Consulting services exist in a complex tax landscape where what’s exempt in one state may be fully taxable in another. Unlike income taxes that operate uniformly at the federal level, sales tax rules vary dramatically across all 50 states and their individual jurisdictions. This complexity makes consulting service sales tax one of the most confusing areas of business taxation in America today.

The fundamental challenge for consultants is that taxability depends on three critical factors: the state where the service is delivered, the specific type of consulting service provided, and how the service is classified for tax purposes. A consultant providing the same service to clients in different states may face completely different tax obligations based on where those clients are located.

If you’re navigating multi-state consulting obligations and need clarity on where you owe tax, HOST offers comprehensive nexus analysis and compliance support tailored to service-based businesses.

Understanding Consulting Service Taxability

Sales tax on professional services remains one of the most misunderstood areas of state taxation. Most business owners understand that physical products are taxable, but the rules governing service taxation (especially consulting) are far less intuitive.

The core issue is that states take fundamentally different approaches to taxing services. Some states exempt services entirely unless specifically enumerated as taxable. Others tax services by default unless specifically exempted. And a handful of states impose no sales tax at all.

For consultants, this means the same strategic advice, market research, or business analysis might be tax-free in one state and fully taxable in another. Understanding which category your state falls into is the critical first step in compliance.

The State-by-State Taxability Framework

Understanding how states approach service taxation is essential for compliance. There are three distinct categories of states:

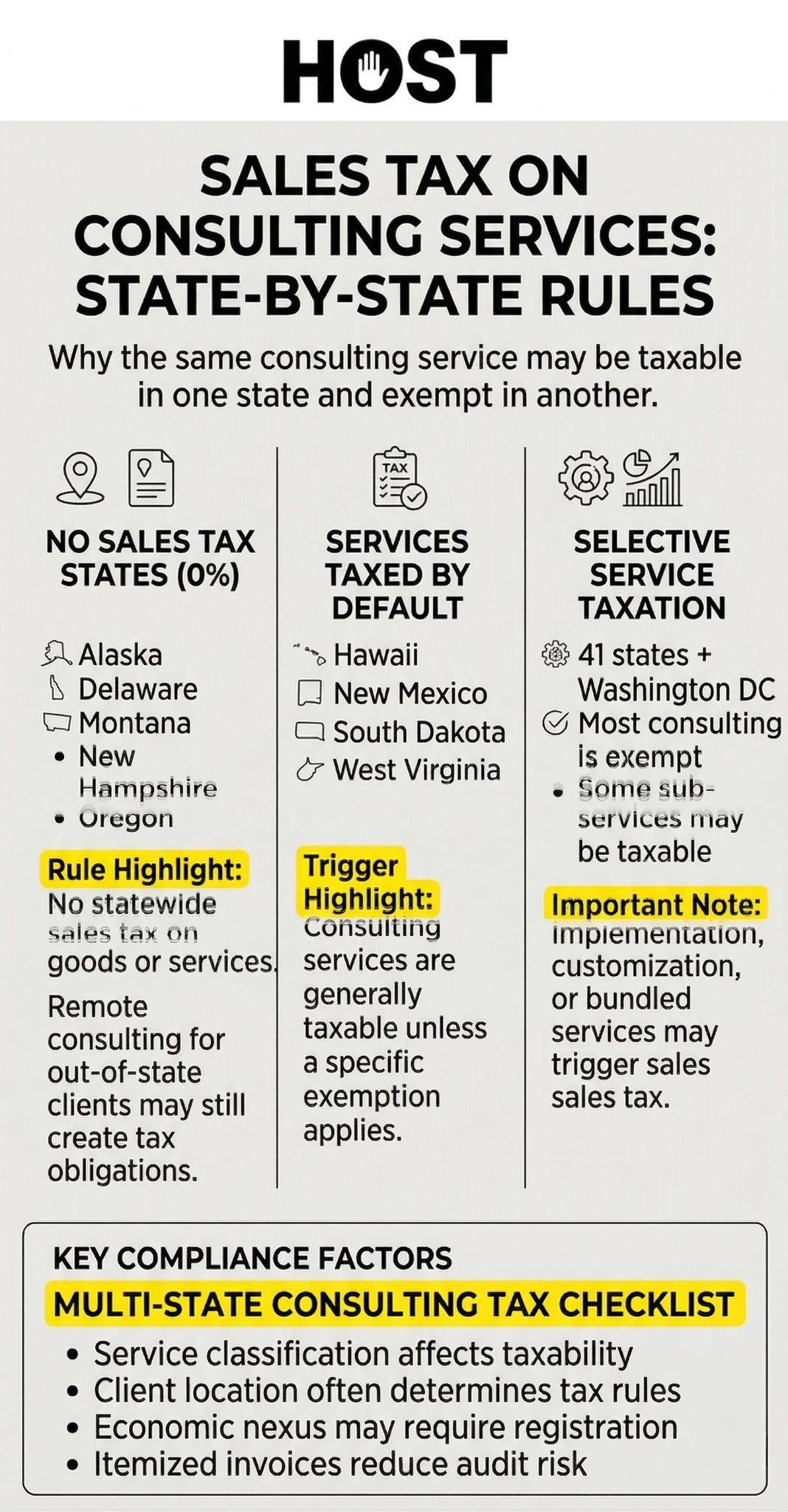

States with No Sales Tax

Five states: Alaska, Delaware, Montana, New Hampshire, and Oregon impose no statewide sales tax on any goods or services. Consultants operating exclusively within these states face no sales tax collection obligations for consulting services.

