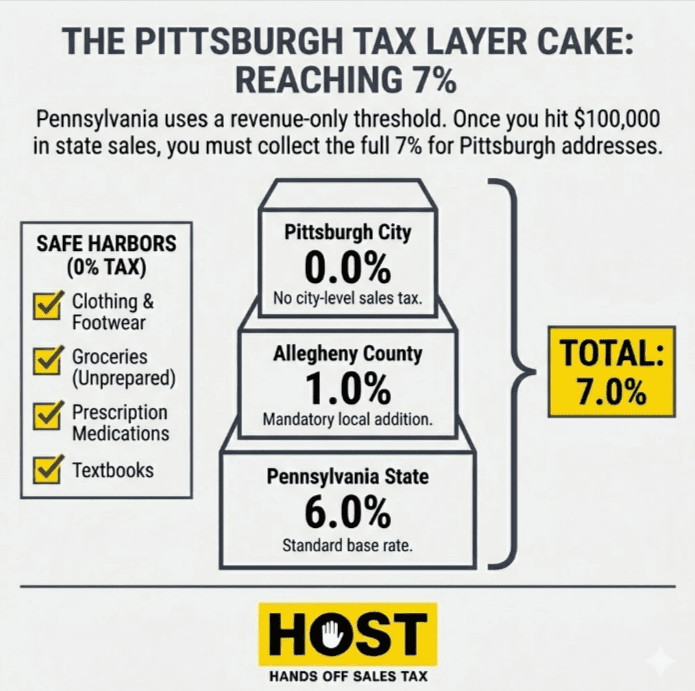

Managing sales tax in Pittsburgh means navigating two layers: Pennsylvania’s 6% state rate and Allegheny County’s 1% local tax. That’s 7% total. Straightforward on the surface, but complexity lurks beneath.

For e-commerce businesses expanding into Pennsylvania, Pittsburgh’s tax structure demands precision. One wrong rate calculation, one missed registration deadline, and you’re facing penalties that eat into margins you worked hard to build.

Hands Off Sales Tax (HOST) specializes in Pennsylvania’s multi-jurisdictional requirements. Our nexus analysis, registration support, and automated filing handle Pittsburgh’s system while you focus on customers, not compliance spreadsheets.

What Is the Sales Tax Rate in Pittsburgh?

Pittsburgh’s combined rate sits at 7%:

- Pennsylvania State: 6%

- Allegheny County: 1%

- Pittsburgh City: 0% (no city-level tax exists)

This 7% applies to most tangible personal property sold within city limits. Step outside Pittsburgh but stay in Allegheny County? Still 7%. Cross into Butler or Washington County? Drops to 6%.

Pennsylvania is one of two states allowing local jurisdictions to add sales tax on top of the state rate. This creates different combinations across 67 counties, Allegheny and Philadelphia being the only two imposing local taxes.

For remote sellers, address precision matters. Shipping to Pittsburgh requires 7%. Shipping to Erie requires 6%. Your automation needs to know the difference, or you’re collecting wrong. Overpaying customers or shortchanging the state.

How Pittsburgh’s Tax System Actually Works

Pennsylvania State Sales Tax (6%)

Pennsylvania’s 6% base has existed since 1953. Post-Wayfair, the state requires remote sellers to collect once they hit $100,000 in annual Pennsylvania sales. No transaction threshold, purely revenue-based.

Cross that $100,000 threshold anywhere in Pennsylvania, and you’re collecting statewide. Pittsburgh, Philadelphia, rural counties, all of them.

Pennsylvania exempts plenty: groceries, clothing, textbooks, prescription medications, residential utilities. These exemptions apply everywhere, which simplifies things. If it’s exempt in Harrisburg, it’s exempt in Pittsburgh.

Allegheny County Tax (1%)

Allegheny County adds 1% under the Local Tax Enabling Act. This hits all 130 municipalities in the county. 1.2 million residents total.

The county tax mirrors state rules. Exempt from state tax? Exempt from county tax. Taxable items face both layers.

Pittsburgh levies no additional city tax. That 7% is entirely state and county. This distinguishes Pittsburgh from Philadelphia, where a 2% local tax pushes the total to 8%.

What’s Taxable in Pittsburgh?

Pennsylvania keeps taxability relatively narrow compared to states like Washington or Texas.

Taxable:

- Tangible personal property (electronics, furniture, appliances)

- Prepared food from restaurants

- Alcoholic beverages for off-premises consumption

- Telecommunications services

- Hotel occupancy

Exempt:

- Clothing and footwear (all price points)

- Groceries (unprepared food)

- Prescription and OTC medications

- Textbooks

- Residential utilities

- Most services

Manufacturing exemptions add complexity. Equipment used directly in manufacturing gets exempted, but you need proper documentation, exemption certificates from buyers.

