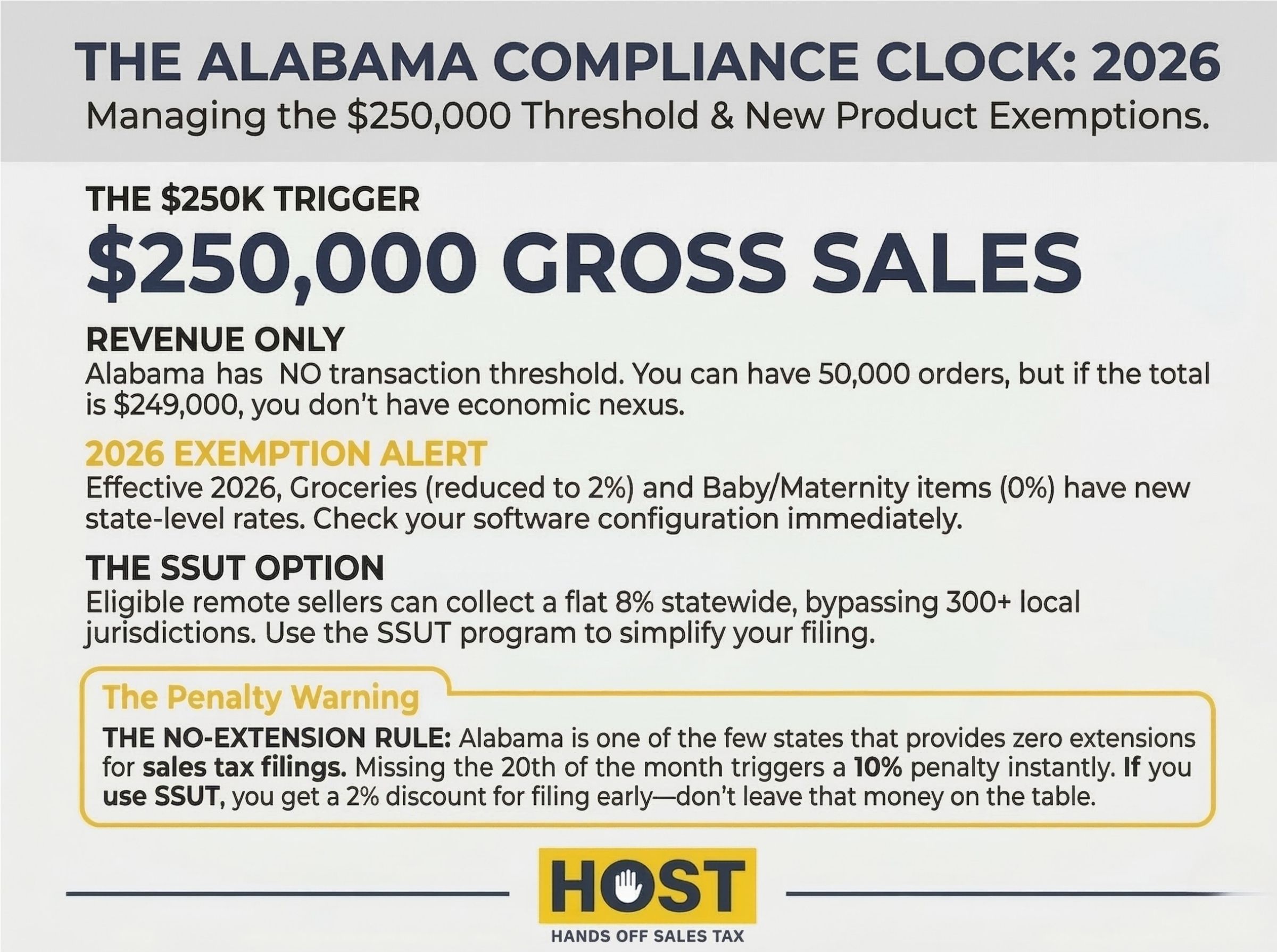

Understanding how to explain economic nexus for online businesses starts with one Supreme Court decision that changed everything. The 2018 South Dakota v. Wayfair ruling eliminated the physical presence requirement for sales tax collection, forcing online sellers to track obligations across 45+ states based purely on sales volume.

