The nonprofit sector operates on thin margins and tireless dedication. Every dollar saved is another family fed, another student tutored, another community served. Yet thousands of charitable organizations across America pay sales tax they don’t legally owe. Not from ignorance of the law, but from the bewildering complexity of claiming what’s rightfully theirs.

Sales tax exemptions represent one of the most valuable yet misunderstood benefits available to nonprofit organizations. While most nonprofits are exempt from federal and state income taxes, many struggle to leverage sales tax exemptions effectively. With combined state and local sales tax rates approaching 10% in some jurisdictions, failing to claim this exemption can cost your organization thousands of dollars annually, which is money that could have gone directly to mission fulfillment.

The challenge lies in the complexity and lack of uniformity across states. Each state maintains different requirements, processes, and documentation standards for sales tax exemptions. Understanding your organization’s eligibility and navigating the application process requires careful attention to detail and knowledge of state-specific regulations.

If your nonprofit operates across multiple states and needs clarity on exemption eligibility and application procedures, HOST provides comprehensive guidance tailored to charitable organizations navigating multi-state compliance.

Understanding Sales Tax Exemptions for Nonprofit Organizations

At its foundation, a sales tax exemption allows qualified nonprofit organizations to purchase goods and services without paying state or local sales tax. The exemption recognizes that charitable organizations operate for public benefit rather than private profit, and that taxing their mission-critical purchases would drain resources meant for community service.

