Do manufacturers pay sales tax? It depends on what you’re buying and where you operate. Most states recognize that taxing manufacturing inputs creates an unfair cascade effect—what economists call “tax pyramiding.” So they’ve carved out exemptions.

But here’s the catch: exemptions vary wildly by state. What’s exempt in Texas might be taxable in Pennsylvania. And without proper documentation, those exemptions disappear faster than inventory in Q4.

Understanding these rules isn’t just compliance theater, it’s about protecting margins. Overpaying sales tax on exempt purchases bleeds profit. Failing to document exemptions properly invites audits and penalties.

Hands Off Sales Tax (HOST) specializes in helping manufacturers navigate sales tax obligations across all 45+ states with sales tax. From exemption certificate management to multi-state compliance, we handle the details so you can focus on production.

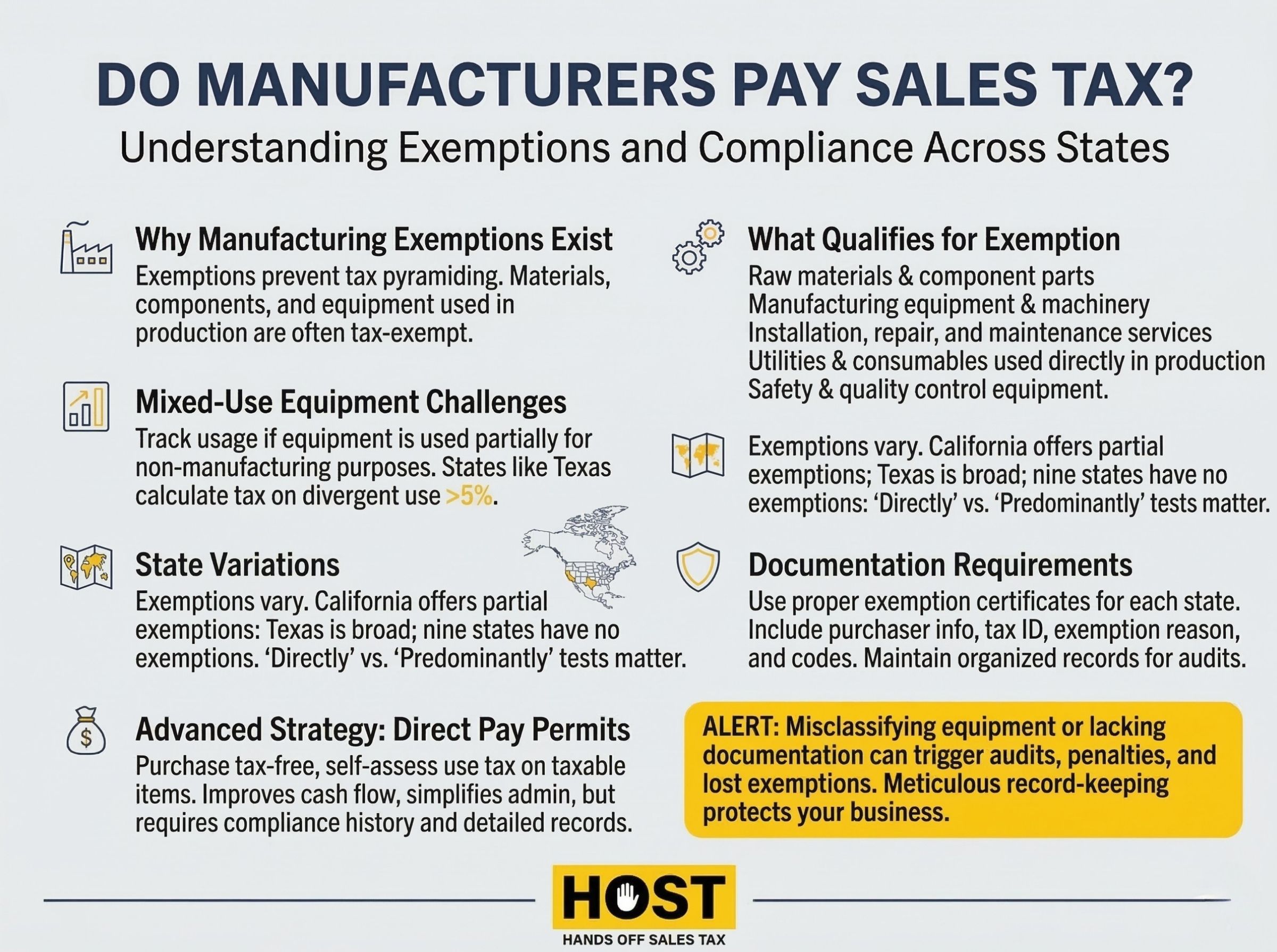

Why Manufacturing Exemptions Exist

Sales tax is a consumption tax charged on retail transactions. Manufacturing isn’t retail is an intermediate step in the supply chain.

