Reporting sales tax in California means more than tallying what customers paid at checkout. District allocations, prepayment schedules, and CDTFA deadlines, California’s system turns monthly compliance into a puzzle that consumes hours without generating a dollar of revenue.

From nexus analysis to automated filings across 500+ districts, Hands Off Sales Tax (HOST) keeps your California reporting current while you focus on growth. Understanding filing requirements, penalty triggers, and reporting methods helps maintain compliance without stealing focus from your core business.

What California Sales Tax Reporting Actually Means

Sales tax reporting means filing returns with the California Department of Tax and Fee Administration (CDTFA) that document gross sales, taxable transactions, collected tax, and any deductions. You’re accounting for every transaction where California sales tax applied, then remitting what’s owed.

California’s statewide base hits 7.25%, which is the highest in the nation. Local jurisdictions add district taxes, pushing combined rates from 7.25% to 10.75% depending on customer location. With over 500 distinct jurisdictions, each requiring proper allocation, manual tracking becomes virtually impossible.

The CDTFA assigns most businesses quarterly filing, though high-volume sellers file monthly or prepay. Missing deadlines triggers 10% penalties immediately, plus daily interest. California’s tax authority has intensified enforcement on remote sellers since Wayfair, making accurate reporting essential for everyone selling into the state.

Who Must Report Sales Tax in California

Economic Nexus Thresholds

After Wayfair, California requires remote sellers to collect and report once they exceed $500,000 in total California sales during the current or previous calendar year. This threshold counts sales only. Transaction volume doesn’t matter. Cross $500,000, and nexus activates immediately.

This applies universally: e-commerce businesses, marketplace sellers, wholesalers, manufacturers selling direct. Physical presence no longer gates California obligations.

Physical Nexus Triggers

Physical presence still creates instant nexus regardless of sales volume. Maintaining offices, warehouses, or distribution centers in California triggers obligations. Having employees or contractors working in-state creates nexus. Storing inventory in California fulfillment centers (including Amazon FBA) establishes presence.

Even temporary presence counts. A single trade show where you take orders creates registration and reporting requirements for those transactions.

Marketplace Facilitator Rules

California’s marketplace facilitator law requires platforms like Amazon, eBay, and Etsy to collect and remit for third-party sellers. If you sell exclusively through these platforms, they handle California reporting for those transactions.

However, direct website sales or non-facilitator channels require separate reporting. Many sellers wrongly assume marketplace sales exempt them entirely, then discover during audits they should’ve been reporting direct sales all along.

Understanding Filing Frequency Requirements

Quarterly Filing (Most Common)

Most California businesses file quarterly. The CDTFA assigns quarterly filing to businesses with moderate tax liability, typically those averaging under $17,000 per month. Quarterly returns cover three-month periods ending March 31, June 30, September 30, and December 31.

Deadlines fall on the last day of the following month: April 30, July 31, October 31, and January 31. These are hard deadlines, so postmarks don’t count. The CDTFA must receive payment by the due date to avoid penalties.

Even with zero sales, you must still file a return. Failure to file zero returns can result in permit revocation and penalties.

Monthly Filing (High-Volume Sellers)

Businesses with average monthly tax liability exceeding $17,000 typically receive monthly filing assignments. Returns cover calendar months with deadlines on the last day of the following month. January sales are reported by February 28/29, February by March 31, and so on.

Monthly filing creates 12 annual deadlines instead of four, multiplying administrative burden while improving cash flow management by spreading payments throughout the year.

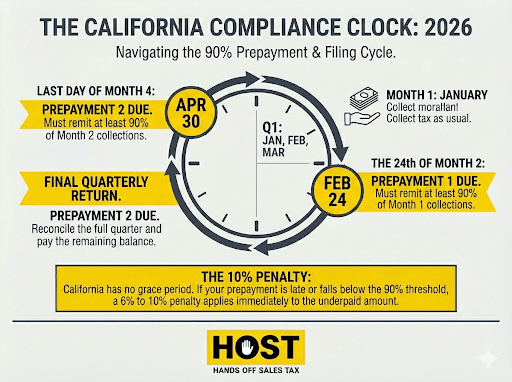

Prepayment Requirements

High-volume sellers with average monthly tax liability of $17,000 or more must prepay a portion of estimated tax before the quarter ends. California requires prepayments by the 24th day of the month following the first and second months of each quarter. For example, January prepayment is due February 24, and February prepayment is due March 24.

