Understanding Pennsylvania sales tax economic nexus matters when you’re selling into the Keystone State. Cross the $100,000 threshold and collection obligations kick in, regardless of whether you have a warehouse in Pittsburgh or employees in Philadelphia.

Missing Pennsylvania’s requirements creates audit risk and back-tax liabilities that can derail small businesses. The right partner eliminates the guesswork.

That’s where Hands Off Sales Tax (HOST) delivers. We analyze your Pennsylvania footprint through our nexus analysis services, handle registration with the Pennsylvania Department of Revenue, and manage ongoing filings so compliance supports growth rather than hindering it.

What Is Economic Nexus in Pennsylvania?

Economic nexus establishes tax obligations based on sales volume, not physical presence. No employees, warehouses, or offices required.

Before Wayfair, only businesses with physical presence in Pennsylvania needed to collect sales tax. The Supreme Court’s June 2018 decision in South Dakota v. Wayfair changed everything, allowing states to require collection from out-of-state sellers based solely on economic activity.

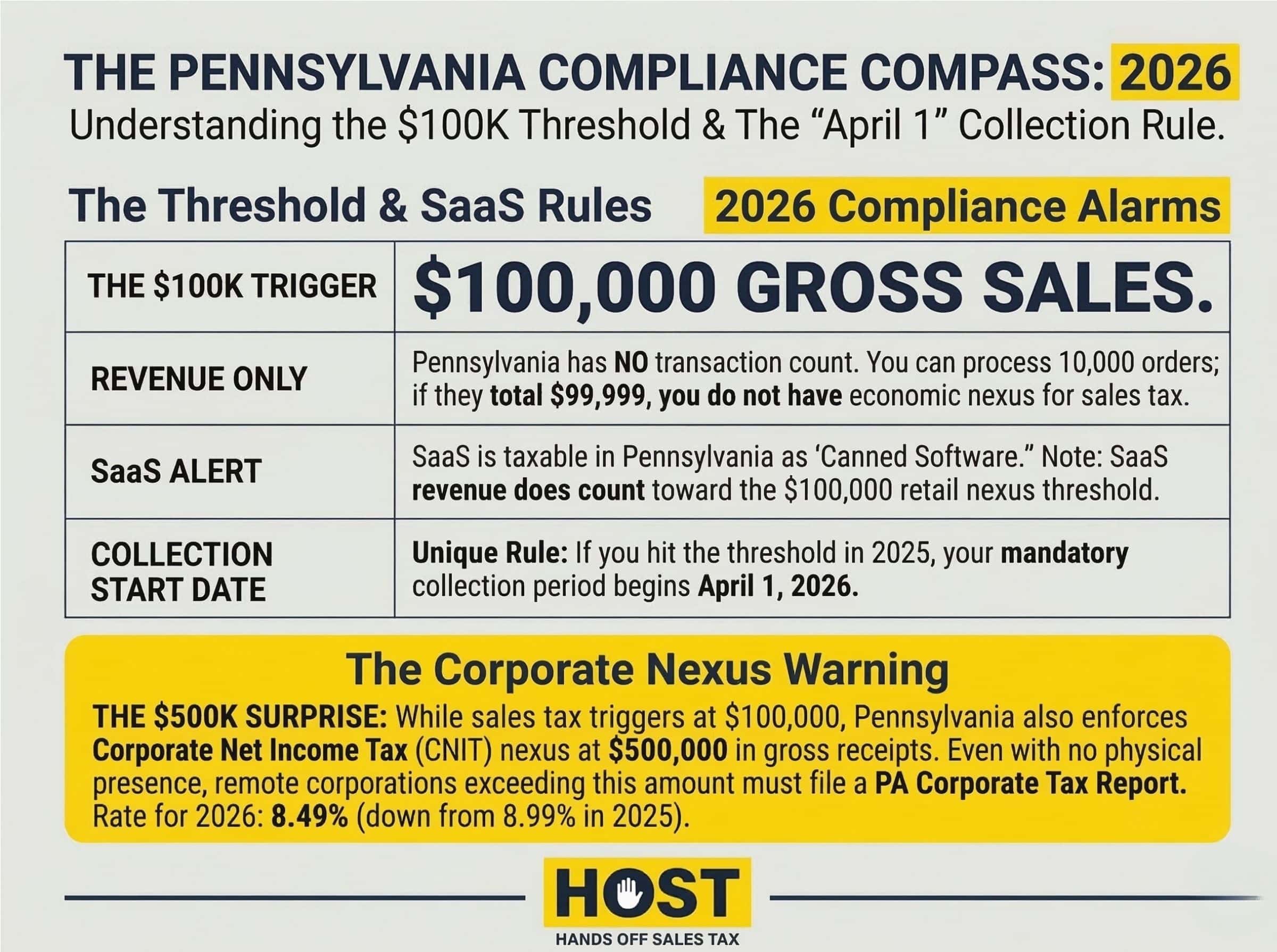

Pennsylvania adopted economic nexus effective July 1, 2019, following the Wayfair decision. The state implemented a $100,000 sales threshold with no transaction count requirement.

A California-based Shopify store selling to Pennsylvania customers now has the same obligations as a brick-and-mortar retailer in Philadelphia.

Other ways to create nexus: Beyond economic nexus, Pennsylvania recognizes physical nexus (employees, offices, inventory), affiliate nexus (relationships with in-state businesses that facilitate your sales), and click-through nexus (agreements with Pennsylvania residents who refer customers for commission). Any of these can trigger collection obligations regardless of sales volume.

Pennsylvania’s Economic Nexus Thresholds

Pennsylvania requires remote sellers to collect sales tax once they exceed $100,000 in gross sales into the state in the current or prior calendar year.

Pennsylvania uses a sales-only threshold. Many states implement dual thresholds ($100,000 OR 200 transactions), but Pennsylvania simplified compliance by eliminating the transaction component.

A single high-value sale exceeding $100,000 triggers nexus. A B2B software company making one $150,000 sale to a Pennsylvania corporation must register and collect.

