SaaS sales tax nexus determines where your software company must collect and remit sales tax. For software-as-a-service businesses selling across state lines, understanding nexus rules isn’t optional, it’s the difference between smooth growth and costly surprises.

The challenge? Every state treats SaaS differently. Some tax it like tangible property. Others exempt it entirely. And nexus thresholds vary dramatically, triggering obligations you might not discover until a notice arrives from a state you’ve never even visited.

The cost of getting it wrong is real. According to industry estimates, non-compliant SaaS companies experience approximately a 4.3% drag on profitability. For a company growing $20M ARR, that’s nearly $1M in exposure from uncollected taxes, penalties, and interest.

Hands Off Sales Tax (HOST) specializes in helping SaaS companies navigate these complexities. From nexus analysis to multi-state registration and automated filings, we handle compliance so you can focus on building great software.

What Is Sales Tax Nexus for SaaS Companies?

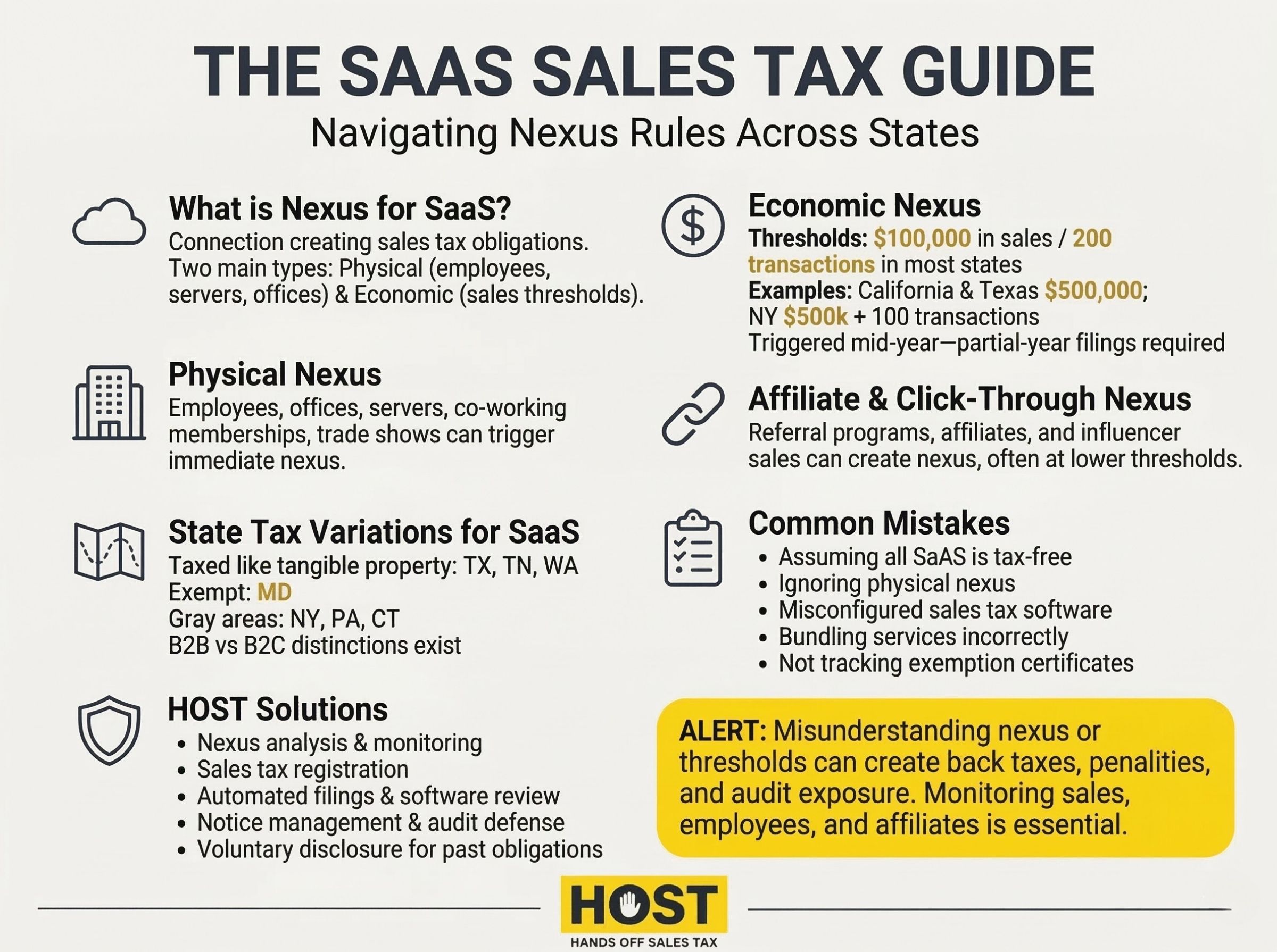

Sales tax nexus is the connection between your business and a state that creates a tax collection obligation. Once you establish nexus, you must register, collect sales tax from customers in that state, and remit it to tax authorities.

