Cross $500,000 in sales AND 100 transactions to New York customers, and you’re on the hook for sales tax. No physical presence required. For e-commerce businesses juggling multi-state compliance, New York presents one of the trickiest jurisdictions: economic nexus rules that demand both revenue and transaction tracking, local tax variations across hundreds of jurisdictions, and enforcement that doesn’t mess around.

That’s where Hands Off Sales Tax (HOST) steps in. With 25+ years laser-focused on sales tax compliance, we handle New York nexus analysis, registration, ongoing filings, and audit defense so you can focus on growth instead of decoding tax codes.

What Is Sales Tax Nexus?

Sales tax nexus is the connection between your business and a state that creates a tax collection obligation. Think of it as the invisible tripwire that triggers your duty to collect and remit.

Nexus comes in two flavors: physical and economic.

Physical nexus means tangible presence, like offices, warehouses, employees, inventory in fulfillment centers. Store products in an Amazon FBA facility in Buffalo? You’ve got physical nexus.

Economic nexus, born from the 2018 South Dakota v. Wayfair Supreme Court decision, changed everything. States can now require sales tax collection based purely on sales volume or transaction count. No boots on the ground needed. Sell enough to New York customers from your California garage, and you still owe New York sales tax.

This shift fundamentally changed e-commerce compliance overnight.