However, consultants providing remote services to clients in taxing states may still face collection requirements in those client jurisdictions. Physical location doesn’t exempt you from obligations where your clients are based.

States Taxing Services by Default

Four states: Hawaii, New Mexico, South Dakota, and West Virginia take an opposite approach, presuming all services are taxable unless specifically exempted by law. In these jurisdictions, consulting services are generally subject to sales tax unless the consultant can identify a specific exemption.

This approach creates a higher burden on service providers to document exemptions rather than taxability. If you operate in any of these four states, assume your consulting services are taxable unless you can point to a specific statutory exemption.

States with Selective Service Taxation

The remaining 41 states and the District of Columbia use an enumeration approach, exempting services unless specifically listed as taxable. Most states in this category exempt professional consulting services broadly, but may tax specific consulting subcategories or consulting combined with tangible property sales.

Even within this majority, nuances matter. Some states exempt strategic consulting but tax implementation services. Others distinguish between business consulting and technical consulting. The devil is in the details.

Key Considerations for Consulting Taxability

Service Classification Matters

Not all consulting services are treated the same, even within a single state. Management consulting, marketing consulting, IT consulting, and technical consulting may have different tax treatments.

For example, some states distinguish between pure advisory services (typically exempt) and services that include implementation, setup, or customization (potentially taxable). A consultant who provides strategic recommendations remains exempt, but the moment they begin hands-on implementation or software configuration, tax obligations may arise.

Bundled Services and Mixed Deliverables

When consulting packages include both taxable and non-taxable components, tax obligations become more complex. If a consultant delivers strategic advice combined with software configuration or installation services, the portion involving tangible deliverables may be subject to tax even if pure advisory services remain exempt.

Proper invoicing becomes critical. Itemizing each service component and separating taxable from non-taxable work can protect both you and your client during audits.

Location of Benefit vs. Location of Service Delivery

Many states have moved toward defining taxability based on where the benefit of the service is received rather than where the service is physically performed. This creates particular complexity for remote consultants.

A consultant based in Oregon providing remote services to a client in New York may face New York’s use tax obligations even though the consultant hasn’t physically performed services in New York. The location where the client receives the benefit determines which state’s rules apply.

Nexus and Multi-State Operations

Consultants providing services across state lines must understand economic nexus requirements. Modern nexus standards mean that remote consulting services can trigger tax collection obligations in multiple states based on revenue thresholds alone.

If your consulting practice crosses $100,000 in sales to clients in a given state, you may have economic nexus there, even without physical presence. This makes it critical to evaluate nexus exposure regularly as your client base grows.

Specific State Examples and Common Patterns

California

California generally exempts professional services from sales tax, including strategic, legal, and marketing advice. However, if a consultant performs installation, setup, or customization of software or systems, that portion may become taxable.

The key is proper invoicing and line-item separation. If you bill consulting and implementation as a single bundled fee, California may tax the entire amount.

New York

New York generally exempts consulting services but has recent court rulings affirming the taxability of certain advertising-research and analytics services. Consultants in New York should carefully classify their specific service offerings.

Additionally, New York aggressively pursues use tax on services consumed in-state, even when provided by out-of-state consultants. If your client is in New York, New York’s rules generally govern.

Texas

Texas clarifies that consulting or strategy services not listed in the state’s taxable services schedule remain non-taxable. However, data processing and certain advertising work may still trigger tax obligations.

Texas also requires careful attention to bundled services. If consulting is bundled with taxable components, the entire package may become taxable unless properly separated.

Connecticut

Connecticut specifically taxes “business analysis, business management, and management consulting services” when they relate to core business activities or human resource management activities. Environmental consulting and certain other categories remain exempt.

This makes Connecticut one of the more aggressive states for taxing consulting services, and consultants serving Connecticut clients should register and collect tax accordingly.

Practical Compliance Steps for Consultants

Conduct a Nexus Analysis

Begin by determining in which states you have sales tax nexus. This includes physical presence and, increasingly, economic nexus based on sales thresholds. Each state maintains different thresholds, some as low as $100,000 in annual sales.

If you’re unsure where you have nexus, consider a professional nexus study to map your exposure accurately.

Research Each State’s Specific Rules

Use official state revenue department publications to determine taxability for your specific consulting services in each state where you have nexus. Don’t rely on general assumptions about service exemptions.

States frequently update their guidance, and what was exempt five years ago may now be taxable. Staying current is essential.

Itemize and Document Services

Invoice line-by-line to separate taxable from non-taxable components. If your engagement includes both consulting (potentially non-taxable) and implementation (potentially taxable), clear documentation protects you during audits.

