Ohio sales tax nexus determines whether your business must collect and remit sales tax in the Buckeye State. For e-commerce sellers shipping products into Ohio, understanding nexus became critical after the 2018 Wayfair decision allowed states to require remote sellers to collect tax based solely on economic activity.

Missing Ohio’s thresholds means potential back taxes, penalties, and audit headaches. Crossing them without proper registration creates the same problem. That’s where Hands Off Sales Tax (HOST) helps! Providing nexus analysis, registration services, and ongoing compliance management so you can focus on growing your business instead of decoding Ohio tax law.

What Is Sales Tax Nexus?

Sales tax nexus is the connection between your business and a state that creates a tax collection obligation. Once you establish nexus in Ohio, you must register for a sales tax permit, collect the appropriate tax from Ohio customers, and file returns with the Ohio Department of Taxation.

Physical nexus occurs when your business maintains a tangible presence in Ohio—employees, warehouse space, inventory, offices, or temporary activity like attending trade shows. Store products in an Ohio fulfillment center or employ remote workers living in Columbus? You’ve established physical nexus.

Economic nexus triggers based solely on sales volume or transaction count, regardless of physical presence. After the Supreme Court’s 2018 South Dakota v. Wayfair ruling, states gained authority to require out-of-state sellers to collect sales tax based on economic activity alone. Ohio adopted its economic nexus standard on August 1, 2019, replacing previous affiliate and click-through nexus provisions.

For most remote sellers, economic nexus is what matters.

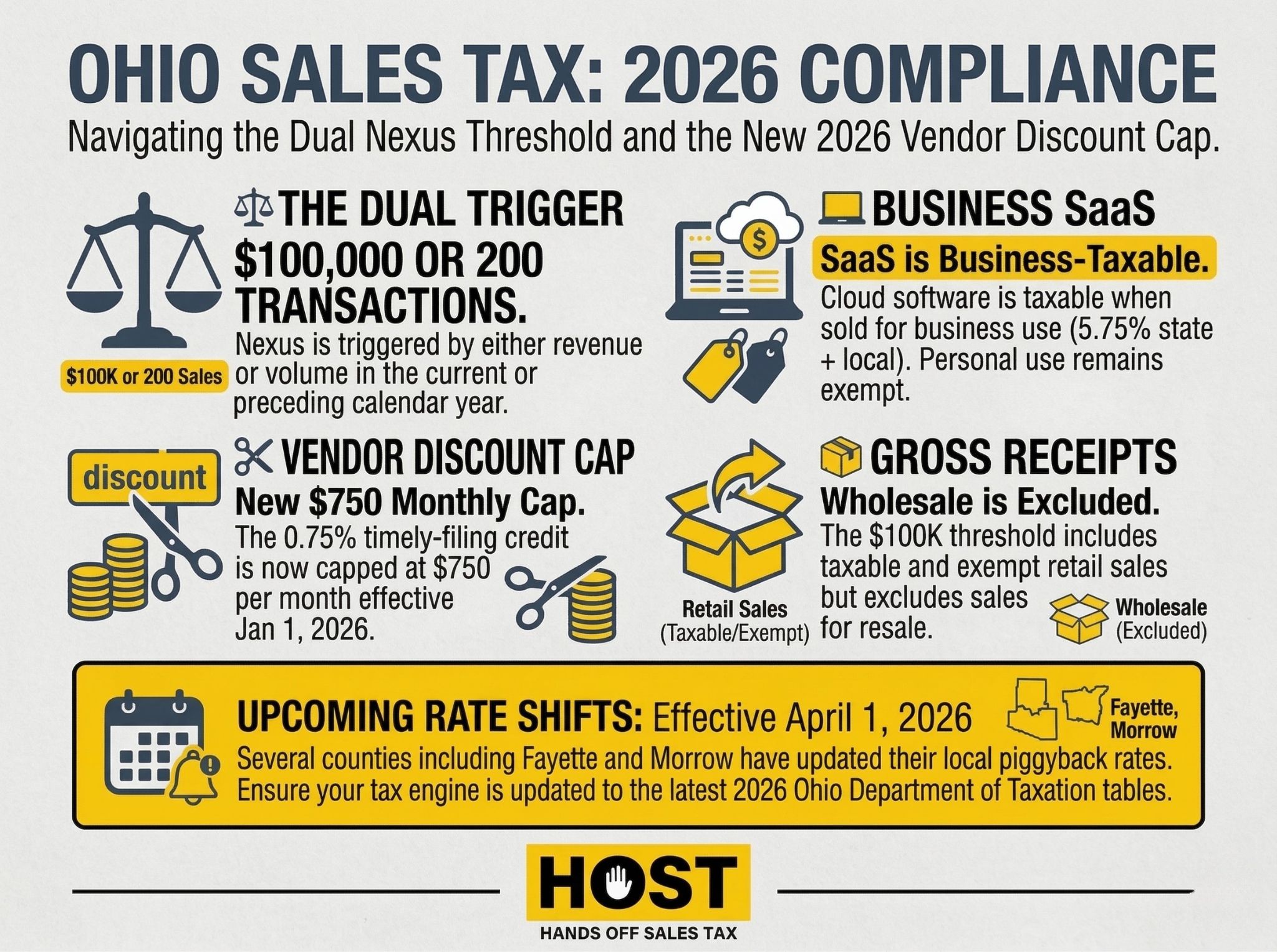

Ohio Economic Nexus Thresholds

Ohio requires remote sellers to collect sales tax once they exceed $100,000 in gross receipts OR 200 or more separate transactions from sales into Ohio during the current or preceding calendar year. Meeting either threshold triggers nexus.

