Navigating Illinois sales tax filing frequency is crucial for businesses to stay compliant and avoid penalties. The Illinois Department of Revenue assigns filing schedules: monthly, quarterly, or annually based on a business’s average tax liability. Misunderstanding these requirements can lead to late fees, audits, or unnecessary complications.

This guide breaks down the filing frequency rules, deadlines, and best practices for accurate tax reporting. Hands Off Sales Tax (HOST) simplifies sales tax compliance, helping businesses determine the right filing frequency and manage tax obligations seamlessly. With expert guidance, you can ensure accuracy, avoid penalties, and focus on growing your business.

Understanding Illinois Sales Tax Filing Frequencies

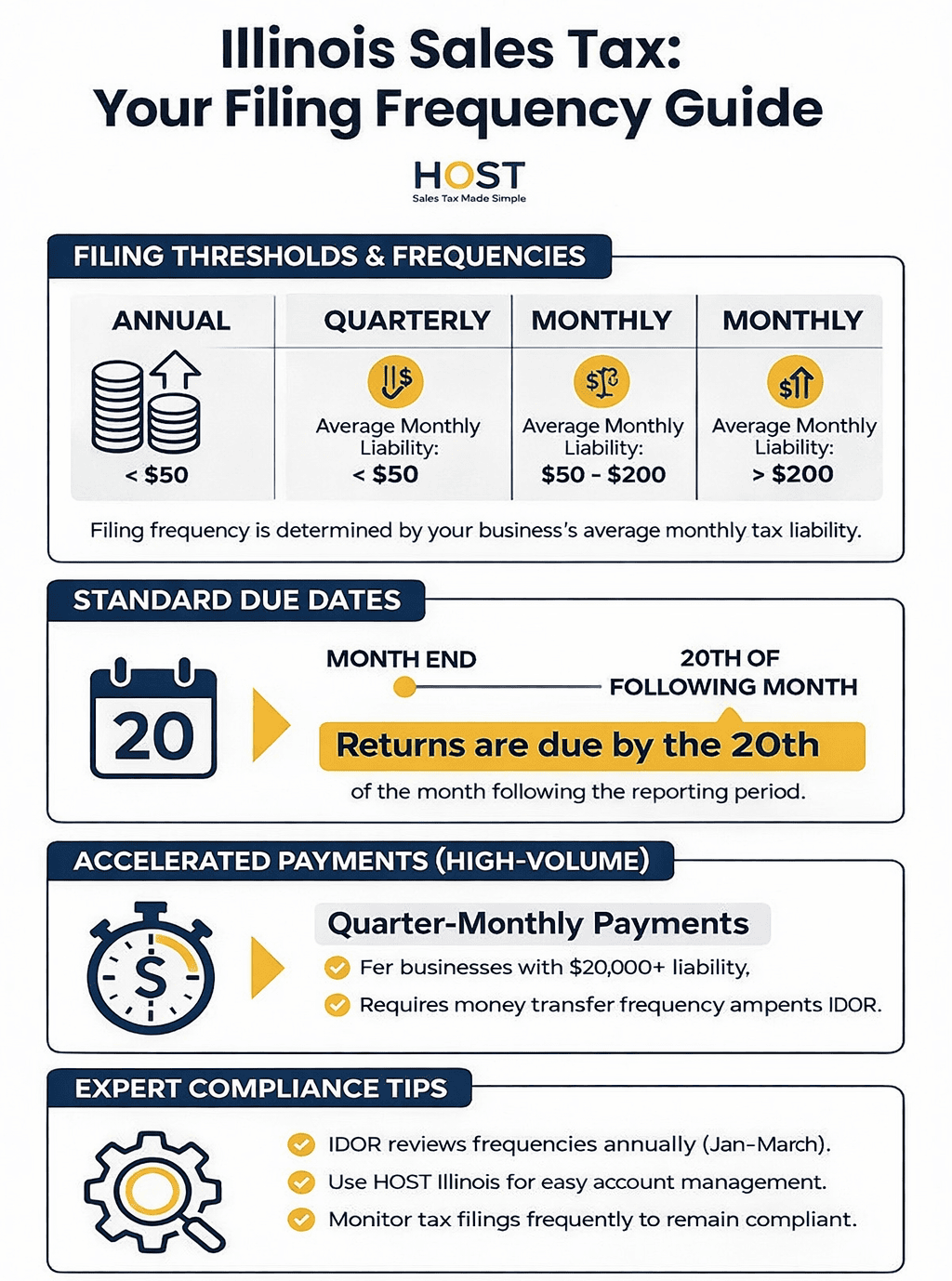

In Illinois, businesses are assigned sales tax filing frequencies: monthly, quarterly, or annually, based on their average monthly tax liability. Understanding these assignments is crucial for timely compliance and avoiding penalties.

