Most businesses worry about underpaying sales tax with the audits, the penalties, the interest that compounds like snow gathering on a roof. But there’s a quieter problem that costs just as much: overpayment. Money remitted to states that never should have left your accounts in the first place.

Sales tax overpayment occurs when a business remits more tax to a state or local authority than legally required. Unlike underpayment,where liability is obvious and states come calling, overpayment often goes unnoticed because returns were filed “correctly” according to internal systems that were themselves misconfigured from the start.

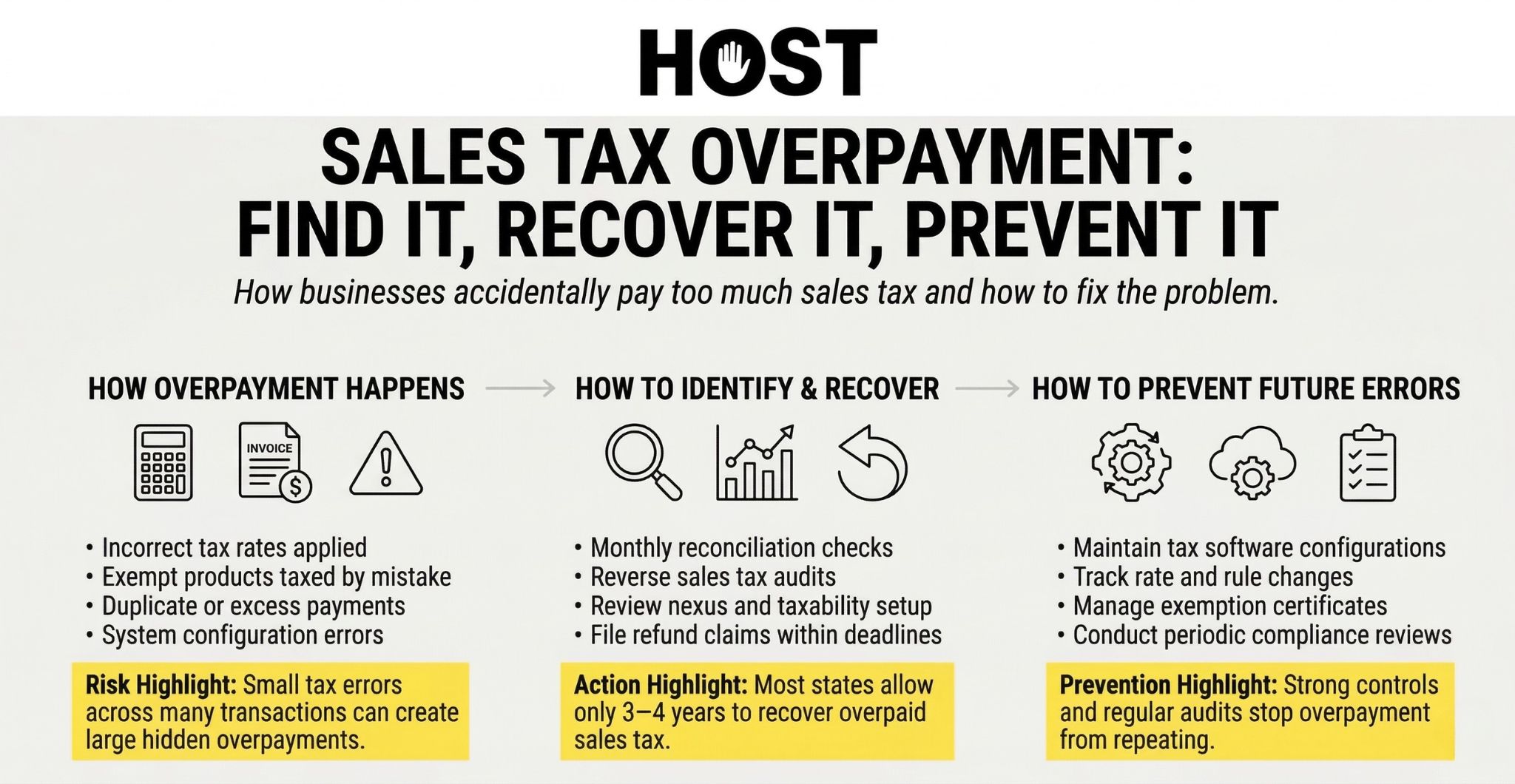

Sales tax overpayment typically arises from systemic errors, not one-off mistakes, meaning small discrepancies can compound into significant recoverable amounts over multiple filing periods or states. A 2% rate error applied to thousands of transactions across three years doesn’t announce itself, it just quietly drains your working capital.

