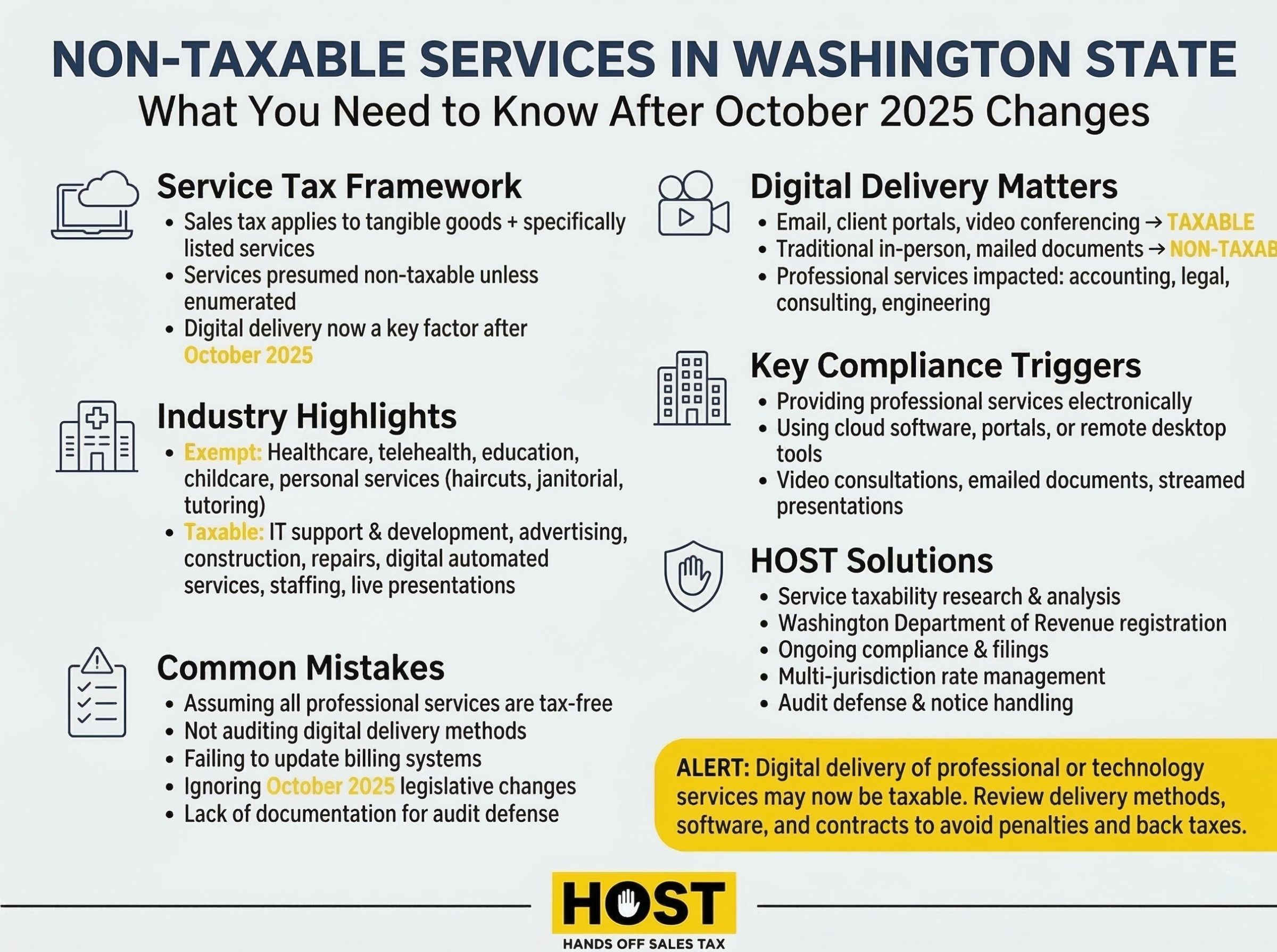

What services are not taxable in Washington State? For businesses operating here, understanding which services escape the 6.5% state sales tax matters, especially after October 2025’s sweeping changes that caught thousands of service providers off guard.

Washington historically exempted most professional services from retail sales tax. Then Senate Bill 5814 flipped the script. Now, how you deliver a service determines whether you charge tax, not just what the service is. A tax return emailed through a client portal? Taxable. The same return printed and mailed? Not taxable.