Prepayment amounts equal at least 90% of the prior month’s tax liability. Underpaying triggers penalties and interest, while overpaying creates credits applied to future returns.

Step-by-Step: How to Report Sales Tax in California

Step 1: Gather Your Sales Data

Collect comprehensive sales data covering all California transactions for the reporting period. You need gross sales (total revenue before deductions), taxable sales (after removing exempt transactions), tax collected from customers, and any purchases subject to use tax.

Use tax applies when you purchase inventory, equipment, or supplies from out-of-state vendors who didn’t collect California sales tax. These purchases must be reported on Line 2 of your return.

Break down sales by jurisdiction using customer destination addresses. California requires district-level reporting, lump sums won’t work. Each city, county, and special district must receive their allocated portion.

Most businesses pull this from accounting software or e-commerce platforms integrated with sales tax automation tools. Manual calculation across 500+ jurisdictions is essentially impossible without software.

Step 2: Calculate Taxable vs. Exempt Sales

Not everything’s taxable. California exempts specific transaction types, and proper categorization matters for accurate reporting. Common deduction categories include:

- Sales for resale (wholesale transactions with valid resale certificates)

- Nontaxable food products (groceries meeting specific criteria)

- Nontaxable labor (repair and installation services)

- Sales to US government (federal, state, local government purchases)

- Interstate/foreign commerce (items shipped out of state)

Each exemption type requires documentation maintained for audits. Miscalculating exemptions creates problems either way. Overtaxing loses customer goodwill and triggers refund requests. Undertaxing creates audit liability and penalties.

Step 3: Allocate Tax by District

California requires district-level allocation showing exactly how much tax applies to each jurisdiction. Your return must break down collections by state, county, city, and special district components.

This district allocation is where most manual errors occur. A single misallocated transaction throws off your entire return, triggering CDTFA notices and requiring amended filings.

Step 4: Complete Your CDTFA Return

Log into CDTFA Online Services using your seller’s permit number. The system guides you through entering gross sales, deductions, taxable sales, district allocations, and tax due.

You’ll answer business-specific questions, then navigate through multiple schedules. The system calculates liability automatically based on entered data, then compares it to prepayments and credits to determine payment due or refund owed.

Step 5: Submit Payment

California requires electronic payment for businesses with estimated monthly tax liability of $10,000 or more. Options include ACH debit from your bank account, credit card (with processing fees), or wire transfer for large payments.

Payment must be received by the deadline. Initiated or pending doesn’t count. If the deadline falls on a weekend or holiday, payment must arrive by the preceding business day, not the following one.

Insufficient funds or rejected transactions trigger penalties identical to non-payment: 10% penalty plus daily interest.

Step 6: Maintain Documentation

California requires maintaining records supporting your return for at least four years. This includes sales invoices, exemption certificates, purchase records, accounting ledgers, and payment confirmations.

During audits, the CDTFA requests documentation proving reported figures. Missing exemption certificates means previously exempt sales become taxable, creating unexpected liability plus penalties.

Understanding California’s Filing Schedules

California’s reporting system requires completing multiple schedules that break down your sales by location and jurisdiction. Understanding these schedules is essential for accurate filing.

Schedule C reports taxable sales at your registered California business locations. If you have a physical storefront or warehouse, you’ll report sales from those addresses here.

Schedule B breaks down sales by county for local tax purposes. You’ll enter taxable amounts for each county where you made sales, ensuring local jurisdictions receive their proper allocation.

Schedule A is where district tax reporting gets complicated. Each county often contains multiple special districts, like transportation districts, hospital districts, or tourism zones, each with its own rate. You’ll allocate sales to each applicable district, and the totals must reconcile perfectly with your gross sales.

This multi-schedule system exists because California’s 500+ tax jurisdictions each need accurate reporting to fund local services. A sale in downtown Los Angeles might incur state tax, county tax, city tax, and multiple district taxes, all requiring separate reporting lines.

Most businesses find this allocation process the most error-prone part of filing. One misallocated transaction throws off multiple schedules, triggering CDTFA notices. The “remaining amount to be reported” must always equal zero before you can submit, forcing perfect mathematical reconciliation across all three schedules.

This complexity is exactly why businesses partner with HOST. We handle district allocation automatically using validated address-level data, ensuring accurate reporting across all jurisdictions without the manual reconciliation headaches.

