Understanding Alabama’s economic nexus threshold matters when you’re selling into one of the Southeast’s fastest-growing e-commerce markets. Cross $250,000 in annual sales to Alabama customers, and collection obligations kick in, regardless of physical presence.

The threshold sits higher than most states, but Alabama’s enforcement is aggressive and their notice process moves quickly. Hands Off Sales Tax (HOST) ensures you’re collecting correctly in Alabama while managing every other jurisdiction where you’ve triggered obligations.

What Is Economic Nexus?

Economic nexus represents the connection between a business and a state based purely on economic activity (sales volume) rather than physical presence. The 2018 South Dakota v. Wayfair Supreme Court decision eliminated the physical presence requirement for sales tax collection, allowing states to require remote sellers to collect tax once they exceed state-specific thresholds.

Before Wayfair, an online seller in California with zero physical presence in Alabama owed nothing to Alabama tax authorities, even with millions in Alabama sales. Post-Wayfair, economic activity alone creates nexus and triggers collection responsibilities.

This fundamentally changed e-commerce compliance. Small businesses that previously managed sales tax only in their home state now face obligations across dozens of jurisdictions.

Economic Nexus vs. Physical Nexus: Different Obligations

Alabama’s $250,000 economic nexus threshold applies specifically to sales tax obligations. This differs from Alabama’s factor presence nexus standards for income tax, which use different thresholds ($538,000 in sales, or $54,000 in property/payroll).

You can trigger sales tax nexus without triggering income tax nexus, and vice versa. Physical presence like FBA inventory, an office, or employees in Alabama, creates immediate sales tax nexus regardless of sales volume. Physical nexus and economic nexus operate independently; having one doesn’t automatically create the other.

For e-commerce sellers, this distinction matters. Storing inventory in Alabama warehouses creates physical nexus and immediate sales tax obligations, even with zero Alabama sales. Conversely, selling $300,000 to Alabama customers from another state creates economic nexus for sales tax but may not trigger Alabama income tax obligations.

