Is it illegal not to refund sales tax? When you return a product, you’re entitled to get back everything you paid, including the sales tax. Merchants who keep sales tax on returned items are violating state law, since they’re holding funds that legally belong to the state, not to them.

For businesses managing returns across multiple states, understanding sales tax refund obligations isn’t just good customer service, it’s legal compliance. Each state has specific rules about when and how sales tax must be refunded, and misconfigured systems can inadvertently create violations.

That’s where Hands Off Sales Tax (HOST) provides clarity. From nexus analysis to refund compliance guidance, we ensure your return processes meet legal requirements everywhere you operate.

The Legal Truth: Merchants Must Refund Sales Tax

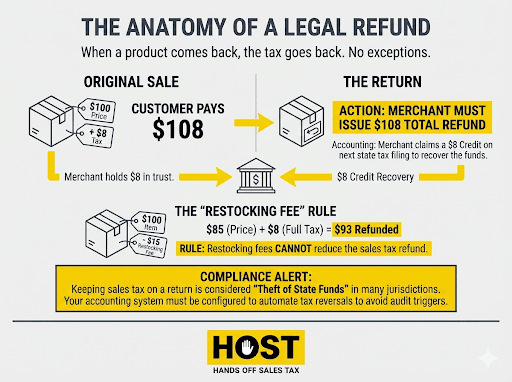

Sales tax represents money collected on behalf of the state. When a customer purchases a $100 item in a location with 8% sales tax, they pay $108 total. $100 to the merchant and $8 held in trust for the tax authority.

If that customer returns the product, the entire transaction reverses. The merchant keeps neither the $100 nor the $8. Legally, the merchant never owned the sales tax, they were merely the collection agent.

State laws mandate sales tax refunds on returned merchandise. When processing returns, merchants must:

- Refund the full purchase price including all sales tax collected

- Issue the refund in the same form as the original payment when possible

- Document the return and adjustment on sales tax filings

- Reduce their sales tax liability by the amount refunded

Failing to refund sales tax isn’t a gray area. Some states classify this as theft, since the merchant is keeping funds that belong to the state.

What Happens to Unrefunded Sales Tax?

When merchants don’t refund sales tax, problems multiply:

Legal Liability: State tax authorities can audit and assess penalties for incorrect filings that don’t account for returns. If you collected $10,000 in sales tax but refunded $1,000 on returns, you only remit $9,000, but you must document those returns. Merchants claim credits on future returns or amend past filings to adjust their liability.

Consumer Complaints: Customers who discover they weren’t refunded sales tax file complaints with state consumer protection agencies. These complaints trigger investigations that uncover broader compliance issues.

Reputation Damage: Word spreads quickly about merchants who don’t process refunds correctly. Online reviews and social media complaints drive customers to competitors.

Criminal Exposure: States treat intentional withholding of sales tax as theft of state funds. In serious cases, this can lead to criminal charges and even jail time, since the merchant is keeping money that never belonged to them.

State Variations in Refund Requirements

While the core principle remains consistent (being refunded sales tax on returns) implementation details vary.

Time Limits and Documentation

Most states require merchants to issue refunds within a “reasonable time” consistent with standard return policies, typically 7-30 days. However, specific states impose stricter statutory time limits for sales tax refund eligibility.

Connecticut, Rhode Island, and D.C. impose 90-day limits from the purchase date. Massachusetts extends this to 180 days for motor vehicles but maintains 90 days for other merchandise. Michigan allows up to 120 days for most items. Returns made after these statutory periods may not qualify for sales tax refunds, even if the merchant accepts the product return.

Documentation requirements include original sales receipts showing tax collected, return authorization, refund transaction records, and adjustment entries on the next sales tax return.

Partial Returns and Restocking Fees

When customers return only part of an order, merchants must refund sales tax proportionally. A customer who purchased five items totaling $500 plus $40 sales tax, then returned two items worth $200, should receive $200 plus $16 in sales tax.

Restocking fees create complexity. If a merchant charges a 15% restocking fee on that $200 return ($30), the customer receives $170 plus the full $16 in sales tax. Sales tax refunds cannot be reduced by restocking fees, the tax must be refunded in full.

Store Credit vs. Cash Refunds

Many retailers offer store credit instead of cash. Legally, this doesn’t change the sales tax obligation. If the original transaction included sales tax, the credit must equal the full amount including tax.

When that store credit is later used, the merchant charges sales tax again on the new purchase. The original tax is effectively “returned” via credit, then new tax is collected on the replacement purchase.

Exchange Transactions: A Special Case

Product exchanges introduce unique considerations. When a customer exchanges a $100 item (plus $8 tax) for another $100 item, many merchants process this as a straight exchange.

From a sales tax perspective, this is actually two transactions: a return of the original item (refund $108 including tax) and purchase of a new item (charge $108 including tax).

The net effect is zero. No money changes hands. However, documentation should reflect both the return and the new sale. Some states require merchants to show the return credit and new charge separately on receipts.

When exchanges involve different prices, merchants must handle the difference correctly. Exchanging a $100 item for a $120 item means the customer pays $20 plus the differential tax.