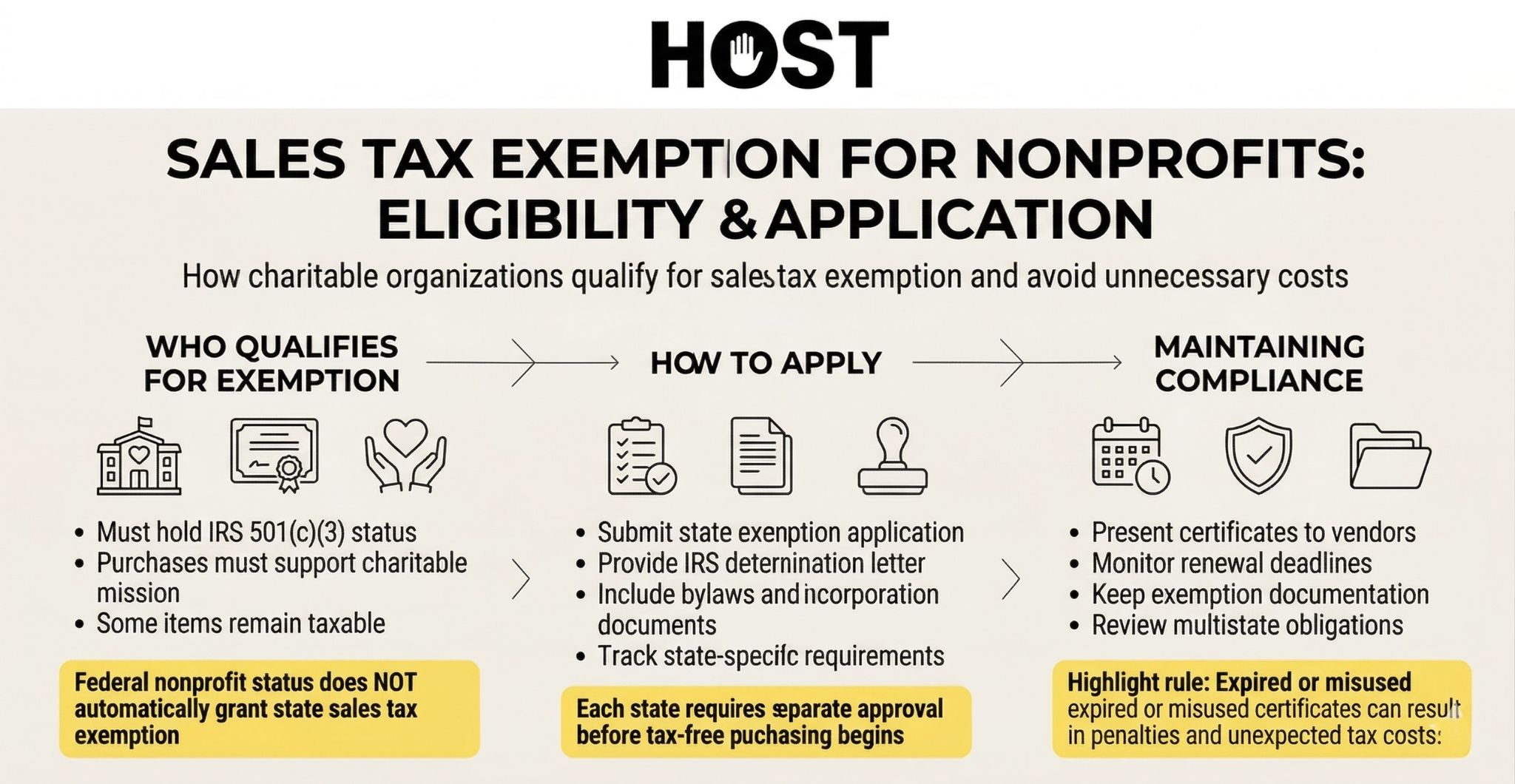

However, the path from federal tax-exempt status to state sales tax exemption is neither automatic nor uniform. The IRS grants 501(c)(3) status for federal income tax purposes, but this designation doesn’t automatically unlock state-level sales tax benefits. Each state operates its own system, maintains its own standards, and requires separate applications.

Five states: Alaska, Delaware, Montana, New Hampshire, and Oregon impose no statewide sales tax at all, making the question moot for organizations operating exclusively within their borders. The remaining 45 states plus the District of Columbia each maintain unique exemption frameworks that nonprofits must navigate independently.

Key Eligibility Requirements for Nonprofit Sales Tax Exemptions

501(c)(3) Status as the Foundation

The primary eligibility requirement for sales tax exemption in most states is maintaining recognized 501(c)(3) tax-exempt status from the IRS. This federal designation serves as the foundation for claiming state-level sales tax exemptions, proof that the IRS has vetted your charitable purpose and organizational structure.

However, it’s critical to understand that federal tax-exempt status does not automatically grant state sales tax exemption. Each state requires separate application and approval. Your IRS determination letter opens the door, but you must still walk through it state by state.

Some nonprofits mistakenly assume their federal status suffices and make tax-exempt purchases without state approval, only to face assessments, penalties, and interest years later when states discover the oversight during audits.

Charitable Mission Requirements

Beyond 501(c)(3) status, many states require that purchases made by the nonprofit directly relate to the organization’s charitable mission. This means employees and volunteers cannot use nonprofit exemption certificates for personal purchases, even if traveling on official business.

The burden of determining whether a purchase qualifies falls on the nonprofit organization itself. You must be prepared to explain how each tax-exempt purchase advances your charitable purpose. Not just generally, but specifically. Office supplies for program administration clearly qualify. A staff member’s lunch while working late does not, even though the staff member is working on behalf of the organization.

Some states, like Pennsylvania, impose particularly strict requirements. Organizations must complete comprehensive applications and demonstrate they meet all qualification criteria, including proving that the organization receives charitable contributions, operates exclusively for charitable purposes, and serves the community rather than private interests.

Purchase Limitations and Restrictions

Not all purchases qualify for exemption even for qualified nonprofits. The exemption doesn’t create a blanket shield, it’s more like a carefully drawn map with clear boundaries. Common exclusions include alcohol and spirits purchases (unless specifically sacramental), motor vehicles (with limited exceptions), meals and catering (varies by state), personal items for employees, and items purchased for resale unless covered by specific resale exemptions.

Organizations must ensure that every purchase claiming exemption genuinely supports their exempt purpose. The connection between purchase and mission should be documentable and defensible during audits.

The Sales Tax Exemption Application Process

The application process follows a generally consistent pattern across states, though details vary significantly. Here’s how to navigate it successfully.