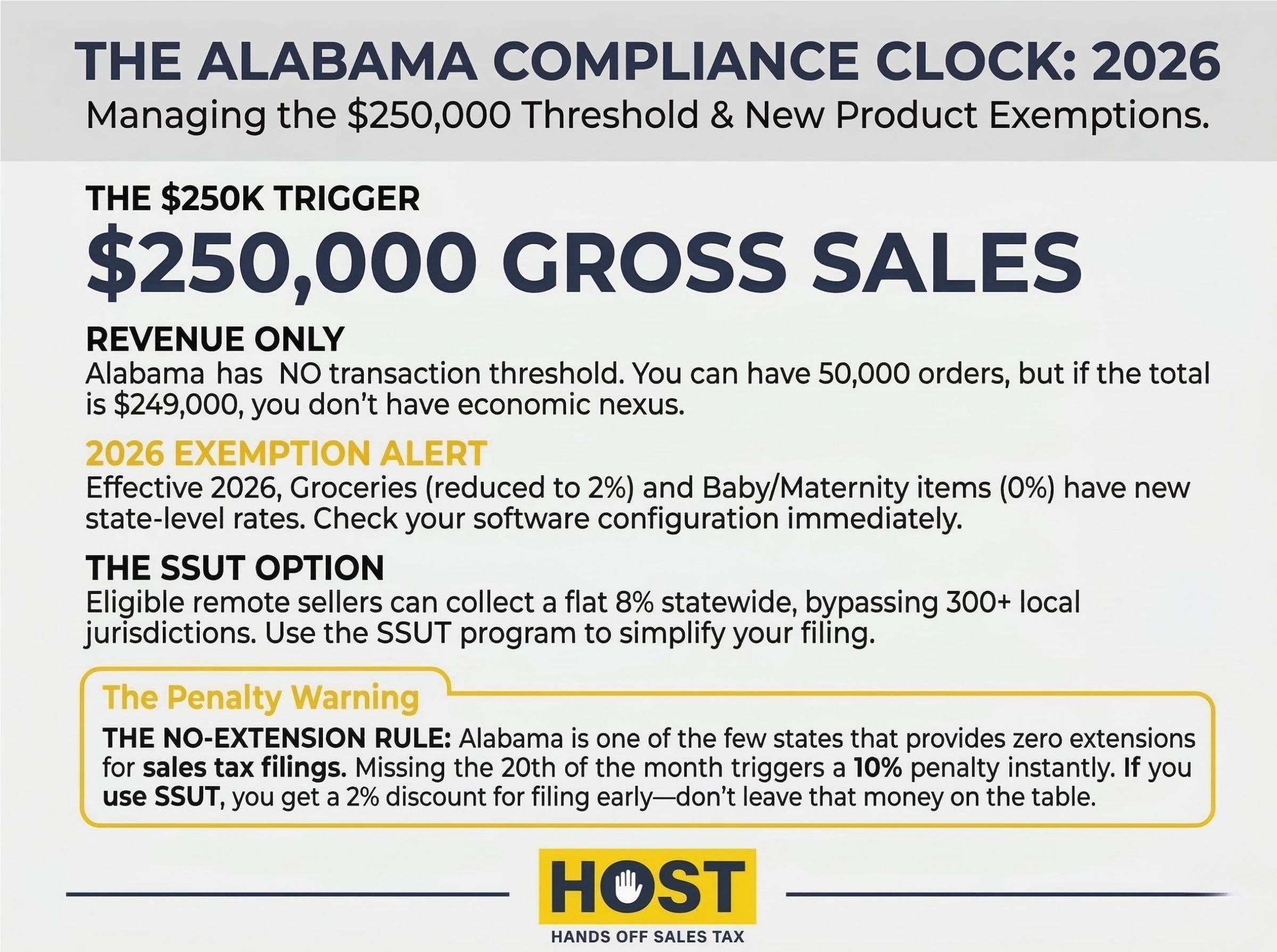

Alabama’s Economic Nexus Threshold: $250,000

Alabama’s economic nexus threshold is $250,000 in annual gross sales to Alabama customers. Unlike many states that use a dual threshold (sales amount or transaction count), Alabama has always relied solely on the dollar amount since the law took effect.

Key threshold details:

- Threshold amount: $250,000 in gross sales

- Measurement period: Current or previous calendar year

- Transaction threshold: None (Alabama has never had a transaction count requirement)

- Effective date: October 1, 2018

Once you exceed $250,000 in Alabama sales during a calendar year, you must register for an Alabama sales tax license, collect applicable state and local sales tax from customers, and file returns according to Alabama’s schedule.

The $250,000 threshold includes all taxable retail sales delivered to Alabama locations like products, digital goods, and taxable services.

What doesn’t count toward the threshold:

- Wholesale transactions with valid resale certificates

- Sales to tax-exempt organizations (government entities, qualifying nonprofits)

- Sales of specifically exempted items (certain manufacturing equipment, agricultural products, prescription drugs)

These exclusions mean you calculate the threshold using only retail sales of taxable goods and services to end consumers.

How Alabama Calculates the Threshold

Alabama measures economic nexus based on gross sales, the total dollar amount of retail sales before any deductions. Tax, shipping, and discounts are all included in the calculation.

Threshold calculation includes:

- Retail sale price of goods

- Taxable services and digital products

- Shipping and handling charges

- Sales tax collected

Threshold calculation excludes:

- Wholesale transactions with valid resale certificates

- Sales to tax-exempt organizations

- Sales of items Alabama specifically exempts

Alabama uses a calendar year lookback period. You evaluate whether you exceeded $250,000 during either the current calendar year or the previous calendar year. If you hit the threshold in 2024, you maintain collection obligations through at least December 31, 2025, even if 2025 sales drop below $250,000.

Registration Requirements Once You Hit the Threshold

Exceeding Alabama’s economic nexus threshold creates an immediate obligation to register for an Alabama sales tax license. You have two paths: traditional registration or Alabama’s Simplified Sellers Use Tax (SSUT) program.

Traditional Registration vs. SSUT Program

Traditional registration requires navigating Alabama’s complex jurisdictional landscape. You’ll register through the My Alabama Taxes (MAT) portal, collect tax at varying rates (5-11% depending on customer location), and potentially file returns with multiple jurisdictions.

The SSUT program offers remote sellers a streamlined alternative. Instead of tracking 300+ local rates, you collect a flat 8% on all Alabama sales regardless of customer location. This single rate covers state and local obligations, and you file one return instead of multiple.

SSUT advantages for remote sellers:

- Simplified rate calculation: 8% on all sales, no address-level validation needed

- Single filing requirement: One return eliminates home rule complications (more below)

- Collection discount: Keep 2% of collected tax (up to $400,000) when filing on time

- Amnesty provision: Pre-October 2019 sales receive amnesty if you register and remain in the program for three years

Most e-commerce businesses meeting the threshold benefit from SSUT. However, if you operate physical locations in Alabama, traditional registration may be required.

