Understanding District of Columbia economic nexus requirements means knowing exactly when your business must start collecting sales tax in the nation’s capital. For e-commerce sellers operating across state lines, DC’s $100,000 threshold triggers collection obligations that many businesses miss until a notice arrives.

Economic nexus rules transformed sales tax compliance after the 2018 Wayfair decision. Remote sellers without physical presence now face collection requirements based purely on sales volume. The District implemented these rules in 2019, and non-compliance creates audit risk, penalties, and back taxes that devastate growing businesses.

That’s where Hands Off Sales Tax (HOST) provides clarity. We analyze your DC sales footprint, handle registration complexities, and manage ongoing filing obligations so you stay compliant without diverting focus from growth.

What Is Economic Nexus?

Economic nexus establishes a state’s authority to require sales tax collection based on economic activity rather than physical presence. Before the Supreme Court’s South Dakota v. Wayfair decision in June 2018, states could only require collection from businesses with physical presence, like stores, warehouses, employees, or inventory in-state.

Wayfair changed everything. The Court ruled states can require remote sellers to collect sales tax once they exceed state-specific economic thresholds. For online retailers, this means monitoring sales into every state and understanding when you’ve crossed each threshold. Missing a nexus trigger means you’re collecting late, often with penalties attached.

District of Columbia’s Economic Nexus Threshold

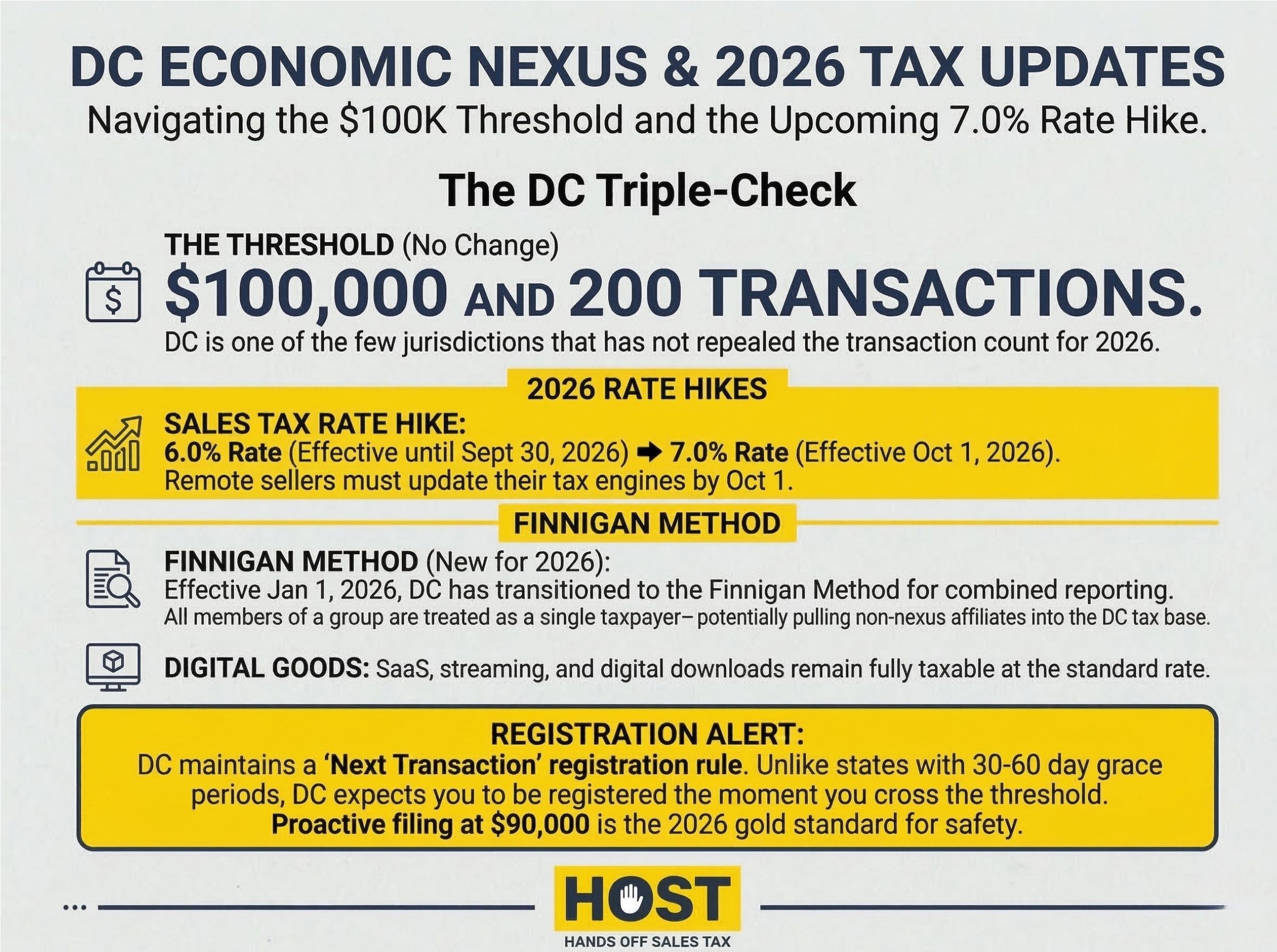

The District of Columbia established economic nexus for remote sellers effective January 1, 2019. DC requires registration when you exceed either of these thresholds during the previous or current calendar year:

- $100,000 in gross receipts from sales into the District, OR

- 200 or more separate retail sales delivered into the District

Meeting either threshold triggers the collection obligation. Both thresholds include all DC sales, whether taxable or exempt. Even if you sell primarily exempt items, those sales count toward determining if you’ve crossed the threshold. Once you exceed either threshold, you must register and begin collecting tax on taxable sales.

DC measures thresholds on a calendar year basis. If you hit $100,000 or 200 transactions during 2024, you trigger nexus and must register. The obligation continues into subsequent years even if your sales drop below thresholds, until you formally close your account.

Do Wholesale and Resale Transactions Count?

Here’s critical relief for B2B sellers: resale and wholesale transactions don’t count toward DC’s economic nexus thresholds. If you have $150,000 in DC sales but $80,000 is wholesale to businesses with valid resale certificates, only $70,000 counts toward the threshold, meaning you haven’t triggered nexus.

