Ecommerce sales tax compliance demands systematic attention across dozens of jurisdictions, each with distinct thresholds and filing requirements. After the 2018 Wayfair decision eliminated physical presence requirements, online sellers face obligations in states they’ve never visited, turning straightforward bookkeeping into a compliance labyrinth.

2025 brings heightened enforcement. States like California, Illinois, Wisconsin, and Washington have ramped up audit activity significantly. Many states eliminated transaction count thresholds (Alaska in January, Utah in July), simplifying tracking but lowering barriers for triggering nexus. Meanwhile, platforms like Shopify’s Shop App now operate as marketplace facilitators, creating new reconciliation challenges when tax is withheld before deposits reach your account.

Hands Off Sales Tax (HOST) specializes in managing multi-state compliance for ecommerce businesses. From nexus analysis to automated filings, we handle the complexity so you can focus on growth instead of decoding tax codes.

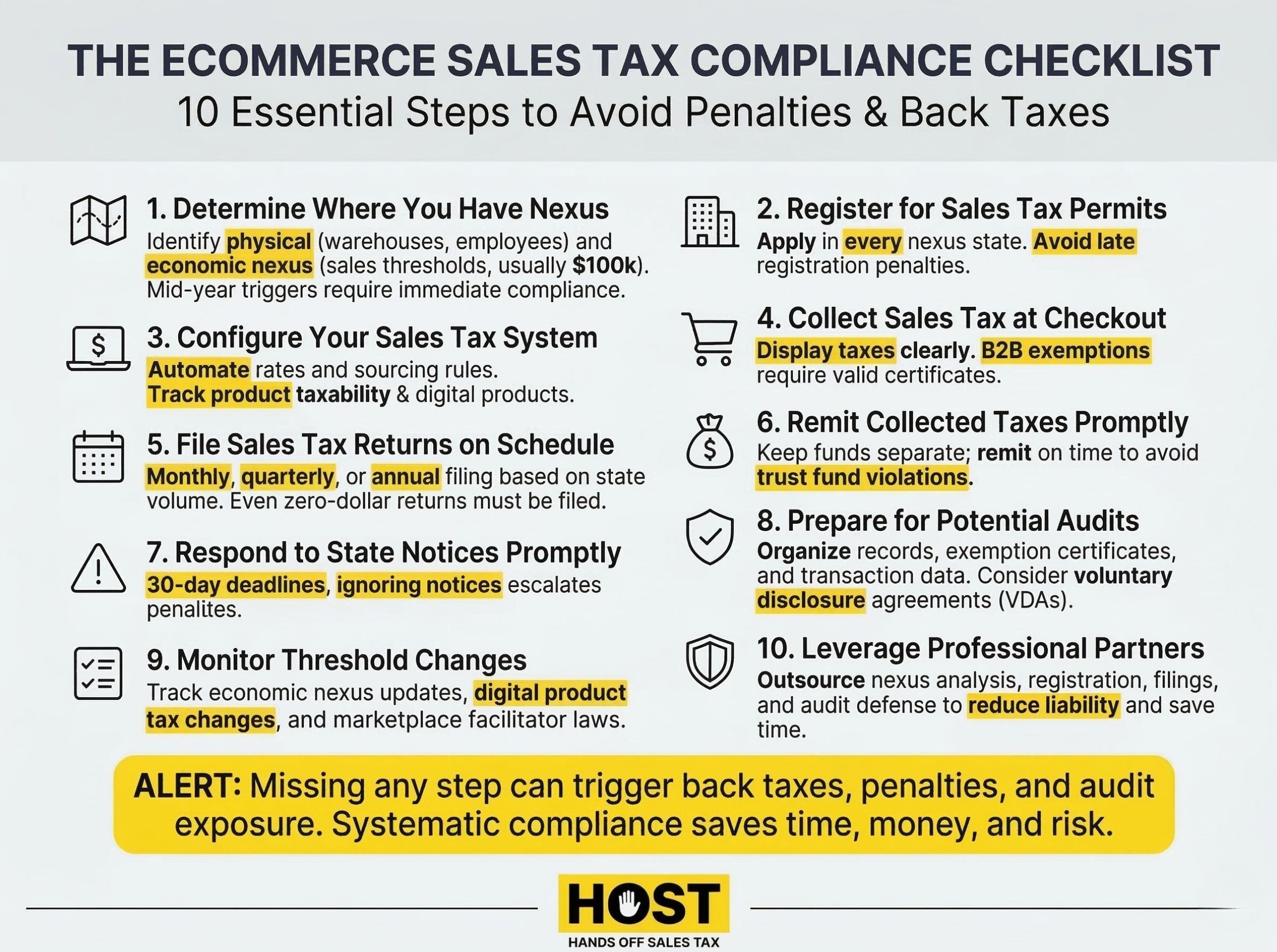

Step 1: Determine Where You Have Nexus

Nexus establishes a state’s authority to require sales tax collection. Post-Wayfair, two types trigger obligations:

Physical Nexus occurs through tangible presence. Offices, warehouses, employees, inventory. A single day at a trade show creates nexus. Inventory stored in Amazon FBA warehouses establishes nexus in those states, often without sellers realizing it.

Economic Nexus triggers when crossing state-specific sales thresholds. Most states require around $100,000 in annual sales, though significant variations exist. California demands $500,000. Texas uses $500,000. Many states have eliminated transaction counts, simplifying compliance.

Monitor sales by state monthly. Crossing a threshold mid-year means obligations begin immediately, not next January. Economic nexus thresholds and measurement periods vary significantly, requiring careful tracking.

HOST’s nexus analysis service examines your complete sales footprint, identifying exactly where you’ve triggered collection obligations and which registrations you need.

Step 2: Register for Sales Tax Permits

Once you’ve identified nexus states, registration becomes mandatory before collecting tax. Each state requires separate applications with unique documentation like EIN numbers, business structure details, projected sales figures.