The threshold applies to gross sales: the total before deducting returns, allowances, or exempt items. Sold $110,000 with $15,000 in exempt items? You still crossed the threshold. Even wholesale and resale transactions count toward the calculation, though they’re not taxable.

Pennsylvania measures on a calendar-year basis. Sales from January 1 through December 31 determine whether you’ve met the mark.

Below $100,000 but above $10,000? Pennsylvania offers an alternative: instead of registering and collecting, you can elect to comply with notice and reporting requirements. You must notify customers that use tax may be due and report customer information to Pennsylvania. The election must be made by March 1 annually. Most businesses find it simpler to just register and collect, but the option exists for smaller sellers.

When Collection Actually Begins

Pennsylvania uses a delayed collection schedule that differs from most states. Collection obligations begin April 1 following the calendar year when you exceeded the threshold, not immediately.

Here’s how it works:

If you crossed $100,000 in calendar year 2024, your collection obligation begins April 1, 2025. You measure based on the previous calendar year, giving you time to compile annual data and prepare.

For the initial collection period (July 1, 2019 – March 31, 2020), Pennsylvania used calendar year 2018 sales. Subsequent years follow the April 1 through March 31 collection cycle.

This delayed schedule means you won’t scramble mid-year when you hit the threshold. However, you must track calendar year sales carefully. Crossing $100,000 in December creates obligations starting the following April.

Best practice: Set automated alerts when Pennsylvania sales approach $90,000. This gives you time to prepare registration before the April 1 deadline.

HOST’s nexus analysis identifies exactly when you crossed thresholds and when your collection obligation begins.

How to Register for Pennsylvania Sales Tax

Registration requires completing the PA-100 Enterprise Registration Form through the Department of Revenue’s online system or by mail.

You’ll need basic information: legal entity name, EIN or SSN, business address, owner information, and NAICS code. Pennsylvania also asks for expected filing frequency based on projected sales.