HOST’s sales tax registration service evaluates which registration path suits your business model and handles the entire process.

Alabama Sales Tax Rates and Local Jurisdictions

Alabama operates a destination-based sales tax system, meaning you charge tax based on where the customer receives the product (their shipping address).

Alabama tax structure:

- State rate: 4%

- Combined rates: Range from 5% to 11%

- Local jurisdictions: Over 300 (counties, cities, and special districts)

Alabama has over 300 local tax jurisdictions. Counties levy taxes (typically 1-4%), and many cities add municipal taxes (1-3%). Combined rates in major cities include:

- Montgomery: 10% (4% state + 6% local)

- Birmingham: 10% (4% state + 6% local)

- Huntsville: 9% (4% state + 5% local)

Alabama’s Home Rule Complication

Alabama uniquely allows approximately 130 municipalities to “self-administer” their sales tax, called home rule jurisdictions. Major home rule cities include Birmingham, Mobile, Montgomery, Huntsville, and Tuscaloosa.

What home rule means for compliance:

Traditional registration requires separate registrations and filings with each home rule city where you have customers, in addition to state filing. This creates multiple login portals, different deadlines, and varying local rules.

For remote sellers, this transforms Alabama from one jurisdiction into potentially dozens. A business selling to customers across Alabama could face 20+ separate filing obligations.

The SSUT program eliminates this complexity entirely. SSUT participants file one return at the flat 8% rate, and Alabama distributes revenue to local jurisdictions based on population. This is why most remote sellers choose SSUT over traditional registration.

Calculating the correct rate for every Alabama address (if not using SSUT) requires address-level validation. Sales tax software like TaxJar or Avalara automates this, but configuration errors remain common.

HOST offers a free sales tax software review to identify costly errors like incorrect rate assignments or double-taxing.

Filing Frequency and Deadlines in Alabama

Once registered, you must file Alabama sales tax returns according to the schedule Alabama assigns based on your tax liability.

Alabama filing frequencies:

- Monthly: Tax liability exceeds $2,400 per month

- Quarterly: Tax liability is $200–$2,400 per month

- Annual: Tax liability is less than $200 per month

Filing deadlines: Returns are due the 20th day of the month following the reporting period.

- Monthly: Due 20th of the following month (January sales due February 20)

- Quarterly: Due 20th of month following quarter-end (Q1 due April 20)

Alabama offers no extensions. Late filing incurs penalties of 10% of tax due plus interest at 1% per month.

Managing monthly or quarterly filings across Alabama and dozens of other states consumes 30+ hours per month for many businesses. HOST’s filing services handle all Alabama returns along with filings in every other state where you have obligations.

Marketplace Facilitator Law: When Amazon Collects for You

Alabama’s marketplace facilitator law requires platforms like Amazon, eBay, Etsy, and Walmart Marketplace to collect and remit sales tax on behalf of third-party sellers.

Effective date: January 1, 2019

If you sell through a marketplace that collects tax, you generally don’t need to collect Alabama sales tax on those specific transactions. The marketplace handles collection and remittance.

Your remaining obligations:

- Direct sales: You must still collect on sales through your own website or non-facilitated channels

- Threshold calculation: Marketplace sales count toward your economic nexus determination, even though the marketplace collects the tax

Example: You generate $300,000 in Alabama sales: $200,000 through Amazon FBA and $100,000 through Shopify. Amazon collects and remits on the $200,000. You must collect on the $100,000 Shopify sales. But both amounts count toward determining you’ve exceeded the threshold.

Common Alabama Nexus Mistakes to Avoid

Mistake #1: Ignoring FBA or warehouse inventory

Physical presence still creates nexus. If you use Amazon FBA or store inventory in Alabama warehouses, you have physical nexus regardless of sales volume, triggering immediate obligations.

Mistake #2: Waiting until year-end to register

Alabama expects registration immediately upon crossing the threshold. If you hit $250,000 in July, register in July or August. Not January. Delayed registration risks retroactive assessments and penalties.

Mistake #3: Assuming marketplace sales exempt you completely

Marketplace facilitator laws cover only transactions through the marketplace. Your direct sales still require collection. Plus, marketplace sales count toward economic nexus determination.

Mistake #4: Filing in the wrong jurisdiction or at incorrect rates

Alabama’s 300+ local jurisdictions mean address-level accuracy matters. Charging Birmingham rates to a Tuscaloosa customer creates compliance problems.