Overview of Filing Frequencies

Monthly Filing: Assigned to businesses with an average monthly tax liability exceeding $200.

Quarterly Filing: Designated for businesses whose average monthly tax liability ranges between $50 and $200.

Annual Filing: Applicable to businesses with an average monthly tax liability below $50.

Criteria for Assignment

The Illinois Department of Revenue (IDOR) determines your filing frequency based on your initial registration and annual tax liability. They may notify you of a change in your filing frequency if your average monthly liability shifts into a different bracket. For instance, if your average monthly liability increases above $200, IDOR may change your filing requirement to monthly.

It’s essential to monitor your tax liabilities regularly, as significant changes can alter your filing obligations. Staying informed about these thresholds ensures compliance and helps prevent potential late fees or penalties.

Illinois Filing Frequency Decision Tree

To quickly determine your correct filing frequency, follow this decision framework:

Step 1: Determine Your Business Status

New Business (First Year of Operations):

- IDOR assigns initial filing frequency based on estimated liability provided during registration

- Frequency may be adjusted after first full year of operations

- Monitor actual liability monthly to anticipate changes

Established Business (Operating 12+ Months):

- Calculate average monthly liability using trailing 12-month period

- IDOR reviews annually and may reassign frequency

- Proceed to Step 2

Step 2: Calculate Average Monthly Tax Liability

For Established Businesses:

- Sum total sales tax liability for previous 12 months

- Divide by 12 to get average monthly liability

- Apply result to Step 3

For Partial-Year Businesses:

- Use actual months of operation (minimum 3 months for meaningful calculation)

- Sum total liability for those months

- Divide by number of months operated

- Note: IDOR typically waits for full calendar year before reassignment

Step 3: Apply Threshold Rules

If average monthly liability is:

- Under $50 → Annual Filing

- Due: January 20th of following year

- Best for: Very small businesses, seasonal operations with minimal sales

- $50 to $200 → Quarterly Filing

- Due: 20th day of month following quarter end

- Best for: Small to medium businesses with steady moderate sales

- Over $200 but under $20,000 → Monthly Filing

- Due: 20th day of following month

- Best for: Growing businesses, consistent revenue streams

- $20,000 or more → Monthly Filing + Quarter-Monthly Payments

- Payments due: 7th, 15th, 22nd, and last day of each month

- Best for: Large operations, high-volume retailers

Step 4: Address Edge Cases

Threshold Boundary Scenarios:

If your average monthly liability hovers right at $50 or $200:

- At exactly $50: Typically assigned to quarterly filing

- At exactly $200: Typically assigned to monthly filing

- Within $10 of threshold: Monitor closely, fluctuations could trigger reassignment

Seasonal Business Considerations:

Illinois does not offer special seasonal filing frequencies. Your average spans all 12 months, including zero-sales periods.

Example: $2,400 liability in 3 peak months + $0 in 9 off months = $200/month average = monthly filing requirement

Refunds, Credits, and Adjustments:

- Customer refunds: Reduce gross tax liability for that period

- Bad debt deductions: Can lower average liability if properly documented

- Credits from overpayments: Applied to future liabilities but don’t reduce average for frequency calculation

- Amended returns: May retroactively affect average if IDOR recalculates

Determining Your Business’s Filing Frequency

Determining your business’s Illinois sales tax filing frequency is essential for compliance and efficient tax management. Here’s how to assess and understand your filing obligations:

Calculating Average Monthly Tax Liability

Step 1: Total Tax Liability Sum your total sales tax liability for a given period (typically a 12-month period for established businesses).

Step 2: Divide by Months Divide this total by the number of months in that period to find your average monthly liability.

