Understanding North Carolina’s economic nexus threshold matters when one busy quarter suddenly puts you on the hook for mandatory tax collection, often without realizing it until a notice arrives from the North Carolina Department of Revenue.

North Carolina requires remote sellers to register and collect sales tax once they exceed $100,000 in gross sales sourced to the state in the current or previous calendar year. That’s the simplified version effective July 2024. Before that, sellers also tracked whether they made 200 or more separate transactions, creating dual compliance headaches.

For online sellers juggling dozens of state requirements, keeping up with North Carolina’s rules while monitoring thresholds, registering correctly, and filing on time creates operational strain. That’s where Hands Off Sales Tax (HOST) makes multi-state compliance manageable. Determining exactly where you’ve triggered nexus, handling registrations, and filing returns so North Carolina’s threshold becomes another detail we manage while you focus on growth.

What Is Economic Nexus in North Carolina?

Economic nexus establishes a connection between your business and North Carolina based on sales volume alone. No physical presence required. After the 2018 South Dakota v. Wayfair Supreme Court decision, states gained authority to require out-of-state sellers to collect sales tax based on economic activity.

North Carolina implemented its economic nexus law on November 1, 2018, initially requiring remote sellers to collect tax if they exceeded either $100,000 in gross sales or 200 separate transactions in the current or previous calendar year. This dual-threshold approach forced businesses to monitor two separate metrics.

Effective July 1, 2024, North Carolina eliminated the 200-transaction threshold entirely. Governor Roy Cooper signed HB 228 on July 1, 2024, and it took effect immediately. North Carolina became the third state in 2024 to repeal its transaction count requirement, following Indiana and Wyoming.

This change simplified compliance significantly. Sellers now track only gross sales (not individual transaction counts) when determining North Carolina nexus obligations.

