Cross $100,000 in Colorado sales and you’ve triggered economic nexus, even without setting foot in the state. But here’s where it gets messy: Colorado’s home rule cities turn what should be straightforward compliance into a multi-jurisdictional maze that catches most remote sellers completely off guard.

Understanding Colorado economic nexus rules determines whether your online business must collect sales tax in the Centennial State. The threshold itself is simple. The filing reality? That’s where businesses stumble.

Hands Off Sales Tax (HOST) manages Colorado nexus analysis, registration, and ongoing filings across all jurisdictions (state and local)so you stay compliant without drowning in administrative overhead.

What Is Economic Nexus in Colorado?

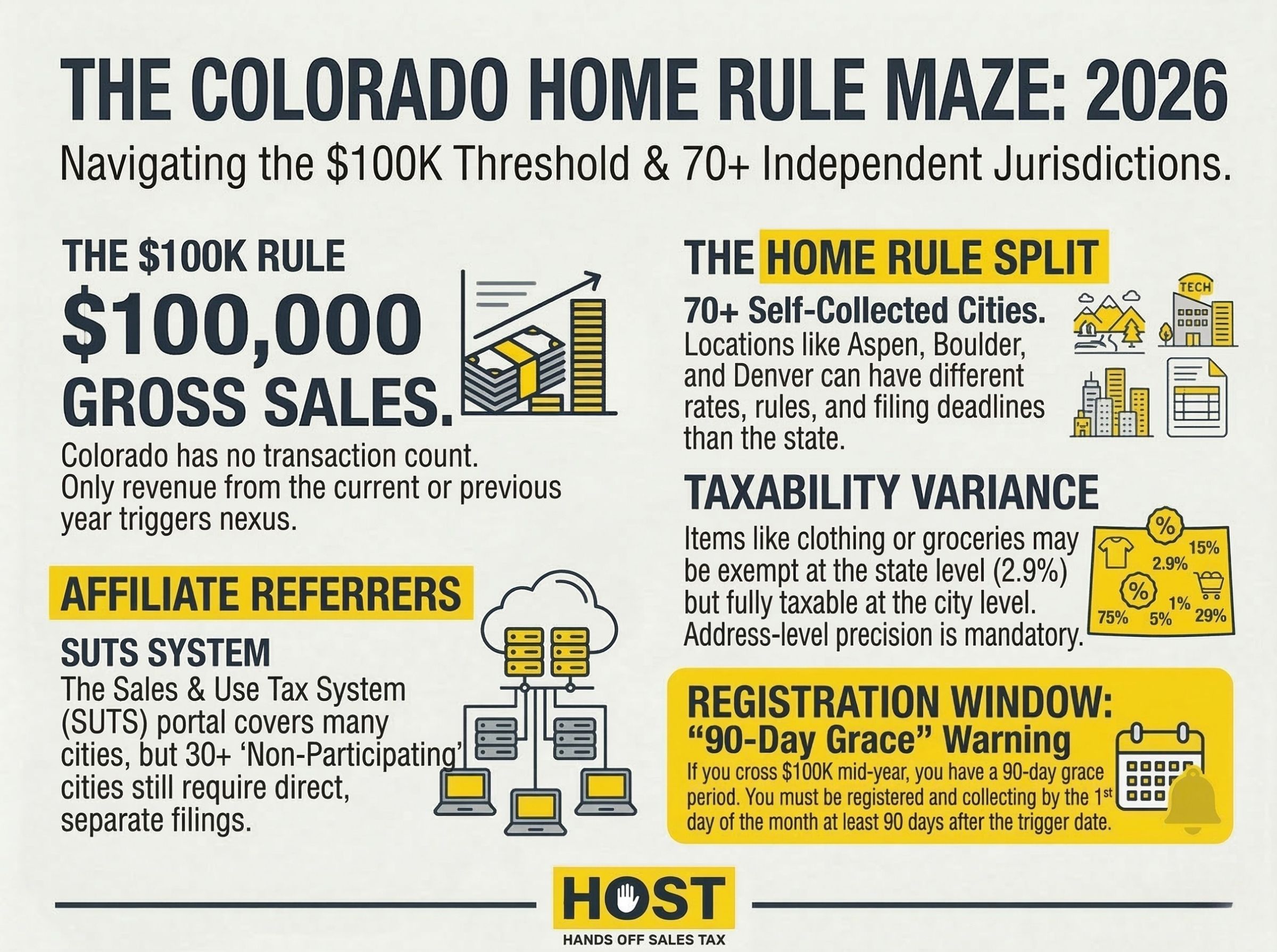

Economic nexus creates a sales tax collection obligation based on your sales volume alone. No physical presence required. After the 2018 Wayfair decision, Colorado established its threshold: $100,000 in gross sales into Colorado during the current or previous calendar year.

