Minnesota economic nexus determines when your e-commerce business must collect sales tax in the state, even without physical presence. Cross the threshold, and you’re legally required to register, collect, and remit. Miss it, and you’re facing back taxes, penalties, and audit exposure that can cripple cash flow.

At Hands Off Sales Tax (HOST), we’ve helped businesses navigate Minnesota economic nexus for over 25 years. From nexus analysis to registration and ongoing compliance, our team ensures you’re collecting in the right states without the headache of tracking changing rules.

What Is Economic Nexus in Minnesota?

Economic nexus is the connection between your business and Minnesota based purely on sales activity—no physical presence required. Once you exceed Minnesota’s threshold through sales to state residents, you’ve triggered a tax collection obligation.

Minnesota’s economic nexus law went into effect October 1, 2018, shortly after the Supreme Court’s Wayfair ruling. The law applies to “remote sellers” like businesses selling tangible personal property, digital goods, or taxable services into Minnesota from outside the state.

This differs fundamentally from physical nexus, which requires an office, warehouse, employee, or inventory in Minnesota. Economic nexus captures purely digital commerce: operate entirely from California, sell through your website to Minnesota customers, and you still owe Minnesota sales tax.

The Minnesota Department of Revenue enforces these rules aggressively. They have access to marketplace data, third-party reporting, and sophisticated tracking that identifies non-compliant sellers. Assuming you’re “too small to notice” is a costly mistake.

