Understanding Ohio’s sales tax filing frequency is essential for businesses to maintain compliance and avoid costly penalties. Whether you’re launching your first venture or scaling an established operation, knowing when to file keeps you ahead of obligations rather than scrambling to catch up.

That’s where Hands Off Sales Tax (HOST) steps in, ensuring businesses never miss a deadline while you focus on what actually drives revenue.

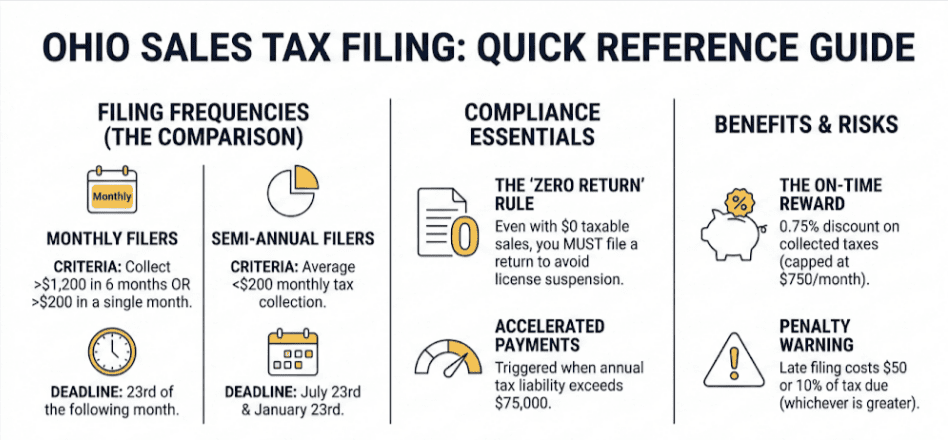

Understanding Filing Frequencies

Ohio categorizes businesses into two primary filing schedules: monthly and semi-annual. Your assignment depends entirely on how much tax you collect.

Monthly Filers

If your business collects more than $1,200 in sales tax over six months, or exceeds $200 in any single month, you’re filing monthly. Returns are due by the 23rd of the following month. January sales by February 23rd, and so on. When the 23rd lands on a weekend or holiday, you get until the next business day.

Semi-Annual Filers

Businesses averaging under $200 monthly in tax collections qualify for semi-annual filing. You’ll submit twice yearly: by July 23rd for January through June, and by January 23rd for the July-December period.

The Quarterly Exception

Quarterly filing exists in Ohio, but it’s reserved for consumer use-tax accounts and direct-pay permit holders, not standard vendor accounts. Regular businesses get monthly or semi-annual assignments based solely on collection volume.

How Filing Frequency Gets Determined

Initial Assignment

New businesses receive their filing frequency assignment from the Ohio Department of Taxation based on projected sales. Cross the $1,200 threshold in six months or hit $200 in any month? You’re filing monthly. Stay below that? Semi-annual will work.

If you’re uncertain about projections, working with a sales tax professional eliminates guesswork before problems surface.

Frequency Adjustments

As your business evolves, so might your filing schedule. The Ohio Department of Taxation adjusts frequencies based on actual performance. Growing businesses often shift from semi-annual to monthly as collections increase.

There’s a penalty trigger too: businesses that repeatedly file late can be forced onto monthly schedules regardless of collection amounts. The state uses frequency as both a tracking mechanism and a compliance tool.

Accelerated Payments

Once annual tax liability exceeds $75,000, accelerated payments kick in. You’ll prepay 75% of the average from your previous four months’ liability. The prior month’s accelerated payment offsets the current month’s total. It’s Ohio’s way of ensuring large collectors don’t accumulate massive liabilities between filing deadlines.

Avoiding Common Compliance Mistakes

Misunderstanding Your Filing Schedule

Confusion about filing frequency tops the list of business mistakes. You might assume you’re semi-annual when you’ve actually crossed into monthly territory, then miss three consecutive deadlines before realizing the problem.

Monitor your tax collections continuously. If you’re approaching $1,200 over six months or $200 in any month, prepare for monthly filing before the state forces the issue.

Skipping Zero Returns

Even months with zero taxable sales require filing. Ohio mandates returns for every assigned period, regardless of activity. Skip a zero return and you’re facing penalties or license suspension. Same consequences as missing a return with actual liability.

Filing Incomplete Returns

Double-check entries before submission. Incomplete or inaccurate returns trigger penalties and interest charges that compound fast. Using accounting software helps, but only if configured correctly. HOST’s sales tax filing services eliminate manual entry errors entirely.

Overlooking Accelerated Payments

Businesses hitting the $75,000 annual threshold often miss accelerated payment obligations. These are required prepayments that keep large collectors current. Missing them means late fees and potential audits.

Why Timely Filing Matters

Penalty Avoidance

Late filing costs a minimum of $50 or 10% of tax due. Whichever hurts more. Interest accrues daily on unpaid balances. A $5,000 tax bill filed 60 days late easily becomes $6,000+ after penalties and interest compound.

The Vendor Discount

File on time and Ohio rewards you with a 0.75% discount on collected taxes, capped at $750 per license monthly as of January 2026. For high-volume retailers, that’s meaningful savings—up to $9,000 annually in reduced liability.

Motor vehicle dealers remain exempt from the cap, but everyone else maxes out at $750 per month. Still, consistent compliance turns into five-figure annual savings for businesses processing significant volume.

Registration and Filing Mechanics

Getting Your License

Register through the Ohio Business Gateway. In-state vendors pay a $25 fee; out-of-state remote sellers register free. Have your EIN, business structure details, and projected sales ready.