Example: If your annual sales tax liability is $2,400:

- $2,400 ÷ 12 months = $200 average monthly liability

This calculation helps determine your filing frequency:

- Monthly Filing: Average monthly liability over $200

- Quarterly Filing: Average monthly liability between $50 and $200

- Annual Filing: Average monthly liability under $50

Common Calculation Scenarios

Scenario 1: Hovering at Thresholds

Your business collects $195-$205 in monthly liability. IDOR reviews annually, so temporary fluctuations won’t immediately trigger changes. If you consistently hover near $200, prepare for monthly filing.

Scenario 2: Partial-Year Business

You opened in July and collected $2,100 through December (6 months).

Calculation:

- Average: $2,100 ÷ 6 = $350/month

- Result: Monthly filing frequency (over $200)

IDOR typically assigns initial frequency conservatively and reassesses after your first full calendar year.

Scenario 3: Seasonal Business

Annual pattern: May-August (4 months) at $800/month = $3,200 total; September-April (8 months) at $0 = $0 total

Calculation:

- Average: $3,200 ÷ 12 = $267/month

- Result: Monthly filing (you’ll file zero returns for off-season months)

Notification Process

The Illinois Department of Revenue (IDOR) assigns your filing frequency based on your initial registration and annual tax liability. If there’s a change in your average monthly liability, IDOR adjusts your filing frequency and notifies you accordingly.

How IDOR Reassignment Works:

- IDOR reviews filing frequencies annually (typically January-March)

- Notification arrives 30-60 days before changes take effect

- Changes become effective at the start of the next quarter

Proactive Frequency Changes:

Businesses can request filing frequency changes before IDOR acts. Contact IDOR MyTax Illinois support or call (217) 782-3336 with documentation showing changed liability patterns. Allow 30-45 days for processing.

Important: Continue current filing schedule until you receive official notification of change.

By accurately calculating your average monthly tax liability and understanding the notification process, you can ensure timely and correct sales tax filings in Illinois.

Due Dates and Compliance

Adhering to the correct Illinois sales tax filing frequency and due dates is essential for businesses to maintain compliance and avoid penalties.

Standard Due Dates

Monthly Filers: Returns are due on the 20th day of the month following the reporting period. For example, the return for January is due by February 20th.

Quarterly Filers: Returns are due on the 20th day of the month following the end of the quarter. For instance, for the quarter ending March 31st, the return is due by April 20th.

Annual Filers: Returns are due by January 20th of the year following the reporting year.

Quarter-Monthly Payments

Businesses with an average monthly tax liability of $20,000 or more are required to make quarter-monthly (accelerated) payments. These payments are due on the 7th, 15th, 22nd, and last day of each month. If a due date falls on a weekend or holiday, the payment is due the next business day.

To calculate each quarter-monthly payment, businesses can choose between:

Option 1: Pay 22.5% of the actual liability for the current month.

Option 2: Pay 25% of the liability for the same month in the preceding year.

Selecting the lesser amount between these options can help manage cash flow effectively.

Compliance and Penalties

Timely filing and payment are crucial. Late submissions can result in penalties and interest charges. For detailed information on penalties, refer to the Illinois Department of Revenue’s guidelines.

By understanding these due dates and payment requirements, businesses can ensure compliance with Illinois sales tax regulations and avoid unnecessary financial penalties.

Adjusting Filing Frequencies

Fluctuations in your business’s tax liability can lead to adjustments in your assigned Illinois sales tax filing frequency. Understanding how these changes occur and the process for requesting modifications is essential for maintaining compliance.

Changes in Tax Liability

The Illinois Department of Revenue (IDOR) monitors businesses’ average monthly tax liabilities to determine appropriate filing frequencies. As your business grows or experiences sales volume changes, your tax liability may shift, prompting IDOR to reassign your filing frequency.