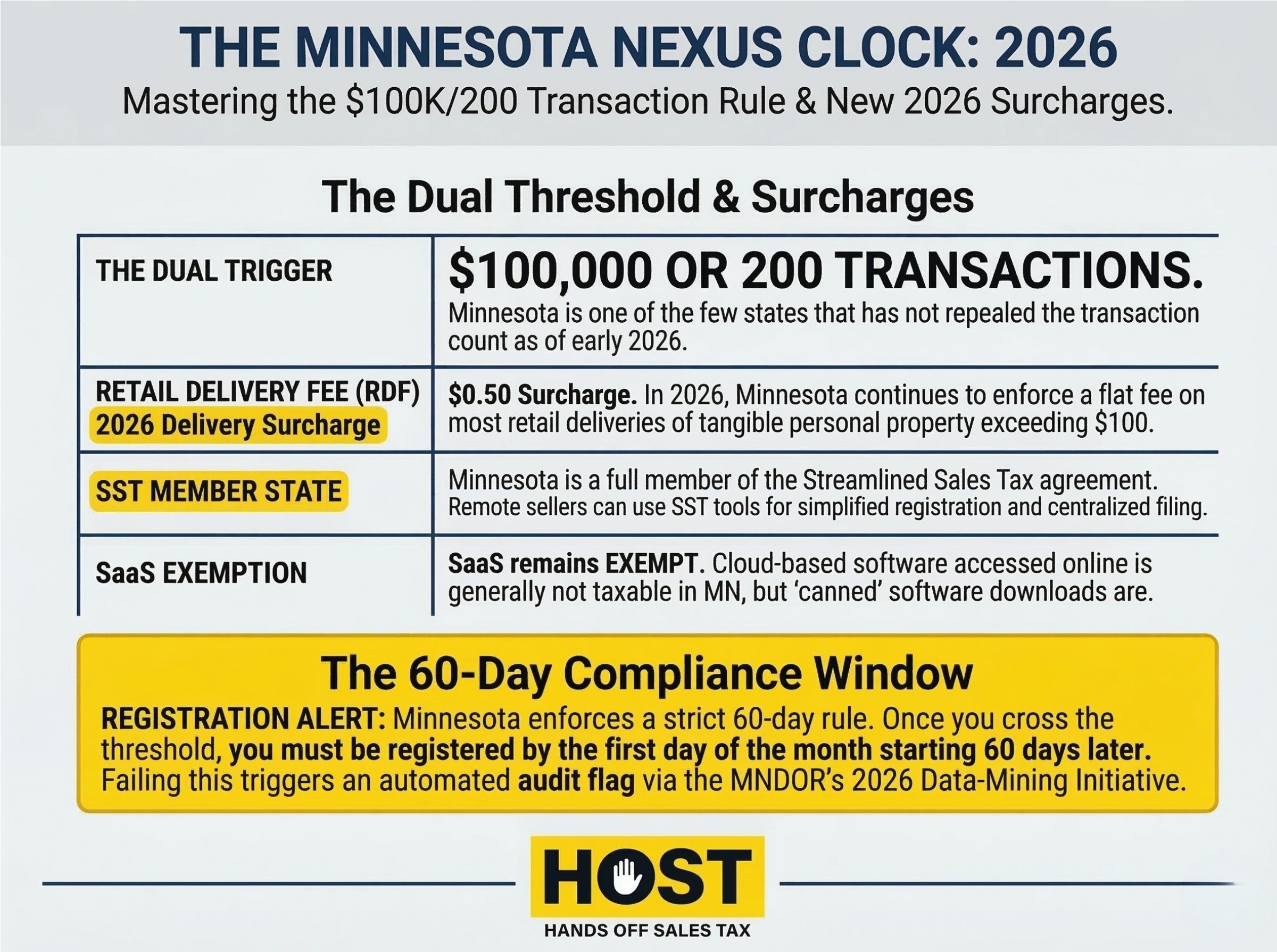

Minnesota Economic Nexus Thresholds

Minnesota uses a dual threshold: $100,000 in retail sales OR 200 separate retail transactions to Minnesota customers in the previous 12-month period or current calendar year.

Meeting either threshold triggers nexus. Sell $100,001 or complete 200 transactions to Minnesota residents, and you’ve crossed nexus.

Key Details on the Threshold

Retail sales only: The $100,000 counts only retail sales of tangible personal property, digital products, and taxable services delivered to Minnesota. Wholesale transactions and exempt sales don’t count.

Delivered to Minnesota: What matters is where the customer receives the product. Ship to a Minnesota address, and it counts, even if the customer placed the order while traveling elsewhere.

12-month or calendar year: Minnesota measures the threshold using either the prior 12 consecutive months or the current calendar year. Monitor both. If you exceed $100,000 in sales OR 200 transactions during any trailing 12-month period or during the current calendar year, nexus is triggered.

Cumulative across all sales channels: All your retail sales to Minnesota count: direct website sales, Amazon FBA, eBay, Etsy, social media sales. The state doesn’t care how customers found you.

When Registration Is Required

Once you exceed either threshold, you must register with the Minnesota Department of Revenue by the first day of the calendar month that begins no later than 60 days after crossing the threshold. Collection obligations begin immediately upon registration.

For example: You exceed the threshold on June 15. You must register by August 1 (the first day of a calendar month within 60 days). Collection obligations start August 1.

Many businesses make the mistake of waiting until they “settle in” or hit a higher number. Minnesota doesn’t grant grace periods. The 60-day clock for registration starts ticking the moment you cross either threshold.

What Counts Toward the Minnesota Threshold?

Understanding what sales count toward your threshold prevents surprises during an audit.

Sales That Count:

- Tangible personal property shipped to Minnesota addresses

- Digital products delivered to Minnesota customers (e-books, music downloads, videos, mobile apps)

- Taxable services provided to Minnesota residents

Note on Digital Products: Minnesota taxes specified digital products like e-books, digital audio, and digital video. However, SaaS (software-as-a-service) subscriptions accessed online are generally not taxable. If you sell both physical goods and digital products, both count toward your threshold calculation.

Sales That Don’t Count:

- Wholesale/resale transactions with valid Minnesota resale certificates

- Exempt sales (groceries, prescription drugs)

- Sales to tax-exempt organizations with valid exemption certificates

HOST’s nexus analysis service reviews your actual sales data to determine exactly when you crossed thresholds in Minnesota and every other state. No guesswork.

Marketplace Facilitator Laws and Economic Nexus

Minnesota’s marketplace facilitator law shifts collection responsibility to platforms for sales they facilitate. Amazon, eBay, Etsy, and Walmart Marketplace collect and remit Minnesota sales tax on your behalf for transactions processed through their systems.

Your marketplace sales still count toward the $100,000/200-transaction threshold, but you don’t collect tax on those specific transactions, the platform does.

