Colorado sales tax nexus determines whether your business must collect and remit sales tax in the state. Cross the $100,000 threshold, and you’re facing immediate obligations like registration, collection, and filing across state and local jurisdictions.

Here’s the catch: Colorado doesn’t stop at state-level requirements. Over 600 local tax jurisdictions operate with unique rates, rules, and filing demands. Add home-rule cities requiring separate registrations, and nexus becomes a multi-layered compliance maze.

Hands Off Sales Tax (HOST) specializes in exactly this. We handle Colorado sales tax nexus analysis, registration across required jurisdictions, ongoing filings, and those inevitable state notices. Understanding nexus is your foundation for staying compliant.

What Is Sales Tax Nexus in Colorado?

Sales tax nexus creates a legal obligation to collect and remit sales tax. Once established, Colorado expects you to charge correct rates, file returns, and remit collections to appropriate authorities.

Colorado recognizes two nexus types: physical and economic. Both create identical obligations once triggered.

Physical Nexus: Traditional Presence

Physical nexus exists when your business maintains tangible presence in Colorado:

- Office, warehouse, or retail location

- Inventory stored in Colorado (including third-party fulfillment centers)

- Employees working in Colorado

- Independent contractors or sales representatives operating in-state

- Attending trade shows or conventions (even one day can trigger use tax obligations)

Physical presence creates nexus immediately, regardless of sales volume. Even one remote employee working from Colorado triggers statewide obligations.

Economic Nexus: The Post-Wayfair Standard

Economic nexus triggers based on sales activity rather than physical presence. Following the 2018 South Dakota v. Wayfair Supreme Court decision, Colorado implemented economic nexus thresholds most remote sellers now navigate.