New York’s Economic Nexus Threshold: $500,000 AND 100 Transactions

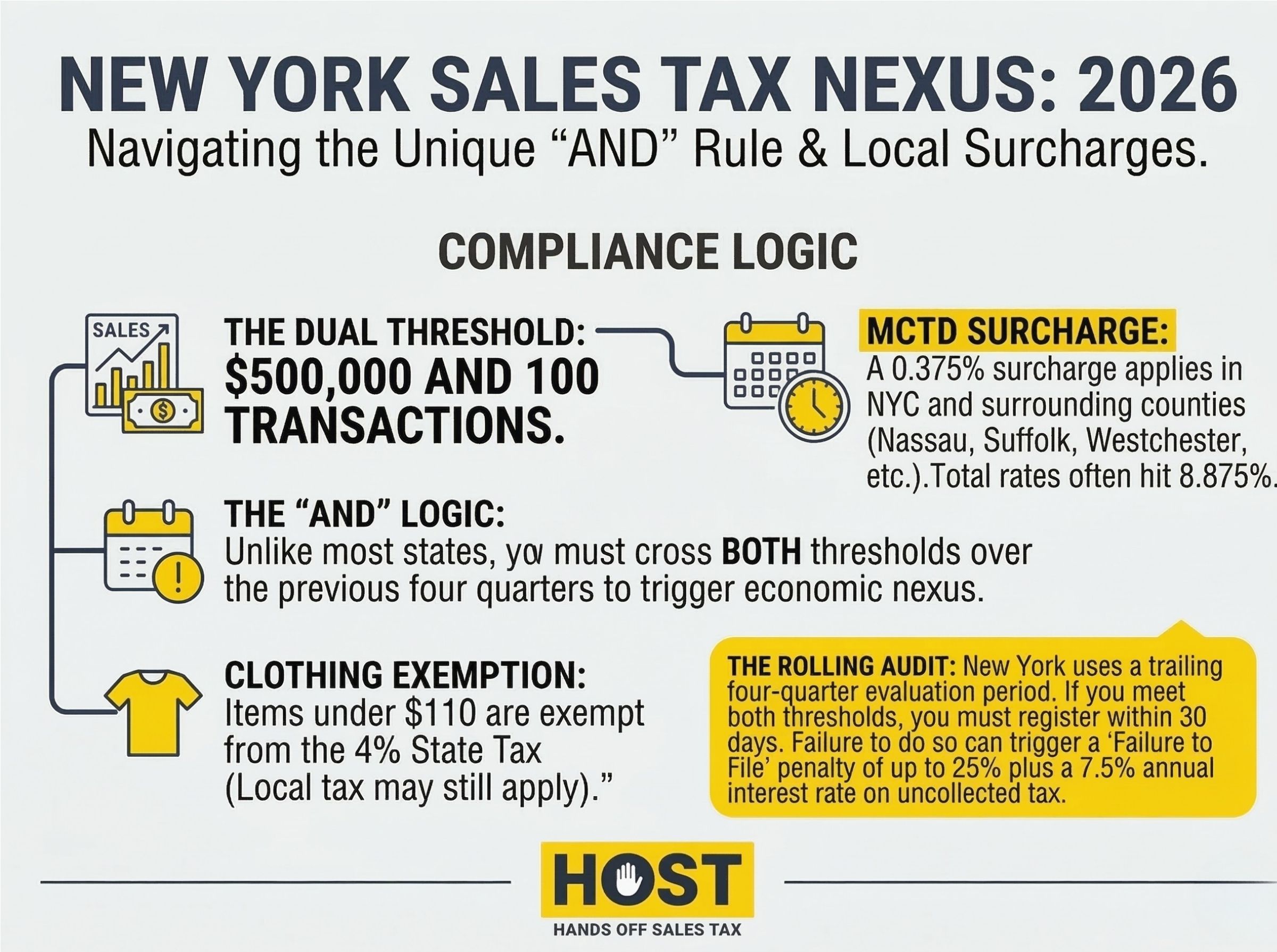

New York’s economic nexus threshold requires meeting BOTH criteria: $500,000 in gross receipts AND more than 100 transactions during the preceding four sales tax quarters.

New York is one of only two states (along with Connecticut) requiring BOTH thresholds to be met. Most states use “OR” logic, meaning if you exceed either the sales threshold or transaction count and you’re in. This dual-threshold approach actually makes New York less aggressive than typical economic nexus states.

Historical note: New York initially set its threshold at $300,000 following the 2018 Wayfair decision. The state raised it to $500,000 on June 24, 2019, effective retroactively to June 21, 2018 (the Wayfair decision date). If you were collecting under the old $300,000 threshold during 2018-2019, you met the requirement even before the increase.

Here’s what matters:

$500,000 threshold: Total sales to New York customers. Not profit, not just taxable sales. Hit $500,001 and you’ve crossed the first hurdle.

100 transactions threshold: You need more than 100 separate sales into New York. Each invoice counts as one transaction, taxable or not.

Both thresholds required: Unlike most states using “OR” logic (hit either threshold, you’re in), New York demands BOTH. Rack up $600,000 in sales but only 95 transactions? No nexus. Make 150 transactions totaling $400,000? Still no nexus.

Four sales tax quarters: New York measures on a rolling four-quarter basis using periods ending February 28/29, May 31, August 31, and November 30. Exceed both thresholds across any consecutive four quarters and nexus kicks in.

Everything counts: All sales delivered to New York count toward your calculation, whether taxable or exempt. That wholesale order with a resale certificate? Still counts.

New York offers no grace period. Meet both thresholds and you must register immediately (within 30 days) and begin collecting 20 days after registration.

When Does Economic Nexus Begin?

Here’s a practical scenario:

By August 31, 2025, your trailing four quarters show:

- September-November 2024: $120,000 (35 transactions)

- December-February 2025: $135,000 (28 transactions)

- March-May 2025: $145,000 (31 transactions)

- June-August 2025: $105,000 (12 transactions)

Total: $505,000 and 106 transactions. You’ve crossed both thresholds.

Register within 30 days and start collecting 20 days after registration. Delay, and you’re building exposure.

For more details on navigating multi-state sales tax compliance, HOST provides comprehensive guidance tailored to your business.

Physical Nexus Still Matters

While economic nexus grabs headlines, physical nexus creates immediate obligations regardless of sales volume.

Physical nexus in New York includes:

- Offices or facilities of any size

- Employees working in New York (including remote workers)

- Inventory storage (including Amazon FBA facilities)

- Certain affiliate relationships

Physical nexus triggers obligation instantly. Even $1 in sales combined with physical presence requires registration and collection.