Example Scenario

- Shopify sales to Minnesota: $60,000 (120 transactions)

- Amazon FBA sales to Minnesota: $50,000 (100 transactions)

- Total: $110,000 and 220 transactions

You’ve crossed nexus on both counts. Amazon collects tax on the $50,000 in FBA sales. You only collect on the $60,000 in Shopify sales. But both count toward determining nexus.

Minnesota Sales Tax Rates and Collection

Once registered, you’ll collect Minnesota sales tax at the point of sale. Minnesota uses a destination-based sales tax system, meaning tax rate depends on where the customer receives the product.

Minnesota State and Local Rates

Minnesota’s state sales tax rate is 6.875%. Local jurisdictions can add up to 2%, creating combined rates ranging from 6.875% to 8.375% or higher depending on the customer’s location. Minneapolis, for example, has a combined rate of approximately 8.025%.

You must calculate tax based on the customer’s delivery address down to the street level. A customer in Minneapolis (combined rate approximately 8.025%) pays more than a customer in areas with lower local rates.

With over 400 local tax jurisdictions in Minnesota, manual rate calculation is impractical. Most businesses use sales tax automation software. However, software must be properly configured. Incorrect rate assignment is one of the most common mistakes we see.

HOST offers a Free Sales Tax Software Review to identify configuration errors before they become expensive audit problems.

Registration and Filing Requirements

How to Register

Register online through the Minnesota Department of Revenue’s e-Services portal. You’ll need your business legal name, Federal EIN, business address, NAICS code, expected monthly sales volume, and the date you first exceeded the threshold.

Registration typically processes within 5-7 business days. You’ll receive a Minnesota Tax ID number and instructions for filing. Minnesota is a member of the Streamlined Sales Tax (SST) program, which can simplify multi-state registration if you’re registering in multiple states simultaneously.

Filing Frequency

Minnesota assigns filing frequency based on monthly tax liability:

- Monthly filing: Expected tax over $500/month

- Quarterly filing: Expected tax under $500/month

Most e-commerce businesses exceeding the threshold (often called the “Small Seller Exception” by Minnesota) will file monthly or quarterly. Returns are due the 20th of the month following the reporting period. If the 20th falls on a weekend or holiday, payment is due the next business day.

Late filing penalties start at 5% of tax due if up to 30 days late, increasing to 15% for returns over 60 days late. Interest accrues daily.

HOST handles all Minnesota filings for clients (monthly, quarterly, or annually) ensuring deadlines are met and returns are accurate. We file in all required states so you never miss a deadline.

Common Minnesota Economic Nexus Mistakes

Waiting Too Long to Register

The biggest mistake is exceeding the threshold and continuing to sell without registration. Every sale after crossing nexus generates liability.

Minnesota conducts regular compliance audits of remote sellers using marketplace data and third-party payment processors. Discovery leads to assessments of back taxes plus penalties and interest.

Ignoring Marketplace Sales

Your Amazon and Etsy sales count toward the threshold even though those platforms collect the tax. Focusing only on your website sales understates your actual Minnesota volume and leaves you non-compliant.

Miscalculating Local Rates

Minnesota’s destination-based system requires precise address-level rate calculation. Applying only the state rate (6.875%) when a customer’s location has local taxes creates undercollection, exposing you to audit liability.

Not Monitoring Threshold Continuously

Nexus isn’t a one-time calculation. You must monitor on a rolling 12-month basis and within the current calendar year. Businesses that checked once in January but had rapid summer growth miss the moment they cross nexus mid-year.

HOST’s ongoing nexus monitoring tracks your sales across all states continuously, alerting you when new thresholds are crossed.

What If You’re Already Non-Compliant?

Discovering you’ve been selling into Minnesota past the threshold without collecting tax is stressful. Ignoring it makes it worse.

Minnesota offers a Voluntary Disclosure Program (VDP) that limits lookback periods and abates penalties for sellers who come forward before an audit begins. Typically, VDP limits lookback to 3 years and can reduce or eliminate penalties.

HOST has extensive experience filing VDAs across all states, including Minnesota. We handle all communications with the Department of Revenue, organize your historical sales data, calculate liabilities, and negotiate the best possible resolution.