If you suspect your business has been overpaying sales tax across multiple states, HOST offers reverse audit services that identify recoverable amounts and manage the refund claim process end-to-end.

What Is Sales Tax Overpayment?

At its core, overpayment means remitting more than you legally owe. But the mechanisms are more subtle than simple arithmetic errors.

Overpayment is not limited to tax collected from customers. It also includes tax remitted on exempt sales, duplicate payments, and tax paid where no nexus or obligation existed. You can overpay by collecting correctly but remitting to the wrong jurisdiction. You can overpay by treating wholesale transactions as retail. You can overpay by letting your marketplace facilitator and your own systems both remit on the same sales.

The fundamental issue is that sales tax systems operate on trust. States don’t proactively review whether you paid too much, only whether you paid too little. If your return says you owe $10,000 and you remit $12,000, they’ll cash the check and thank you for your diligence.

Common Causes of Sales Tax Overpayment

Understanding where overpayments originate helps you audit your own processes and identify potential recovery opportunities.

Incorrect Tax Rate Application (Jurisdictional Drift)

Sales tax rates vary across more than 14,000 U.S. jurisdictions. Errors occur when systems apply destination-based rates incorrectly, default to state-level rates only, or fail to update special district or city surcharges.

A business shipping to Denver might apply Colorado’s base state rate of 2.9% when the actual combined rate (including city, county, and special district taxes) should be 8.81%. Alternatively, systems might apply the highest rate in a state uniformly, overtaxing transactions in lower-rate jurisdictions.

High-risk signal: Rate consistency across invoices for customers in different ZIP+4 locations. If every Colorado sale shows the same rate regardless of city, you’re likely misconfigured.

Misclassified Products or Services

Overpayment frequently results from over-taxing exempt or conditionally exempt items. Common categories include clothing and footwear (exempt in several states), groceries and dietary supplements (complex partial exemptions), digital goods and SaaS (taxability varies dramatically by state), and bundled service offerings (where service components may be exempt while tangible components are taxable).

Misclassification often stems from platform defaults that treat all SKUs as taxable. E-commerce platforms like Shopify or WooCommerce require manual product tax code configuration. If you skip this step, everything becomes taxable by default.

High-risk signal: Uniform tax treatment across product categories in states with partial exemptions. If you sell both clothing and electronics in New York and both show tax collected, you’re likely overtaxing the clothing.

Software Configuration and Platform Overlap Errors

Even sophisticated platforms rely on accurate setup. Overpayment commonly occurs when wholesale transactions are treated as retail (because exemption certificates weren’t properly uploaded), marketplace facilitator rules are ignored (resulting in double remittance), or ERP, accounting, and tax engines overlap remittance logic.

The last issue is particularly insidious. A business might have Avalara calculating tax, Shopify collecting it, QuickBooks recording it, and a manual spreadsheet reconciling it, with each system making slightly different assumptions about what’s owed. When systems don’t talk to each other cleanly, overpayment becomes almost inevitable.

High-risk signal: Tax collected and remitted through multiple systems for the same transaction stream. If you’re manually adjusting numbers between platforms every filing period, errors are compounding.

Returns, Credits, and Adjustments Not Properly Applied

Customer refunds require corresponding tax reversals. Overpayments arise when credits are not applied to the correct filing period, refunds occur after returns are filed (creating a mismatch), or tax is refunded to customers but not recovered from the state.

Many businesses process customer refunds promptly but forget to claim the corresponding tax credit on their next sales tax return. Over time, these unclaimed credits accumulate into substantial overpayments.

High-risk signal: Sales returns exceeding tax credits claimed on returns. If your refund volume is significant but your sales tax returns show minimal credit activity, you’re leaving money on the table.

Duplicate or Excess Remittances

Duplicate payments often occur during system migrations (when old and new systems both process the same period), payment resubmissions after filing errors (where the correction adds to rather than replaces the original payment), or manual “catch-up” payments overlapping automated debits.

These errors are particularly common when businesses switch from manual filing to automated systems or change accounting software mid-year.

High-risk signal: Multiple payments tied to the same filing period or confirmation number. Review your state payment history! If you see two debits for the same month, one is likely recoverable.

How to Identify Sales Tax Overpayment

Detection requires both routine monitoring and periodic deep audits. Here’s how to uncover overpayments systematically.

Monthly Reconciliation (Non-Negotiable)

Reconcile three critical relationships every month: sales tax collected versus remitted, filed returns versus bank debits, and platform reports versus accounting ledgers.