North Carolina’s Current Economic Nexus Threshold

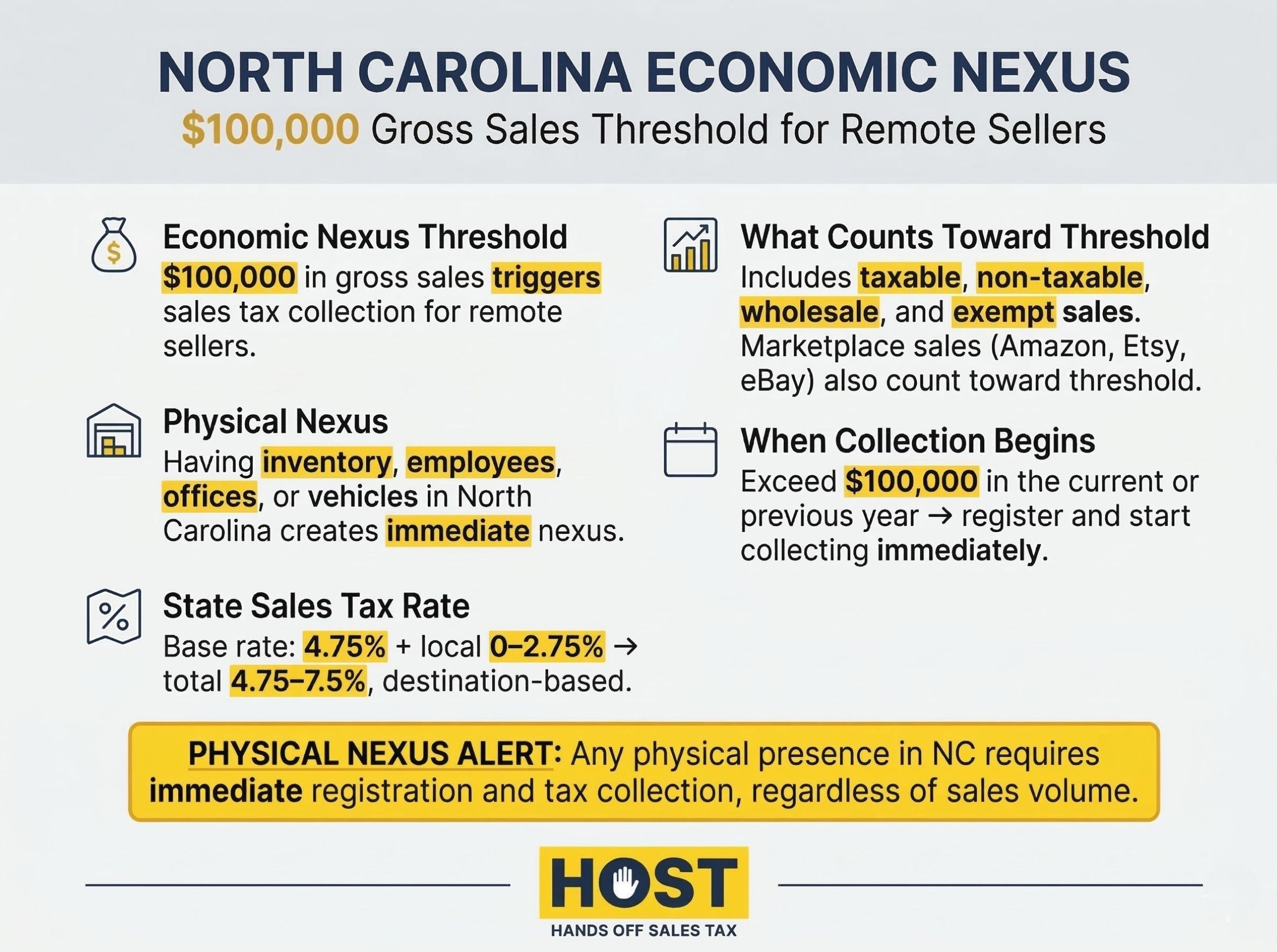

North Carolina’s economic nexus threshold is $100,000 in gross sales sourced to the state in the current or previous calendar year. Cross that threshold in either timeframe, and you’re required to register, collect, and remit sales tax immediately.

What Counts Toward the Threshold?

North Carolina casts a wide net when calculating whether you’ve crossed $100,000. Non-taxable sales, resale transactions, wholesale sales, and exempt sales all count toward the economic nexus threshold. Even transactions where you don’t collect tax because the customer provided an exemption certificate still count.

The threshold includes the sum total sales price of tangible personal property, digital property, and services sourced to North Carolina. This means SaaS subscriptions, digital downloads, and software licenses count just as much as physical products.

Sales made through marketplace facilitators like Amazon, Etsy, or eBay are included in your threshold calculation. While the marketplace handles tax collection on those sales, they still count when determining whether you’ve triggered North Carolina nexus through your direct sales channels.

Example: You made $60,000 in taxable retail sales, $25,000 in wholesale transactions (with valid resale certificates), and $20,000 through Amazon FBA to North Carolina customers. Your total gross sales equal $105,000 and you’ve exceeded the threshold even though only $60,000 required you to collect tax. All three categories count toward determining nexus.

Physical Presence Still Triggers Nexus

Economic nexus isn’t the only way to create North Carolina sales tax obligations. Physical nexus arises from maintaining an office, warehouse, or inventory in the state, selling from company-owned vehicles, owning income-producing property, or having employees working in the state.

If you have physical presence, the $100,000 threshold doesn’t matter. You must collect North Carolina sales tax regardless of sales volume.

Who Must Register for North Carolina Sales Tax?

All remote sellers with gross sales exceeding $100,000 sourced to North Carolina in the previous or current calendar year must register to collect and remit sales and use tax. Registration must happen immediately after crossing the threshold. There’s no grace period.

Marketplace facilitators must collect and remit sales tax if they exceed $100,000 in gross sales sourced to North Carolina, including both their direct sales and all third-party marketplace sales they facilitate.

For marketplace sellers, this creates a nuanced situation: your marketplace sales count toward your nexus threshold, but the marketplace collects the tax on those transactions. However, if you also make direct sales through your own website, you’re responsible for collecting tax on those once you cross the threshold.

When Registration Is Required

North Carolina requires registration immediately after establishing economic nexus. The “current or previous calendar year” language creates what’s effectively a trailing nexus situation.