Misconfiguring your system to tax clothing creates friction. Customers notice. Failing to tax electronics creates audit liability. The state definitely notices.

HOST’s software review catches these errors before they compound. We audit TaxJar, Avalara, and other platforms to ensure Pittsburgh customers see correct calculations.

When You Must Collect Pittsburgh Sales Tax

Physical presence always creates a nexus. Store, warehouse, office in Pittsburgh? You’re collecting from day one.

Wayfair introduced an economic nexus for remote sellers—collection based purely on revenue.

Pennsylvania’s threshold: $100,000 in annual gross sales. No transaction count. Current year or prior year, either triggers nexus.

The threshold applies statewide. You don’t separately track Pittsburgh versus Harrisburg sales. But once you have nexus, you apply the correct rate per customer location: 7% for Allegheny County, 8% for Philadelphia, 6% elsewhere.

Additional nexus triggers:

- Warehouses or fulfillment centers (including FBA in PA)

- Employees, contractors, or sales representatives

- Trade shows or temporary events

- Affiliate relationships in-state

Marketplace facilitator laws shift the burden. Amazon, eBay, Etsy, Walmart Marketplace, they collect on your behalf for transactions through their platforms. Your own website? That’s still your responsibility.

Figuring out where you have nexus across all states requires systematic analysis. HOST’s nexus analysis examines your complete footprint: sales data, inventory locations, employee presence, identifying every state where you’ve triggered obligations.

Registering for Sales Tax in Pittsburgh

Registration flows through Pennsylvania’s Department of Revenue. No separate county or city registration exists.

Process:

- Complete PA-100 Enterprise Registration Form

- Provide business details (legal name, structure, ownership, FEIN)

- Describe business activities and locations

- Specify nexus basis (physical, economic, or both)

- Receive license (typically 10-15 business days)

Registration is free. Errors delay approval. Operating without registration when nexus exists? Penalties accumulate fast.

You’ll get assigned a filing frequency. Monthly, quarterly, or annually based on expected liability. Pennsylvania typically starts with quarterly, adjusting as collections materialize.

HOST handles registrations end-to-end. We complete paperwork, manage state communications, obtain licenses, and ensure correct filing frequency from launch. You stay focused on operations.

Filing Pittsburgh Sales Tax Returns

Filing schedules vary: monthly (liability exceeding $25,000 annually), quarterly (most businesses), or annually (minimal volume).

Returns due by the 20th of the month following the reporting period. January sales? Due February 20th.

Pennsylvania’s system automatically distributes collected taxes to state and county. One consolidated return covers everything—no separate Pittsburgh or Allegheny filings.

Common mistakes:

- Incorrect jurisdiction codes (tax goes to wrong locality)

- Late remittance (penalties trigger even when returns file on time)

- Not reconciling marketplace collections (duplicate payments)

- Misreporting exempt sales (audit red flags)

Late filing costs 5% of unpaid tax for the first month, plus 1% each additional month, capped at 50%. Interest compounds at 3% annually (adjusted quarterly).

HOST manages Pennsylvania filing obligations across all frequencies. We track marketplace versus direct sales, apply correct codes, ensure timely remittance. You avoid penalties and stay audit-ready without touching a spreadsheet.

Pennsylvania Filing Options and Systems

Pennsylvania’s myPATH system provides multiple filing methods depending on your collection volume:

Online filing through myPATH: Businesses remitting $1,000 or more monthly must use Electronic Funds Transfer (EFT). Smaller remitters can use ACH Debit, ACH Credit, or credit card payments.

Telefile by phone: Don’t have computer access? Call 1-800-748-8299 to file returns and remit payments. You’ll need your 8-digit Account ID, FEIN or SSN, and period ending date.

The myPATH portal also handles registration (PA-100 Enterprise Registration Form), return preparation, payment processing, and account management—all through a single interface.

Understanding Pennsylvania Use Tax

Pennsylvania’s use tax complements sales tax at the same 7% rate in Pittsburgh. When you purchase items from out-of-state sellers who don’t collect Pennsylvania sales tax, you technically owe use tax directly to the Department of Revenue.

For businesses, use tax commonly applies to equipment, supplies, or inventory purchased from vendors who didn’t charge Pennsylvania sales tax. Remote sellers exceeding economic nexus eliminate this burden for customers by collecting at purchase.

The distinction matters for compliance: if you buy a $5,000 piece of equipment from an out-of-state vendor who doesn’t collect Pennsylvania sales tax, you owe $350 use tax on your next return.