The process typically takes 2-4 weeks. Pennsylvania issues a Sales Tax License and assigns filing frequency monthly, quarterly, or annually based on tax liability.

Pennsylvania charges no registration fee. However, you must maintain an active license and file returns even in zero-sales periods.

One complication: Pennsylvania requires marketplace sellers to register separately even if platforms like Amazon collect on marketplace-facilitated sales. You may still have non-marketplace sales (direct website, wholesale) requiring your own registration.

Alternative option: Pennsylvania contracts with Certified Service Providers (CSPs) who can handle registration, filing, and remittance at free or reduced cost. Using a CSP provides liability relief if the provider makes errors. The Department of Revenue maintains a list of approved CSPs.

HOST handles Pennsylvania registration from start to finish. Completing the PA-100, following up with the Department, and ensuring you receive your license without delays.

Pennsylvania Sales Tax Rates

Pennsylvania’s state sales tax rate is 6%. Allegheny County (Pittsburgh area) imposes a 1% local tax for a combined 7%, and Philadelphia imposes a 2% local tax for a combined 8%.

These are the only local sales taxes in Pennsylvania. Most of the state charges only 6%. This makes Pennsylvania relatively simple compared to states with hundreds of local jurisdictions.

Pennsylvania uses destination-based sourcing for remote sellers. You collect tax based on where your Pennsylvania customer is located.

Ship to Pittsburgh? Charge 7%. Ship to Philadelphia? Charge 8%. Ship anywhere else in Pennsylvania? Charge 6%.

Your sales tax software must calculate the correct rate based on customer zip code. Incorrectly charging 6% to a Philadelphia customer means you’re undercharging by 2%, creating personal liability.

HOST’s Free Sales Tax Software Review audits your automation tools to ensure Pennsylvania rates are calculated correctly, avoiding costly errors.

What’s Taxable in Pennsylvania?

Pennsylvania taxes most tangible personal property. Physical goods like electronics, furniture, and household items.

However, Pennsylvania provides significant exemptions:

Clothing: Most clothing is exempt. This includes everyday apparel, shoes, and accessories. However, formal wear, sporting goods, and protective equipment are taxable.

Food: Grocery items are generally exempt. Prepared foods, restaurant meals, and certain beverages are taxable.

Digital Products: Pennsylvania taxes downloaded software, digital books, music, and streaming services. SaaS is generally taxable if it provides software functionality.

Services: Most services are exempt. However, telecommunications, hotel accommodations, and vehicle parking are taxable.

HOST’s consultation services provide clarity on Pennsylvania taxability for your specific product mix.

Filing Requirements and Deadlines

Pennsylvania assigns filing frequencies based on annual tax liability:

- Monthly: Businesses owing more than $25,000 annually

- Quarterly: Businesses owing $201 to $25,000 annually

- Annual: Businesses owing $200 or less annually

Most remote sellers crossing the threshold initially file quarterly.

Pennsylvania returns are due on the 20th day of the month following the reporting period. January’s sales (if filing monthly) are due by February 20th.

Pennsylvania allows no extensions. Late filing triggers a 5% penalty immediately, plus interest.

Zero sales into Pennsylvania during a filing period? You must still file a zero return to maintain compliance.

HOST manages Pennsylvania filings on your behalf. Preparing returns, ensuring deadlines are met, and handling remittance so you never miss a filing date.

Common Pennsylvania Mistakes

Ignoring the Threshold: Businesses assume they don’t need to worry until establishing physical presence. Economic nexus means sales volume alone creates obligations.

Delaying Registration: Discovering you crossed the threshold months ago creates back-tax liability for sales made after crossing.

Miscalculating Gross Sales: Some businesses exclude exempt sales when calculating the threshold. Pennsylvania’s threshold is based on gross sales, the total before exemptions.

Charging Wrong Rates: Philadelphia and Allegheny County have local taxes. Charging only 6% to Philadelphia customers creates personal liability for the missing 2%.

