Understanding South Carolina sales tax nexus determines whether your business must collect and remit sales tax in the state. One misstep: a warehouse you didn’t track, an employee working remotely, crossing the economic threshold, creates compliance obligations many e-commerce sellers discover only after a notice arrives from the South Carolina Department of Revenue (SCDOR).

South Carolina enforces both physical and economic nexus rules. Physical presence triggers obligations immediately. Economic nexus activates once you exceed $100,000 in gross revenue during the previous or current calendar year. Missing either threshold means potential back taxes, penalties, and audit exposure.

Hands Off Sales Tax (HOST) specializes in South Carolina nexus analysis, registration, and ongoing compliance. We’ve helped businesses navigate these requirements for over 25 years—ensuring you collect in the right states and file on time.

What Is Sales Tax Nexus?

Sales tax nexus is the connection between your business and a state that creates a tax collection obligation. The connection can be physical (office, warehouse, employee) or economic (sales volume). Once nexus exists, you must register, collect tax from South Carolina customers, and remit it to the SCDOR.

South Dakota v. Wayfair (2018) fundamentally changed nexus rules. Before Wayfair, only physical presence triggered obligations. Now, economic activity alone like selling to customers in a state, can require collection, even without physical presence.

South Carolina adopted economic nexus immediately after Wayfair, setting its threshold at $100,000 in gross revenue. Remote sellers, marketplace sellers, and out-of-state businesses operating entirely online face the same obligations as brick-and-mortar retailers with South Carolina storefronts.