The principle is straightforward: items consumed or incorporated into products for resale shouldn’t face sales tax. This includes raw materials, component parts, and in many cases, manufacturing equipment. Without exemptions, products would be taxed repeatedly as they move through production, tax pyramiding that inflates consumer prices and disadvantages manufacturers.

States define “manufacturing” differently, though. Some apply broad definitions covering any transformation of materials. Others require substantial alteration.

Unexpected Industries That Qualify

Many businesses don’t realize they qualify as manufacturers for exemption purposes:

Restaurants and food service operations qualify in Texas: ovens, mixers, and food preparation equipment can be purchased exempt. Bakeries in grocery stores and caterers fall under the same umbrella.

Printers are considered manufacturers in Florida, making their production equipment eligible for exemptions.

Biotechnology operations qualify in Maine when using biological processes as part of integrated manufacturing.

If your business transforms materials into products for sale, you might qualify for manufacturing exemptions even in non-traditional industries.

What Typically Qualifies for Exemption

Raw Materials and Component Parts: Materials that become physical components of finished products are almost universally exempt. Steel purchased to manufacture machinery, fabric used in clothing production, or ingredients in food manufacturing typically qualify as purchases for resale in altered form.

Manufacturing Equipment and Machinery: Many states exempt equipment used directly in manufacturing—production line machinery, industrial robots, conveyor systems, and specialized manufacturing tools.

The “directly used” requirement creates gray areas. Equipment that touches the product or controls production processes usually qualifies. Equipment in ancillary roles like office furniture or break room appliances, typically doesn’t.

Services on Manufacturing Equipment: Installation, repair, maintenance, and cleaning services for exempt equipment often qualify for exemption too. Installing plumbing or electrical systems for production equipment, repairing assembly line machinery, or cleaning production areas can all be purchased tax-free. However, cleaning supplies for administrative offices remain taxable.

Utilities and Consumables: Some states exempt electricity, natural gas, or water consumed directly in manufacturing processes. Industrial consumables like lubricants, coolants, and chemicals used to prevent equipment failure may qualify, though documentation requirements are stringent.

Safety Equipment: Protective clothing and safety apparel required for the manufacturing process (if not resold to employees) can be purchased exempt in many states.

Quality Control and Testing: Equipment used to test, inspect, or verify products during production typically qualifies for exemption.

Mixed-Use Equipment: The Hidden Complexity

One of the trickiest scenarios manufacturers face is divergent use. When exempt equipment serves both manufacturing and non-manufacturing purposes.

Say you purchase a camera for photographing products in production (exempt). Later, you use that same camera for marketing photos (taxable use). Most states require you to track and self-assess tax on the non-exempt usage.

Texas uses a formula: If divergent use during any month exceeds 5% of total use, you owe tax calculated as 1/48 of the purchase price × percent divergent use × original tax rate. Below 5%, no tax is due. After four years, divergent use becomes tax-free.

Mixed-use inventory creates similar headaches. Purchase materials in bulk under exemption for manufacturing, then pull some for facility repairs or other non-production purposes? That inventory’s exempt status gets questioned.

The solution: meticulous documentation tracking how and when purchased materials and equipment are used. Without it, states can disallow exemptions entirely during audits.

State-by-State Exemption Variations

California provides a partial exemption (3.9375% reduction) for manufacturing equipment rather than full exemption. The relief applies only to state tax, not local taxes.

Texas offers one of the broadest exemption programs, covering machinery, equipment, raw materials, repair parts, utilities powering exempt equipment, and even gases used to prevent contamination.

New York requires equipment to be used “directly and predominantly” in manufacturing, meeting both tests is mandatory.

Nine states don’t exempt manufacturing equipment at all: Alabama, Hawaii, Kentucky, Mississippi, Nevada, New Mexico, North Dakota, South Dakota, and DC. Manufacturers in these states face competitive disadvantages.

Understanding “predominantly” vs. “directly” tests matters. “Predominantly” typically means more than 50% use in manufacturing. “Directly” means the equipment must touch the product, control production, or handle materials during the manufacturing process.

For manufacturers operating across multiple states, HOST’s nexus analysis and registration services ensure you’re claiming appropriate exemptions while maintaining proper documentation.

Exemption Certificates: Your Documentation Shield

Claiming manufacturing exemptions requires proper documentation, exemption certificates provided to vendors before purchase.