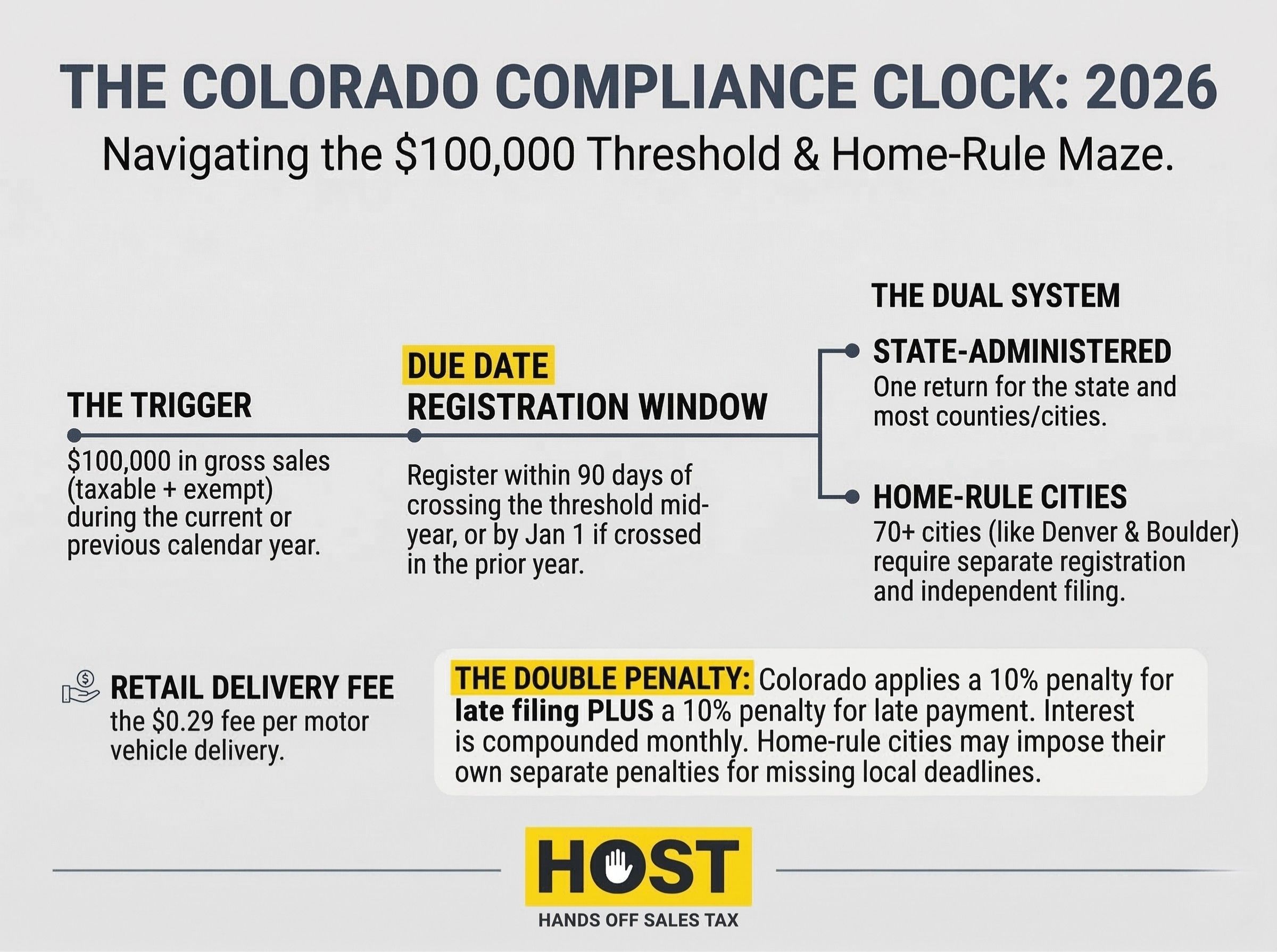

Colorado’s economic nexus threshold is $100,000 in gross sales during the current or previous calendar year. No transaction count requirement. Only the dollar threshold matters.

Critical Detail: Colorado counts gross sales, not taxable sales. Sold $80,000 in taxable products and $30,000 in exempt products to Colorado customers? You’ve crossed the threshold.

Economic nexus applies on a calendar-year basis. Exceed $100,000 in 2024, and you must register and begin collecting by the first day of the following month. Cross mid-year? You have 90 days from the date you exceed the threshold to register and begin collecting. Register by the first day of the first month starting at least 90 days after crossing.

Affiliate Nexus: The Hidden Trigger

Colorado also recognizes affiliate nexus, which is an often-overlooked path to sales tax obligations that kicks in at a lower threshold than economic nexus.

You may have affiliate nexus if you work with Colorado-based affiliates, representatives, or related entities that:

- Sell similar products under the same or similar business name

- Maintain facilities in Colorado that facilitate your sales

- Deliver, install, or service products you sell to Colorado customers

- Allow customers to pick up your products at a Colorado location

Critical difference: Affiliate nexus has a $50,000 exception. If your sales through Colorado affiliates exceeded $50,000 in the prior year, you have nexus, well below the $100,000 economic nexus threshold.

This catches businesses off guard. Affiliate marketing programs, referral partnerships, or related company operations in Colorado can trigger obligations faster than you expect.

How Colorado’s Local Jurisdictions Complicate Nexus

Unlike most states with unified systems, Colorado fragments compliance across state, county, municipal, and special district levels.

State-Administered vs. Home-Rule Cities

Colorado divides into two collection systems:

State-Administered Jurisdictions: The Colorado Department of Revenue manages tax collection for the state, most counties, and many cities. You file a single return covering all state-administered locations.

Home-Rule Cities: Approximately 70 municipalities administer their own sales tax independently. These cities require separate registration, separate filing, and separate remittance. Each operates under unique rules, deadlines, and rates.

Denver, Aurora, Colorado Springs, Boulder, Fort Collins, there are dozens of cities that function as home-rule jurisdictions. If you have nexus and sell to customers in these cities, you register with each individually and file monthly, quarterly, or annually based on their specific requirements.

The 600+ Jurisdiction Challenge

Colorado contains over 600 tax jurisdictions when combining state, county, municipal, and special district taxes. Combined rates range from 2.9% (state minimum) to over 11% in some mountain resort towns.

Calculating correct rates requires address-level precision. Two customers living three blocks apart might fall under different municipal boundaries, triggering different rates and filing obligations.

HOST manages these complex filing requirements, state-administered and home-rule, so you never miss a deadline or file with the wrong authority.

Colorado’s Retail Delivery Fee: Another Nexus Consideration

In July 2022, Colorado implemented a Retail Delivery Fee. A $0.28 charge (as of July 2025) on every delivery of tangible personal property by motor vehicle to a Colorado address. This fee applies separately from sales tax but operates under similar nexus principles.