This practice prevents multi-year accumulation. A $500 monthly discrepancy becomes a $6,000 annual problem becomes an $18,000 three-year problem. Early detection keeps recovery simple.

Configuration and Product Taxability Review

Audit your nexus settings (are you filing in states where you no longer have nexus?), product tax codes (are exempt items properly flagged?), exemption logic (are resale certificates being applied?), and marketplace facilitator toggles (is your system aware of who’s collecting tax?).

Key insight: Correct filings do not equal correct liability. You can file every return on time, remit every dollar your system calculates, and still be overpaying by 15% if your system is misconfigured.

Multi-State Transaction Pattern Review

Overpayments spike in businesses operating across multiple destination-based states, states with partial exemptions, and states with frequent rate changes.

Economic nexus compliance without proper taxability analysis is a major overpayment driver. Businesses often register in new states to comply with economic nexus thresholds, then immediately start overtaxing because they apply blanket taxability assumptions rather than researching state-specific exemptions.

Rate Change Monitoring Failures

States update rates quarterly or annually. Overpayments occur when systems update late (you’re using last quarter’s higher rate), update incompletely (state rate changes but local rates don’t), or apply changes retroactively (creating confusion about which rate applies to which transaction).

Staying current requires either dedicated monitoring or professional rate management that tracks changes across all active jurisdictions.

Reverse Sales Tax Audit (Professional Methodology)

A reverse audit examines multi-year filings, exemption eligibility, rate accuracy, and duplicate remittances. Unlike a state audit where examiners look for underpayment, a reverse audit identifies where you’ve been too generous.

This process often uncovers recoverable overpayments businesses assumed were unrecoverable. Many businesses think “we already filed and paid, it’s too late” when in reality they’re well within the statute of limitations for refund claims.

If you operate in multiple states and suspect systematic overpayment, HOST can conduct a comprehensive reverse audit to quantify recoverable amounts before filing any claims.

The Sales Tax Refund and Credit Recovery Process

Once you’ve identified overpayment, recovery follows a state-specific process with strict requirements and deadlines.

Statute of Limitations (Know the Clock)

Most states allow 3–4 years for refund claims, measured from either the return due date or payment date (varies by state). Some states are more generous. California allows four years, while others like Texas use stricter limits.

Missed deadlines permanently forfeit refunds. Money you overpaid four years and one day ago is gone forever, regardless of how clearly you can prove the error.

Documentation Standards (What States Actually Expect)

Typically required documentation includes filed returns (proving what you reported), proof of payment (canceled checks, bank statements, or state payment confirmations), transaction-level detail (showing what was sold, to whom, and at what rate), invoices and exemption certificates (supporting any exemption claims), and recalculation worksheets (demonstrating the correct tax versus what you paid).

Key insight: Insufficient documentation is the leading cause of denial, not ineligibility. You might legitimately be owed $50,000, but if you can’t prove it with the right paperwork, the state will deny your claim.

Refund vs. Credit (Strategic Choice)

Some states allow you to choose between a cash refund or a credit against future tax liability. The choice matters for cash flow and compliance efficiency.

Refunds return money to your bank account, improving liquidity. Credits reduce future payment obligations, which works well if you have ongoing liability in that state but provides no value if you’ve closed operations there or no longer have nexus.

If you’re winding down operations in a state, always choose refund. If you’re continuing to operate and file, credits can simplify compliance by reducing what you owe going forward.

Claim Submission and Validation

Submission methods vary by state: some use online portals, others require paper filings, and a few accept email submissions. Each state has its own forms, procedures, and review timelines.

Important: Incomplete claims may not toll the statute of limitations. If you file a claim missing required documentation, some states treat it as though you never filed, meaning the clock keeps running toward your deadline.

Processing, Follow-Up, and State Requests

Processing times range from weeks to months depending on claim complexity and state workload. States may request additional documentation, clarifications, or affirmations under penalty of perjury.

During this phase, responsiveness matters. Delayed responses to state inquiries can extend processing times or result in denial. Many businesses file claims and then ignore follow-up requests, forfeiting legitimate refunds through inattention.

Managing refund claims across multiple states while running your business is challenging. HOST handles the entire process, from claim preparation through state correspondence to final recovery.

Multi-State and Marketplace Facilitator Complications

Marketplace facilitator laws shift collection responsibility to platforms like Amazon, Etsy, or eBay, but do not eliminate reconciliation risk. Overpayments occur when sellers and facilitators both remit (double payment on the same sales), refunds are processed inconsistently (seller refunds customer, facilitator doesn’t adjust remittance), or facilitator reports do not align with seller records (creating confusion about what was actually collected and remitted).