Typical Reassignment Triggers:

- Consistent threshold crossing (3+ consecutive months above or below thresholds)

- Annual review shows trailing 12-month average in different bracket

- Significant events (major sale, acquisition, closure) dramatically affecting liability

Implementation Timeline:

- IDOR reviews: January-March annually

- Notification: 30-60 days before effective date

- Implementation: Beginning of next quarter

Business-Requested Changes:

- Processing time: 30-45 days

- Continue current frequency until official approval received

Requesting a Change

If your assigned filing frequency no longer aligns with your current tax liability, you can request a modification:

- Gather Supporting Documentation: Last 6-12 months of sales tax liability records and calculation showing new average monthly liability

- Contact IDOR:

- Online: Through MyTax Illinois message center

- Phone: (217) 782-3336 (Monday-Friday, 8:00 AM – 5:00 PM)

- Mail: Illinois Department of Revenue, P.O. Box 19044, Springfield, IL 62794-9044

- Provide Clear Rationale: Explain why current frequency no longer matches your business pattern with supporting calculations

- Await Official Response: IDOR will review and notify you of approval or denial with an effective date

Pro Tip: If your business is approaching the $200 threshold, proactively requesting monthly filing can help avoid mid-year surprise reassignment.

Edge Cases and Common Misconceptions

Misconception 1: “My Filing Frequency Changes Immediately When I Cross a Threshold”

Reality: IDOR reviews frequencies annually, not after each filing. Crossing a threshold once doesn’t automatically trigger reassignment. Your 12-month average determines frequency changes at annual review.

Misconception 2: “Seasonal Businesses Get Special Treatment”

Reality: Illinois does not offer seasonal-specific filing frequencies. Your filing schedule is based on 12-month average, regardless of when sales occur. You must file returns (even $0 returns) for all assigned periods.

Misconception 3: “Refunds and Credits Lower My Filing Frequency”

Partial truth: Refunds reduce your gross tax liability for a period. Bad debt deductions (properly documented) can lower your average. However, overpayment credits help cash flow but don’t reduce the underlying liability used for frequency calculation.

Edge Case: Multi-Location Businesses

Filing frequency is determined by your consolidated statewide average monthly liability across all Illinois locations. You file one return covering all locations. Adding locations can push you into a higher frequency bracket.

Edge Case: Marketplace Facilitator Sales

Tax collected by Amazon, eBay, or other marketplace facilitators is their liability, not yours. Your filing frequency is based only on sales where you are responsible for collection. Transitioning to primarily marketplace sales may decrease your filing frequency.

Best Practices for Compliance

Maintaining compliance with Illinois sales tax regulations requires diligent record-keeping, utilizing available resources, and staying informed about tax law changes.

Record-Keeping

Accurate records are essential for correct tax reporting. The Illinois Department of Revenue mandates that businesses retain records documenting all sales for three and one-half years after filing the relevant return.

Required records include:

- Sales receipts and invoices

- Exemption certificates

- Credit memos

Records must be available for inspection during normal business hours and maintained in English. Failure to keep adequate records can result in fines up to $3,000 for repeated offenses.

Utilizing MyTax Illinois

The MyTax Illinois portal is a valuable tool for businesses to manage their tax obligations efficiently. Through this online platform, businesses can:

- File and amend returns

- Make payments

- Renew licenses

- Respond to audits

- Access correspondence

Utilizing MyTax Illinois streamlines the filing process and helps ensure timely compliance.

Staying Informed

Tax laws and filing requirements can change, making it crucial for businesses to stay updated. Regularly consulting the Illinois Department of Revenue’s resources, such as publications, bulletins, and the official website, can provide valuable information on:

- Changes in tax rates

- New legislation

- Updated filing procedures

Subscribing to updates and participating in informational webinars can also help businesses remain compliant with current regulations.

By implementing these best practices, businesses can effectively manage their sales tax responsibilities and minimize the risk of non-compliance.

Streamlining Illinois Sales Tax Compliance with HOST

Managing Illinois sales tax filing frequency can be challenging, especially with changing tax liabilities, varying deadlines, and evolving compliance requirements. Hands Off Sales Tax (HOST) simplifies tax management, ensuring businesses remain compliant while minimizing administrative burdens.

Personalized Filing Frequency Assessment

HOST helps businesses determine the correct filing frequency: monthly, quarterly, or annually, by evaluating sales tax liabilities and transaction history. If your assigned frequency no longer aligns with your tax obligations, HOST assists in requesting changes with the Illinois Department of Revenue (IDOR).