South Carolina Economic Nexus Rules

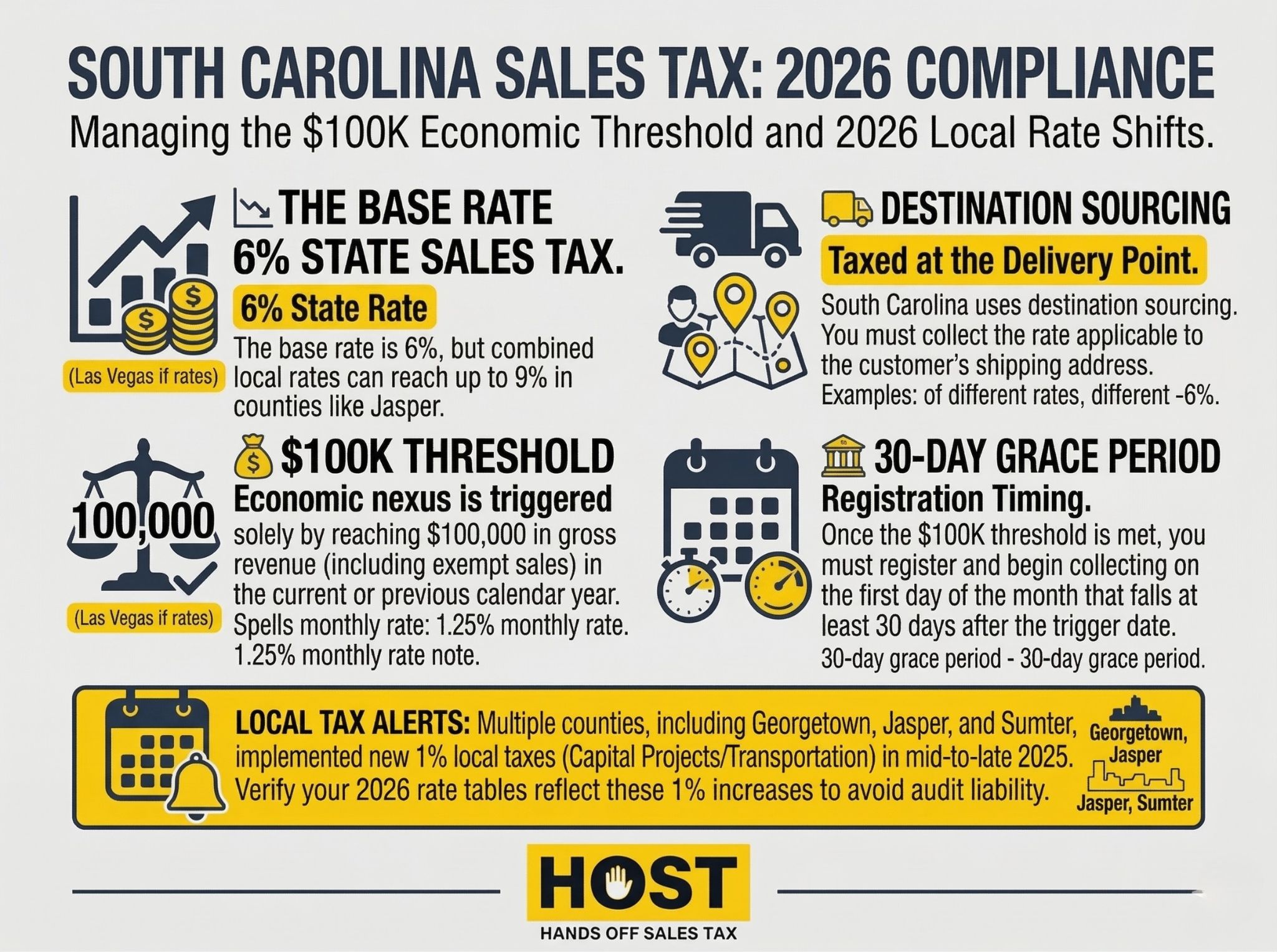

South Carolina’s economic nexus threshold is $100,000 in gross revenue from sales delivered into the state during the previous or current calendar year. There is no transaction count threshold. Only the dollar amount matters.

How the $100,000 Threshold Works

The SCDOR monitors cumulative gross revenue from sales to South Carolina customers. Once your total exceeds $100,000 in either the current or previous calendar year, nexus is established.

Example: Your business generated $95,000 in South Carolina sales in 2024. In January 2025, you make another $6,000 in sales. You’ve now exceeded $100,000 and triggered economic nexus. Registration and collection obligations begin immediately.

Gross revenue includes all sales delivered to South Carolina addresses:

- Taxable sales

- Exempt sales (wholesale, resale certificates, exempt products)

- Shipping charges included in the sale price

The threshold uses gross revenue, not taxable revenue. Even if half your sales are exempt, those sales count toward the $100,000 threshold. This catches many businesses off guard because they assume only taxable sales matter, but South Carolina counts everything.

When Collection Obligations Begin

Once you exceed $100,000, you must register and begin collecting sales tax on the first day of the month that starts at least 30 days after exceeding the threshold.

Example: You exceed $100,000 on March 15, 2025. You must register and begin collecting by May 1, 2025.

However, if you exceeded the threshold based on prior year sales, you should already be collecting. Many businesses discover they crossed the threshold months or years ago, creating retroactive liability.

HOST’s nexus analysis service identifies exactly when you triggered economic nexus in South Carolina and every other state, eliminating guesswork and preventing costly compliance gaps.

Physical Nexus in South Carolina

Physical nexus exists when your business maintains a tangible presence in South Carolina. Physical nexus triggers immediately. There’s no threshold or waiting period.

Office or Facility

Maintaining an office, retail location, warehouse, or distribution center in South Carolina establishes nexus. This includes third-party logistics providers storing your inventory.

Many e-commerce sellers unknowingly trigger nexus through third-party warehouses. If you use a 3PL in South Carolina to store inventory, you have physical nexus. Even if you’ve never visited the state.

Employees and Representatives

Having employees, contractors, or sales representatives working in South Carolina creates nexus:

- Remote employees living in South Carolina

- Sales representatives soliciting orders in the state

- Independent contractors performing services on your behalf

The rise of remote work post-2020 created unexpected nexus for many businesses. Hiring a single remote employee in South Carolina establishes physical presence, triggering collection obligations immediately.

Inventory Storage

Storing inventory in South Carolina creates nexus, regardless of whether you own the facility. This applies to Fulfillment by Amazon (FBA) inventory in South Carolina warehouses, third-party logistics providers, and drop-shipping arrangements.

Amazon’s inventory distribution system moves FBA inventory across multiple states without seller control. If Amazon stores your products in a South Carolina fulfillment center (even temporarily) you have physical nexus.