Processing times vary dramatically. Some states issue permits electronically within days. Others require 4-8 weeks for paper processing. Late registration triggers penalties even if you weren’t collecting tax yet. States expect compliance from the moment nexus occurred.

Common registration mistakes include incorrect NAICS codes, mismatched business names, and failing to register for local taxes in home-rule states like Colorado or Louisiana where hundreds of separate jurisdictions require individual registration.

HOST handles sales tax registration across all required jurisdictions, managing paperwork, follow-ups, and ensuring you’re properly licensed everywhere you conduct business.

Step 3: Configure Your Sales Tax System

Accurate calculation prevents both undercollection (creating liabilities) and overcollection (harming customer trust). The U.S. has over 12,000 tax jurisdictions with rates that change frequently.

Manual calculation becomes impossible at scale. Rates vary by customer address down to the ZIP+4 level. Origin versus destination sourcing rules differ by state. Product taxability varies. Clothing is tax-exempt in some states, taxable in others, with exemptions only for items under specific price thresholds elsewhere.

Sales tax automation software like TaxJar or Avalara provides real-time calculation through API integration. These systems maintain updated rate tables and apply correct sourcing rules automatically.

Configuration errors create costly problems. Common mistakes include treating wholesale transactions as retail sales, double-taxing when multiple systems overlap, or incorrectly categorizing products. Digital products present particular challenges like SaaS taxability varies dramatically by state (Connecticut taxes it fully, California exempts it, Texas taxes 80%).

Modern transaction types add complexity. Buy Online, Pick Up In-Store (BOPIS) orders may trigger different sourcing rules than shipped sales. Buy Now, Pay Later (BNPL) services can complicate timing of tax recognition and payment processing.

HOST offers a free sales tax software review to audit your existing configuration and identify costly errors before they become audit problems.

Step 4: Collect Sales Tax at Checkout

Collection begins the moment registration completes in a state. Delaying collection while registered creates liabilities. You owe the tax whether or not you collected it from customers.

