California sales tax nexus determines whether your business must collect and remit sales tax in the state. For remote sellers shipping into California, understanding nexus is the difference between compliance and costly audits.

California’s base rate hits 7.25%, but local districts push combined rates to 10.25% in some areas. Add economic nexus thresholds, marketplace facilitator rules, and aggressive enforcement, and you’ve got a compliance landscape that punishes mistakes hard.

That’s where Hands Off Sales Tax (HOST) steps in. We analyze your California footprint, determine precise nexus obligations, handle registrations, and manage ongoing filings. From nexus analysis to automated monthly returns, we’ve navigated California’s requirements for over 25 years, so you don’t have to.

What Is Sales Tax Nexus in California?

Nexus is your connection to California that creates a tax collection obligation. Once it exists, you register with the California Department of Tax and Fee Administration (CDTFA), collect the appropriate tax on California sales, and file returns on schedule.

California recognizes two nexus types that both trigger full obligations: physical presence and economic activity.

Physical Presence Nexus

Physical presence nexus exists when your business maintains any tangible California connection:

- Office, warehouse, or retail location

- Inventory in California fulfillment centers (including Amazon FBA)

- Employees, contractors, or sales representatives working in-state

- Temporary presence at trade shows, pop-ups, or events exceeding 15 days annually or generating $100,000+ in revenue during the preceding calendar year

