resolve factual or legal disagreements before they escalate to the Fifteenth Court of Appeals. The IAR is faster and cheaper than formal litigation and is your best opportunity to present “reconstructed” data under the new Sufficient Records standard. To utilize this, you must notify your auditor of your intent to request an IAR typically on or before the 61st day after receiving your preliminary findings.