Step 1: Verify Your Organization’s Federal Tax-Exempt Status

Before applying for state sales tax exemption, confirm that your organization has current 501(c)(3) status from the IRS. You’ll need your IRS Determination Letter and possibly Form 1023 or 1024.

Keep these documents readily accessible, not buried in storage or scattered across old email accounts, because as most states require copies during the application process. Some states accept digital copies, others demand originals or certified copies. Check your target state’s requirements before submitting.

Step 2: Research State-Specific Requirements

States vary significantly in their application requirements. Most states accept a short application form along with supporting documentation including your IRS Determination Letter, Articles of Incorporation, and organizational bylaws. Some states, however, require more extensive documentation or have unique forms that don’t resemble standard templates.

The Simplified Sales Tax Uniform Certificate of Exemption (SSUTA-COE) is accepted by 24 member states plus several non-member states, streamlining the process for multistate nonprofits. This standardized form allows you to claim exemptions across multiple jurisdictions without completing separate applications in each.

However, not all states accept all exemptions listed on this form, so verification remains essential. A state might accept the SSUTA-COE but still require supplemental documentation or reject certain exemption categories your organization claims.

Step 3: Complete the State Application

Complete your state’s official exemption certificate application form with care and precision. The bureaucracy is unforgiving, and small errors cascade into long delays.

Common mistakes that delay processing include incomplete information or blank fields (some states reject applications with any empty spaces), incorrect seller information that doesn’t match your account, missing authorized signatures (many states require board member or executive director signatures, not just staff), and using non-approved exemption certificate forms (downloading an outdated form from an unofficial website).

Most applications rarely require fees, making this an accessible process for organizations of all sizes. The barrier is administrative, not financial.

Step 4: Submit Required Documentation

Standard documentation typically includes a completed exemption application form, IRS Determination Letter, Articles of Incorporation, organization bylaws, any state-specific supplemental forms, and authorization letters from qualified signatories.

Assemble everything before submitting. Piecemeal submissions like sending the application now, the bylaws next week, the determination letter when you find it, frustrate processors and extend timelines unnecessarily.

Step 5: Maintain and Renew Your Exemption

Exemption certificates typically remain valid for extended periods, though some states require renewal. Maryland, Virginia, and Florida, for example, require renewal every five years. Others operate on a “one-and-done” basis after initial approval.

Keep track of your renewal deadlines to maintain uninterrupted exemption status. Missing a renewal deadline means reverting to taxable status immediately. Past the deadline, vendors must charge you tax until you reapply and get approved again.

If your nonprofit needs help tracking renewal deadlines across multiple states, HOST provides compliance monitoring that ensures exemptions remain current in all jurisdictions where you operate.

Documentation Requirements for Nonprofit Sales Tax Exemption

Essential Documents to Gather

Successful applications require thorough documentation preparation, gathered and organized before you begin. Essential items include IRS Form 1023 or 1023-EZ (Determination Letter showing 501(c)(3) status), Certificate of Incorporation or Articles of Organization, current bylaws or governance documents, proof of address and organizational location, and board resolution authorizing exemption certificate application.

The board resolution is often overlooked but frequently required. It demonstrates that your organization’s leadership has formally authorized the exemption application and designated who may sign on behalf of the organization.

Providing Exemption Certificates to Vendors

Once approved, your organization receives an exemption certificate: a document you’ll present repeatedly over the years ahead. To substantiate tax-exempt status when making purchases, you must present a valid, timely, and accurate certificate for each applicable jurisdiction.

Vendors bear responsibility for maintaining certificate records to protect themselves during audits, but your organization should keep copies of all submitted certificates for your own audit protection. If a vendor loses your certificate and charges tax three years from now, you’ll need proof you provided it originally to claim a refund.

Exemption certificates expire periodically (typically five years after issuance in states that impose expiration dates) so maintain a system for tracking expiration dates and managing renewals before they lapse.

State Variations and Special Considerations

Understanding State-Specific Rules

Each state maintains unique requirements for nonprofit sales tax exemptions, and the variations matter more than the similarities. Understanding your specific state’s approach is non-negotiable for compliance.

