Understanding South Dakota’s economic nexus threshold matters for every e-commerce business selling into the state. Since the landmark 2018 Supreme Court decision in South Dakota v. Wayfair, this threshold has reshaped sales tax compliance nationwide, creating obligations for remote sellers who’ve never set foot in South Dakota.

The rule is straightforward: $100,000 in gross sales to South Dakota customers in the current or previous calendar year. Cross that line, and you’re required to register, collect, and file. Regardless of physical presence.

For businesses juggling compliance across dozens of states, tracking where obligations begin creates constant pressure. That’s where Hands Off Sales Tax (HOST) steps in, handling nexus analysis, registration, and ongoing filings so compliance doesn’t consume your day.

What Is Economic Nexus?

Economic nexus establishes a state’s authority to require sales tax collection based solely on economic activity within its borders. Before Wayfair, states could only impose collection duties on businesses with physical presence like stores, warehouses, employees, or inventory.

The June 21, 2018 ruling changed everything, though enforcement didn’t begin until November 1, 2018. States gained authority to require out-of-state sellers to collect sales tax once they meet specific thresholds. This shift eliminated the competitive advantage online retailers held over brick-and-mortar stores and dramatically expanded state tax collection capabilities.

South Dakota’s law became the constitutional model because it included safeguards the Supreme Court found reasonable: a substantial threshold, prospective application, and simplified compliance through Streamlined Sales Tax membership, allowing businesses to register across multiple states through a single system.