For SaaS companies, nexus triggers in two primary ways:

Physical Nexus: Traditional nexus based on physical presence like offices, employees, servers, or property. If your SaaS company has developers working remotely in Colorado or maintains servers in Virginia, you likely have physical nexus there.

Economic Nexus: Post-Wayfair nexus based on sales volume. After the 2018 Supreme Court decision in South Dakota v. Wayfair, states can require out-of-state sellers to collect sales tax once they exceed thresholds, typically $100,000 in sales or 200 transactions annually.

Most SaaS companies trigger economic nexus long before establishing physical presence. Hit $100,000 in California sales and you have nexus, even without a single employee or server in the state.

The complexity multiplies because each state sets its own thresholds, and not all states tax SaaS identically. Understanding where you have nexus is step one. Understanding what you need to collect is step two.

How States Tax SaaS Differently

The biggest challenge for SaaS compliance is the lack of uniformity. States fall into several categories:

States That Tax SaaS as Tangible Property: Texas, Tennessee, and Washington treat SaaS subscriptions like tangible personal property, making them fully taxable. Sell project management software to a Texas customer? You collect sales tax.

States That Exempt SaaS: Maryland doesn’t tax software accessed remotely. Your Baltimore customer pays no sales tax on their monthly subscription.

States With Gray Areas: New York doesn’t tax SaaS but does tax prewritten software sold electronically. The line between “SaaS” and “downloaded software” becomes critical and confusing.

States Taxing Specific Features: Connecticut might tax SaaS used for data processing but exempt collaboration tools. Pennsylvania taxes software used for business operations but may exempt others.

B2B vs B2C Distinctions: Some states differentiate between business and consumer sales. Iowa and Ohio may exempt B2B software sales while taxing consumer subscriptions. If you’re selling enterprise software, verify whether customer type affects taxability in each state.

California presents unique challenges. While most cloud-based SaaS is exempt, rules change when software is bundled with hardware or includes taxable services. Pure subscription? Exempt. Add consulting or custom development? Potentially taxable.

This patchwork means SaaS companies need state-by-state analysis. Misconfiguring your sales tax software creates overcharging (losing customers) or undercharging (owing back taxes).

Economic Nexus Thresholds by State

Economic nexus thresholds determine when remote sales trigger collection obligations. While most states use $100,000 in sales or 200 transactions, variations exist:

Common Threshold: Most states use $100,000 in annual sales as the trigger. Some dropped transaction count requirements, focusing solely on revenue.

California: $500,000 in sales annually. SaaS companies can operate below this threshold without collecting California sales tax.

Texas: $500,000 in sales annually. Like California, Texas has a higher threshold but applies sales tax to SaaS once nexus is established.

New York: $500,000 in sales AND more than 100 transactions. Both conditions must be met.

Thresholds apply to total sales in the state, not just taxable sales. Even if SaaS is exempt in a state, crossing the threshold for other products could create registration requirements.

Monitoring these thresholds manually is nearly impossible for SaaS companies. Monthly recurring revenue models mean crossing thresholds mid-year, creating partial-year obligations that are easy to miss.

HOST’s nexus analysis tracks your sales across all 45 states with sales tax, identifying exactly where and when you’ve triggered obligations. So you register on time and avoid penalties.

Physical Nexus Considerations

While economic nexus dominates discussions, physical nexus remains critical:

Remote Employees: Hiring a developer or customer success manager in a new state can trigger immediate nexus. Fully remote team with employees in ten states? Potentially nexus in all ten regardless of sales volume.

Servers and Cloud Infrastructure: Maintaining servers in a state traditionally created nexus. Cloud computing complicates this. Use AWS servers in multiple states? Some states argue this creates physical presence.

Offices and Co-Working Spaces: Any physical location establishes nexus: headquarters, satellite offices, even co-working memberships.

Trade Shows and Events: Attending a conference or setting up a booth can create temporary nexus in some states. Texas has particularly strict rules around event-based nexus, though it typically only applies if you’re making sales at the event.

Physical nexus triggers registration obligations immediately, unlike economic nexus which activates once thresholds are crossed. A SaaS company opening a sales office in Florida must register for sales tax right away, even with zero Florida sales.

Affiliate and Click-Through Nexus

Beyond physical and economic nexus, SaaS companies with referral programs face another trigger: affiliate nexus.

How It Works: When in-state affiliates or referral partners generate sales for your business, some states consider this sufficient connection to require tax collection, even without physical presence or crossing economic thresholds.

Lower Thresholds: Affiliate nexus often triggers at lower levels than economic nexus. Pennsylvania can establish nexus with $0 in affiliate-generated revenue. Other states set thresholds as low as $10,000-$50,000 in affiliate sales.

Who’s Affected: SaaS companies running affiliate programs, referral partnerships, or influencer marketing campaigns in multiple states need to track not just total sales, but sales generated through in-state affiliates specifically.

This creates an additional compliance layer that catches many SaaS companies by surprise. Over 20 states have enacted click-through nexus laws, and enforcement became significantly easier after the Wayfair decision eliminated physical presence requirements.