- Property or equipment located in California

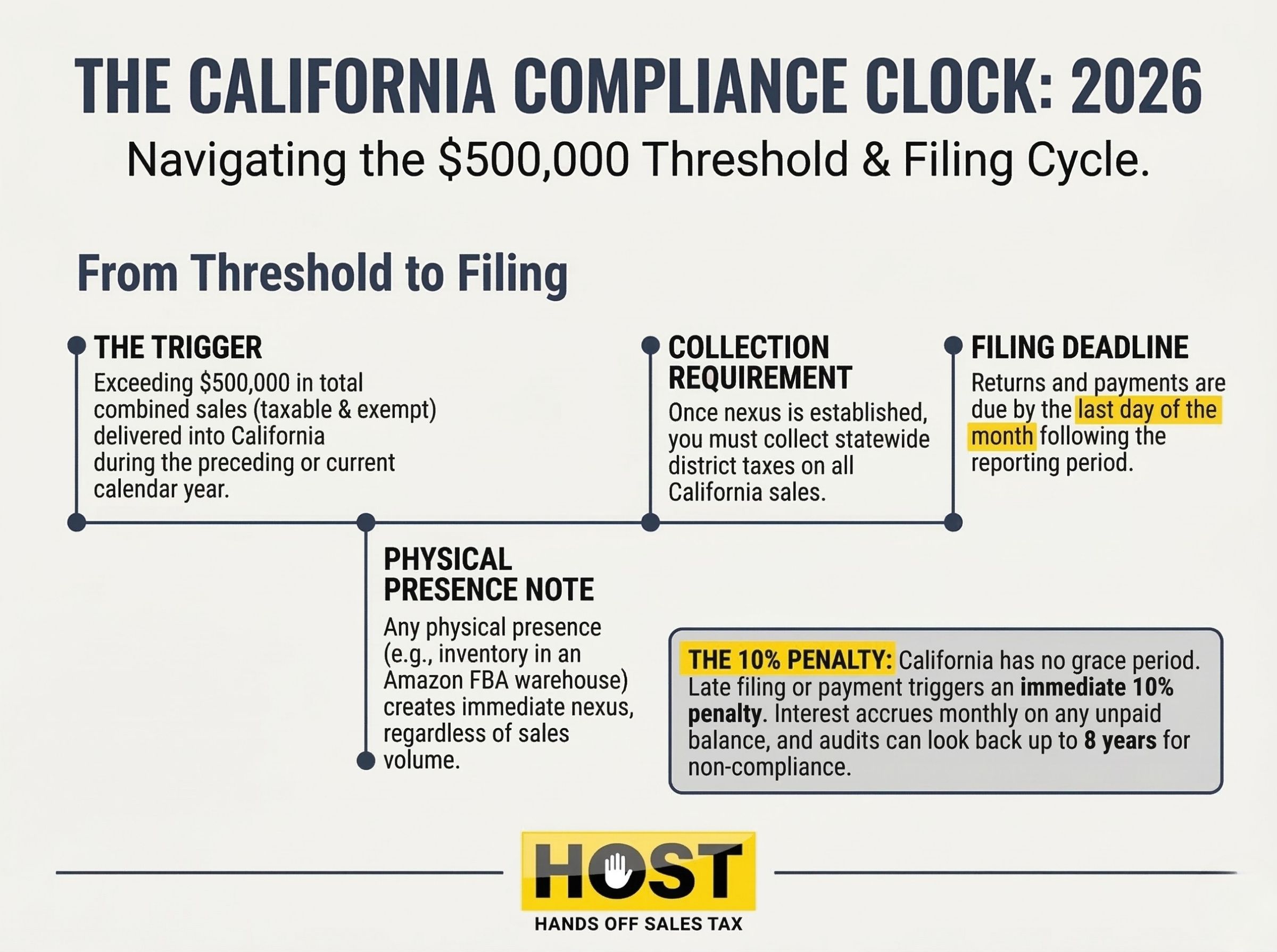

Physical presence creates immediate nexus regardless of sales volume. A single employee working remotely from San Diego? That’s nexus.

Important: Trailing nexus means obligations continue even after you cease California activities. Your nexus typically extends through the quarter you stop operations plus the following quarter.

Economic Nexus

California’s economic nexus law requires out-of-state sellers to collect use tax (the complement to sales tax for remote transactions) once they exceed $500,000 in total combined sales of tangible personal property delivered into California during the preceding or current calendar year.

Key details:

- $500,000 threshold applies to total sales, not just taxable sales

- Includes wholesale and resale transactions (even if tax-exempt)

- No transaction count requirement (unlike many states)

- Includes all California sales from the preceding 12 months

- Marketplace sales count toward the threshold

- Non-taxable and exempt sales count toward the threshold

California implemented economic nexus on April 1, 2019, following the South Dakota v. Wayfair decision that fundamentally changed obligations for e-commerce sellers nationwide.

How to Determine If You Have Nexus

Evaluate Physical Connections

Review your California footprint. Inventory at Amazon fulfillment centers in California? Employees living in-state? Trade show attendance exceeding 15 days annually?

Any physical presence, no matter how minimal, creates nexus. Remote work arrangements complicate this. An employee working from home in Sacramento creates nexus even if your headquarters sits in Austin.

Calculate Your California Sales

Pull sales data for the current calendar year and preceding calendar year. Total all sales (taxable and exempt) delivered to California customers.

If your combined total exceeds $500,000, you’ve met economic nexus. California’s threshold is straightforward compared to other states, but monitoring requires consistent tracking.

Account for Marketplace Facilitator Sales

California’s marketplace facilitator law requires platforms like Amazon, eBay, Etsy, and Walmart to collect sales tax on behalf of third-party sellers. When the marketplace collects, you’re relieved of collection obligation for those transactions.

However, sales through facilitator marketplaces still count toward your $500,000 threshold for direct sales channels. If you sell through Amazon (marketplace collects) and your own website (you collect), total California sales through both channels determine whether you have nexus for direct sales.

What Happens Once You Have Nexus

Registration Requirements

Once nexus exists, you must register with the CDTFA for a seller’s permit. Registration is free but mandatory. Operating without a permit when nexus exists subjects you to penalties and back tax assessments. Note that the CDTFA may require a security deposit based on estimated tax liability or prior tax history.

The CDTFA assigns filing frequency based on estimated tax liability: monthly, quarterly, or annually. Most new registrants start quarterly, with frequency adjusted based on actual collections.

HOST handles all sales tax registration requirements, completing paperwork, following up with the CDTFA, and ensuring your permit is active before you begin collecting.

Collection Obligations

You must collect sales tax on all taxable California sales. California’s base rate is 7.25%, but local district taxes add up to 3%, creating combined rates from 7.25% to 10.25% depending on customer location.

Tax rate sourcing: Out-of-state sellers and multi-location California retailers use destination-based sourcing (charge tax based on customer location). Single-location California retailers use origin-based sourcing (charge tax based on their business location).

Critical district tax rule: If you have economic nexus, you must collect district taxes on ALL California sales—not just in districts where you individually meet thresholds. This is statewide, not district-by-district.

Calculating the correct rate requires address-level validation. A customer in Los Angeles might pay different rates depending on their specific neighborhood. Manual calculation isn’t scalable, so most businesses use automation software like TaxJar or Avalara. The CDTFA provides a “Find a Sales and Use Tax Rate by Address” tool for rate lookup.