California requires separate state tax-exemption applications despite federal status and maintains particularly detailed application procedures. New York accepts purchases of tangible property, services, and amusement charges for exempt organizations, covering a broader range than many states. Texas distinguishes between exemptions for purchases (what you buy for your organization) versus sales (what your organization sells to others), requiring separate analysis for fundraising activities. Washington State provides exemptions only for donated goods and specific fundraising activities, limiting what qualifies more strictly than most jurisdictions.

These aren’t minor technical distinctions, they determine whether your organization pays tax or doesn’t on substantial purchases.

Multistate Compliance Challenges

Nonprofits operating across multiple states face compounded complexity. The SSUTA-COE certificate helps streamline this process, but each state retains authority to accept or reject specific exemptions.

Organizations cannot assume their primary state exemption automatically qualifies in other jurisdictions. A food bank operating in three states needs three separate exemption approvals, each following different procedures and requiring different documentation standards.

The administrative burden multiplies with geographic reach. A national nonprofit with chapters in 20 states must track 20 different exemption certificates, 20 different renewal schedules, and 20 different sets of rules about what qualifies for exemption.

If your nonprofit operates across multiple states, HOST can manage the entire exemption application and renewal process across all jurisdictions, ensuring consistent compliance without internal administrative burden.

Common Mistakes That Delay or Deny Applications

Application Errors

The most frequent application rejections result from avoidable mistakes that careful review prevents. Incomplete information or illegible handwriting tops the list. States won’t guess what you meant to write. Mismatched seller information on certificates creates confusion about which entity is claiming exemption. Missing authorized signatures invalidate applications immediately in most states. Using outdated or unapproved forms (downloaded from non-official sources or held over from previous years) gets applications rejected outright. Submitting photocopies instead of originals where required violates stated procedures.

These errors waste weeks or months while you correct and resubmit. Take time to verify everything before sending.

Misunderstanding Exemption Scope

Many nonprofits incorrectly assume all their purchases qualify for exemption. Personal employee purchases, items for resale without proper documentation, and purchases unrelated to charitable purposes remain taxable. Period.

Pennsylvania frequently denies applications from organizations failing to quantifiably prove they meet all exemption criteria. Vague statements about doing good work don’t suffice. You must demonstrate with specificity that you meet statutory requirements.

Neglecting Renewals

Organizations often lose exemption status through oversight rather than ineligibility. Missing renewal deadlines in states like Maryland, Virginia, and Florida automatically invalidates your exemption status until reapplication.

The loss isn’t merely technical. Vendors must immediately begin charging you tax, increasing your costs until you complete reapplication and receive new certificates. Those increased costs come directly out of program budgets.

How Hands Off Sales Tax Can Support Your Nonprofit

Organizations managing complex exemption requirements across multiple states benefit from professional guidance that removes administrative burden and ensures continuous compliance.

Hands Off Sales Tax (HOST) specializes in simplifying sales tax compliance for organizations of all sizes, including nonprofits navigating multi-state operations. Services include comprehensive nexus analysis to identify states where exemption applies, application preparation and submission assistance, documentation organization and tracking, renewal reminder management, exemption certificate maintenance and updates, and consulting for organizations with unique purchasing situations.

Whether you’re a small local nonprofit expanding to a second state or a national organization managing exemptions in 30+ jurisdictions, HOST provides the expertise and systems to maintain compliance without diverting staff time from mission-critical work.

Frequently Asked Questions (FAQ)

Does federal 501(c)(3) status automatically grant state sales tax exemption?

No. Federal tax-exempt status does not automatically grant state sales tax exemption. Each state requires separate application and approval. Even states that accept federal determination letters as primary evidence require organizations to formally apply through state procedures.

The IRS and state revenue departments operate independently. Federal recognition establishes eligibility but doesn’t confer state benefits automatically. You must take action in each state to claim what your federal status makes you eligible to receive.

What if my organization operates in multiple states?

Organizations must apply for sales tax exemption in each state where they have operations or make significant purchases. The SSUTA-COE form simplifies this process for 24 member states, but individual applications remain necessary for non-member states or when supplemental documentation is required.