Marketplace Facilitator Law

South Carolina requires marketplace facilitators like Amazon, Etsy, eBay, and Walmart to collect and remit sales tax on behalf of third-party sellers once the platform exceeds $100,000 in gross revenue from South Carolina sales.

This law, enacted April 26, 2019, shifts collection responsibility to the marketplace platform. If you sell exclusively through marketplaces that collect tax on your behalf, you don’t need a separate South Carolina retail license for those sales.

However, marketplace sales still count toward your personal economic nexus threshold. If you generate $75,000 through your own website and $30,000 through Amazon (where Amazon collects the tax), you’ve exceeded the $100,000 threshold. You must register and collect tax on your direct sales, even though Amazon handles marketplace sales.

If you make both marketplace and direct sales, you’ll need to track and report them separately. Marketplace sales appear on your return as sales where tax was collected by the facilitator.

South Carolina Sales Tax Rates and Collection

South Carolina imposes a 6% state sales tax rate. Additionally, counties and municipalities levy local sales taxes ranging from 1% to 3%, creating combined rates between 6% and 9%.

South Carolina is destination-based for sales tax purposes. You must collect tax based on the customer’s location (delivery address), not your business location. This means calculating the correct rate for every South Carolina ZIP code where you ship products.

South Carolina offers an annual sales tax holiday during the first weekend in August (Friday through Sunday), exempting clothing, computers, and school supplies from state and local sales tax. While this benefits consumers, businesses must track eligible items and apply exemptions correctly during the holiday period.

With over 100 local tax jurisdictions, manual rate determination is impractical. Sales tax automation software like TaxJar or Avalara can calculate rates, but misconfiguration leads to errors: overtaxing customers, missing required local taxes, or double-taxing due to system overlaps.

HOST offers a Free Sales Tax Software Review to audit your configuration and identify costly mistakes before they impact your bottom line or trigger audits.

How to Register for a South Carolina Sales Tax Permit

Once nexus is established, registration is mandatory. South Carolina requires a Retail License, obtained through the SCDOR’s MyDORWAY online portal.

The registration process involves creating a MyDORWAY account, completing the Business Tax Application (Form SCTC-111), providing your Federal Employer Identification Number, describing your business activities, and identifying all South Carolina locations.

Processing typically takes 7-10 business days. South Carolina doesn’t charge a registration fee for the Retail License, though there’s a one-time $50 fee per retail location.

Common Registration Mistakes

Many businesses make critical errors during registration:

- Incorrect Start Date: Reporting the wrong collection start date can trigger penalties for uncollected tax

- Misclassified Products: Failing to identify exempt products correctly leads to over-collection or under-collection

- Incomplete Location Information: Not disclosing all physical locations creates compliance gaps

HOST handles South Carolina registration, completing paperwork, following up with the SCDOR, and ensuring accurate filing frequency assignment, eliminating the stress and errors of DIY registration.

South Carolina Filing Requirements

South Carolina assigns filing frequency based on your tax liability. New businesses are typically assigned monthly filing by default. Quarterly or annual filing frequencies require written approval from the SCDOR.

Returns are due the 20th of the month following the reporting period. South Carolina doesn’t offer an automatic extension. Late filings incur penalties of 5% of tax due per month (maximum 25%) plus 0.5% interest per month.

Even if you collect no tax during a period, you must file a zero return. Failing to file (even with no liability) triggers penalties and potentially revokes your license.

Managing sales tax across multiple states consumes 30+ hours monthly, and that’s time that generates no revenue but creates significant liability risk if done incorrectly.

HOST’s filing services handle monthly, quarterly, or annual South Carolina returns, including local and special district returns, ensuring everything stays current while you focus on growth.

What to Do If You’ve Missed South Carolina Nexus

Discovering past nexus creates immediate stress. Many businesses panic, wondering whether to register immediately or wait, hoping the SCDOR won’t notice.

Ignoring the problem is the worst approach. South Carolina actively pursues non-compliant remote sellers through data sharing with marketplaces, neighboring states, and third-party data providers. Waiting only compounds penalties and interest.

Voluntary Disclosure Agreements (VDAs)

South Carolina offers VDAs that allow businesses to come forward voluntarily, limiting lookback periods and abating penalties. A properly structured VDA typically limits liability to three years and eliminates most penalties.