Common Merchant Mistakes That Create Legal Issues

Misconfigured E-Commerce Systems

Many online retailers use automated systems that calculate sales tax at checkout but don’t properly handle refunds. Common errors include:

- Refunding product price but not tax

- Calculating refund tax at current rates rather than original transaction rates

- Failing to credit sales tax when issuing store credit

- Not adjusting sales tax liability on returns processed after the filing period

Sales tax software like TaxJar or Avalara can automate refund calculations, but misconfiguration leads to consistent violations across thousands of transactions. HOST offers a Free Sales Tax Software Review to identify these costly errors before they become audit problems.

Multi-State Complications

For businesses operating across state lines, refund complexity multiplies. A customer in California who purchased during a visit to Oregon (no sales tax) later returns by mail—no tax was collected, none is refunded.

But a California customer who purchased online and paid California sales tax must receive that tax back. Tracking which transaction included which state’s tax, then processing refunds correctly, demands sophisticated systems.

Economic nexus rules mean businesses collect tax in dozens of states. Each return must reference the correct jurisdiction’s original tax collection and adjust the appropriate state’s liability.

Consumer Rights: What to Do if You’re Not Refunded Sales Tax

Document Everything

If a merchant refuses to refund sales tax, gather documentation:

- Original receipt showing tax collected

- Return receipt or confirmation

- Refund statement showing only product price refunded

- Any communication with the merchant about the tax

Contact the Merchant First

Many sales tax refund issues stem from system errors rather than intentional violations. Contact customer service, explain that sales tax wasn’t refunded, and request correction. Reference your state’s requirement that sales tax must be refunded on returned merchandise.

File a Complaint with State Authorities

If the merchant refuses, file complaints with:

- State Department of Revenue: The tax authority investigates merchants who mishandle sales tax. In some states like Colorado, consumers can file direct refund claims (Form DR 0137B) when merchants won’t cooperate.

- Attorney General’s Consumer Protection Division: Handles consumer fraud and unfair business practices

- Better Business Bureau: While not government, BBB complaints often motivate resolution

Consider Small Claims Court

For significant amounts, small claims court provides a mechanism to recover improperly withheld sales tax. The merchant’s violation of state tax law strengthens your case.

HOST: Managing Refund Compliance Across All Jurisdictions

Sales tax compliance extends beyond collection. It includes proper refund processing, documentation, and filing adjustments. For e-commerce businesses handling returns across multiple states, ensuring every refund meets legal requirements prevents audit exposure and customer complaints.

What HOST Delivers:

- Nexus Analysis: We determine where you have collection obligations and refund compliance requirements across all states

- Sales Tax Filing: We prepare and file returns with proper return/refund adjustments, ensuring your liability reflects actual net sales

- Software Review: We audit your e-commerce platform and tax software configuration to ensure refunds process correctly

- Consultation: We provide guidance on complex refund scenarios, multi-state returns, and policy development

- Audit Defense: We handle communications with tax authorities and defend your position in refund-related audits

- Voluntary Disclosure Agreements: If you discover past refund processing errors, we file VDAs to limit lookback periods and abate penalties

We’ve been 100% focused on sales tax since 1999. That’s over 25 years managing compliance so you can keep your hands on your business.

Protect Your Business and Your Customers

Sales tax refund compliance protects both your business from legal liability and your customers’ rights. Every return processed incorrectly represents potential exposure. Multiply that across hundreds or thousands of annual returns, and the risk becomes substantial.

Whether you’re handling returns in multiple states, configuring e-commerce systems, or responding to customer complaints about missing tax refunds, the right compliance partner ensures your processes meet legal requirements everywhere you operate.

Contact HOST today to discuss your compliance needs or schedule a free consultation. Let us handle the complexity so you can focus on delivering great customer experiences.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Is it illegal for a store not to refund sales tax on returns?

Yes. Sales tax collected by merchants is held in trust for state governments. When merchandise is returned, the transaction reverses and the merchant must refund the full amount including sales tax. Keeping sales tax on returns violates state tax law and may constitute theft of state funds.

Do I get sales tax back if I return an item?

Yes, you should receive a full refund including all sales tax paid on the original purchase. If you paid $108 for an item ($100 product plus $8 sales tax), your return refund should be the full $108. Merchants who refund only the product price are violating state law.

Can a store charge a restocking fee but not refund sales tax?

No. Restocking fees reduce the product refund but cannot reduce the sales tax refund. If you return a $100 item with 8% sales tax ($108 total) and face a $15 restocking fee, you should receive $85 product refund plus the full $8 sales tax, totaling $93.

What if I paid sales tax in one state but returned tax in another state?

You’re entitled to a refund based on the original transaction. If you paid California sales tax when purchasing, you should receive that California tax back regardless of where you process the return. The merchant must track which state’s tax was originally collected and refund accordingly.

How do I report a merchant who won’t refund sales tax?

File complaints with your state’s Department of Revenue, Attorney General’s Consumer Protection Division, and the Better Business Bureau. Document your original receipt showing tax collected and your refund receipt showing tax was not returned. State tax authorities take these violations seriously.

Does store credit have to include sales tax?

Yes. Store credit issued for returns must include the full value of the original purchase including sales tax. When you later use that credit, sales tax will be charged again on the new purchase. The original tax is effectively refunded via credit and new tax is collected on the replacement.