Calculating Pittsburgh Sales Tax

Here’s how the math works:

Example purchase: $100.00

- Pennsylvania state tax (6%): $6.00

- Allegheny County tax (1%): $1.00

- Total tax: $7.00

- Customer pays: $107.00

The calculation applies uniformly across Pittsburgh and all Allegheny County municipalities. Outside the county, only the 6% state rate applies, reducing a $100 purchase to $106 total.

Hotel Occupancy Tax in Pittsburgh

Hotel occupancy tax applies at the same 7% rate for rentals under 30 days. This includes traditional hotels, motels, and short-term rentals through platforms like Airbnb and VRBO.

Booking platforms typically collect this tax automatically for properties they list. However, property owners managing rentals independently must register for a separate hotel occupancy tax license and file returns even during periods with no bookings.

Special Product Taxes in Pittsburgh

Beyond standard sales tax, certain products face additional Pennsylvania taxes:

Cigarettes and tobacco: $2.60 per pack of 20 cigarettes ($0.13 per stick) plus the 7% sales tax.

Alcoholic beverages: Pennsylvania Liquor Control Board charges 18% on the consumer price (including markup and fees), plus the 7% sales tax on top.

Vehicle rentals: Rentals under 29 days face a 2% Vehicle Rental Tax plus the standard 7% sales tax.

Medical marijuana: 5% gross receipts tax applies to sales from grower/processors to dispensaries.

These stacked taxes significantly impact final prices. A $30 liquor purchase faces $5.40 in PLCB tax (18%) plus $2.48 in sales tax (7% of $35.40), totaling $37.88—nearly 26% above the base price.

Neighboring Municipality Rates

Pittsburgh’s 7% matches all Allegheny County communities:

- Mount Lebanon: 7%

- Bethel Park: 7%

- Monroeville: 7%

- Penn Hills: 7%

Outside Allegheny:

- Cranberry Township: 6% (Butler County)

- Washington: 6% (Washington County)

Pennsylvania uses destination-based sourcing for remote sellers. Customer location determines rate, not your business location. Proper address validation ensures accuracy.

HOST: Your Partner for Pittsburgh Compliance

Managing Pennsylvania’s structure alongside obligations in 45+ other states demands systems most businesses lack in-house.

What HOST Delivers:

Nexus Analysis: We analyze sales data across all states, identifying where you’ve crossed thresholds, Pennsylvania’s $100,000 included.

Registration: We handle Pennsylvania and every other required state, managing applications and communications.

Automated Filing: We prepare and file returns monthly, quarterly, or annually with accurate jurisdiction coding.

Multi-State Management: We handle filings across all states with obligations. Varying deadlines, forms, requirements.

Software Review: We audit automation tools, ensuring Pittsburgh calculates at 7% and other locations calculate correctly.

Notice Resolution: We interpret and respond to Department of Revenue notices, protecting you from penalties.

Audit Defense: We represent you in audits, organizing documentation and defending positions.

We’ve focused exclusively on sales tax for 25+ years. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

You handle the sales, we handle the tax.

Ready to Simplify Compliance?

Pennsylvania’s structure drains time without adding revenue. Whether managing Pittsburgh’s 7% rate, tracking economic nexus across multiple states, or ensuring automation accuracy, professional support eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss Pennsylvania compliance or schedule a free consultation. Let us handle complexity while you focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the total sales tax rate in Pittsburgh, PA?

Pittsburgh’s combined rate is 7%: Pennsylvania’s 6% state rate plus Allegheny County’s 1% local tax. Pittsburgh imposes no separate city tax.

Do I need to register separately for Pittsburgh city tax?

No. Pittsburgh has no city sales tax. Registration happens through Pennsylvania’s Department of Revenue using the PA-100 form, which handles state and county distribution automatically.

Is clothing taxable in Pittsburgh?

No. Pennsylvania exempts all clothing and footwear from sales tax regardless of price. Statewide, including Pittsburgh.

What is Pennsylvania’s economic nexus threshold?

$100,000 in gross sales during the current or prior calendar year. No transaction threshold exists. Cross $100,000 and you must register and collect.

Do marketplace sellers need to collect Pittsburgh sales tax?

Platforms like Amazon, eBay, and Etsy collect Pennsylvania sales tax on your behalf for transactions through their systems. Sales through your own website remain your responsibility if you have nexus.

How do I know if I’m charging the right rate for Pennsylvania customers?

Pennsylvania uses destination-based sourcing in which customer location determines rate. Allegheny County requires 7%, Philadelphia County 8%, most other locations 6%. HOST offers free software reviews to identify calculation errors.