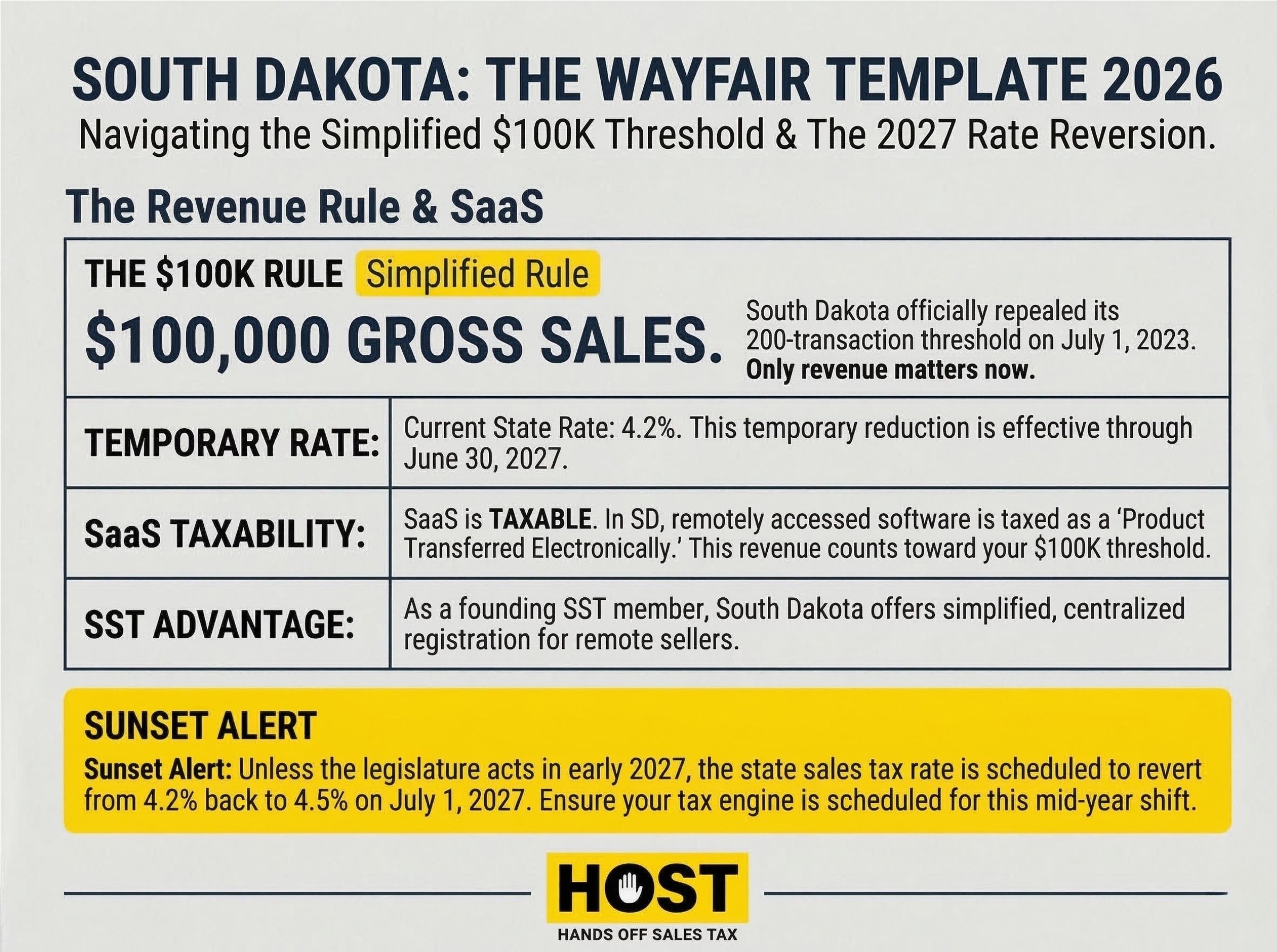

South Dakota’s Threshold: Simple, But Strict

South Dakota’s economic nexus threshold cuts through complexity:

$100,000 in gross sales to South Dakota customers in the current or previous calendar year.

Key characteristics make this straightforward:

- No transaction count: Unlike some states, South Dakota eliminated its 200-transaction threshold in July 2023. You’re tracking one metric, and that’s revenue.

- Gross sales measurement: The $100,000 includes all sales into South Dakota, whether taxable or exempt. Even tax-exempt items count toward the threshold. This includes electronically transferred products like software downloads, digital goods, and SaaS.

- Calendar year lookback: South Dakota measures the threshold on a calendar year basis. Exceed $100,000 in either the current year or previous year, and nexus applies.

- No small seller exception: Once you hit the threshold, size doesn’t matter. Solo entrepreneurs and mid-market retailers face identical obligations.

The practical effect: Sell $100,001 worth of goods to South Dakota customers in 2024, and you have economic nexus in 2025, even if your 2025 sales drop significantly.

Why South Dakota Created This Standard

South Dakota faced severe revenue loss from online sales. The state has no income tax and relies heavily on sales tax to fund education, infrastructure, and public services. As e-commerce exploded, the inability to collect from remote sellers created budget shortfalls and competitive disadvantages for local businesses.

In 2016, South Dakota passed legislation specifically designed to challenge the Quill precedent: the 1992 Supreme Court case requiring physical presence for sales tax obligations. The law imposed economic nexus at $100,000 or 200 transactions, deliberately inviting legal challenge.

The gamble worked. In South Dakota v. Wayfair, Inc. (2018), the Supreme Court ruled 5-4 that physical presence was no longer required, upholding South Dakota’s economic nexus law. The decision praised South Dakota’s threshold as “reasonable” and “not retroactive,” creating a template other states quickly adopted.

Within two years, 45 states with sales tax implemented their own economic nexus laws, most mirroring South Dakota’s $100,000 threshold.

Calculating If You’ve Met the Threshold

Determining whether you’ve crossed South Dakota’s threshold requires tracking all sales delivered to South Dakota addresses:

- Pull sales data by destination state: Review transaction records and identify all orders shipped to South Dakota customers.

- Sum gross revenue: Total the dollar value of all South Dakota sales within the calendar year. Include shipping charges if billed separately. Exclude returns and refunds.

- Include all products: Count both taxable and exempt sales. Even exclusively non-taxable items count toward the $100,000 threshold.