Accurate Tax Filings and Payment Support

HOST streamlines sales tax reporting by:

- Preparing and filing accurate ST-1 Sales and Use Tax Returns on time

- Managing quarter-monthly payments for high-liability businesses

- Ensuring proper record-keeping to avoid penalties

Audit Defense and Compliance Monitoring

If IDOR audits your business, HOST provides expert audit support, defending your filings and minimizing risks. Additionally, HOST keeps you updated on tax law changes, ensuring compliance with evolving regulations.

Stay Compliant and Avoid Costly Mistakes

Understanding and adhering to Illinois sales tax filing frequency is crucial for avoiding penalties and ensuring smooth business operations. Whether filing monthly, quarterly, or annually, staying compliant requires accurate record-keeping, timely payments, and awareness of changing tax laws. Missteps can lead to unnecessary fines or audits, making professional guidance invaluable.

Hands Off Sales Tax (HOST) takes the guesswork out of sales tax compliance, offering expert support for tax filings, payment management, and audit defense. Don’t risk compliance issues, schedule a consultation with HOST today and ensure your business meets all Illinois sales tax obligations with confidence.

Frequently Asked Questions

What happens if my average monthly tax liability is exactly $50 or $200?

When your average monthly liability falls exactly on a threshold, IDOR typically assigns the lower filing frequency. At exactly $50, you’ll likely be assigned quarterly filing. At exactly $200, practices vary, but IDOR tends toward monthly filing to ensure adequate collection frequency. If you’re consistently at an exact threshold, monitor closely and consider proactively requesting clarification from IDOR.

How do I calculate average monthly liability if I was only in business for part of the year?

For partial-year businesses, divide your total tax liability by the actual number of months you operated. However, IDOR typically waits for a full calendar year before reassessing frequency. If you opened mid-year, you’ll likely keep your initially assigned frequency until IDOR reviews your first full year of operations.

Do seasonal businesses get different filing frequency treatment?

No. Illinois does not offer seasonal-specific filing frequencies. Your filing schedule is based on your average monthly liability calculated across all 12 months, regardless of when your sales occur. This means even if you only operate 3-4 months per year, you may still require monthly filing if your average exceeds $200. You must file returns (even zero returns) for all assigned periods, including off-season months.

How do refunds, credits, or bad debt affect my average monthly liability?

Refunds: Customer refunds reduce your gross tax liability in the month processed and are factored into your average calculation.

Bad debt deductions: Properly documented bad debt reduces your liability for frequency calculation purposes when claimed per IDOR requirements.

Overpayment credits: These help with cash flow but generally don’t reduce the underlying liability used for frequency calculation. IDOR considers your actual collection obligation, not net payments after credits.

Amended returns: May retroactively affect your calculated average if IDOR recalculates, but rarely trigger immediate frequency changes unless substantial.

How often does IDOR review and potentially change my filing frequency?

IDOR typically conducts annual reviews of filing frequencies, usually between January and March for the previous year’s activity. Changes typically take effect at the beginning of the next quarter. Mid-year changes are rare but can occur if dramatic liability increases are detected (such as major business expansion or acquisition).

Can I request a change to my filing frequency before IDOR reassigns me?

Yes. Businesses can proactively request filing frequency changes by contacting IDOR through MyTax Illinois, calling (217) 782-3336, or mailing documentation showing changed liability patterns. You’ll need to provide 6-12 months of liability records and clear rationale. Allow 30-45 days for processing. Important: Continue your current filing schedule until you receive official approval.

If I’m right at a threshold, what’s my “safe zone” to avoid reassignment?

Generally, being $10-$20 below a threshold provides reasonable cushion against reassignment due to normal business fluctuations. For example, if your average monthly liability is $180-$190, you’re in a relatively safe quarterly filing zone. If you consistently hover at $195-$205, prepare for potential monthly filing reassignment at the next annual review.

What if I operate multiple locations in Illinois?

Your filing frequency is determined by your consolidated statewide average monthly liability across all Illinois locations under your tax registration. You file one combined return covering all locations, and IDOR assigns one frequency based on total liability. Adding locations can push you into a higher frequency bracket even if individual locations have small liabilities.

Does tax collected by Amazon or other marketplace facilitators count toward my filing frequency?

No. Tax collected and remitted by marketplace facilitators is their liability, not yours. Your filing frequency is based only on sales where you are directly responsible for collection and remittance. If you transition from direct sales to primarily marketplace facilitator sales, your average liability and filing frequency may decrease.