Common exemptions: While most tangible personal property is taxable, California exempts groceries (unprepared food), prescription medications, and certain medical devices from sales tax.

Software configuration matters enormously. Common mistakes include treating exempt items as taxable, applying wrong local rates, or double-taxing due to system overlaps. HOST offers a Free Sales Tax Software Review to identify costly errors before they become audit problems.

Filing and Remittance

California requires returns filed by the last day of the month following the reporting period. Late filing triggers immediate penalties: 10% of tax due right away, plus an additional 10% if more than 30 days late. Interest accrues monthly on unpaid balances.

HOST manages all sales tax filing obligations across California’s complex reporting requirements, ensuring returns are filed accurately and on time every period.

California’s Aggressive Enforcement

California actively pursues remote sellers. The CDTFA uses data-matching technology, monitors marketplace sales, and conducts regular compliance audits. With budget pressures mounting, California has intensified enforcement dramatically.

Common audit triggers:

- Sudden registration after years of California sales

- Inconsistent reporting between state and federal returns

- Marketplace sales data provided by facilitators

- Industry-specific sweeps targeting high-volume sectors

Audits look back 3 years, or up to 8 years if fraud or willful non-compliance is suspected. Penalties include 10% negligence penalties, 40% fraud penalties, plus interest compounding monthly.

HOST’s audit defense services provide expert representation during CDTFA audits, organizing documentation, preparing responses, and negotiating outcomes to minimize liability.

Voluntary Disclosure: Limiting Past Exposure

If you discover years of California nexus without collecting, a Voluntary Disclosure Agreement (VDA) can limit exposure. California’s VDA program allows businesses to come forward voluntarily, limiting the lookback period to 3 years and potentially abating penalties.

Timing is critical. Once the CDTFA contacts you about non-compliance, VDA eligibility disappears. HOST manages the VDA process from initial contact through negotiation, settlement, and registration.

HOST: Your California Compliance Partner

California sales tax compliance creates operational burden that diverts focus from growth. Manual compliance across thousands of jurisdictions isn’t scalable.

What HOST Delivers:

- Nexus Analysis: We analyze your sales data and California footprint to determine precise nexus status

- Sales Tax Registration: We handle CDTFA registration, following up on all correspondence until your permit is active

- Automated Filing: We prepare and file all California returns. State, local, and district, on schedule, every period

- Software Optimization: We review your automation setup to prevent costly configuration errors

- Notice Management: We interpret and respond to CDTFA notices, protecting you from penalties

- Audit Defense: We provide expert representation during California audits

- VDA Support: We file voluntary disclosure agreements to limit lookback periods

We’ve been 100% focused on sales tax since 1999. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

Ready to Get California Compliant?

California nexus obligations don’t wait. Whether you’re crossing the $500,000 threshold for the first time, discovering years of past exposure, or managing ongoing compliance across multiple states, the right partner ensures you collect correctly, file on time, and minimize audit risk.

Contact us today to discuss your California nexus situation or schedule a free consultation. You handle the sales, we handle the tax.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the economic nexus threshold for California sales tax?

California’s economic nexus threshold is $500,000 in total combined sales of tangible personal property delivered into California during the preceding or current calendar year. There’s no transaction count requirement.

Do I have California nexus if I use Amazon FBA?

Yes. Inventory stored in California fulfillment centers creates physical presence nexus regardless of sales volume. Amazon’s marketplace facilitator collection doesn’t eliminate your nexus, it just shifts collection responsibility for marketplace sales to Amazon.

How far back can California audit my sales tax?

California typically audits the prior 3 years of returns. However, if the CDTFA suspects willful evasion or fraud, the lookback period extends to 8 years. Unfiled years remain open indefinitely.

What happens if I don’t register when I have California nexus?

Operating without registration when nexus exists subjects you to back tax assessments, 10-40% penalties depending on circumstances, monthly compounding interest, and potential criminal charges in extreme cases. California actively pursues non-compliant remote sellers.

Can I use a Voluntary Disclosure Agreement if California contacts me first?

No. VDA eligibility ends once the CDTFA initiates contact regarding your non-compliance. VDAs only work when you come forward voluntarily before the state discovers the issue.

How do I calculate the correct California sales tax rate?

California sales tax combines the 7.25% state base rate with local district taxes that vary by customer location. Combined rates range from 7.25% to 10.25%. Most businesses use sales tax automation software with address-level validation to calculate correctly.