However, you must maintain valid, current resale certificates for every wholesale transaction. Missing documentation turns exempt wholesale sales into taxable retail sales during audits, potentially creating unexpected nexus and liability.

Similarly, sales to exempt customers (nonprofits with valid exemption certificates, government entities) don’t count toward thresholds. But sales of exempt products (prescription drugs, groceries) to regular consumers do count, even though no tax is collected. The distinction matters: it’s about the customer’s status, not the product’s taxability.

How DC Compares to Other States

DC’s $100,000 threshold aligns with most states post-Wayfair, but comparing reveals important differences. California and Texas set thresholds at $500,000, giving smaller sellers more breathing room. New York requires $500,000 and 100 transactions, a dual threshold. Virginia uses $100,000 or 200 transactions like DC.

DC’s relatively accessible threshold means smaller e-commerce businesses trigger nexus faster compared to states with higher bars. For businesses selling into multiple jurisdictions, DC often becomes one of the first states requiring registration after home state obligations.

Who Must Register for DC Sales Tax?

Any remote seller exceeding either threshold must register with the Office of Tax and Revenue and collect sales tax. This includes e-commerce retailers, subscription services, SaaS companies, and B2B sellers. Even wholesale transactions count toward the $100,000 or 200-transaction determination, though you may not collect tax on exempt wholesale sales.

Marketplace Facilitator Laws

DC enacted marketplace facilitator legislation effective April 1, 2019. Marketplaces like Amazon, eBay, Etsy, and Walmart must collect and remit sales tax on behalf of third-party sellers using their platforms.

If you sell exclusively through Amazon FBA, Amazon handles DC sales tax collection. You don’t need to register separately for marketplace-facilitated sales. However, if you also sell through your own website, you must track those direct sales separately. Many sellers operate hybrid models, like marketplace sales plus direct sales. Only your direct-to-consumer sales create registration obligations, but all DC sales count toward determining if you’ve exceeded thresholds.

HOST’s nexus analysis examines your complete sales footprint, separating marketplace-facilitated sales from direct sales to determine your actual registration obligations.

How to Register for DC Sales Tax

Once you’ve triggered economic nexus, registration is mandatory before you begin collecting tax. DC requires you to register “by the next transaction,” which sounds precise but creates practical confusion.