Each state prescribes specific certificate formats. Multi-state manufacturers need certificates for each state where they purchase exempt items. Using the wrong state’s certificate or outdated forms creates compliance gaps.

Certificates must include purchaser information, sales tax registration number, exemption reason, and often specific exemption codes. Generic certificates won’t work.

Common mistakes include using blanket certificates without specifying exemption reasons, failing to provide certificates before transactions (requiring refund claims later), and not maintaining organized certificate records for audits.

HOST offers comprehensive exemption certificate management, ensuring you have current, state-appropriate certificates for all jurisdictions.

Direct Pay Permits: Advanced Strategy

Some states offer direct pay permits allowing qualified manufacturers to purchase items tax-free, then self-assess and remit use tax only on taxable purchases.

Benefits include:

- Simplified purchasing without upfront tax payments

- Cash flow improvements by retaining working capital longer

- Administrative efficiency through internal exemption determinations

States typically require manufacturers to demonstrate substantial compliance history and sophisticated tax management capabilities. Applications involve financial reviews and compliance audits.

Once approved, manufacturers must maintain detailed purchase records, properly classify transactions, and accurately report use tax. Misuse can result in permit revocation and penalties.

Common Compliance Challenges

Gray areas abound: Is that computer controlling production equipment (exempt) or managing inventory (taxable)? State auditors scrutinize these classifications.

Multi-state complexity multiplies fast: A component manufactured in Tennessee, assembled in Georgia, and shipped from North Carolina creates nexus in three states with different exemption rules.

Drop shipping complications: When shipping directly to distributors versus end customers, different exemption documentation applies. Central inventory shared between plants triggers use tax tracking requirements.

Use tax exposure: Manufacturers often have greater use tax obligations than sales tax. Consumables purchased from out-of-state vendors without tax collection require use tax self-assessment and remittance.

State auditors examine manufacturing exemptions closely because they represent significant revenue. Without proper documentation and classification, manufacturers face substantial assessments for past periods.

How HOST Helps Manufacturers Stay Compliant

Manufacturing sales tax compliance demands specialized expertise. HOST provides comprehensive solutions tailored to manufacturers operating across multiple states.

Nexus Analysis: We determine exactly where your manufacturing activities create sales tax obligations.

Exemption Certificate Management: We maintain current, state-appropriate exemption certificates for all jurisdictions where you purchase materials or equipment.

Multi-State Registration: We handle registrations, paperwork, follow-ups, and state communications.

Audit Defense: When states examine your exemptions, we organize documentation, prepare responses, and defend your positions.

We’ve focused exclusively on sales tax for over 25 years, helping manufacturers navigate multi-state compliance complexities.

Protect Your Operations From Tax Surprises

Manufacturing exemptions can save thousands or millions annually. But claiming exemptions without proper documentation or misunderstanding state rules exposes you to audits, penalties, and unexpected liabilities.

Whether you’re purchasing raw materials in multiple states, investing in new production equipment, or expanding operations across state lines, understanding exemption rules protects your investment.

Contact HOST today to discuss your manufacturing operations and discover how we handle the complexity so you can focus on production.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book. Many principles apply to manufacturers too.

Frequently Asked Questions

Do manufacturers pay sales tax on raw materials?

Generally no. Most states exempt raw materials purchased for incorporation into products for resale. You must provide proper exemption certificates documenting that purchases qualify for manufacturing exemption.

Is manufacturing equipment exempt from sales tax?

In most states, yes. With variations. Many states exempt machinery used “directly” or “predominantly” in manufacturing. Nine states (Alabama, Hawaii, Kentucky, Mississippi, Nevada, New Mexico, North Dakota, South Dakota, and DC) don’t exempt manufacturing equipment at all.

What documentation do manufacturers need to claim exemptions?

Valid exemption certificates for each state where you purchase exempt items. Certificates must be provided to vendors before purchase and maintained in organized records. States may also require detailed purchase records documenting how items qualify.

How does mixed-use equipment affect exemptions?

When equipment serves both manufacturing and non-manufacturing purposes, most states require tracking usage percentages and self-assessing tax on non-exempt use. Texas applies tax when divergent use exceeds 5% monthly, using specific formulas to calculate liability.

Can installation and repair services be purchased tax-free?

Often yes. Services performed on exempt manufacturing equipment including installation, repair, maintenance, and certain cleaning services, typically qualify for exemption when the underlying equipment is exempt.

How do manufacturing exemptions work across multiple states?

Each state maintains its own rules, definitions, and certificate requirements. Multi-state manufacturers must track varying exemption criteria, maintain state-specific certificates, and ensure compliance with each jurisdiction’s unique requirements. Professional sales tax management helps navigate this complexity.