Display tax clearly at checkout. Transparency reduces cart abandonment. Customers accept taxes they expect but abandon carts when surprised by unexpected charges.

For marketplace sellers, platform facilitator laws shift collection responsibility to Amazon, eBay, or Etsy in most states. Starting January 2025, Shopify’s Shop App operates as a marketplace facilitator, collecting and remitting tax directly to states. This creates accounting challenges such as your sales reports showing full amounts including tax, but bank deposits are lower because the platform withheld it. Without proper reconciliation, you’ll face mismatched books and potential compliance issues.

You remain responsible for non-marketplace sales and for states where marketplace facilitator laws don’t cover your transaction types.

Exemption certificates require careful handling. B2B sales to registered resellers are typically exempt, but only with valid certificates on file. Accepting verbal claims without documentation exposes you to liability during audits.

Step 5: File Sales Tax Returns on Schedule

Filing frequency depends on your sales volume in each state. High-volume sellers file monthly. Medium volume files quarterly. New or low-volume registrants file annually. States assign frequencies based on expected tax liability. Typically under $100 monthly qualifies for quarterly filing, while higher amounts trigger monthly requirements. As your business grows, states may increase your filing frequency.

Deadlines vary by state. Most require filing by the 20th of the following month, but variations exist. Louisiana requires the 20th, Alabama uses different dates for quarterly filers, and several states use the last day of the month.

Missing deadlines triggers penalties immediately. Late filing penalties often start at $50 per return and increase with each month of delinquency. A $1,000 tax obligation filed 60 days late can balloon to $1,200+ after penalties and interest.

Even zero-dollar returns require filing in many states. If you’re registered but had no sales that period, you still must file a return indicating zero activity. Failing to file zero returns eventually triggers penalties and potential permit revocation.

HOST manages filing across all jurisdictions monthly, quarterly, or annually based on each state’s requirements, including local and special district returns, keeping everything current so you never face penalties.

Step 6: Remit Collected Taxes Promptly

Collected sales tax is held in trust for the state. Using collected funds for operations (even temporarily) constitutes trust fund misappropriation with severe penalties including personal liability for officers and owners.

Maintain separate accounting for collected sales tax. While separate bank accounts aren’t legally required, they prevent commingling and ensure sufficient funds exist when remittance is due.

Most states accept ACH direct debit or credit cards, though credit cards often incur convenience fees of 2-3%. Some states offer discounts for timely filing, typically 1-2% of tax due as vendor compensation for collection costs.

Step 7: Respond to State Notices Promptly

State revenue departments send notices for various reasons: requesting returns, questioning discrepancies, assessing penalties, or initiating audits. Ignoring notices escalates situations rapidly.

Common notice types include failure-to-file notices (when returns are late or missing), discrepancy notices (when reported sales don’t match state records), and nexus inquiry letters (when states identify potential obligations).

Response deadlines are strict, typically 30 days. Missing response deadlines often means automatic acceptance of the state’s assessment without opportunity for appeal.

HOST’s notice management service interprets confusing state correspondence and responds appropriately, protecting you from penalties while resolving issues efficiently.

Step 8: Prepare for Potential Audits

Sales tax audits examine 3-4 years of transaction history. States select audit targets based on industry risk profiles, sales volume, or nexus indicators from data-sharing agreements. Audit activity increased dramatically in 2024-2025, with California, Illinois, Wisconsin, Washington, Massachusetts, and Maine leading enforcement efforts. Penalties can reach 39% in some jurisdictions when penalties and interest compound.

Audit preparation requires organized records. States request complete sales data, exemption certificates, general ledger details, product descriptions, and documentation of any non-taxable transactions.

Common audit findings include uncollected tax on taxable sales, invalid exemption certificates, use tax on untaxed purchases, and errors in local tax allocation. Even small errors multiply across thousands of transactions into substantial liabilities.

Voluntary Disclosure Agreements (VDAs) offer amnesty before audits. If you discover past obligations, proactively filing VDAs limits lookback periods (typically 3-4 years versus unlimited) and often waives penalties entirely, leaving only tax and interest due.