If you have Colorado sales tax nexus (physical or economic), you likely have Retail Delivery Fee nexus. The fee applies to each delivery, not each item. A single shipment containing five products incurs one $0.28 fee.

Exemptions exist for deliveries under $500 and sales to tax-exempt entities, but tracking and applying these exemptions adds operational complexity. The fee generates revenue for road and transit improvements, with collections remitted quarterly.

When Does Nexus Start?

Economic Nexus Timing

Colorado economic nexus obligations begin when you exceed $100,000 in gross sales. The Colorado Department of Revenue expects continuous monitoring and registration once you cross the threshold.

Example: You started selling to Colorado customers in March 2024. By September, cumulative gross sales reached $105,000. You must register by the first day of the first month commencing at least 90 days after crossing, so December 1 if you crossed on September 1.

If you exceed the threshold in the prior calendar year, you must register and begin collecting by January 1 of the current year.

What If You Don’t Collect? Use Tax Notification Requirements

Not ready to register or below the threshold but making substantial Colorado sales? You’re not off the hook completely.

Colorado requires non-collecting retailers with $100,000+ in annual Colorado sales to comply with use tax notification requirements:

- Transactional Notice: Inform customers at purchase that use tax is due

- Annual Purchase Summary: Provide customers who spent $500+ with a yearly purchase summary by January 31

- Annual Customer Report: File customer information with the Colorado Department of Revenue by March 1

These requirements apply even if you haven’t established nexus. While enforcement has been inconsistent, the law remains on the books. Most businesses find collecting sales tax simpler than managing these notification obligations.

Retroactive Nexus Risk

Failing to register once nexus exists creates retroactive liability. Colorado can assess back taxes, penalties, and interest for prior periods when you had nexus but weren’t collecting.

Voluntary Disclosure Agreements (VDAs) limit lookback periods and potentially abate penalties. HOST files VDAs on behalf of businesses discovering past nexus, resolving liabilities while minimizing financial impact.

Colorado Registration Process: State and Home-Rule

State Registration

Colorado registration occurs through the Revenue Online portal. You’ll need your FEIN or SSN, business structure details, Colorado Revenue Account Number (if applicable), bank account information, and estimated monthly sales volume.

Cost: In-state businesses pay a $16 application fee plus $50 deposit. Out-of-state remote sellers register free.

The state issues a Sales Tax License number, typically within 7-10 business days.

Home-Rule City Registrations

Each home-rule city operates independently. Denver registration happens through the Denver Treasury Division. Aurora uses its own portal. Colorado Springs requires paper applications.

Some cities issue immediate licenses; others take 2-4 weeks. Missing registration in a home-rule city where you have nexus creates separate liability from state obligations.

HOST handles all Colorado registrations, state and every applicable home-rule city, eliminating paperwork burden and ensuring nothing slips through.

Colorado Filing Requirements and Frequencies

State-Administered Jurisdiction Filing

Colorado assigns filing frequency based on monthly tax liability:

- Monthly Filing: Average monthly liability exceeds $300

- Quarterly Filing: Average monthly liability is $15-$300

- Annual Filing: Average monthly liability is under $15

Most e-commerce businesses with Colorado economic nexus file monthly due to crossing the $100,000 threshold. Returns are due the 20th of the month following the reporting period.

Common Filing Mistakes

Incorrect Jurisdiction Allocation: Assigning sales to the wrong city or county creates underpayment in one jurisdiction and overpayment in another.

Missing Home-Rule Cities: Many businesses register with the state but overlook home-rule cities, creating unfiled liability.

Failing to File Zero Returns: Even months with no Colorado sales require zero returns in many jurisdictions.

HOST prepares and files all Colorado returns! State-administered and home-rule, ensuring accurate jurisdiction allocation, timely submission, and proper zero-return handling.

Exemptions and Special Circumstances

Marketplace Facilitator Laws

Colorado’s marketplace facilitator law requires platforms like Amazon, eBay, and Etsy to collect and remit sales tax on behalf of third-party sellers.

Critical Exception: Marketplace facilitators don’t handle home-rule city tax for third-party sellers in many cases. You may still need to register and file with home-rule cities even when Amazon collects state tax.