Marketplace Facilitator Laws

New York’s marketplace facilitator law (effective June 1, 2019) requires platforms like Amazon, eBay, and Etsy to collect and remit sales tax for third-party sellers.

For marketplace-only sellers, this simplifies life. The platform handles everything.

The complexity hits multi-channel sellers:

Threshold monitoring: Marketplace sales count toward your thresholds. Sell $300,000 through Amazon (80 transactions) and $250,000 through Shopify (25 transactions)? You’ve hit $550,000 and 105 transactions—both thresholds met. You must register for direct sales.

New York Sales Tax Rates: Local Complexity

New York imposes 4% state sales tax, but combined rates reach 8-8.875% in most locations due to local jurisdictions adding their own percentages.

New York has over 1,200 local taxing jurisdictions. Combined rates include:

- New York City: 8.875% (includes 0.375% MCTD surcharge)

- Buffalo: 8.75%

- Rochester: 8%

- Albany: 8%

The 0.375% Metropolitan Commuter Transportation District (MCTD) surcharge applies in New York City plus Dutchess, Nassau, Orange, Putnam, Rockland, Suffolk, and Westchester counties.

Calculating the correct rate requires destination-based sourcing. You charge based on where the customer receives the product. Ship from Albany to Manhattan? Charge the 8.875% NYC rate.

This destination-based approach demands address validation at the ZIP+4 level. A single ZIP code can span multiple tax jurisdictions with different rates.

Common Exemptions

Clothing and footwear under $110: Individual items priced below $110 are exempt from state sales tax (though NYC and some counties still impose local tax).

Groceries: Most food for home consumption is exempt. Prepared foods, restaurant meals, and soda remain taxable.

Prescription medications: Exempt.

Resale exemption: Purchases for resale are exempt with valid resale certificate (Form ST-120).

Exemptions create complexity. Misconfiguring software to charge tax on exempt items costs customer goodwill. Failing to collect tax on taxable items creates audit liability.

HOST’s free sales tax software review identifies configuration errors costing you money or creating compliance gaps.

Filing Frequency and Deadlines

Once registered, New York assigns filing frequency based on expected tax liability:

Quarterly filers: Most businesses file quarterly (under $3,000 annual liability). Returns due on the 20th day after quarter-end. New York’s quarters run March-May, June-August, September-November, December-February.

Monthly filers: Businesses with taxable receipts exceeding $300,000 per quarter file monthly. Returns due the 20th of the following month.

Annual filers: Rare for e-commerce sellers with nexus.

New York requires electronic filing. Missing deadlines triggers penalties and interest—late filing penalty up to 25% of tax due, late payment penalty up to 25%, and interest around 7.5% annually.

These penalties compound quickly.

Audit Risk and Enforcement

New York aggressively pursues sales tax compliance, particularly targeting:

- Out-of-state sellers who should have registered for economic nexus

- Businesses with physical presence (inventory, employees) who haven’t registered

- Companies with inconsistent reporting or filing gaps

A sales tax audit examines your records to verify correct collection and remittance. Auditors review sales records, exemption certificates, rate calculations, and filing history.

Audits look back three years (six if you never filed). Assessments include unpaid tax, penalties, and interest, often totaling 1.5-2x the original tax owed.

If you’re facing an audit, HOST’s audit defense services provide expert representation throughout the process.

Beyond Sales Tax: New York’s Franchise Tax Obligation

Sales tax isn’t the only obligation triggered by New York sales. Businesses earning over $1 million in New York receipts also face New York corporate franchise tax requirements, even without physical presence in the state.

This $1 million franchise tax threshold is separate from the $500,000 sales tax threshold. Many businesses hitting sales tax nexus will also trigger franchise tax obligations as they scale. Unlike sales tax (which you collect from customers), franchise tax is a direct tax on your business income allocated to New York.