Treating All Clothing as Taxable: Pennsylvania’s clothing exemption is broader than many states. Overcharging Pennsylvania customers creates refund requests and dissatisfaction.

HOST’s expertise prevents these costly mistakes, ensuring you collect correctly and file on time.

Voluntary Disclosure for Past Non-Compliance

Discovered you crossed Pennsylvania’s threshold months ago but never registered? A Voluntary Disclosure Agreement (VDA) can limit exposure.

Pennsylvania’s VDA program allows businesses to come forward voluntarily, register, and pay back taxes for a limited lookback period, which is typically 3 years instead of the standard statute. The VDA process waives penalties (though interest applies) and provides immunity from criminal prosecution.

To qualify, you must approach Pennsylvania before the state contacts you. Once Pennsylvania initiates an audit, you no longer qualify.

HOST manages Pennsylvania VDAs from start to finish, evaluating whether VDA is appropriate, preparing applications, and ensuring you achieve maximum liability reduction.

HOST: Your Pennsylvania Compliance Partner

Pennsylvania’s economic nexus rules create real compliance burdens. From monitoring the $100,000 threshold to navigating local rates to managing quarterly filings, Pennsylvania demands attention that diverts focus from growth.

What HOST Delivers:

- Nexus Analysis: We determine exactly when you crossed the threshold and when collection begins

- Pennsylvania Registration: We handle the PA-100 registration and follow up with the Department

- Ongoing Filings: We prepare and file Pennsylvania returns ensuring deadlines are met

- Software Optimization: We review your automation tools to ensure rates calculate correctly

- Notice Management: We interpret and respond to Pennsylvania Department of Revenue notices

- Audit Defense: We’re your trusted partner in resolving Pennsylvania sales tax audits

- VDA Support: We file agreements to limit lookback periods and abate penalties

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate Pennsylvania and 44 other states. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

Ready to Get Pennsylvania Compliant?

Pennsylvania’s $100,000 threshold isn’t a suggestion, it’s a legal requirement that triggers audit risk when ignored. Whether you’re approaching the threshold, recently crossed it, or discovered past non-compliance, acting now prevents costly penalties.

The right sales tax partner eliminates guesswork, handles administrative burden, and ensures compliance supports growth. At HOST, we combine deep Pennsylvania expertise with transparent communication and personalized support.

When you’re ready to take Pennsylvania sales tax off your plate, we’re ready to help. Contact HOST today to discuss your Pennsylvania compliance needs and discover how we handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is Pennsylvania’s economic nexus threshold for sales tax?

Pennsylvania requires remote sellers to collect sales tax once they exceed $100,000 in gross sales into the state in the current or prior calendar year. There is no transaction count requirement. Only the sales threshold matters.

Do I need physical presence in Pennsylvania to have nexus?

No. Economic nexus is based solely on sales volume. A business with no employees, offices, or warehouses in Pennsylvania must still collect sales tax once exceeding $100,000 in Pennsylvania sales.

When does my Pennsylvania collection obligation begin?

Your obligation begins immediately after crossing the $100,000 threshold—on the very next sale into Pennsylvania. Pennsylvania provides no grace period or delayed effective date.

Does the $100,000 threshold include exempt sales?

Yes. Pennsylvania measures the threshold based on gross sales—the total before deducting returns, allowances, or exempt items. Only after exceeding the threshold do exemptions matter for actual collection. Even wholesale and resale transactions count toward your threshold calculation.

What sales tax rate do I charge Pennsylvania customers?

Most of Pennsylvania charges 6% state sales tax. Allegheny County (Pittsburgh area) charges 7% combined (6% state + 1% local). Philadelphia charges 8% combined (6% state + 2% local). Remote sellers use destination-based sourcing, charge based on customer location.

Is clothing taxable in Pennsylvania?

Most clothing is exempt from Pennsylvania sales tax. However, formal wear, sporting goods, and certain accessories are taxable. The distinction creates complexity requiring careful product classification.