What “Next Transaction” Actually Means

DC’s guidance says you must register “by the next transaction” after exceeding thresholds. In practice, this means if you cross $100,000 on your 150th sale, you should register before making sale #151. If you hit 200 transactions with only $80,000 in sales, register before transaction #201.

Here’s the reality: registration takes 5-10 business days. If you make 20 more sales while waiting for approval, technically you’ve violated the requirement. DC hasn’t aggressively enforced this timing, but waiting invites risk.

Practical advice: Register when you’re within 10% of either threshold. If you’re approaching $90,000 or 180 transactions, start the registration process. This protects you from the timing squeeze and demonstrates good faith compliance if questions arise later.

The District requires online registration through the MyTax.DC.gov portal. Create an account with basic business information like your legal name, EIN, business address, and contact details. Complete the FR-500 Combined Business Tax Registration form, provide your business structure and NAICS code, then await confirmation.

Processing typically takes 5-10 business days. Once registered, you must begin collecting DC sales tax immediately on all taxable sales to DC customers.

Common Registration Challenges

Businesses often encounter obstacles. DC’s system sometimes requires physical DC addresses for certain fields, which confuses remote sellers. Determining the correct “start date” can be unclear if you’ve been selling into DC for years. Generally you want to use the date you triggered nexus.

International sellers face additional hurdles. If you’re based in Canada, the UK, or elsewhere outside the U.S., you’re still subject to DC economic nexus. You’ll need a U.S. bank account for tax remittance and potentially an EIN (Employer Identification Number) if you don’t already have one for federal tax purposes.

If you’ve been selling without collecting for months or years, you may owe back taxes. A Voluntary Disclosure Agreement can limit lookback periods and reduce penalties.

HOST handles DC registration end-to-end, ensuring your application is complete, accurate, and processed efficiently.

DC Sales Tax Rates and What’s Taxable

The District of Columbia charges a 6% sales tax rate on most tangible personal property and certain services. Unlike states with local jurisdictions adding their own taxes, DC has a single, uniform rate. No county or city taxes exist. Every taxable sale to a DC customer gets taxed at 6%, regardless of the specific address.

DC taxes most tangible personal property including clothing, electronics, furniture, books, and sporting goods. Exempt items include prescription medications, certain medical devices, and groceries for home consumption (though prepared food is taxable).

Digital Products: DC taxes digital goods, including downloaded or streamed software, music, movies, and books. If you sell SaaS, digital downloads, or streaming services to DC customers, these are generally taxable.

Services: DC taxes select services including telecommunications, parking and storage, health club memberships, and some repair services. Many professional services remain exempt (accounting, legal, consulting), but verify if your specific service falls under taxable categories.

Filing Frequency and Deadlines

Once registered, you must file sales tax returns regularly. DC assigns filing frequency based on your tax liability:

Monthly Filers: Businesses with average monthly tax liability of $200 or more file monthly. Returns are due by the 20th of the following month.

Quarterly Filers: Businesses with average monthly liability under $200 may qualify for quarterly filing. Returns are due by the 20th of the month following the quarter-end.

Even if you had no DC sales during a period, you must file a zero return by the deadline. Failing to file creates penalties regardless of whether tax is owed. This catches seasonal sellers off-guard. DC sends delinquency notices for missing zero returns, and penalties apply even with $0 tax due. Many businesses discover this requirement only after receiving their first penalty notice.

DC imposes penalties for late filing and late payment: 5% of tax due per month (up to 25% maximum), 10% late payment penalty, and interest around 10% annually. These penalties accumulate quickly, so a business owing $1,000 and filing three months late faces $150 in late filing penalties, $100 late payment penalty, plus interest.

HOST’s automated filing services ensure your DC returns are filed accurately and on time, every period, eliminating penalty risk.

What Happens If You Don’t Comply?

Non-compliance creates serious consequences. DC can assess uncollected tax retroactively. If you’ve been selling into DC for two years without collecting, you owe tax on all those sales plus penalties and interest. The Office of Tax and Revenue conducts audits of non-compliant sellers: time-consuming, expensive, and often uncovering additional liabilities. Penalties add up to 35% or more of tax due. In certain business structures, owners can be held personally liable for unpaid sales tax.

Voluntary Disclosure Agreements

If you discover you’ve triggered nexus but haven’t been collecting, a Voluntary Disclosure Agreement (VDA) offers a solution. DC allows businesses to come forward voluntarily, limiting lookback periods (typically to 3 years instead of the full statute of limitations) and often waiving penalties.