Multi-state recovery requires jurisdiction-specific procedures and tracking. A claim in California follows different rules than one in Texas. You need to know which states allow online filing, which require notarization, which accept combined multi-period claims, and which demand separate filings for each period.

The complexity multiplies when your overpayment spans multiple states and multiple years. A comprehensive recovery strategy requires coordinating claims across jurisdictions while maintaining documentation standards that satisfy the strictest state in your portfolio.

When Professional Assistance Becomes Justified

Professional recovery is typically warranted when you’re operating in 3+ states (each with unique procedures), processing high transaction volumes (where small percentage errors become large dollar amounts), managing marketplace sales (requiring facilitator reconciliation), recoverable amounts exceed internal resource cost (the math has to work), or claims span multiple filing periods (increasing documentation complexity).

Attempting DIY recovery on a $5,000 single-state, single-period overpayment might make sense. Pursuing $50,000 across seven states over three years while running your business rarely does.

Firms like Hands Off Sales Tax (HOST) manage identification, documentation, filing, and state correspondence end-to-end. They know which states audit refund claims aggressively, which accept email submissions, which require original signatures, and how to structure claims to maximize approval likelihood.

Preventing Future Sales Tax Overpayments

Recovery is good. Prevention is better. Here’s how to eliminate systemic overpayment going forward.

Tax Software With Ongoing Oversight

Automation reduces risk, but only when actively maintained. Tax calculation software must be configured correctly, updated regularly, and monitored for accuracy. Don’t assume your platform is perfect just because it’s sophisticated.

Monthly Reconciliation Controls

Embed review into close procedures. Make sales tax reconciliation a non-negotiable part of your month-end checklist, just like bank reconciliation or accounts receivable aging.

Rate and Rule Change Monitoring

Subscribe to state notices and platform updates. States don’t always announce changes prominently, so you might need systems that track them proactively.

Exemption Documentation Discipline

Poor documentation defeats recovery. Maintain organized exemption certificate files, validate certificates before accepting them, and ensure your systems apply exemptions correctly at the point of sale.

Periodic Reverse Audits

Prevent silent accumulation by conducting annual or biannual reverse audits. Even with good controls, small errors creep in. Catching them early keeps recovery simple and prevents statute expiration.

How HOST Simplifies Overpayment Recovery and Prevention

Sales tax overpayment recovery requires deep multi-state expertise, meticulous documentation, and persistent state follow-up. Between varying statutes of limitations, documentation standards, and claim procedures, managing recovery internally often costs more than the refunds justify.

Hands Off Sales Tax (HOST) specializes in both identifying overpayments and implementing controls that prevent future errors. From comprehensive reverse audits through claim filing and state negotiation, HOST manages the entire process while you focus on operations.

Whether you’re recovering from a system migration gone wrong or simply want to audit years of filings for potential overpayments, HOST provides the expertise and persistence required to maximize recovery across all jurisdictions.

Frequently Asked Questions (FAQ)

How long do sales tax refunds take?

Typically 6–12 weeks for straightforward single-state claims, longer for multi-year or multi-state claims that require additional documentation or state review. Complex claims involving marketplace facilitators or exemption certificate validation can extend to 6+ months.

Processing times vary dramatically by state. Some states like Wyoming process claims within 30 days. Others like California can take 120+ days even for simple claims. Filing complete, well-documented claims reduces processing time significantly.

Need help navigating multi-state refund timelines? HOST tracks claim status across all jurisdictions and handles state follow-up requests proactively.

Can I recover sales tax from prior years?

Yes, within statute limits usually 3–4 years from the later of the return due date or payment date. Each state sets its own statute of limitations for refund claims.

For example, if you overpaid on your Q4 2021 return filed in January 2022, you typically have until January 2025 or 2026 to file a refund claim, depending on the state. Once that deadline passes, the overpayment becomes unrecoverable regardless of documentation quality.

Some states have shorter windows. Missouri allows only three years. California allows four. Knowing your specific deadlines is critical, and they run independently in each state where you’ve overpaid.

Can states audit refund claims?

Yes. Refund claims often trigger review, which is why documentation matters so critically. States treat large refund claims with the same scrutiny they apply to auditing potential underpayments.

The state may request transaction-level detail, exemption certificates, invoices, shipping records, and detailed explanations of how you calculated the overpayment. They may examine whether you properly applied exemptions, used correct rates, and followed sourcing rules.