HOST’s nexus analysis service identifies exactly where you have obligations across all states, including Alabama, preventing these costly mistakes before they happen.

What Happens If You Don’t Comply

Alabama enforces sales tax collection aggressively. Non-compliance triggers penalties, interest, and potential audits.

Consequences of non-compliance:

- Penalties: 10% of unpaid tax for late filing, 10% for late payment (can stack to 20%)

- Interest: 1% per month on unpaid tax

- Retroactive collection: Alabama can assess back taxes for uncollected periods, typically 3 years

- Audits: Non-compliant businesses face higher audit risk

Alabama regularly data-mines e-commerce transactions and coordinates with other states. They identify sellers exceeding thresholds who haven’t registered, then send compliance notices demanding registration and back tax payment.

Voluntary Disclosure Agreements (VDAs): If you discover past non-compliance, a VDA can limit your exposure. Alabama offers VDA programs that typically limit the lookback period to 3 years and waive penalties (though interest still applies).

HOST’s VDA services negotiate directly with Alabama and other states on your behalf, minimizing liability and protecting you from maximum penalties.

HOST: Your Partner for Alabama Sales Tax Compliance

Alabama’s economic nexus threshold is just one of 45+ state rules you’re monitoring simultaneously. Each state has different thresholds, rates, filing frequencies, and local complications. Managing this yourself diverts focus from growing your business and creates constant compliance anxiety.

What HOST delivers:

- Nexus Analysis: We analyze your sales footprint to determine exactly where you’ve triggered economic or physical nexus

- Sales Tax Registration: We handle Alabama registration and all other required states, managing paperwork and follow-up

- Ongoing Filing: We prepare and file Alabama returns (monthly, quarterly, or annually) along with returns in every other jurisdiction

- Software Optimization: We review your TaxJar, Avalara, or other automation tools to ensure accurate Alabama rate calculations

- Notice Management: We interpret and respond to Alabama Department of Revenue notices efficiently

- Audit Defense: We’re your trusted partner in Alabama sales tax audits, organizing documentation and defending your position

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping e-commerce businesses navigate changing requirements. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

You handle the sales, we handle the tax.

Ready to Ensure Alabama Compliance?

Understanding Alabama’s economic nexus threshold is step one. Monitoring whether you’ve crossed it, registering promptly, collecting at correct rates across 300+ jurisdictions, and filing on time month after month, and that’s where the real challenge lives.

Whether you’re approaching the $250,000 threshold, just crossed it, or discovered you should have been collecting years ago, the right sales tax partner ensures compliance supports growth rather than hindering it.

Contact HOST today to discuss your Alabama compliance needs or schedule a free consultation. Let us handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is Alabama’s economic nexus threshold?

Alabama’s economic nexus threshold is $250,000 in annual gross sales to Alabama customers. Alabama has no transaction count threshold. Only the dollar amount matters. If you exceed $250,000 in either the current or previous calendar year, you must register, collect, and remit Alabama sales tax.

Do marketplace sales count toward Alabama’s economic nexus threshold?

Yes, marketplace sales count toward the $250,000 threshold calculation. However, if the marketplace collects and remits tax on your behalf (like Amazon or eBay), you don’t need to collect on those specific transactions. You must still collect on direct sales through your own website once you exceed the threshold.

When should I register for Alabama sales tax after crossing the threshold?

Alabama requires registration immediately upon exceeding the $250,000 threshold. If you cross mid-year, register within 30 days, not at year-end. Delayed registration risks retroactive assessments, penalties, and interest on uncollected tax.

How often do I need to file Alabama sales tax returns?

Alabama assigns filing frequency based on your tax liability: monthly if you collect over $2,400/month, quarterly for $200-$2,400/month, or annually for under $200/month. Returns are due by the 20th day of the month following the reporting period. Alabama provides no extensions.

What happens if I have physical inventory in Alabama?

Physical inventory in Alabama like FBA inventory or warehouse stock creates physical nexus separate from economic nexus. Physical nexus triggers immediate registration and collection obligations regardless of sales volume, even if you’re below the $250,000 threshold.

Can I avoid penalties if I discover past non-compliance in Alabama?

Yes, through Alabama’s Voluntary Disclosure Agreement (VDA) program. A VDA typically limits the lookback period to 3 years and waives penalties, though interest still applies. HOST negotiates VDAs with Alabama on your behalf, minimizing liability and protecting you from maximum penalties.