VDAs provide a path to compliance without devastating financial consequences. However, timing matters. Once DC contacts you about non-compliance, you lose VDA eligibility. HOST manages VDA filings with DC, negotiating favorable terms and minimizing your liability while bringing you into full compliance.

HOST: Your Partner for DC Sales Tax Compliance

District of Columbia economic nexus creates real obligations that demand attention. Between monitoring thresholds, navigating registration, determining taxability, and filing returns on time, sales tax compliance drains resources without adding revenue.

Hands Off Sales Tax has focused exclusively on sales tax for over 25 years. We bring enterprise-level expertise to e-commerce sellers of all sizes, managing DC compliance (and all other states) so you can focus on growth.

What HOST Delivers

Nexus Analysis: We analyze your complete sales footprint to determine exactly where you’ve triggered economic nexus, including DC.

DC Registration: We handle the entire registration process, completing forms, communicating with OTR, and ensuring your account is properly established.

Automated Filing: We prepare and file your DC returns on time, every period: monthly, quarterly, or annually as required.

Sales Tax Software Review: If you use automation tools, we audit your configuration to ensure DC tax calculates correctly.

Notice Management: If DC sends a notice, we interpret it and respond appropriately, protecting you from penalties.

Audit Defense: Should DC audit your business, we organize documentation, communicate with auditors, and defend your position.

Voluntary Disclosure: If you’ve been selling without collecting, we file VDAs to bring you into compliance while limiting lookback periods.

We’ve helped businesses navigate sales tax since 1999. Through our parent company TaxMatrix, we’ve served North America’s largest companies. Now we bring that expertise to e-commerce sellers facing the same multi-state complexity.

Ready to Handle DC Sales Tax Correctly?

District of Columbia economic nexus requirements don’t disappear when ignored, they accumulate into larger problems. Whether you’re just crossing thresholds, expanding into new markets, or discovering past non-compliance, the right partner ensures you stay ahead of obligations rather than reacting to notices.

Contact HOST today to discuss your DC sales tax needs, or schedule a free consultation. Let us handle the tax so you can focus on sales.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the District of Columbia economic nexus threshold?

The District of Columbia’s economic nexus threshold is $100,000 in gross receipts OR 200 or more separate retail sales during the previous or current calendar year. Meeting either threshold triggers the collection obligation.

Do marketplace sales count toward DC’s economic nexus threshold?

Yes, all DC sales count toward thresholds, including marketplace-facilitated sales. However, if you sell exclusively through marketplaces like Amazon, the marketplace handles collection and you don’t need to register. Direct sales through your own channels require separate registration once you exceed thresholds.

What is DC’s sales tax rate?

The District of Columbia charges a uniform 6% sales tax rate on most tangible personal property and certain services. Unlike states with local taxes, DC has a single rate throughout the entire district.

When do I need to start collecting DC sales tax after triggering nexus?

You should register and begin collecting as soon as you determine you’ve exceeded either threshold. DC expects prompt registration, ideally within 30 days. Delaying creates back tax liability and penalties on uncollected tax.

Are digital products taxable in DC?

Yes, the District of Columbia taxes digital goods including downloaded or streamed software, music, movies, e-books, and similar digital products delivered electronically to DC customers.

What happens if I’ve been selling into DC without collecting sales tax?

If you’ve exceeded thresholds but haven’t been collecting, you owe back taxes plus penalties and interest. A Voluntary Disclosure Agreement can limit the lookback period (typically to three years) and often waive penalties, significantly reducing your liability compared to waiting for DC to discover the non-compliance.

I’m an international seller. Do DC nexus rules apply to me?

Yes. Remote sellers based outside the United States (Canada, UK, Europe, etc.) are subject to DC economic nexus if they exceed thresholds. You’ll need a U.S. bank account for tax remittance and an EIN for registration purposes.

Do my wholesale sales count toward the $100,000 threshold?

No. Sales to customers with valid resale certificates don’t count toward DC’s economic nexus thresholds. However, you must maintain current, valid resale certificates for every wholesale transaction. Missing documentation can turn exempt sales into taxable sales during audits.

What if I hit the threshold mid-month?

DC requires registration “by the next transaction” after exceeding thresholds. If you cross $100,000 on January 15th, you should register before your next DC sale. Since registration takes 5-10 business days, we recommend registering proactively when you’re within 10% of either threshold.