Cross an invisible threshold in a state, which is typically $100,000 in sales or 200 transactions, and you’ve triggered mandatory registration, collection, and filing requirements. Miss these obligations and audits, penalties, and back taxes can devastate your operation.

Hands Off Sales Tax (HOST) specializes in helping online businesses navigate the post-Wayfair landscape. From nexus analysis determining exactly where you’ve crossed thresholds, to automated multi-state filings and audit defense, HOST handles the complexity so you can focus on growth.

What Is Economic Nexus?

Economic nexus is the legal principle allowing states to require sales tax collection from businesses based solely on economic activity within state borders. No physical presence required. After Wayfair overturned the 1992 Quill precedent, states gained authority to impose obligations on remote sellers exceeding state-specific thresholds.

The Wayfair Decision Explained

Before June 21, 2018, the Supreme Court’s Quill Corp. v. North Dakota decision protected online sellers. No physical presence (no warehouse, office, or employees) meant no requirement to collect sales tax. This created a competitive advantage for e-commerce over brick-and-mortar stores.

South Dakota challenged this framework, arguing it lost approximately $50 million annually in uncollected sales tax while local retailers faced unfair competition. The ruling addressed a fundamental fairness issue—online retailers effectively had a 6-10% price advantage over local stores simply by avoiding sales tax collection. States were hemorrhaging revenue, the GAO estimated $13+ billion in uncollected taxes annually, because consumer self-reporting compliance rates hover around 1-2%.

The Supreme Court ruled 5-4 in South Dakota’s favor, finding that physical presence rules were “unsound and incorrect” in the modern digital economy. Justice Kennedy wrote that Quill created market distortions inappropriate for the contemporary marketplace.

Wayfair didn’t mandate specific thresholds. It gave states authority to impose economic nexus laws as they saw fit, resulting in a patchwork of varying requirements across 45 states—the compliance burden online sellers face today.

How Economic Nexus Works for Online Businesses

Each state sets its own economic nexus threshold, typically based on gross sales revenue or transaction count within a 12-month period. Cross a state’s threshold and you’ve established nexus. You must register, collect, and remit sales tax there.

Common Economic Nexus Thresholds

Most states adopted thresholds similar to South Dakota’s original law:

- $100,000 in sales: California, Texas, Florida, New York, Illinois, and 30+ other states use this revenue threshold.

- $100,000 OR 200 transactions: Some states include both criteria—exceeding either triggers nexus. Examples include New York, Illinois, and New Jersey.

- Higher thresholds: Texas requires $500,000 in revenue. California has no transaction count requirement.

The 12-month measurement period varies. Some states measure by calendar year, others by rolling 12 months, and a few use the previous calendar year to determine current-year obligations. You might cross California’s threshold in March but Texas’s threshold in October, triggering different registration deadlines.

Registration timing varies dramatically by state. Texas requires registration by the first day of the fourth month after crossing thresholds. Rhode Island allows until January 1 of the year after reaching the threshold. Some states demand immediate registration. These variations make compliance timing as complex as the thresholds themselves.

What Counts Toward Thresholds

States generally include all retail sales delivered into the state, whether or not you collected sales tax:

- Gross revenue counts: The $100,000 threshold applies to total sales, not profit.

- Exempt sales typically count: Sales of non-taxable items or to exempt buyers usually still count toward threshold calculations.

- Marketplace sales vary: Platforms like Amazon collect tax under marketplace facilitator laws, but some states still count those sales toward your independent nexus threshold.