- Monitor continuously: Check South Dakota sales quarterly at minimum. Approaching $80,000 mid-year likely means you’ll cross the threshold before year-end.

- Apply the lookback: Exceeding the threshold in either the current or previous calendar year creates nexus.

Common mistake: Businesses sometimes track only taxable sales, missing that the threshold includes exempt sales. A company selling $120,000 of non-taxable medical supplies into South Dakota still has economic nexus and must register.

HOST’s nexus analysis service eliminates guesswork, analyzing your complete sales footprint to identify exactly where you’ve met thresholds.

What Happens When You Exceed the Threshold

Crossing South Dakota’s threshold creates immediate obligations:

Registration Timeline

Registration timing depends on when you cross the threshold:

- Current year: If you exceed $100,000 during the current calendar year, you must register for your next transaction.

- Previous year: If you met the threshold in the previous calendar year, you must register by the start of the following calendar year.

You must register for a South Dakota sales tax license through the South Dakota Department of Revenue. South Dakota doesn’t charge a registration fee, and licenses remain active until you close your business.

As a Streamlined Sales Tax (SST) member state, South Dakota also allows registration through the Streamlined Sales Tax Registration System, enabling businesses to register across multiple SST states simultaneously.

Collection

Once registered, you must collect South Dakota sales tax on all taxable sales to South Dakota customers. South Dakota’s state rate is 4.2% (temporarily reduced from 4.5%, reverting June 30, 2027), with local jurisdictions adding up to 2% for combined rates reaching 6.2% in some areas.

Calculating correct rates requires destination-based sourcing, applying the rate where the customer receives the product.

Filing and Remittance

South Dakota assigns filing frequency based on tax liability:

- Monthly filers: Collecting $400+ per month

- Quarterly filers: Collecting $100-$399 per month

- Annual filers: Collecting less than $100 per month

Returns are due the 20th of the month following the reporting period. Missing deadlines triggers 10% penalties or $10 minimum, plus 1.5% monthly interest on unpaid balances.

HOST manages every stage, handling registration, calculating correct rates, filing returns on schedule, and responding to notices.

Common Misconceptions

“No Physical Presence Means No Tax Obligation”

This was true before 2018. Wayfair eliminated physical presence requirements. Economic activity alone ($100,000 in sales) creates nexus.

“The Threshold Is $100,000 in Taxable Sales”

The threshold measures gross sales, including exempt products. A business selling $150,000 of non-taxable groceries into South Dakota has nexus and must register.

“I Can Wait Until Next Year”

Economic nexus applies based on when you cross the threshold. Hit $100,000 in November, and you must register promptly for the next transaction. If you met the threshold in the previous year, you had until January 1 to register. Delaying beyond these timelines creates retroactive liability and audit exposure.

“Marketplace Sellers Don’t Need to Worry”

If you sell exclusively through platforms like Amazon, the marketplace facilitator collects and remits sales tax on your behalf (effective March 1, 2019). However, if you have any direct sales through your own website, at events, or wholesale, you must track those separately and register if they exceed $100,000.

How South Dakota Compares to Other States

South Dakota’s law became the national template, but states implemented variations:

Threshold amounts: Most states adopted $100,000, but Alabama uses $250,000, Texas uses $500,000, and California requires $500,000.

Transaction counts: Many states include both revenue and transaction thresholds. States like New York require meeting both criteria. South Dakota dropped its transaction count, simplifying compliance.

Measurement periods: South Dakota uses calendar year with a lookback. Other states use rolling 12-month periods, previous 12 months, or current year only.

The variation across states makes multi-state compliance exponentially complex. Tracking 45+ different thresholds, measurement periods, and filing schedules consumes massive time and creates error risk.

HOST’s comprehensive nexus analysis evaluates your sales against every state’s unique criteria, ensuring you’re collecting where required without over-registering.