Include detailed descriptions of each service component, dates of service, and location where work was performed or benefit received.

Track Client Locations

Monitor where your client base is located and adjust your tax collection practices accordingly. A client’s location determines which state’s rules apply to your consulting services.

Use CRM systems or invoicing software to tag client locations and flag states where you may be approaching economic nexus thresholds.

Monitor for Changes

State tax laws change frequently. Tax authorities regularly expand their bases to include previously exempt services. Subscribe to state revenue department updates or work with a sales tax compliance partner who monitors changes on your behalf.

Red Flags and Audit Triggers

Even seemingly straightforward consulting work can draw scrutiny from tax authorities. Advertising-related consulting, market research, business analytics, and services bundled with software or technology components face higher audit risk.

Consultants should maintain detailed records showing the nature of work performed, the location where work was performed or benefit received, and the reasoning behind any tax treatment applied. During audits, states will scrutinize whether services were properly classified and whether nexus obligations were met.

Poor documentation, inconsistent invoicing, or failure to register in nexus states are common triggers that can result in back taxes, penalties, and interest spanning multiple years.

How HOST Simplifies Consulting Service Tax Compliance

Sales tax compliance for consulting services requires constant vigilance across multiple jurisdictions. Between varying state rules, economic nexus thresholds, and evolving service definitions, staying compliant without expert help is increasingly difficult.

Hands Off Sales Tax (HOST) specializes in service-based business compliance, offering multi-state registrations, ongoing filings, and nexus monitoring tailored to consulting firms operating across state lines.

Whether you’re a solo consultant expanding into new states or a growing firm managing dozens of client jurisdictions, HOST provides clarity and peace of mind. From initial nexus analysis to audit defense, they handle the complexity so you can focus on serving clients.

Frequently Asked Questions (FAQ)

Do I need to charge sales tax on my consulting services?

It depends entirely on where you provide services and what type of consulting you offer. Most states exempt professional consulting services, but several states tax them broadly. Even in exempt states, certain consulting activities might be taxable. You must research rules in every state where you have nexus.

What’s the difference between taxable and non-taxable consulting services?

Generally, pure advisory services based on expertise and knowledge remain exempt in most states. However, consulting that includes implementation, setup, customization, or creation of tangible property often becomes taxable. The distinction varies dramatically by state.

How do I determine where to charge tax on remote consulting services?

Tax obligations depend on your state’s sourcing rules. Some states tax based on where the service is performed; others tax based on where the benefit is consumed. Your client’s location typically determines which state’s rules apply.

What happens if I operate in multiple states?

You must understand and comply with each state’s specific rules. This means potentially registering, collecting, and remitting tax in multiple states. A consultant operating in Arizona and New Mexico faces different tax obligations despite the geographic proximity.

What documentation should I maintain for consulting service audits?

Keep detailed records showing the nature of work performed, dates of service, client location, invoicing details showing line-item separation between taxable and non-taxable components, and the tax treatment applied. This documentation protects you during state audits.

How often should I review my consulting service tax compliance?

At minimum, review annually. Additionally, review whenever you add a new service offering, expand to a new state, or when your annual revenue crosses a state’s economic nexus threshold. Tax laws change frequently, so staying current is essential.

What role does nexus play in my consulting tax obligations?

Nexus determines whether you must collect sales tax in a state. Physical presence always creates nexus. Economic nexus thresholds vary. Some states require action at $100,000 in sales while others use different thresholds. Remote consultants commonly trigger economic nexus in multiple states.

What should I do if I’ve been providing consulting services without collecting sales tax?

If you discover you should have been collecting sales tax but haven’t, you may be able to resolve past non-compliance through a Voluntary Disclosure Agreement (VDA). VDAs allow businesses to come forward voluntarily and often result in reduced penalties, limited lookback periods, and sometimes waived interest. The key is acting before the state contacts you. Once an audit begins, VDA options disappear.

Discovered past non-compliance? HOST’s VDA services can help you resolve tax obligations with minimal penalties, protecting your business from aggressive state collections.

How do marketplace facilitator laws affect consulting services?

Marketplace facilitator laws primarily impact physical goods sold through platforms like Amazon or Etsy, where the platform collects tax on behalf of sellers. For consulting services, these laws have limited direct application unless you sell consulting through a platform that facilitates payment and delivery. However, if you offer consulting bundled with digital products or SaaS through a marketplace, that platform may handle some (but not all) of your tax obligations. You’ll still need to monitor your independent consulting work and direct client relationships separately.

Can I use resale certificates for consulting services?

Resale certificates generally don’t apply to consulting services since consulting is typically a final service provided to end users rather than something purchased for resale. However, if you purchase tangible goods or taxable services as part of delivering your consulting (such as software licenses, research reports, or materials you’ll incorporate into a deliverable you resell), you may be able to use resale certificates for those specific purchases. The key is that the item must be resold in substantially the same form, not simply used as a tool in providing your service.

Need help determining what qualifies for resale treatment? HOST can create custom tax matrices that clarify taxability for every component of your service offerings across all jurisdictions where you operate.