Common California Sales Tax Reporting Mistakes

Incorrect District Allocation

Allocating tax to the wrong district is the most common error. California’s 500+ jurisdictions overlap in complex ways. A single street can span multiple tax districts.

The CDTFA imposes penalties when district allocations are materially incorrect, even if total tax remitted is correct.

Missing Exemption Certificates

Accepting exemption claims without obtaining proper certificates creates audit liability. During audits, every exempt transaction needs a certificate on file. Missing documentation means those sales become taxable retroactively, with penalties and interest applied.

Failing to Track Use Tax

Many businesses forget to report use tax on out-of-state purchases where the seller didn’t collect California tax. If you buy inventory, supplies, or equipment without California sales tax, you owe use tax.

HOST’s team manages these confusing state notices so you don’t have to decipher them yourself.

Late Filing and Payment

California’s penalties are severe. Late filing: 10% of tax due. Late payment: 10% penalty plus 0.5% monthly interest. The penalties stack! File late AND pay late, you’re facing a 20% penalty immediately plus ongoing interest.

Filing even one day late triggers the full 10% penalty with no grace period.

HOST: Your Partner for California Sales Tax Reporting

California’s reporting requirements consume hours monthly without generating revenue. Between district allocation complexity, prepayment calculations, and documentation requirements, staying compliant demands specialized expertise.

What HOST Delivers:

- Nexus Analysis: We determine whether you’ve met California’s $500,000 threshold or triggered physical nexus

- CDTFA Registration: We handle your seller’s permit application and CDTFA communications

- Automated Filing: We prepare and file your returns quarterly, monthly, or with prepayments

- District Allocation Management: We ensure accurate allocation across 500+ jurisdictions using validated address data

- Software Optimization: We configure your TaxJar, Avalara, or other tools for accurate California calculations

- Notice Management: We interpret and respond to CDTFA notices, protecting you from penalties

- Audit Defense: We’re your trusted partner in resolving California sales tax audits

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate California’s complex requirements. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

Take California Sales Tax Reporting Off Your Plate

California sales tax reporting doesn’t have to consume hours monthly or create constant worry. Every hour spent researching allocations, calculating prepayments, or filing returns is an hour not spent growing your business.

Whether you’re crossing California’s $500,000 threshold, struggling with district allocation, or overwhelmed by prepayment calculations, professional help eliminates guesswork and prevents costly mistakes.

At HOST, we combine deep California expertise with 25+ years of specialized experience, transparent communication, and personalized support. You handle the sales, we handle the tax.

Contact us today to discuss your California sales tax needs or schedule a free consultation. Let us handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

How often do I need to report sales tax in California?

Most California businesses file quarterly with deadlines April 30, July 31, October 31, and January 31. High-volume sellers averaging over $17,000 monthly tax liability typically file monthly. The CDTFA assigns your filing frequency during registration.

What happens if I file my California sales tax return late?

Late filing triggers a 10% penalty immediately with no grace period. Late payment adds another 10% penalty plus 0.5% monthly interest accruing daily. These penalties stack. File and pay late, you face a 20% penalty immediately plus ongoing interest.

Do I need to report sales tax in California if I only sell online?

Yes, if you exceed $500,000 in total California sales during the current or previous calendar year. The Wayfair decision eliminated physical presence requirements. Remote sellers meeting economic nexus thresholds must register, collect, and report California sales tax.

How do I allocate sales tax across California’s different districts?

District allocation requires identifying customer destination addresses, determining which state, county, city, and special district taxes apply, then reporting the breakdown. Sales tax automation software handles this automatically. Manual allocation across 500+ jurisdictions is extremely error-prone.

Can I file California sales tax returns by mail, or must I file online?

The CDTFA requires most filers to use the online filing system. Paper returns are only accepted for filers specifically authorized by the department.

What records must I keep to support my California sales tax returns?

California requires maintaining sales invoices, exemption certificates, purchase records, accounting ledgers, payment confirmations, and all supporting documentation for at least four years. During audits, missing exemption certificates mean previously exempt sales become taxable retroactively with penalties and interest.

What if I discover an error after filing my return?

You can file an amended return through CDTFA Online Services by checking the “amended return” box and entering corrected information. File amendments as soon as you discover errors to minimize interest charges. The CDTFA processes amended returns to adjust your account accordingly.