Best Practices for Managing South Dakota Nexus

Implement sales tax automation: Tools like TaxJar or Avalara calculate correct rates and track nexus thresholds. However, software requires proper configuration because misconfigured systems create expensive errors.

Review sales quarterly: Don’t wait until year-end to discover you crossed the threshold months ago. Quarterly reviews enable proactive registration.

Document exemption certificates: When selling to South Dakota businesses claiming resale or other exemptions, maintain valid exemption certificates.

Consider voluntary disclosure: If you discover past nexus, South Dakota offers a Voluntary Disclosure Program that limits lookback periods and can abate penalties.

HOST’s sales tax software review service audits your automation configuration to identify costly errors before they trigger audits.

The Wayfair Decision’s Broader Impact

South Dakota v. Wayfair didn’t just create nexus in South Dakota, it unleashed nationwide economic nexus. Within 18 months, every state with sales tax adopted economic nexus laws. The compliance landscape transformed from managing physical presence in a handful of states to monitoring thresholds across 45+ jurisdictions simultaneously.

This administrative burden is precisely why most businesses eventually seek professional help. The cost of internal management, which can be 30+ hours monthly according to industry surveys, far exceeds outsourcing to specialists.

HOST: Your Partner for South Dakota Compliance

South Dakota’s economic nexus threshold represents just one of 45+ state obligations you’re managing. Each state has unique rules, thresholds, rates, filing schedules, and registration requirements.

What HOST Delivers:

Nexus Analysis: We analyze your complete sales footprint to determine exactly where you’ve met thresholds, including South Dakota.

Sales Tax Registration: We handle South Dakota registration and all other state registrations, managing paperwork and communications.

Automated Filing: We file your South Dakota returns monthly, quarterly, or annually as required, along with all other state obligations.

Audit Defense: We’re your battle-tested partner in resolving South Dakota sales tax audits.

Voluntary Disclosure: If you discover past South Dakota nexus you didn’t address, we file voluntary disclosures to limit lookback periods and minimize penalties.

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate post-Wayfair complexity.

Ready to Simplify South Dakota Compliance?

South Dakota’s economic nexus threshold might seem straightforward. Just $100,000 in sales. But managing compliance across South Dakota and 44 other states creates overwhelming complexity.

Contact HOST today to discuss your South Dakota sales tax needs and discover how we handle the complexity so you can focus on growth. You handle the sales, we handle the tax.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is South Dakota’s economic nexus threshold?

South Dakota’s economic nexus threshold is $100,000 in gross sales to South Dakota customers in the current or previous calendar year. There’s no transaction count—only the revenue threshold matters.

Do exempt sales count toward the $100,000 threshold?

Yes. South Dakota’s threshold includes all sales, taxable and exempt. Even if you sell exclusively non-taxable products, those sales count toward determining whether you’ve met the threshold.

When must I register after crossing the threshold?

Registration timing depends on when you cross the threshold. If you exceed $100,000 during the current calendar year, register for your next transaction. If you met the threshold in the previous calendar year, you must register by the start of the following year. South Dakota expects timely registration. Delaying creates retroactive liability and potential penalties.

Does the marketplace facilitator law eliminate my obligation?

The marketplace facilitator law means platforms like Amazon collect tax on your behalf for marketplace sales. However, you still have nexus based on total sales volume. If you have direct sales (outside marketplaces) exceeding $100,000, you must register and collect on those transactions.

What happens if I don’t register after meeting the threshold?

Failing to register after meeting South Dakota’s economic nexus threshold creates sales tax liability, penalties, and interest. South Dakota can audit and assess back taxes, plus 10% penalty on unpaid amounts. Voluntary disclosure programs can limit exposure if you proactively address past obligations.

How does HOST help with South Dakota economic nexus?

HOST analyzes your sales data to determine if you’ve met South Dakota’s threshold, handles registration with the South Dakota Department of Revenue, calculates and collects correct rates, files returns on schedule, and responds to state notices. Managing complete compliance so you can focus on running your business.