Geographic expansion requires corresponding expansion of compliance efforts. Opening a new program site in another state triggers new exemption application requirements in that state.

Managing exemption applications across multiple states? HOST handles multi-state compliance so your team can focus on mission delivery rather than administrative procedures.

How long does the exemption certificate application process take?

Processing times vary by state and application completeness. Most states process applications within 2-6 weeks, but some may take longer if additional documentation is requested or if applications are submitted during peak processing periods.

Incomplete applications extend timelines significantly. A complete, accurate application submitted with all required documentation processes faster than a rushed application that triggers multiple follow-up requests.

Can nonprofit employees purchase personal items tax-free using the organization’s exemption?

No. Exemption certificates apply only to purchases made for the organization’s charitable purposes. Personal employee purchases remain subject to sales tax regardless of whether the employee is traveling on official business or using organizational purchasing accounts.

The exemption follows the purchase purpose, not the purchaser’s employment status. An executive director buying lunch for themselves pays tax even though they’re traveling for organizational business. The same executive buying supplies for a program event presents the exemption certificate because the purchase serves organizational purposes.

What happens if I use an expired exemption certificate?

Using an expired certificate may result in sales tax liability, penalties, and interest. Organizations are responsible for tracking renewal dates and obtaining new certificates before expiration.

Vendors who accept expired certificates may face their own liability, so many maintain systems that flag expired certificates and refuse to honor them. Once your certificate expires, you’ll immediately begin paying tax on purchases until you renew.

Struggling to track renewal deadlines across multiple states? HOST’s compliance monitoring ensures all exemption certificates remain current before they expire.

Can my nonprofit claim exemption on all types of purchases?

No. Certain items like alcohol, motor vehicles, and items unrelated to your charitable mission typically don’t qualify. Review your state’s specific exemptions and your organization’s exempt purpose before assuming eligibility.

Even qualified nonprofits face limitations on exemption scope. The exemption isn’t universal, it’s targeted to purchases that directly support tax-exempt purposes as defined by state law.

What documentation do I need to keep for audit protection?

Maintain copies of your exemption certificate, all state approvals, renewal confirmations, and records associating each tax-exempt purchase with your organization’s charitable purpose.

During audits, states examine whether claimed exemptions were legitimate. Documentation proving the connection between purchases and charitable mission protects your organization from assessments on improperly exempted transactions.

Can I claim back tax refunds for purchases made before applying for exemption?

Most states allow refunds for purchases made within a specific timeframe before application (typically 2-4 years, depending on the state’s statute of limitations). Contact your state’s tax department with proof of exempt status eligibility.

However, claiming refunds for pre-exemption purchases requires detailed documentation proving each purchase would have qualified for exemption had you possessed the certificate at the time. The administrative burden is substantial but may be worthwhile for large purchases.

Need help recovering sales tax paid before obtaining exemption certificates? Contact HOST for guidance on filing refund claims across multiple states.

What if a vendor refuses to accept my exemption certificate?

Vendors have the right to refuse exemption certificates if they appear invalid, expired, or improperly completed. However, if your certificate is valid and the purchase qualifies for exemption, you can provide additional documentation (such as your IRS determination letter or state approval confirmation) to reassure the vendor.

Some vendors refuse exemption certificates out of caution or misunderstanding rather than genuine concerns about validity. Polite persistence and clear documentation usually resolve these situations. If a vendor continues to refuse a valid certificate, you may pay the tax and file a refund claim with the state afterward.

Do fundraising sales by nonprofits qualify for sales tax exemption?

This depends entirely on state law and the nature of the fundraising activity. Many states distinguish between purchases made by the nonprofit (input tax) and sales made by the nonprofit (output tax).

Some states provide exemptions for occasional fundraising sales, annual fundraisers, or sales of donated goods. Others tax all retail sales regardless of nonprofit status. Texas, for example, grants exemptions for certain fundraising activities but requires careful documentation. California provides limited exemptions for qualified fundraising events.

If your nonprofit conducts fundraising sales, research your state’s specific rules about both sales tax collection obligations and exemptions for fundraising activities. Don’t assume your purchase exemption extends to your selling activities.