Hit $100,000 in 2025 or 2024? You have economic nexus. You must register and collect Colorado sales tax.

Unlike many states, Colorado doesn’t use a transaction count threshold. Just dollars. The threshold applies to gross sales of tangible personal property and taxable services delivered into Colorado. Track your sales annually. Once you cross $100,000 in either the current or previous year, collection obligations begin.

Marketplace sales where the platform already collects tax don’t count toward your threshold. Your direct sales through all other channels do.

Colorado’s Home Rule Complication

Here’s what separates Colorado from nearly every other state: approximately 70 home rule cities and counties administer their own separate sales tax systems. Different rates. Different rules. Different exemptions. Different filing deadlines.

Colorado’s state sales tax sits at 2.9%. That’s the easy part. But you also face obligations to individual home rule jurisdictions like Denver, Boulder, Colorado Springs, Aspen, and Aurora—each operating independent tax systems with rates ranging from 3% to over 8% when combined with county and special district taxes.

You don’t file one Colorado return. You file dozens.

Home rule cities require separate registration, separate filings, and separate remittance. Each jurisdiction maintains its own account numbers, login credentials, and reporting formats. Denver’s deadline might differ from Boulder’s. Aspen’s exemptions might contradict state rules.

Clothing is generally exempt from state sales tax but may be taxable in certain home rule jurisdictions. Food for home consumption is exempt at the state level but taxed in some cities. The same product gets different tax treatment depending on the customer’s specific address.

Combined rates can exceed 11% in some areas. But the real burden is managing separate filing relationships with dozens of municipalities.

How Economic Nexus Affects Remote Sellers

Threshold Monitoring

You must track your Colorado sales continuously. All sales of tangible personal property and taxable services delivered to Colorado customers count, regardless of how you fulfill them. FBA sales, drop-shipped orders, direct shipments. They all contribute to threshold calculation.

Registration Requirements

Cross $100,000 and you must register with the Colorado Department of Revenue for state sales tax. Timing matters: if you exceed the threshold mid-year, you get a 90-day grace period. Hit $100,000 on June 15? You must register and begin collecting by October 1 (the first day of the first month at least 90 days after crossing). If you exceeded the threshold last year, you must begin collecting January 1 of the current year.

That’s step one.

Step two catches everyone: separately registering with each home rule jurisdiction where you have customers. Potentially dozens of individual applications, each with unique requirements.

Colorado created the Sales & Use Tax System (SUTS) to simplify this. A centralized portal where you can file for the state and participating home rule cities in one place. Approximately 40 home rule cities participate. But that leaves 30+ that don’t. For non-participating cities like Aspen and Telluride, you’re back to separate registrations and separate filings.

Many sellers register with the state and assume they’re done. They’re not. Home rule cities actively pursue remote sellers who collect state tax but fail to remit locally. Some municipalities enforce economic nexus provisions without formal notice to impacted sellers, making retroactive compliance demands when they catch up with you.

Collection Obligations

After registration, you must collect the correct combined rate based on each customer’s specific location. Address-level precision matters because rates vary by street address.

Sales tax software can calculate rates, but only if configured correctly. Misconfigured systems charge wrong local rates, apply state exemptions where local taxes still apply, or miss special district taxes entirely.

Filing and Remittance

Colorado assigns state filing frequency based on your liability. Typically monthly for new sellers. You file separately with the state and with each home rule jurisdiction.

State returns are generally due the 20th of the month following the reporting period. Home rule cities set their own deadlines. Some want filings by the 15th. Others by the 20th. Some by month-end.

Juggling dozens of deadlines, login credentials, and formats creates massive administrative burden. Missing any deadline triggers penalties, even when the tax owed is minimal.

Common Compliance Mistakes

Ignoring Home Rule Jurisdictions: The most expensive mistake. Sellers register with the state, assume compliance is complete, and discover years of unfiled returns and accumulating liabilities when a home rule city catches up with them.

Miscalculating the Threshold: Some businesses exclude certain sales or use net figures instead of gross. Colorado’s threshold is gross sales of tangible personal property and taxable services delivered into Colorado before deductions, returns, or discounts.