Digital products and SaaS face even more complexity. Not all states tax digital goods like e-books, online courses, or music downloads. Those that do define them differently. SaaS businesses face particularly unique regulations since the software isn’t downloaded. Some states classify it as a service, others as tangible property. Rules vary dramatically between physical products and digital offerings.

This complexity is precisely why HOST’s nexus analysis service examines your complete sales footprint, ensuring you’re collecting in the right states without over-registering.

Physical Nexus Still Matters

Economic nexus added another layer to physical nexus. Physical presence creates nexus regardless of sales volume:

- Inventory in fulfillment centers: Amazon FBA or third-party warehouse storage creates physical nexus immediately.

- Employees or contractors: Remote workers, sales reps, or contractors performing services in a state can create nexus.

- Temporary presence: Trade shows, installations, or deliveries can trigger nexus in some states.

For online businesses using multi-channel fulfillment, physical nexus can create obligations in 8-10 states before you even consider economic nexus. HOST’s comprehensive nexus analysis evaluates both to identify all obligations.

Registration and Compliance Requirements

Once you’ve crossed an economic nexus threshold, states require specific actions within defined timeframes.

Registration Process

You must apply for a sales tax permit in each state where you’ve established nexus. This involves completing state applications requiring business information, ownership details, and expected sales volume, then obtaining permits authorizing you to collect sales tax.

Critical: Never collect sales tax before completing registration. Collecting without proper permits creates legal complications in most states.

Registration seems straightforward until you encounter state-specific complications: North Dakota requires separate city registrations in some localities. Louisiana has both state and parish-level permits. Colorado has dozens of self-collecting home-rule cities requiring individual registrations.

HOST handles sales tax registration in all required states, managing paperwork, follow-up, and state communications so you’re properly licensed everywhere.

Ongoing Filing Obligations

After registration, you’ll file returns on schedules determined by your sales volume:

- Monthly filing: High-volume sellers often file monthly

- Quarterly filing: Mid-volume sellers typically file quarterly

- Annual filing: Low-volume sellers may file annually

Each state assigns filing frequency based on tax collected. In Texas, you might file monthly while filing quarterly in New York, creating a complex calendar of deadlines across dozens of jurisdictions.

Returns include not just state-level taxes but county, city, and special district taxes. HOST’s filing services manage returns across all jurisdictions, keeping everything current so you avoid penalties.

The Real Impact on E-Commerce Businesses

Economic nexus obligations multiplied compliance burdens exponentially. Pre-Wayfair, a California-based seller might only collect California sales tax. Post-Wayfair, that same seller crossing thresholds in 20 states now manages 20 registrations and 20+ filing schedules.

Time and Resource Drain

Managing multi-state sales tax compliance consumes significant time. Companies spend 30+ hours monthly on sales tax administration: maintaining software, pulling data, filing returns, handling notices, tracking law changes.

For lean e-commerce teams, this represents enormous productivity loss. Every hour spent on compliance is time not spent on marketing or customer service, activities that actually generate revenue.

Audit Risk and Penalties

States aggressively pursue sales tax from remote sellers. An audit can uncover years of unfiled returns with penalties including back taxes, compounding interest, and late filing penalties reaching 25-50% of tax owed.

For a business that crossed nexus thresholds 3 years ago but never registered, a $100,000 tax liability can easily become $150,000+ with interest and penalties.

HOST offers audit defense services, acting as your trusted partner by organizing documentation, communicating with authorities, and defending your position to minimize liability.

Common Mistakes Online Businesses Make

Waiting Too Long to Address Nexus

Many businesses discover economic nexus obligations years after crossing thresholds, often during growth phases when no one was monitoring compliance. The “I didn’t know” defense doesn’t eliminate liability, states still assess back taxes and penalties.

Tracking thresholds manually across multiple sales channels becomes nearly impossible as you scale. Your website, Amazon, eBay, Etsy, retail locations, all channels contribute to state thresholds. Missing even one channel could mean overlooking nexus obligations entirely, and by the time you realize it, you’re facing years of back taxes.