Here’s how it works: If your 2024 sales into North Carolina exceeded $100,000, you have nexus throughout 2025, even if your 2025 sales drop to $80,000. You’re evaluated on either timeframe. Only after a full calendar year below $100,000 (and the prior year also below threshold) can you potentially cancel registration.

This means once you cross the threshold, you maintain nexus obligations for at least the remainder of the current year plus the entire following year. Plan accordingly when projecting compliance costs and obligations.

What Changed in July 2024?

Between November 1, 2018, and June 30, 2024, North Carolina’s economic nexus threshold required either more than $100,000 in gross sales or 200 or more separate transactions. Businesses selling lower-priced items could trigger nexus through transaction count long before hitting the sales threshold.

The repeal of the 200-transaction requirement means some remote sellers who previously had nexus may no longer meet the threshold. North Carolina joined 12 other states that have eliminated transaction thresholds as of mid-2024, recognizing that transaction counts unfairly burden small sellers of low-value items.

Canceling Your Registration After the Change

If you were registered solely because of transaction count but never exceeded $100,000 in sales, you can cancel your North Carolina registration by filing Form NC-BN (Out-of-Business Notification), available at www.ncdor.gov.

To qualify for cancellation, you must meet these requirements:

- Did not make gross sales exceeding $100,000 in 2023

- Have not made gross sales exceeding $100,000 from January 2024 through your cancellation date

- Are not otherwise engaged in business in North Carolina (no physical presence)

Critical detail: List your desired end date in the “Date of Permanent Closure” field. This date must be on or after the date you file the form. You must continue collecting and remitting sales tax and filing returns until your cancellation is officially processed.

HOST’s nexus analysis service helps you determine whether canceling North Carolina registration makes strategic sense, considering your sales trajectory and compliance goals.

How to Register for North Carolina Sales Tax

North Carolina offers two registration paths: direct registration with the state or through the Streamlined Sales Tax (SST) system.

Remote sellers can register directly with North Carolina using the Department’s online business registration portal or by submitting Form NC-BR. There is no fee to apply for a certificate of registration.

North Carolina is a member of the Streamlined Sales Tax Governing Board, allowing remote sellers to register with all 24 member states by completing one online application. This approach works well if you’ve triggered nexus in multiple Streamlined states simultaneously.

HOST handles sales tax registration in all required states, including North Carolina. We complete the paperwork, follow up on applications, track approval timelines, and ensure you receive your certificate of registration without diverting your attention from business operations.

North Carolina’s Destination-Based Sales Tax System

North Carolina uses a destination-based sales tax system, meaning the customer’s ship-to address determines the applicable sales tax rate. You must charge the rate for where your customer receives the product, not where your business operates.

North Carolina’s base state sales tax rate is 4.75%, with local rates ranging from 0% to 2.75%, creating total rates between 4.75% and 7.5%. Combined state and local rates vary by county and municipality, requiring address-level tax calculation.

Food sellers note: North Carolina exempts groceries from the 4.75% state portion but applies 2% local sales tax to food. “Non-qualifying food” including prepared foods at restaurants, dietary supplements, vending machine items, and bakery items sold with eating utensils, faces the full combined rate. This nuance matters significantly for restaurant and grocery businesses.

For e-commerce businesses shipping to dozens of North Carolina addresses daily, calculating the correct rate manually is impractical. Sales tax automation software calculates rates based on ship-to address, but proper configuration is critical to avoid overcharging customers or underremitting tax.

HOST offers a free sales tax software review to identify configuration errors like incorrectly taxing exempt items, missing required local taxes, or double-taxing due to system overlaps before they create audit liability or damage customer relationships.

Common Compliance Mistakes for North Carolina Sellers

Many sellers track only taxable revenue when evaluating nexus thresholds. In North Carolina, this creates exposure. Non-taxable sales, wholesale transactions, and exempt sales all count toward the $100,000 threshold even though no tax is collected.

Even though marketplace facilitators collect tax on your behalf for marketplace sales, those sales are still counted toward your economic nexus threshold. If you made $80,000 in direct sales through your website plus $30,000 through Amazon FBA shipped to North Carolina customers, you’ve exceeded the threshold at $110,000 total.