That’s where Hands Off Sales Tax (HOST) cuts through the confusion. With over 25 years managing compliance across all states, we help businesses navigate Washington’s tangled service taxation rules. No guesswork, no surprises.

Understanding Washington’s Service Tax Framework

Washington operates under dual taxation: Business & Occupation (B&O) tax hits gross receipts, while retail sales tax applies only to tangible goods and specifically enumerated services.

Here’s the twist: services are presumed non-taxable unless explicitly listed as taxable. That consultant who streams video presentations? Likely taxable. The one presenting in conference rooms? Still exempt.

Combined state and local rates range from 7% to 10.5%, with Seattle reaching 10.4%. Washington collected over $11 billion in retail sales tax in fiscal 2023. 47% of General Fund revenue. Misclassification triggers audits, back taxes, penalties, and interest.

Quick Reference: Service Taxability by Industry

| Service Category | Generally Taxable? | Key Exceptions & Notes |

| Accounting (traditional) | ❌ No | ✅ YES if delivered via portal/email |

| Legal (in-person) | ❌ No | ✅ YES if via Zoom/online delivery |

| IT Support & Development | ✅ YES | No exceptions (New Oct 2025) |

| Consulting (traditional) | ❌ No | ✅ YES if via video conference |

| Healthcare & Medical | ❌ No | Telehealth specifically protected |

| Real Estate Services | ❌ No | No exceptions |

| Advertising (all types) | ✅ YES | No exceptions (New Oct 2025) |

| Repairs (vehicles, appliances) | ✅ YES | Labor and parts both taxable |

| Construction Services | ✅ YES | No exceptions |

Real-World Scenarios: How Digital Delivery Changes Everything

The CPA’s Dilemma: Sarah prepares identical tax returns for two clients. Client A receives returns via client portal → TAXABLE. Client B receives printed returns by mail → NOT TAXABLE. Same service, different tax treatment based purely on delivery.

The Consultant’s Choice: Marcus provides business strategy consulting. In-person presentation with printed materials → NOT TAXABLE. Zoom presentation with emailed PDF → TAXABLE.

Healthcare’s Protection: Dr. Chen’s telehealth therapy → NOT TAXABLE (specifically excluded). Lisa’s online life coaching → TAXABLE (not healthcare).

The Bookkeeper’s Problem: Working on-site using client’s desktop software → NOT TAXABLE. Working remotely via QuickBooks Online → TAXABLE.

Professional Services: The Digital Delivery Dilemma

Effective October 1, 2025, Washington expanded sales tax to capture services delivered electronically. Traditional in-person consultations remain exempt. Electronic delivery via email, portals, or video conferencing? Potentially taxable under “digital automated services” rules.

Legal Services

Traditional attorney fees, courtroom representation, and document preparation remain non-taxable when delivered conventionally. But legal consultations via Zoom or documents delivered through online portals may now trigger sales tax.

Accounting and Bookkeeping

CPAs providing in-person consultations or mailing physical documents stay sales-tax-free. The October 2025 earthquake: tax returns delivered via portals, bookkeeping through QuickBooks Online, services via remote desktop all may now face retail sales tax as digital automated services.

Consulting Services

Management consulting and professional advisory services provided in-person remain non-taxable. October 2025 changed everything: consulting delivered via video conferences, research emailed to clients, presentations streamed online all trigger digital automated service classification.

Engineering, Architecture, and Real Estate

Professional engineering, architectural, real estate agent, and insurance broker services remain exempt when delivered traditionally. Digital delivery complicates this, and electronic plan delivery and online collaboration tools may create taxability issues.

Healthcare and Educational Services: Still Exempt

Washington exempts healthcare services from retail sales tax. Physician consultations, surgeries, dental treatments, mental health services, physical therapy are all non-taxable. Telehealth and telemedicine services remain specifically excluded from digital automated services taxation.

Private tutoring, test prep, professional development training, and educational instruction remain non-taxable when focused on instruction rather than materials.

Personal Services That Escape Taxation

Childcare, daycare, preschool, residential cleaning, janitorial services are examples of being non-taxable as pure service transactions. Haircuts, styling, coloring are all barbering and cosmetology services avoid sales tax. Products sold separately face taxation.

Which Services ARE Taxable?

Construction involving real property, hotel stays, telecommunications, utilities are all taxable. Repairing tangible personal property (vehicles, appliances, electronics) triggers sales tax on labor and parts. Gym memberships, personal training, fitness classes, any recreational service is taxable.