Early nexus analysis prevents this. By identifying obligations proactively, you can register in states where you’ve recently crossed thresholds and potentially use voluntary disclosure agreements (VDAs) for states where you’ve had unreported nexus for longer periods.

HOST facilitates VDAs with states to limit lookback periods and abate penalties when businesses discover past obligations.

Relying Solely on Automation Software

Sales tax software like TaxJar or Avalara automates rate calculations and assists with filing. However, software requires proper configuration. Common mistakes include treating non-taxable items as taxable, missing required local taxes, or double-taxing due to system overlap.

Software doesn’t determine where you have nexus, doesn’t register you in new states, and won’t respond to state notices on your behalf.

HOST offers a free sales tax software review to audit your existing configuration and identify costly errors before they impact your bottom line.

Voluntary Disclosure Agreements

If you discover you’ve had economic nexus for years without collecting tax, voluntary disclosure agreements offer a path to compliance with reduced penalties.

VDAs are agreements between taxpayers and states where you voluntarily come forward to report past liabilities. In exchange, states typically limit lookback periods to 12-36 months instead of 3-4 years, waive failure-to-file and failure-to-pay penalties, and provide anonymity while exploring terms.

HOST manages the VDA process with states, negotiating favorable terms and guiding you through disclosure to resolve past obligations efficiently.

How HOST Helps Navigate Economic Nexus

Economic nexus transformed sales tax compliance from a manageable obligation into a complex, multi-state challenge requiring specialized expertise. HOST provides comprehensive solutions:

Nexus Analysis: We analyze your sales data across all channels and states to determine precisely where you’ve met economic or physical nexus thresholds.

Sales Tax Registration: We handle registrations in all required states, managing paperwork and state communications.

Automated Filing Services: We prepare and file returns across all jurisdictions based on each state’s requirements.

Audit Defense: We organize documentation, communicate with tax authorities, and defend your position during audits.

VDA Support: We facilitate voluntary disclosure agreements with states, limiting lookback periods and abating penalties.

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate compliance. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

Ready to Achieve Compliance?

Economic nexus obligations aren’t going away. Every state continues refining rules, adjusting thresholds, and improving enforcement. Staying compliant requires ongoing attention, or the right partner to handle it for you.

Whether you’re crossing thresholds in multiple states, managing existing obligations, or discovering past nexus, HOST ensures sales tax supports growth rather than hindering it. Contact us today to discuss your compliance needs or schedule a free consultation.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What exactly is economic nexus?

Economic nexus is the legal requirement to collect sales tax in a state based solely on sales volume or transaction count within that state, regardless of physical presence. It was established by the 2018 Wayfair Supreme Court decision, which overturned previous physical presence requirements.

How do I know if I’ve crossed economic nexus thresholds?

You must track gross sales delivered into each state over a 12-month period. Most states use $100,000 in revenue as the threshold, though some include transaction counts (typically 200) or use higher revenue thresholds.

Do marketplace sales through Amazon count toward nexus thresholds?

This varies by state. Some states count all sales delivered into the state toward thresholds, even if Amazon collected the tax. Other states exclude marketplace facilitator sales from independent nexus calculations.

What happens if I’ve had economic nexus for years but never registered?

You’re liable for back taxes, interest, and penalties for the period you had nexus without collecting. However, voluntary disclosure agreements (VDAs) can limit lookback periods to 12-36 months and waive penalties, significantly reducing financial impact.

Can sales tax software handle economic nexus compliance?

Software automates rate calculations and can assist with filing, but it doesn’t determine where you have nexus, register you in new states, or respond to state notices. Software requires proper configuration and oversight.

How often do I need to file sales tax returns?

Filing frequency varies by state and your sales volume in each state. High-volume sellers typically file monthly, mid-volume sellers file quarterly, and low-volume sellers may file annually. Each state assigns frequency independently, creating different deadlines across jurisdictions.