The key is acting quickly. Once Minnesota initiates contact, VDP is no longer available and you face full penalties and extended lookback periods.

Physical Nexus Still Applies

Economic nexus isn’t the only way to trigger Minnesota tax obligations. Physical nexus remains, and Minnesota’s definition is broad.

You have physical nexus in Minnesota if you:

- Maintain an office, warehouse, or distribution center in the state

- Have employees, contractors, or sales representatives working in Minnesota

- Store inventory in Minnesota (including FBA inventory in Minnesota fulfillment centers)

- Attend trade shows or events where you make sales or take orders

Amazon FBA creates particular complexity. If Amazon stores your inventory in a Minnesota fulfillment center (even temporarily) you have physical nexus in Minnesota.

Physical nexus triggers immediate collection obligations without thresholds.

HOST: Your Partner for Minnesota Sales Tax Compliance

Sales tax compliance in Minnesota, and across 45+ states, is complex, time-consuming, and unforgiving of mistakes. You crossed economic nexus in Minnesota, but how many other states have you triggered without knowing?

What HOST Delivers

Nexus Analysis: We analyze your sales data across all channels and determine exactly where you have economic or physical nexus. Minnesota and every other state.

Sales Tax Registration: We handle Minnesota registration and registrations in all required states, managing paperwork, follow-up, and state communications.

Automated Filing: We file your Minnesota returns monthly, quarterly, or annually, plus all other state filings. Keeping everything current and accurate.

Notice Management: We interpret and respond to Minnesota Department of Revenue notices, protecting you from penalties and resolving issues efficiently.

Audit Defense: We’re your trusted partner in resolving Minnesota sales tax audits, organizing documentation and defending your position.

Voluntary Disclosure: We file VDAs with Minnesota and other states to limit lookback periods and abate penalties for past non-compliance.

Software Optimization: We review and optimize your sales tax automation to ensure correct Minnesota rate calculation and prevent costly overcharging or undercollection.

We’ve been 100% focused on sales tax since 1999. Through our parent company TaxMatrix, we’ve served North America’s largest companies, and now we bring that expertise to growing online sellers.

Ready to Get Minnesota Compliant?

Minnesota economic nexus isn’t optional once you cross the threshold. Continuing to sell without registration creates escalating liability that compounds daily. Whether you’re just crossing the threshold, already non-compliant, or managing nexus across dozens of states, the right partner eliminates guesswork and prevents expensive mistakes.

Contact HOST today to discuss your Minnesota nexus situation and discover how we handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book and learn how to avoid costly compliance errors.

Frequently Asked Questions

What is Minnesota’s economic nexus threshold?

Minnesota’s economic nexus threshold is $100,000 in retail sales OR 200 separate retail transactions to Minnesota customers in the previous 12 months or current calendar year. Meeting either threshold triggers nexus.

Do marketplace sales count toward Minnesota’s threshold?

Yes. All retail sales delivered to Minnesota count toward the threshold, including sales through Amazon, eBay, and Etsy. Even though those platforms collect tax on your behalf. You must track total Minnesota sales across all channels.

When do I need to register after crossing Minnesota’s nexus threshold?

You must register with the Minnesota Department of Revenue by the first day of the calendar month that begins no later than 60 days after exceeding either threshold. Collection obligations begin immediately upon registration.

What happens if I’ve been selling into Minnesota without collecting tax?

Minnesota can assess back taxes, penalties, and interest for past non-compliance. However, the state’s Voluntary Disclosure Program can limit lookback periods to 3 years and reduce or eliminate penalties if you come forward before an audit begins.

Does Minnesota use origin or destination-based sales tax?

Minnesota uses a destination-based system. You must collect tax based on the customer’s delivery address, which can range from 6.875% to 8.375% or higher depending on local jurisdiction rates.

Can I just wait until Minnesota contacts me about nexus?

No. Once Minnesota initiates contact, you’ve lost access to voluntary disclosure benefits and face full penalties plus extended lookback periods. If you’ve crossed the threshold, register immediately or contact a sales tax professional to explore voluntary disclosure options.