Cross $100,000 in Louisiana sales, and you’ve triggered a collection obligation in one of America’s most complex tax states, where combined rates hit 10.5% and filing requirements split between state and parish authorities.

For e-commerce businesses managing nexus across dozens of states, Louisiana presents unique challenges. From parish-specific rates to dual filing systems, the complexity drains time without adding revenue. That’s where Hands Off Sales Tax (HOST) delivers value: comprehensive nexus analysis, registration handling, and ongoing filing management across Louisiana’s intricate landscape and all 45+ sales tax states.

What Is Economic Nexus in Louisiana?

Economic nexus is the connection between your business and Louisiana based solely on sales volume, no physical presence required. Once you exceed Louisiana’s threshold, you must register, collect sales tax from Louisiana customers, and file returns.

The 2018 South Dakota v. Wayfair Supreme Court decision gave states authority to require out-of-state sellers to collect sales tax based on economic activity. Louisiana adopted its law effective July 1, 2020, joining 45 other states in requiring remote sellers to comply.

Unlike physical nexus: having an office, warehouse, or employees, economic nexus triggers purely through transactions. You could operate entirely from California or overseas. If your Louisiana sales cross the threshold, you have an obligation.

Louisiana’s Economic Nexus Threshold: $100,000 in Sales

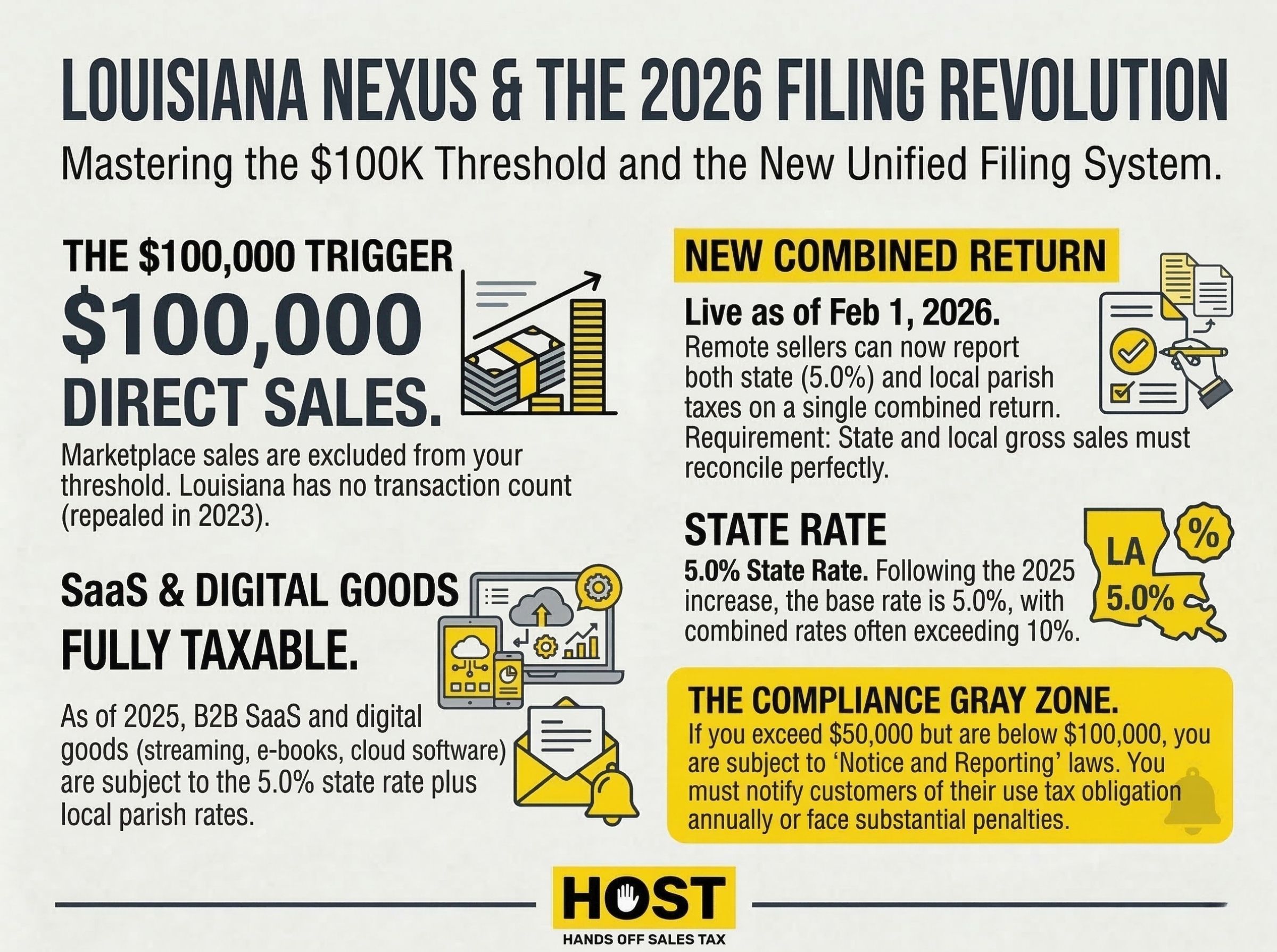

Louisiana sets its threshold at $100,000 in retail sales to Louisiana customers in the current or previous calendar year. No transaction count requirement. Only the dollar threshold matters.