This creates a compliance gap many sellers miss. HOST analyzes your sales channels to determine which jurisdictions you must handle independently.

What Happens If You Ignore Colorado Nexus?

Audit Risk

Colorado actively pursues remote sellers with unreported nexus. The Department of Revenue uses data-matching from marketplace platforms, credit card processors, and interstate compacts to identify businesses exceeding thresholds.

Once Colorado initiates an audit, they examine 3-4 years of sales history, assess back taxes on all taxable sales, and add penalties and interest.

Penalties and Interest

Colorado penalties include late filing penalty (10% of tax due), late payment penalty (10% of unpaid tax), compounded monthly interest, and negligence penalty (additional 25% for willful non-compliance).

A $10,000 tax liability can become $15,000+ after penalties and interest compound over multiple years.

Notice Management

Colorado sends notices for various triggers: missing returns, discrepancies between reported and actual sales, registration requirements. These notices often confuse recipients with unclear language and tight response deadlines.

HOST interprets Colorado notices, determines actual issues, and responds appropriately, protecting you from penalties while resolving legitimate concerns.

HOST: Your Colorado Nexus Compliance Partner

Colorado sales tax nexus creates obligations across state, county, municipal, and special district levels. Managing 600+ jurisdictions, home-rule city registrations, varying deadlines, and complex rate calculations diverts focus from growth.

What HOST Delivers:

Nexus Analysis: We analyze your Colorado sales data and business footprint to determine exactly where you have obligations: state-administered, home-rule cities, and special districts.

Complete Registration: We handle state registration and every applicable home-rule city, managing paperwork, follow-up, and communications.

Multi-Jurisdiction Filing: We prepare and file returns across all Colorado jurisdictions monthly, quarterly, or annually based on each jurisdiction’s requirements.

Notice Resolution: We interpret Colorado notices (state and local), determine required actions, and respond to protect you from penalties.

Audit Defense: We organize documentation, communicate with auditors, and work to minimize liability if Colorado initiates an audit.

Software Review: We audit your sales tax automation configuration to ensure correct Colorado rate calculation and jurisdiction allocation.

We’ve focused exclusively on sales tax since 1999. That’s over 25 years helping businesses navigate compliance. Through our parent company TaxMatrix, we’ve served North America’s largest companies. Now we bring that expertise to e-commerce sellers managing Colorado’s complex requirements.

Ready to Handle Colorado Nexus Correctly?

Colorado sales tax nexus is an ongoing obligation requiring monitoring, registration, collection, filing, and response to state communications. Every month you operate without proper compliance increases audit risk and potential liability.

Whether you’ve just crossed the $100,000 threshold, discovered physical nexus through fulfillment centers, or want to ensure your current Colorado compliance is accurate, professional guidance eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss your Colorado nexus situation or schedule a free consultation. Let us handle the multi-jurisdiction complexity so you can focus on growing your business.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the Colorado sales tax nexus threshold for remote sellers?

Colorado’s economic nexus threshold is $100,000 in gross sales (taxable and exempt combined) during the current or previous calendar year. No transaction count requirement—only the dollar threshold matters.

Do I need to register with every Colorado city individually?

You must register with the Colorado Department of Revenue for state-administered jurisdictions. Additionally, you must register separately with each home-rule city where you have nexus, approximately 70 cities including Denver, Aurora, Colorado Springs, and Boulder.

When should I start collecting Colorado sales tax after crossing the nexus threshold?

You must register and begin collecting once you exceed $100,000 in gross sales. The obligation starts immediately after crossing the threshold. Colorado provides no grace period.

Does Colorado’s Retail Delivery Fee apply to all shipments?

The $0.28 Retail Delivery Fee (as of July 2025) applies to deliveries of tangible personal property by motor vehicle to Colorado addresses when the sale is $500 or more. One fee per delivery, regardless of item count. If you have Colorado sales tax nexus, you likely have Retail Delivery Fee nexus.

What happens if I discover I should have been collecting Colorado sales tax for past years?

Colorado can assess back taxes for prior periods when you had nexus but weren’t collecting. A Voluntary Disclosure Agreement (VDA) can limit the lookback period and potentially abate penalties. HOST files VDAs to resolve past liabilities while minimizing financial impact.