If your documentation is insufficient or your methodology is flawed, the state will deny all or part of the claim. This is why professional assistance often yields better recovery rates. Experts know what states expect and structure claims accordingly.

Is a credit better than a refund?

It depends on your circumstances. Credits improve compliance efficiency by reducing future payment obligations automatically. They work well when you have ongoing liability in that state and want to simplify future filings.

Refunds improve cash flow by returning money to your operating accounts. They’re essential when you no longer have nexus in that state, when you need the capital for other purposes, or when you’re uncertain about future sales volume in that jurisdiction.

If you’re continuing operations in the state and expect similar or higher liability going forward, credits often make sense. If you’re winding down operations, closing locations, or have eliminated nexus, always choose refund.

Can overpayment claims be denied even if tax was overpaid?

Yes. Documentation and procedural errors are common denial reasons, often more common than substantive ineligibility. States deny claims for missing required forms, insufficient transaction detail, expired statutes of limitations, failure to respond to state inquiries, or mathematical errors in recalculations.

You might legitimately be owed $100,000, but if you file the wrong form, miss a required signature, or fail to provide itemized transaction listings, the state will deny your claim. Procedural precision matters as much as substantive correctness.

This is why professional claim preparation typically achieves higher approval rates and faster processing because experts know exactly what each state requires and structure submissions accordingly.

How do I know if overpayments exist?

Monthly reconciliation and reverse audits reveal discrepancies that suggest overpayment. Start by comparing sales tax collected (from your sales records) versus sales tax remitted (from your filed returns and payment records).

If you consistently remit more than you collect, you’re either improperly configured or processing exempt transactions as taxable. Review your product taxability settings, examine whether you’re remitting in states where you no longer have nexus, and check for duplicate payments.

A comprehensive reverse audit examines transaction-level detail across multiple years and states, identifying specific overpayment sources and quantifying recoverable amounts before you invest time in filing claims.

Uncertain whether overpayments justify recovery efforts? Contact HOST for a no-obligation assessment that quantifies potential recovery across all states where you file.

What happens if I discover overpayments after the statute of limitations expires?

Once the statute expires, refunds become unrecoverable through normal channels. The money is permanently lost unless you can demonstrate extraordinary circumstances that justify equitable relief, which states rarely grant.

However, credits for overpayments discovered outside the statute period can sometimes be applied if you can document the error occurred within a filing period that remains open for adjustment. State rules vary significantly on this issue.

The key lesson: conduct regular reverse audits to identify overpayments while they’re still recoverable. Waiting until you’re cleaning out old files or preparing to close operations often means discovering money you can no longer claim.

Do marketplace facilitator laws affect overpayment recovery?

Yes, significantly. When marketplace facilitators collect and remit tax on your behalf, overpayment recovery becomes more complex because you must coordinate with the facilitator rather than claiming refunds directly.

If you and the facilitator both remitted tax on the same sales (double payment), you’ll need detailed facilitator reports proving they already remitted before states will refund your duplicate payment. If the facilitator overcollected tax, you may need to work through the facilitator’s refund process rather than filing state claims directly.

Additionally, some states require facilitators to handle all refund claims related to marketplace sales, meaning you can’t file direct claims even when you identify overpayments. Understanding who has refund authority in each state is critical for marketplace sellers.

Can I file refund claims for exempt sales where I incorrectly collected tax?

Yes, but the process differs depending on whether you remitted the tax to the state. If you collected tax on an exempt sale but haven’t yet remitted it, simply don’t include that amount on your next return and refund the customer.

If you already remitted the tax, you can file a refund claim; but you may need to prove you refunded the customer first. Some states require affidavits confirming customer refunds before approving your claim. Others allow you to keep refunds if sufficient time has passed and customer refunds are no longer feasible.

The key is maintaining documentation: proof the sale qualified for exemption (exemption certificates, product taxability rules, statute citations), proof you collected and remitted tax, and proof you refunded customers if required by state law.

Should I amend returns or file separate refund claims?

It depends on the state and the nature of the error. Some states prefer or require amended returns that correct the original filing. Others require separate refund claim forms. Still others allow either method but process one faster than the other.

Generally, if the error is simple (rate miscalculation, data entry error) and occurred in a recent period, amended returns work well. If the error is complex, spans multiple periods, or involves exemption eligibility rather than calculation mistakes, dedicated refund claims with supporting documentation are typically more appropriate.

Unsure which approach maximizes recovery in your specific situation? HOST evaluates each overpayment and determines the optimal filing strategy for each state and circumstance.