Sell $100,001 to Louisiana customers in 2024? You triggered nexus and must register to collect sales tax. The threshold applies to the current calendar year or previous calendar year, whichever creates the obligation first.

Key Threshold Details

Measurement Period: Current or previous calendar year (January 1 – December 31). Louisiana uses a rolling approach, so monitor your sales throughout the year.

Retail Sales Calculation: The $100,000 includes retail sales of tangible personal property delivered to Louisiana addresses. Wholesale sales and sales-for-resale generally don’t count toward the threshold.

Marketplace Sales Exclusion: Only direct sales count toward your threshold. If you sell $75,000 directly and $40,000 through Amazon, only the $75,000 counts. You haven’t triggered nexus. The marketplace sales count toward Amazon’s threshold, not yours. Track this split carefully, as incorrectly including marketplace sales is a common mistake.

No Transaction Count: Louisiana eliminated its 200-transaction requirement on August 1, 2023. Only dollar volume matters now.

When Collection Begins: You must begin collecting sales tax within 60 days after exceeding the threshold or upon Louisiana Sales and Use Tax Commission approval, whichever comes later. Registration should happen within 30 days of triggering nexus.

⚠️ The $50,000 Notice & Reporting Trap

Louisiana maintains a separate $50,000 Notice & Reporting requirement that exists alongside the $100,000 economic nexus threshold. If you exceed $50,000 in gross sales but haven’t reached $100,000, you’re not required to collect sales tax; but you may face notification obligations.

This creates a compliance gray zone: businesses between $50K-$100K must either register voluntarily or comply with onerous customer notification requirements. The penalties for ignoring this requirement can be substantial. HOST’s nexus analysis identifies whether you’re in this zone and recommends the optimal compliance approach.

How Louisiana Sales Tax Works

Louisiana operates a state sales tax of 5% as of January 2025, but the total rate consumers pay includes parish and local taxes that push combined rates to 9-11% in many areas. Louisiana has over 200 local tax jurisdictions, each with different rates and rules.

State vs. Local Tax Structure

The Louisiana Department of Revenue collects state tax, while individual parishes collect their local portions. As a remote seller, you’ll file a single return with the state covering state tax, but you must also calculate and remit local taxes to appropriate parish authorities.

This dual-filing structure creates significant complexity. Unlike states with single filing portals for all jurisdictions, Louisiana requires sellers to understand which parish applies to each transaction and ensure correct local rate application.

What’s Taxable in Louisiana

Louisiana taxes most tangible personal property and certain services. Taxable items include clothing, electronics, furniture, digital products and downloads, and Software-as-a-Service in many cases.

Exemptions include: prescription medications, groceries for home consumption (prepared food is taxable), manufacturing machinery and equipment, and sales to tax-exempt organizations with proper documentation.

Physical Nexus Still Matters

Economic nexus isn’t the only trigger. Physical presence in Louisiana creates immediate sales tax obligations regardless of sales volume. Activities that establish physical nexus include:

- Maintaining an office, warehouse, or distribution facility

- Having employees, sales representatives, or agents operating in Louisiana

- Attending trade shows or conventions (even temporarily)

- Storing inventory in Louisiana fulfillment centers (including third-party FBA warehouses)

- Making deliveries with your own vehicles (not common carriers)

Physical nexus means you’re classified as a “Dealer” rather than a “Remote Seller,” which affects registration portals and filing requirements. If you’re attending a trade show in New Orleans, you’ve just created nexus.

When You Must Register in Louisiana

For Remote Sellers (Economic Nexus Only)

Register within 30 days of establishing economic nexus. You’ll register through the Louisiana Sales and Use Tax Commission for Remote Sellers, not the standard Louisiana Department of Revenue portal. Begin collecting within 60 days of exceeding the threshold or upon approval.

For Dealers (Physical Presence)

Register immediately through the Louisiana Department of Revenue’s Louisiana Taxpayer Access Point (LaTAP). Collection obligations begin from the first day of physical presence, regardless of sales volume.

HOST handles Louisiana registration for you: We complete all paperwork, determine the correct registration portal based on your nexus type, and ensure you’re properly licensed before you begin collecting.

Filing Requirements and Deadlines

Louisiana requires monthly, quarterly, or annual filing depending on your tax liability:

- Monthly filing: Tax liability exceeds $5,000 per month

- Quarterly filing: Tax liability between $300 and $5,000 per month

- Annual filing: Tax liability less than $300 per month

Returns are due the 20th of the month following the reporting period.

Parish-Level Filing Complexity

Many parishes require separate returns for local tax. While you file state tax through LaTAP, local tax filing may require separate portals, different deadlines, and unique reporting formats for each parish.