Common SaaS Sales Tax Mistakes

Assuming All SaaS Is Tax-Free: This misconception leads to years of uncollected tax in states like Texas or Washington, creating liabilities during audits.

Ignoring Physical Nexus: Hiring remote employees triggers nexus, but many SaaS companies don’t register until discovering obligations years later.

Misconfigured Sales Tax Software: Common mistakes include treating all SaaS as exempt, failing to enable specific state rules, or double-taxing. HOST offers a Free Sales Tax Software Review to identify and fix these errors.

Crossing Thresholds Mid-Year: Economic nexus triggers during the year create partial-year filing obligations. Hit California’s $500,000 threshold in July? Register and file for the remaining months. Most states take 2-4 weeks to process registrations, so plan ahead! You cannot legally collect sales tax until you receive your permit.

Bundling and Ancillary Services: Watch for taxability changes when bundling services with SaaS. Implementation, training, support, and configuration may become taxable when sold with software even if separately invoiced. Texas, for example, may tax professional services bundled with subscriptions differently than standalone SaaS.

Not Tracking Exemption Certificates: B2B SaaS companies selling to resellers or tax-exempt organizations must collect and maintain valid exemption certificates. Invalid or expired certificates make you liable for uncollected tax during audits. Maintain organized records with clear expiration tracking.

Each mistake compounds over time. A small oversight in year one becomes significant liability by year three.

How HOST Simplifies SaaS Sales Tax Compliance

Nexus Analysis: We analyze your sales footprint, employee locations, and infrastructure to determine exactly where you have nexus across all states.

Sales Tax Registration: We handle registrations in every required state, managing paperwork, follow-ups, and state communications.

Automated Filings: HOST files your sales tax returns monthly, quarterly, or annually based on each state’s requirements.

Software Optimization: We review and optimize your TaxJar, Avalara, or other automation tools to ensure correct calculations.

Notice Management: Received a confusing letter from a state tax authority? We interpret and respond to notices, protecting you from unnecessary penalties.

Audit Defense: If a state audit occurs, we serve as your trusted partner organizing documentation and defending your position.

Voluntary Disclosure Agreements: Discovered past obligations? We file VDAs with states to limit lookback periods and abate penalties.

We’ve focused exclusively on sales tax for over 25 years. Through our parent company TaxMatrix, we’ve helped North America’s largest companies manage sales tax requirements. Now we bring that expertise to SaaS companies of all sizes.

Take Control of Your SaaS Sales Tax Compliance

SaaS sales tax nexus rules are complex, constantly changing, and vary dramatically by state. What works in Maryland doesn’t work in Texas. What triggers nexus in California differs from New York.

Trying to manage this internally drains time, creates stress, and increases audit risk. Every hour spent researching state rules or preparing returns is time not spent improving your product or serving customers.

Whether you’re crossing economic nexus thresholds in new states, hiring remote employees, or unsure about your current compliance status, professional help eliminates uncertainty and prevents costly mistakes.

At HOST, we combine deep technical expertise with transparent communication and personalized support. We handle the complexity so you can focus on growing your SaaS business.

Contact us today to discuss your sales tax needs or schedule a free consultation. Let us handle the tax so you can focus on building great software.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book. Many of these mistakes apply to SaaS companies too.

Frequently Asked Questions

Do I need to collect sales tax on my SaaS subscriptions?

It depends on where your customers are located and where you have nexus. Some states like Texas fully tax SaaS, while others like Maryland exempt it. You must collect tax in states where: (1) you have nexus, and (2) SaaS is taxable. HOST’s nexus analysis identifies your specific obligations.

What’s the difference between physical and economic nexus for SaaS?

Physical nexus is created by offices, employees, servers, or property in a state, triggering immediate tax obligations. Economic nexus is triggered by exceeding sales thresholds (typically $100,000 annually) even without physical presence. SaaS companies often have both types simultaneously.

How do I know if I’ve crossed economic nexus thresholds?

You must track total sales by state throughout the year. Once you exceed a state’s threshold (often $100,000), nexus is established. HOST monitors your sales data across all states, alerting you when registration becomes necessary.

Can I get in trouble for not collecting sales tax on SaaS?

Yes. States can assess back taxes, penalties, and interest for uncollected sales tax, often looking back three to four years. During audits or M&A due diligence, undiscovered liabilities create serious problems. Proactive compliance prevents these issues.

Should I use sales tax software or hire a service like HOST?

Sales tax software automates calculations but requires proper configuration and ongoing management. You’re still responsible for registration, filing, nexus monitoring, and responding to notices. HOST provides full-service management. We handle everything from nexus analysis to filings and audit defense, ensuring nothing falls through the cracks.

Does hiring remote employees in a new state create sales tax nexus?

Yes. Having employees (even one) in a state typically creates physical nexus immediately, regardless of sales volume. If you hire a developer in Colorado, you likely need to register for Colorado sales tax right away. Even if your SaaS is exempt there, because physical nexus creates a filing obligation.