HOST provides audit defense services, acting as your trusted partner in resolving sales tax audits by organizing documentation and defending your position to minimize liability.

Step 9: Monitor Threshold Changes

Economic nexus thresholds change. States adjust dollar amounts, eliminate transaction counts, or modify rules for specific industries. While most states adopted post-Wayfair rules by 2021, ongoing legislative sessions create new obligations or modify existing requirements.

Product taxability evolves. Digital products, SaaS, and marketplace transactions face ongoing legislative attention. States that once exempted digital goods now tax them. Services previously untaxed become taxable.

Marketplace facilitator laws expand. States initially covered major platforms but now extend requirements to smaller facilitators and niche platforms.

Expanding internationally introduces additional complexity. VAT and GST regimes operate differently than US sales tax, with their own registration thresholds and compliance requirements across dozens of countries.

Stay informed through industry publications, state revenue websites, or compliance partners who monitor changes. Ignorance doesn’t excuse non-compliance, so states expect businesses to track requirements.

Step 10: Leverage Professional Partners

Managing sales tax across 45+ states while running an ecommerce business diverts substantial time from revenue-generating activities. Most sellers spend 30+ hours monthly on sales tax administration with researching rules, filing returns, handling notices, tracking thresholds.

Professional compliance partners eliminate this burden entirely. Services include nexus analysis, registration management, calculation system optimization, filing automation, notice response, audit defense, and VDA facilitation.

Cost-benefit analysis strongly favors outsourcing. Professional compliance typically costs $1,000-10,000 annually which is a fraction of potential penalty exposure which can reach $10,000-100,000+ when factoring in back taxes, penalties, and interest across multiple states. A compliance partner costs less than hiring in-house expertise while delivering superior results through specialization and technology.

HOST has focused exclusively on sales tax services for 25+ years. Through parent company TaxMatrix, we’ve helped North America’s largest companies manage compliance requirements. Now we bring that expertise to small and medium-sized ecommerce businesses navigating identical multi-state challenges.

Ready to Simplify Your Compliance?

Sales tax compliance shouldn’t drain your time or create constant stress. Every hour spent researching rules or filing returns is an hour not spent growing your business.

Whether you’re crossing economic nexus thresholds in new states, unsure about product taxability, or overwhelmed by filing requirements across dozens of jurisdictions, professional help eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss your compliance needs or schedule a free consultation. Let us handle the tax so you can focus on sales.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What triggers sales tax obligations for ecommerce sellers?

Physical nexus (warehouses, inventory, employees) and economic nexus (exceeding state sales thresholds, typically $100,000 annually) both create obligations requiring registration, collection, and filing. Post-Wayfair, customer location determines obligations rather than seller location.

How often do I need to file sales tax returns?

Filing frequency varies by state and your sales volume: monthly for high volume, quarterly for medium volume, annually for low volume. Each state assigns frequencies independently, meaning you might file monthly in California but quarterly in Texas.

What happens if I miss a sales tax filing deadline?

Late filing penalties typically start at $50 per return and increase monthly. Interest accrues daily on unpaid balances. Repeated late filings can trigger audits, permit revocation, or criminal charges in extreme cases of trust fund misappropriation.

Do marketplace sellers need to collect sales tax?

Marketplace facilitator laws require platforms like Amazon, eBay, and Etsy to collect and remit sales tax in most states. However, sellers remain responsible for non-marketplace channels (own website, wholesale, B2B sales) and for reviewing platform-reported amounts.

Should I use sales tax software or hire a compliance service?

Software automates calculations but requires configuration, maintenance, and monitoring. Compliance services handle end-to-end obligations including registration, filing, notices, and audits. Most growing ecommerce businesses find full-service partners more cost-effective than internal management.

Can I be held personally liable for uncollected sales tax?

Yes. Collected sales tax is held in trust for states. Officers and owners can face personal liability for trust fund misappropriation if collected taxes are used for operations rather than remitted. This liability persists even through bankruptcy.