Electronic Filing Requirements

Ohio requires electronic filing through the Business Gateway. Paper returns exist only for rare exceptions. The portal accepts ACH and credit card payments. Schedule them early to avoid last-minute technical issues derailing your compliance.

What You’ll Need

Accurate sales records, collected tax amounts, and exemption certificates for non-taxable transactions. Missing documentation during an audit means penalties even if you filed on time. HOST handles documentation management as part of comprehensive sales tax services.

How HOST Simplifies Ohio Compliance

Managing sales tax filing frequencies, tracking thresholds, calculating accelerated payments, and ensuring zero returns get filed, it’s all administrative overhead that generates zero revenue while consuming finite time.

Hands Off Sales Tax offers complete solutions:

- Sales Tax Registration – We handle Ohio licensing and multi-state registration

- Nexus Analysis – Determine exactly where you have obligations before problems surface

- Filing and Remittance – Every return filed correctly and on time, including zero returns

- Audit Defense – Expert representation if the state comes knocking

- Free Sales Tax Software Review – Identify configuration errors costing you money

We’ve been exclusively focused on sales tax for over 25 years. That depth of specialization means we catch nuances general accountants miss, such as Ohio’s accelerated payment calculations or the new vendor discount caps.

What About Marketplace Sales?

If you sell through Amazon, Etsy, or other marketplace facilitators, those platforms collect and remit Ohio sales tax on your behalf; however, you still need to report these sales correctly because they appear in your gross sales figures but get entered as exempt transactions.

Critical distinction: Marketplace sales don’t count toward economic nexus thresholds. But if you also make direct sales outside the marketplace and cross the $100,000 or 200-transaction threshold, you need to register and file returns showing all sales with proper exemptions claimed.

Understanding Payment vs. Filing Deadlines

Here’s a nuance many businesses miss: Ohio processes payments separately from return submissions. While both are due by the 23rd, the state requires an extra business day to process payments. In practice, this means you cannot file your return without simultaneously remitting payment through the Ohio Business Gateway.

Unlike some states where you can file first and pay later, Ohio links the two functions. Your return submission won’t process until payment clears.

Audit Triggers and Record Retention

Ohio requires businesses to maintain all sales tax records for at least four years. During audits, examiners review:

- Sales tax returns and payment history

- Exemption certificates for non-taxable transactions

- Documentation supporting claimed exemptions

- County-by-county sales allocation accuracy

Common audit triggers include consistently late filings, significant discrepancies between reported sales and economic indicators, and failure to respond to state notices. Businesses that properly manage exemption certificates and maintain organized records typically resolve audits faster with minimal adjustments.

If you disagree with audit findings, you have 60 days to file a petition for reassessment with the Tax Commissioner.

The CAT Tax Confusion

Don’t confuse Ohio’s sales tax with the Commercial Activity Tax (CAT). The CAT applies a 0.26% tax on gross receipts exceeding $150,000 annually, completely separate from sales tax obligations. CAT filing occurs quarterly regardless of your sales tax filing frequency.

This guide addresses only sales tax filing frequencies. CAT obligations require separate analysis and compliance.

Requesting Filing Frequency Changes

Businesses can request filing frequency changes through the Ohio Department of Taxation. The Commissioner may approve changes that improve compliance or increase administrative efficiency.

For example, if your business experiences seasonal fluctuations and semi-annual filing would better match your cash flow, you can petition for a change. However, the state retains discretion. Chronic late filers get moved to monthly regardless of collection volume.

Take Control of Compliance

Ohio sales tax filing isn’t complex, but it’s unforgiving. Cross a threshold and miss the frequency change? Penalties. Forget a zero return? License suspension. Miscalculate accelerated payments? Interest compounds.

The businesses that thrive don’t spend their energy on compliance mechanics, they delegate that work to specialists and focus on growth, product development, and customer relationships.

Contact HOST today to discuss your Ohio sales tax needs. We’ll ensure you’re collecting correctly, filing on time, and maximizing that vendor discount while you get back to running your business.

Frequently Asked Questions

What happens if I file late in Ohio?

Late filing triggers penalties of $50 or 10% of tax due (whichever is greater), plus daily interest charges. Chronic late filing can force your business onto monthly filing schedules regardless of collection volume, and repeated violations may result in license suspension.

Do I need to file if I had no sales during the period?

Yes. Ohio requires zero returns for every assigned filing period. Skipping a zero return carries the same penalties as failing to file a return with actual liability. The state uses zero returns to confirm your business remains active and compliant.

How do marketplace sales like Amazon affect my filing?

Marketplace facilitators collect and remit sales tax on your behalf, so you don’t owe tax on those transactions. However, you must report marketplace sales in your gross sales figures and claim them as exempt. If you also make direct sales outside marketplaces, track both channels separately to ensure accurate reporting.

Can I change my filing frequency?

Yes, but the Ohio Department of Taxation must approve your request. Changes are typically granted when they improve compliance or administrative efficiency. Submit your request through the Ohio Business Gateway, explaining why a different frequency better suits your business cycle.

What’s the difference between sales tax and the CAT tax?

Sales tax is a consumption tax on retail transactions that you collect from customers. The Commercial Activity Tax (CAT) is a 0.26% tax on your business’s gross receipts exceeding $150,000 annually. They’re separate obligations with different filing schedules. Sales tax follows your assigned frequency, while CAT is always quarterly.

How long must I keep Ohio sales tax records?

Ohio requires four-year retention of all sales tax documentation, including returns, exemption certificates, transaction records, and supporting documentation. During audits, examiners review these records to verify compliance. Organized record-keeping significantly reduces audit duration and potential adjustments.