The $100,000 calculation includes all retail sales to Ohio customers, whether taxable or exempt. Even if you sell exempt goods, those sales count toward the threshold. However, Ohio excludes wholesale transactions from the calculation. The 200-transaction threshold counts all separate retail transactions delivered into Ohio.

Ohio implemented its economic nexus law on August 1, 2019, following Wayfair. Since then, thousands of remote sellers have registered for Ohio sales tax permits.

Key point: Ohio uses a “current or preceding calendar year” measurement. Exceeded $100,000 in Ohio sales OR 200 transactions during 2024? You have nexus throughout 2025, even if 2025 volume drops below the thresholds.

How to Determine If You Have Ohio Nexus

Start by analyzing your Ohio sales data over the past two calendar years. Pull reports from your e-commerce platform, accounting software, or sales tax automation tool showing total gross receipts from Ohio customers.

Step 1: Calculate your Ohio gross receipts and transaction count for the current calendar year (year-to-date).

Step 2: Calculate your Ohio gross receipts AND transaction count for the preceding calendar year (full year).

Step 3: If either year exceeds $100,000 OR 200 transactions, you have economic nexus in Ohio.

Most e-commerce platforms can generate sales reports filtered by state. If you use sales tax software like TaxJar or Avalara, nexus monitoring features often alert you when approaching state thresholds.

Don’t forget physical nexus triggers: inventory at third-party logistics providers, employees working remotely in Ohio, or drop-shipping arrangements where suppliers ship from Ohio on your behalf.

HOST offers comprehensive nexus analysis services, examining your sales footprint across all states to identify exactly where you’ve triggered obligations, including Ohio’s specific rules.

What Happens After You Cross Ohio’s Threshold

Once you establish nexus, registration obligations begin on the first day of the month following at least 30 days after crossing either threshold. For example, if you meet the threshold on January 20, you must register by March 1.

Ohio registration occurs through the Ohio Business Gateway, the state’s online portal. You’ll need your FEIN or SSN, business legal name and structure, business address, estimated monthly sales tax liability, and banking information for electronic payments.

The state issues your Ohio Vendor’s License electronically. There’s no registration fee, though Ohio requires a $50 security deposit from some out-of-state sellers depending on projected volume.

After registration, you must collect Ohio sales tax on all taxable sales to Ohio customers. Ohio’s state rate is 5.75%, but most transactions also include county and transit authority taxes. Combined rates range from 6.5% to 8%. Cleveland charges 8%, Columbus 7.5%, and Cincinnati 7.8%.

Ohio assigns filing frequencies based on estimated tax liability: monthly (over $2,400 annual), quarterly ($600-$2,400 annual), or annual (under $600 annual). New registrants typically start with monthly filing until Ohio reviews actual collections. All returns are filed electronically through the Ohio Business Gateway, with payment due on the 23rd of the month following the reporting period.

HOST manages the entire registration process and files your Ohio returns on schedule, so you never miss a deadline.

Common Ohio Sales Tax Exemptions

Understanding what Ohio taxes helps you collect correctly.

Generally Taxable:

- Tangible personal property (physical goods)

- Digital products for business use (software, streaming, downloads)

- Software-as-a-Service (SaaS) for business use

- Clothing and apparel

Important distinction: Ohio taxes SaaS and digital products only when sold for business purposes. Sales for personal use are not taxable.

Generally Exempt:

- Groceries (unprepared food for home consumption)

- Prescription drugs and prosthetic devices

- Newspapers and magazines (by subscription)

- Manufacturing machinery and equipment

- Sales for resale (wholesale transactions)

- Custom software developed for specific clients

When selling exempt items, obtain proper exemption certificates from customers. Ohio accepts the Multistate Tax Commission’s Uniform Sales & Use Tax Certificate.

Marketplace Facilitator Laws

Ohio’s marketplace facilitator law, effective October 1, 2019, requires platforms like Amazon, eBay, Etsy, and Walmart Marketplace to collect and remit sales tax on behalf of third-party sellers.

Sell exclusively through marketplace facilitators? You likely don’t need to register. The platform handles collection and remittance. However, track your sales for nexus purposes in states where you sell through other channels.

Critical distinction: Sell both on marketplaces and through your own website? You must register and collect tax on your direct sales once you cross Ohio’s threshold. Your total Ohio sales (marketplace + direct) determine nexus, but you only collect tax on sales the marketplace doesn’t handle.