Using Incorrect Tax Rates: Colorado’s fragmented rate structure creates chaos. Sellers charge statewide averages, fail to update when jurisdictions change rates, or apply wrong local rates for specific addresses. Overcharging damages customer relationships. Undercharging creates tax liability you can’t retroactively collect.

Missing Exemption Nuances: Colorado exempts groceries, prescription drugs, and some agricultural products at the state level. Home rule jurisdictions may not honor these exemptions. You might collect local tax but not state tax on the same transaction. Failing to configure these differences leads to undercollection or overcollection.

How HOST Simplifies Colorado Compliance

Colorado’s multi-jurisdictional complexity makes it one of the toughest states for remote seller compliance. Hands Off Sales Tax handles every aspect so you can focus on business instead of managing dozens of tax filing relationships.

Comprehensive Nexus Analysis: We analyze your sales data across all channels to determine exactly when you’ve triggered Colorado economic nexus. We track threshold progression and notify you before obligations begin. Learn more about our nexus analysis services.

Complete Registration Services: HOST registers your business with the Colorado Department of Revenue and separately with every home rule jurisdiction where you have sales. We handle paperwork, follow-up communications, and credential management. Explore our sales tax registration service.

Accurate Tax Calculation Setup: We configure your sales tax software to calculate correct combined state and local rates for every Colorado address, accounting for home rule jurisdictions, special districts, and exemption differences. Get a free sales tax software review to identify potential issues.

Multi-Jurisdictional Filing Management: We prepare and file your Colorado state return and all home rule jurisdiction returns on time, every time, whether they’re SUTS participants or require separate submission. We manage different deadlines, formats, and requirements across all jurisdictions.

Ongoing Compliance Support: We monitor rate changes across Colorado jurisdictions and update systems accordingly. We handle notices from the state or home rule cities, interpret what they mean, and respond appropriately.

Audit Defense: If Colorado or any home rule jurisdiction audits your compliance, we’re your trusted partner in resolving it. We organize documentation, communicate with auditors, and defend your position to minimize liability. Learn about our audit defense services.

Ready to Handle Colorado Economic Nexus Correctly?

Colorado’s combination of economic nexus obligations and home rule complexity creates one of the most challenging compliance environments for remote sellers. Managing dozens of separate registrations, filings, and rate configurations demands specialized expertise and serious time investment.

The right partner eliminates this burden entirely. At HOST, we’ve managed Colorado sales tax for businesses of all sizes for over 25 years. We understand home rule nuances, track the constantly changing rate landscape, and ensure you’re compliant everywhere you need to be.

Whether you’ve just crossed the threshold, discovered years of missed obligations, or simply want to offload ongoing compliance, we’re ready to help. Contact HOST today to discuss your Colorado sales tax needs and discover how we handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the economic nexus threshold for Colorado?

Colorado’s economic nexus threshold is $100,000 in gross sales of tangible personal property and taxable services delivered into Colorado during the current or previous calendar year. Colorado does not use a transaction count threshold.

Do I need to register separately with Colorado cities?

Yes. Colorado has approximately 70 home rule jurisdictions that administer their own sales tax systems. You must register separately with each home rule city or county where you have customers, in addition to registering with the Colorado Department of Revenue for state sales tax.

How often do I need to file Colorado sales tax returns?

Filing frequency depends on your tax liability and varies by jurisdiction. The Colorado Department of Revenue typically assigns monthly filing for state tax initially. Each home rule jurisdiction sets its own filing frequency and deadlines, creating multiple separate filing obligations.

What happens if I exceeded the threshold but haven’t registered?

If you’ve exceeded Colorado’s economic nexus threshold but haven’t registered, register immediately and begin collecting tax. For past periods, Colorado offers a Voluntary Disclosure Agreement (VDA) program that can limit lookback periods and waive penalties. HOST can help you navigate VDAs to minimize liability.

What happens if I’m under the $100,000 threshold?

Even below $100,000, you’re not entirely off the hook. Colorado requires non-collecting retailers to provide transactional notices to customers about their use tax obligations, send annual purchase summaries by January 31, and file annual customer information reports with the Colorado Department of Revenue by March 1. These notice and reporting requirements apply to sellers under the threshold who choose not to register.

How do I know which home rule jurisdictions to register with?

You should register with every home rule jurisdiction where you have customers once you’ve established Colorado economic nexus. HOST’s nexus analysis identifies all jurisdictions where you have sales and handles registration with each one, ensuring complete compliance across Colorado’s complex tax landscape.