Without a VDA, South Carolina can assess up to eight years of back taxes plus full penalties. The difference can be tens of thousands of dollars.

HOST’s VDA services manage the process from initial contact to final agreement, protecting your interests while resolving past liabilities efficiently.

HOST: Your Partner for South Carolina Nexus Compliance

South Carolina’s nexus rules, combined with 45 other states’ requirements, create overwhelming complexity for e-commerce businesses. Missing triggers, misunderstanding thresholds, or filing incorrectly creates significant financial and legal risk.

What HOST Delivers

Nexus Analysis: We analyze your sales data, physical presence, and remote employees to determine exactly where you have South Carolina nexus and when it was triggered.

Sales Tax Registration: We handle South Carolina Retail License applications, including all paperwork, follow-up, and communication with the SCDOR.

Automated Filing: We prepare and file South Carolina returns monthly, quarterly, or annually based on your assigned frequency, including all required schedules and local tax calculations.

Notice Management: We interpret and respond to SCDOR notices, protecting you from penalties while resolving issues efficiently.

Audit Defense: We organize documentation, communicate with auditors, and defend your position throughout South Carolina sales tax audits.

VDA Support: We file voluntary disclosure agreements to limit lookback periods and abate penalties when past nexus is discovered.

We’ve focused exclusively on sales tax for over 25 years. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

You handle the sales, we handle the tax.

Ready to Get Compliant in South Carolina?

South Carolina nexus (whether physical or economic) creates immediate compliance obligations. Understanding when you triggered nexus, registering correctly, and filing on time protects your business from audits, penalties, and unexpected tax bills.

Whether you’re expanding into South Carolina, discovered past nexus, or simply want peace of mind that you’re collecting correctly across all states, professional help eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss your South Carolina nexus situation and discover how we handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the economic nexus threshold in South Carolina?

South Carolina’s economic nexus threshold is $100,000 in gross revenue from sales delivered into the state during the previous or current calendar year. There is no transaction count requirement. Only the dollar threshold matters.

Do I need to register if I only make wholesale sales in South Carolina?

Yes. Once nexus is established (physical or economic), you must register for a Retail License even if you only make wholesale sales. While wholesale sales themselves aren’t taxable, registration is required, and you must collect tax on any retail sales to South Carolina customers.

How does South Carolina treat marketplace sales for nexus purposes?

Sales made through marketplace facilitators like Amazon, Etsy, or Walmart count toward your $100,000 economic nexus threshold. However, the marketplace collects and remits tax on those sales, so you don’t collect tax twice. You still must monitor total sales (marketplace + direct) to determine if you’ve exceeded the threshold.

Can I register for South Carolina sales tax retroactively?

You can register after triggering nexus, but you’ll owe back taxes, penalties, and interest for the period between when nexus was established and when you began collecting. A Voluntary Disclosure Agreement can limit lookback periods and abate penalties, significantly reducing liability.

What happens if I don’t register after triggering nexus?

South Carolina can assess back taxes for up to eight years, plus penalties of up to 25% and interest of 0.5% per month. The SCDOR actively pursues non-compliant sellers through data sharing and audits. Voluntary compliance or a VDA dramatically reduces financial exposure.

Does having FBA inventory in South Carolina create nexus?

Yes. Storing inventory in South Carolina through Fulfillment by Amazon or any third-party logistics provider creates physical nexus, triggering immediate registration and collection obligations. Amazon’s inventory distribution moves products across states, so monitoring where your FBA inventory is stored is critical for multi-state compliance.

How do marketplace sales affect my nexus threshold?

Sales made through marketplace facilitators (Amazon, Etsy, eBay, Walmart) count toward your $100,000 economic nexus threshold. If you sell $75,000 through your website and $30,000 through Amazon, you’ve exceeded the threshold. However, you only need to register and collect tax on your direct sales. The marketplace handles collection for platform sales.

What items are exempt from South Carolina sales tax?

Common exemptions include groceries (unprepared food items), prescription medications, certain manufacturing machinery and equipment, and agricultural products. However, many exemptions apply only to state sales tax, not local taxes. During the annual August sales tax holiday, clothing, computers, and school supplies are also exempt from both state and local tax.