HOST helps sort through these scenarios, determining your precise obligations across all sales channels.

Penalties for Non-Compliance

Ohio enforces sales tax compliance aggressively. Failing to register, collect, or remit tax after establishing nexus exposes your business to:

- Late filing: $50 or 10% of tax due (whichever is greater)

- Late payment: 15% of unpaid tax for the first month, then 5% per month up to 50%

- Interest on unpaid tax (typically 3-7% annually)

- Lookback period: Four years from when a return was due, or indefinitely in cases of fraud

Consider a seller who crossed Ohio’s threshold in January 2023 but didn’t register until an audit notice in January 2025. They owe two years of uncollected tax (which they must pay from their own funds), plus penalties up to 50%, plus interest, which is potentially tens of thousands of dollars.

Voluntary Disclosure Agreements: Limiting Past Liability

Discovered you should have been collecting Ohio sales tax but weren’t? A Voluntary Disclosure Agreement (VDA) can limit damage.

Ohio’s VDA program allows businesses to come forward voluntarily, typically limiting the lookback period to three years and waiving many penalties. You’ll owe back taxes and interest, but avoid the worst financial consequences.

HOST facilitates VDAs with Ohio and other states, negotiating on your behalf to minimize lookback periods, secure penalty abatement, and resolve past obligations.

Multi-State Compliance: Beyond Ohio

Ohio is rarely the only state where you’ll have nexus. E-commerce businesses typically trigger thresholds in multiple states as they grow.

Each state maintains different rules: varying thresholds, lookback periods, marketplace facilitator laws, and product taxability. Managing compliance across 45+ sales tax states means tracking thresholds, registering in each state, calculating varying rates, filing on different schedules, and responding to notices from multiple tax authorities.

This complexity explains why most growing e-commerce businesses eventually seek professional help.

HOST: Your Partner for Ohio Sales Tax Compliance

Hands Off Sales Tax specializes in multi-state sales tax compliance for e-commerce businesses. We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate obligations in Ohio and nationwide.

What HOST Delivers:

- Nexus Analysis: We analyze your sales data to determine exactly where you’ve triggered nexus

- Sales Tax Registration: We handle Ohio registration through the Business Gateway

- Sales Tax Filings: We prepare and file your Ohio returns on schedule

- Notice Management: We interpret and respond to Ohio Department of Taxation notices

- Audit Defense: We’re your trusted partner in resolving Ohio sales tax audits

- VDA Support: We file voluntary disclosures to limit lookback periods and abate penalties

Through our parent company TaxMatrix, we’ve helped North America’s largest companies manage sales tax requirements. Now we bring that enterprise expertise to small and mid-sized e-commerce sellers.

You handle the sales, we handle the tax.

Ready to Get Ohio Compliant?

Ohio sales tax nexus affects thousands of remote sellers who never set foot in the state. Understanding when you’ve crossed the threshold prevents costly penalties while letting you focus on business growth.

Whether you’re newly crossing Ohio’s thresholds, managing nexus in multiple states, or discovering past obligations that need resolution, the right sales tax partner eliminates guesswork and prevents expensive mistakes.

At HOST, we combine 25+ years of specialized experience with transparent communication and personalized support. When you’re ready to take Ohio sales tax off your plate, we’re ready to help.

Contact us today to discuss your Ohio compliance needs or schedule a free consultation.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the Ohio sales tax nexus threshold for remote sellers?

Ohio requires remote sellers to collect sales tax once they exceed $100,000 in gross receipts OR 200 or more separate transactions from Ohio sales during the current or preceding calendar year. Meeting either threshold triggers nexus.

Do marketplace sales count toward Ohio’s nexus threshold?

Yes, all sales to Ohio customers count toward the thresholds, including sales made through marketplace facilitators. However, if the marketplace collects tax on your behalf, you don’t need to collect it again. You only collect on direct sales through other channels.

What happens if I crossed Ohio’s threshold but haven’t registered?

You’re technically required to register, collect, and remit sales tax once nexus is established. If you discover past obligations, consider a Voluntary Disclosure Agreement to limit lookback periods and penalty exposure. HOST can help negotiate favorable terms.

Does Ohio charge sales tax on digital products and SaaS?

Ohio taxes digital products and SaaS when sold for business purposes, including downloaded software, cloud subscriptions, and streaming services. However, these same products are not taxable when sold for personal use.

How often do I need to file Ohio sales tax returns?

Ohio assigns filing frequencies based on your tax liability: monthly (over $2,400 annual), quarterly ($600-$2,400 annual), or annual (under $600 annual). New registrants typically start with monthly filing.

Can HOST help with Ohio sales tax compliance?

Absolutely. HOST provides comprehensive Ohio sales tax services including nexus analysis, registration, ongoing filing management, notice response, audit defense, and voluntary disclosure agreements. We handle everything so you can focus on running your business.