Orleans Parish has its own filing system. Jefferson Parish operates differently. East Baton Rouge Parish has different requirements still. Tracking which parishes require separate filing creates substantial administrative burden.

HOST manages all Louisiana filing obligations: state and local returns, on time, every filing period.

Common Mistakes Sellers Make

Mistake 1: Including Marketplace Sales in Threshold Calculation

Sellers incorrectly add Amazon/eBay/Etsy sales to their direct sales when calculating the $100,000 threshold. Only direct sales count. If you sell $60,000 direct and $50,000 through marketplaces, you haven’t triggered nexus.

Solution: Separate your sales channels in reporting. HOST’s nexus analysis service reviews your complete sales mix to determine accurate threshold calculations.

Mistake 2: Ignoring the $50K Notice & Reporting Law

Businesses between $50K-$100K assume they have no obligations, then face penalties for failing to comply with notification requirements.

Solution: Proactive nexus monitoring starting at $40,000 in sales. HOST identifies when you’re approaching either threshold and recommends the optimal compliance path.

Mistake 3: Applying Wrong Local Rates

Louisiana’s 200+ local jurisdictions mean rate calculation errors are common. Using the wrong parish rate leads to undercollection, which you’re liable for even if you didn’t charge the customer.

Solution: Use destination-based sourcing software that applies exact rates based on customer address. HOST offers a free sales tax software review to identify rate calculation errors.

Mistake 4: Missing Parish-Level Filing Requirements

Sellers register with Louisiana and file state returns but completely miss separate parish filing requirements, creating compliance gaps.

Solution: Partner with experts who understand Louisiana’s dual-filing structure. HOST manages both state and parish-level obligations.

How HOST Simplifies Louisiana Compliance

Louisiana’s complexity with dual filing, parish-specific rates, 200+ jurisdictions, the $50K-$100K gray zone creates a compliance burden that diverts resources from growth.

What HOST Delivers for Louisiana

Nexus Analysis: We review your complete sales data including marketplace vs. direct sales split—to determine precisely when you crossed Louisiana’s threshold and whether you’re in the $50K-$100K notification zone.

Louisiana Registration: We determine whether you’re a Remote Seller or Dealer, handle registration with the appropriate portal, and ensure proper licensing before collection begins.

Complete Filing Management: We prepare and file all Louisiana returns (state and parish-level) monthly, quarterly, or annually. Every deadline met, every jurisdiction covered.

Audit Defense: If Louisiana audits your compliance, we organize documentation and defend your position with 25+ years of specialized expertise.

We’ve been 100% focused on sales tax since 1999. Co-founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, HOST brings enterprise-level expertise to e-commerce sellers of all sizes.

Ready to Handle Louisiana Economic Nexus Correctly?

Louisiana’s $100,000 threshold creates immediate obligations in one of America’s most complex tax states. Between the $50,000 notification requirement, parish-level filing, marketplace sales tracking, and combined rates exceeding 10%, managing Louisiana compliance diverts substantial time from growth.

Contact HOST today to discuss your Louisiana nexus situation or schedule a free consultation. Let us handle Louisiana’s complexity so you can focus on sales, not tax compliance.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is Louisiana’s economic nexus threshold for remote sellers?

Louisiana’s economic nexus threshold is $100,000 in retail sales to Louisiana customers in the current or previous calendar year. No transaction count requirement, only the dollar threshold matters. Only direct sales count; marketplace sales are excluded.

What’s the difference between Louisiana’s $50,000 and $100,000 thresholds?

The $50,000 threshold triggers Notice & Reporting requirements (customer notifications), while the $100,000 threshold triggers actual sales tax collection obligations. Businesses between these amounts face a compliance gray zone requiring careful navigation.

Do marketplace sales count toward Louisiana’s economic nexus threshold?

No. Only sales made directly by your business count toward the $100,000 threshold. Sales through Amazon, eBay, Etsy, or other marketplaces count toward the marketplace’s threshold, not yours. Example: $75,000 direct + $40,000 marketplace = $75,000 toward your threshold.

When must I start collecting Louisiana sales tax after crossing the threshold?

You must register within 30 days of exceeding $100,000 and begin collecting within 60 days of crossing the threshold or upon Louisiana Sales and Use Tax Commission approval, whichever comes later. Don’t wait—penalties accrue from when you should have registered.

Does Louisiana require separate filing for local parish taxes?

In many cases, yes. While you file state tax through Louisiana Taxpayer Access Point (LaTAP), numerous parishes require separate local tax returns through different systems with different deadlines. Orleans Parish, Jefferson Parish, and others maintain their own filing portals.

Can I use a Voluntary Disclosure Agreement if I missed Louisiana’s nexus threshold?

Yes. If you crossed Louisiana’s threshold months or years ago without collecting tax, a Voluntary Disclosure Agreement (VDA) can limit your lookback period to 3-4 years (instead of 10) and potentially eliminate penalties. HOST files VDAs with Louisiana to resolve past obligations with minimal liability.