If you’re approaching or exceeding $1 million in New York revenue, consult with a tax professional about both sales tax and corporate franchise tax obligations. HOST focuses exclusively on sales tax compliance, but we can connect you with qualified advisors for franchise tax matters.

How HOST Simplifies New York Compliance

Managing New York sales tax in-house drains time and creates risk. Most e-commerce businesses spend 30+ hours monthly on sales tax between monitoring thresholds, calculating rates across 1,200+ jurisdictions, and filing on time.

Hands Off Sales Tax eliminates this burden:

Nexus Analysis: We analyze your sales data and marketplace activity to determine precisely when you crossed both thresholds.

Registration Services: We handle Certificate of Authority registration, managing state communications and securing your sales tax ID.

Automated Filing: We prepare and file your returns (quarterly or monthly) with proper local tax allocation. You never miss a deadline.

Software Review: We review your TaxJar, Avalara, or other tools to ensure correct rate calculation across all jurisdictions.

Notice Management: When New York sends confusing notices, we interpret and respond appropriately.

Voluntary Disclosure Agreements: If you discover you should have been collecting for years, we file VDAs to limit lookback periods and abate penalties.

We’ve been 100% focused on sales tax for over 25 years. Through our parent company TaxMatrix, we’ve helped North America’s largest companies manage complex compliance. Now we bring that expertise to e-commerce sellers navigating New York and 44 other states.

Ready to Handle New York Sales Tax Correctly?

New York’s dual thresholds ($500,000 in sales AND 100 transactions), complex local tax structure, and aggressive enforcement make compliance challenging. Every day you collect incorrectly or fail to register increases audit risk.

Whether you’re approaching the thresholds, recently crossed them, or discovered you should have registered years ago, professional help eliminates guesswork and prevents costly mistakes.

At HOST, we combine deep technical expertise with transparent communication and personalized support. You handle the sales, we handle the tax.

Contact us today to discuss your New York compliance needs or schedule a free consultation. Let us take New York sales tax off your plate so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is New York’s sales tax nexus threshold?

New York’s economic nexus threshold requires meeting BOTH criteria: $500,000 in gross receipts AND more than 100 transactions during the preceding four sales tax quarters. Unlike many states using “OR” logic, New York requires you to exceed both thresholds to trigger collection obligation.

Do marketplace sales count toward the New York nexus threshold?

Yes. Sales made through Amazon, eBay, Etsy, and other marketplaces count toward both thresholds: the $500,000 revenue threshold and the 100-transaction threshold, even though the marketplace collects and remits tax. You must track all New York sales across all channels when determining if you’ve crossed both thresholds for your direct sales.

What happens if I don’t register after exceeding the threshold?

Failure to register creates audit risk and potential liability. New York can assess back taxes for up to three years (six if you never filed), plus penalties up to 50% and interest around 7.5% annually. The state requires registration within 30 days of meeting both thresholds and collection beginning 20 days thereafter.

How do I calculate the correct sales tax rate in New York?

New York uses destination-based sourcing, meaning you charge based on the customer’s location. With over 1,200 local jurisdictions, accurate rate calculation requires address validation at the ZIP+4 level. Most businesses use sales tax automation software, though proper configuration is critical to avoid errors.

Does physical presence in New York create nexus regardless of sales volume?

Yes. Any physical presence: offices, warehouses, employees, inventory storage (including Amazon FBA) creates nexus immediately, regardless of sales volume. Even minimal physical presence requires registration and collection.

How often do I need to file New York sales tax returns?

Filing frequency depends on your tax liability. Most e-commerce sellers file quarterly (if under $3,000 annual liability) or monthly (if taxable receipts exceed $300,000 per quarter). Returns are typically due on the 20th of the month following the period end.

Can I stop collecting New York sales tax if my sales drop below the thresholds?

If your sales fall below both $500,000 AND 100 transactions across any rolling four-quarter period, you may be able to file a final return and deregister. However, you must continue filing until both thresholds remain below limits for an extended period. New York doesn’t have explicit trailing nexus policies, so consult with a sales tax professional before deregistering.