Remote sellers must register and begin collecting sales tax immediately after establishing economic nexus. Delays create retroactive liability, if the state identifies you should have been collecting, they can assess back taxes, penalties, and interest from the date you crossed the threshold.

What E-Commerce Businesses Need to Know

Understanding North Carolina’s threshold is just one piece of a 45-state compliance puzzle. Most successful e-commerce businesses trigger nexus in 10-20+ states simultaneously as they scale, each with different thresholds, filing frequencies, and local tax rules.

Managing this complexity internally typically consumes 30+ hours monthly, tracking thresholds across states, registering in new jurisdictions, calculating correct rates, filing returns, handling notices, and responding to audits. That’s 360+ hours annually that generate zero revenue.

HOST’s comprehensive sales tax services eliminate this drain:

Nexus Analysis: We analyze your sales data to determine exactly where you’ve met economic or physical nexus thresholds across all states, including North Carolina’s $100,000 threshold.

Sales Tax Registration: We handle registrations with every applicable state taxing jurisdiction, completing paperwork and managing follow-up.

Ongoing Filing: We file your returns monthly, quarterly, or annually based on each state’s requirements, including North Carolina’s local returns.

Notice Management: When North Carolina or any state sends a confusing notice, we interpret what it means and respond appropriately.

Audit Defense: We’re your trusted partner in resolving sales tax audits, organizing documentation and defending your position.

Voluntary Disclosure Agreements: If you discover past North Carolina nexus you didn’t know about, we file VDAs to limit look-back periods and abate penalties.

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate compliance. Co-founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

North Carolina Nexus: Peace of Mind Through Expert Management

North Carolina’s economic nexus threshold might seem straightforward. $100,000 in gross sales triggers collection obligations. But calculating what counts toward that threshold, determining when to register, managing destination-based rate calculations, and handling ongoing filing creates real complexity.

Missing North Carolina’s threshold or delaying registration leads to back taxes, penalties, and audit exposure. Managing it yourself diverts focus from growth and customer experience.

When you’re ready to take North Carolina sales tax compliance (and all your multi-state obligations) off your plate, HOST is ready to help. Contact us today to discuss your needs or schedule a free consultation. Let’s ensure you’re collecting in the right states, handling obligations correctly, and staying ahead of threshold changes like North Carolina’s July 2024 update.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book to identify costly errors before they create audit problems.

Frequently Asked Questions

What is North Carolina’s economic nexus threshold?

North Carolina’s economic nexus threshold is $100,000 in gross sales sourced to the state in the current or previous calendar year. Exceed that amount in either timeframe, and you must register and collect sales tax immediately.

When did North Carolina remove the 200-transaction threshold?

North Carolina eliminated the 200-transaction requirement effective July 1, 2024, through HB 228 signed by Governor Roy Cooper. The state now uses sales volume only when determining economic nexus.

Do exempt sales count toward the North Carolina threshold?

Yes, non-taxable sales, wholesale transactions, resale sales, and exempt sales all count toward North Carolina’s $100,000 economic nexus threshold even though no tax is collected on those transactions. Track total gross sales, not just taxable revenue. This includes digital property like SaaS subscriptions and software licenses.

Do marketplace sales count toward my North Carolina threshold?

Yes, sales made through marketplace facilitators are included in your threshold calculation. While Amazon, Etsy, or eBay collects tax on those sales, they still count when determining whether you’ve triggered nexus through your direct sales.

Can I cancel my North Carolina registration after the July 2024 change?

Remote sellers may cancel their North Carolina registration if they did not exceed $100,000 in gross sales during 2023 and have not exceeded $100,000 from January 2024 through the cancellation date. Cancellation isn’t automatic. You must submit the request.

How is North Carolina sales tax calculated?

North Carolina uses a destination-based system, meaning the customer’s ship-to address determines the applicable sales tax rate. The base state rate is 4.75%, with local rates adding 0-2.75%, creating total rates between 4.75% and 7.5%.