Technology and Business Services (NEW – October 2025)

Senate Bill 5814 fundamentally altered Washington’s tax landscape:

- IT Services: Support, custom website development, software customization are all taxable

- Advertising: All services including creation, production, dissemination

- Temporary Staffing: Employment placement (excluding hospitals)

- Live Presentations: Lectures, seminars, workshops—taxable whether in-person or online

- Security Services: Investigation, monitoring, armored car services

- Digital Automated Services: Services delivered electronically using software

Am I Affected by October 2025 Changes?

Do you deliver services electronically? (email, portals, video, cloud software)

- NO → You’re likely unaffected

- YES → Continue…

Are you a licensed healthcare provider delivering telehealth?

- YES → You’re protected

- NO → Continue…

Do you provide professional services? (accounting, legal, consulting, engineering)

- YES → HIGH RISK – Your digital delivery may now be taxable. Get expert review immediately.

- NO → Check if you provide newly taxable services: IT support, advertising, staffing, live presentations, or security services.

Common Compliance Mistakes

Red Flags You’re Collecting Wrong:

- ❌ Using cloud software to serve clients

- ❌ Delivering documents via portals or email

- ❌ Conducting consultations exclusively via video

- ❌ Haven’t reviewed delivery methods since October 2025

- ❌ Assuming “professional services are always exempt”

Immediate Action Steps:

- Audit service delivery methods (digital vs. traditional)

- Review client contracts for tax treatment

- Consult sales tax expert about your situation

- Update billing systems for conditional tax collection

- Document taxability analysis for audit defense

How HOST Simplifies Washington Service Tax Compliance

What HOST Delivers:

- Nexus Analysis: Determine whether your business triggered Washington obligations

- Taxability Research: Analyze your services against Washington’s tax code

- Sales Tax Registration: Handle Department of Revenue registration and paperwork

- Ongoing Compliance: File returns monthly, quarterly, or annually

- Multi-Jurisdiction Management: Ensure correct rates across dozens of local jurisdictions

- Audit Defense: Partner resolving audits and defending your position

We’ve been 100% focused on sales tax since 1999. That’s over 25 years navigating compliance across all states including Washington’s unique landscape.

Tools & Resources

Official Washington Resources:

Industry-Specific Guidance:

Healthcare: Services remain protected including telehealth. Focus on B&O tax compliance.

Technology/IT: Virtually all services became taxable October 2025. IT support, development, website services all require sales tax collection.

Professional Services: Tax obligations hinge on delivery method. Traditional in-person remains exempt. Electronic delivery may trigger taxation.

Advertising/Marketing: All services became taxable October 2025. Digital and traditional formats face sales tax.

Ready to Eliminate Washington Sales Tax Guesswork?

Washington’s service taxation demands precision. Digital delivery rules blindside businesses daily. Whether you’re a professional service provider navigating digital delivery, an e-commerce business offering services, or a multi-state operation managing compliance, the right partner ensures accuracy.

At HOST, we combine deep technical expertise with 25+ years of specialized experience, transparent communication, and personalized support.

Contact HOST today to discuss your Washington compliance needs.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Are consulting services taxable in Washington State?

Consulting services delivered in-person or through traditional methods remain exempt. However, consulting delivered via video conferencing, email, or online platforms may now be taxable as digital automated services under rules effective October 1, 2025.

Do I charge sales tax on professional services in Washington?

Most professional services such as legal, accounting, engineering, or architecture remain non-taxable when delivered conventionally. Services delivered electronically through portals, video conferencing, or cloud software may now face taxation. Construction, repairs, and installations are taxable.

What is the difference between B&O tax and sales tax in Washington?

B&O (Business & Occupation) tax applies to gross receipts which is the business’ responsibility. Sales tax applies to retail sales of tangible goods and specific services, collected from customers. Businesses providing exempt services still owe B&O tax but don’t collect sales tax.

Are repair services taxable in Washington State?

Yes. Services that repair, maintain, or improve tangible personal property like vehicles, appliances, electronics, and furniture are taxable. Both labor and parts face sales tax. This differs from professional services which remain exempt.

How do I know if my service requires Washington sales tax collection?

Washington exempts most professional and personal services unless specifically enumerated as taxable; however, October 2025 changes added many technology and digitally-delivered services. HOST provides taxability research determining exactly which transactions require collection.

Are healthcare services subject to sales tax in Washington?

No. Medical services, dental care, mental health treatment, physical therapy, and healthcare services by licensed professionals remain exempt. Telehealth and telemedicine services are specifically excluded from digital automated services taxation.