Understanding Illinois sales tax nexus is absolutely essential. Cross the wrong threshold, and you’re suddenly on the hook for collection obligations that trigger immediately. Miss Illinois nexus entirely, and you’re looking at back taxes, penalties, and audit exposure that can drain your cash flow faster than a quarterly filing deadline.

Illinois doesn’t mess around with economic nexus. Hit $100,000 in sales to Illinois customers over twelve months, and collection obligations begin. That’s it. No grace period, no registration cushion, just immediate responsibility whether you’ve filed the paperwork or not.

That’s where Hands Off Sales Tax (HOST) makes the difference. We analyze your sales footprint, identify exactly when you triggered nexus, handle registration across all Illinois jurisdictions, and manage ongoing filings so compliance never pulls focus from growth.

What Sales Tax Nexus Actually Means

Sales tax nexus is the connection between your business and Illinois that creates legal obligation to collect and remit tax. Think of it as crossing an invisible threshold. Once you’re over, you’re in.

Two nexus types exist: physical and economic. Physical nexus triggers through tangible presence like offices, warehouses, employees, or inventory. Economic nexus triggers through sales volume alone, regardless of whether you’ve ever set foot in the state.

The 2018 Wayfair decision changed everything. States gained authority to require remote sellers to collect sales tax based purely on economic activity. This eliminated the physical presence requirement that had protected online sellers for decades.

For Illinois, once nexus exists (either type) you must register, collect the correct combined state and local tax, and file returns on schedule.

Illinois Economic Nexus: The $100,000 Rule

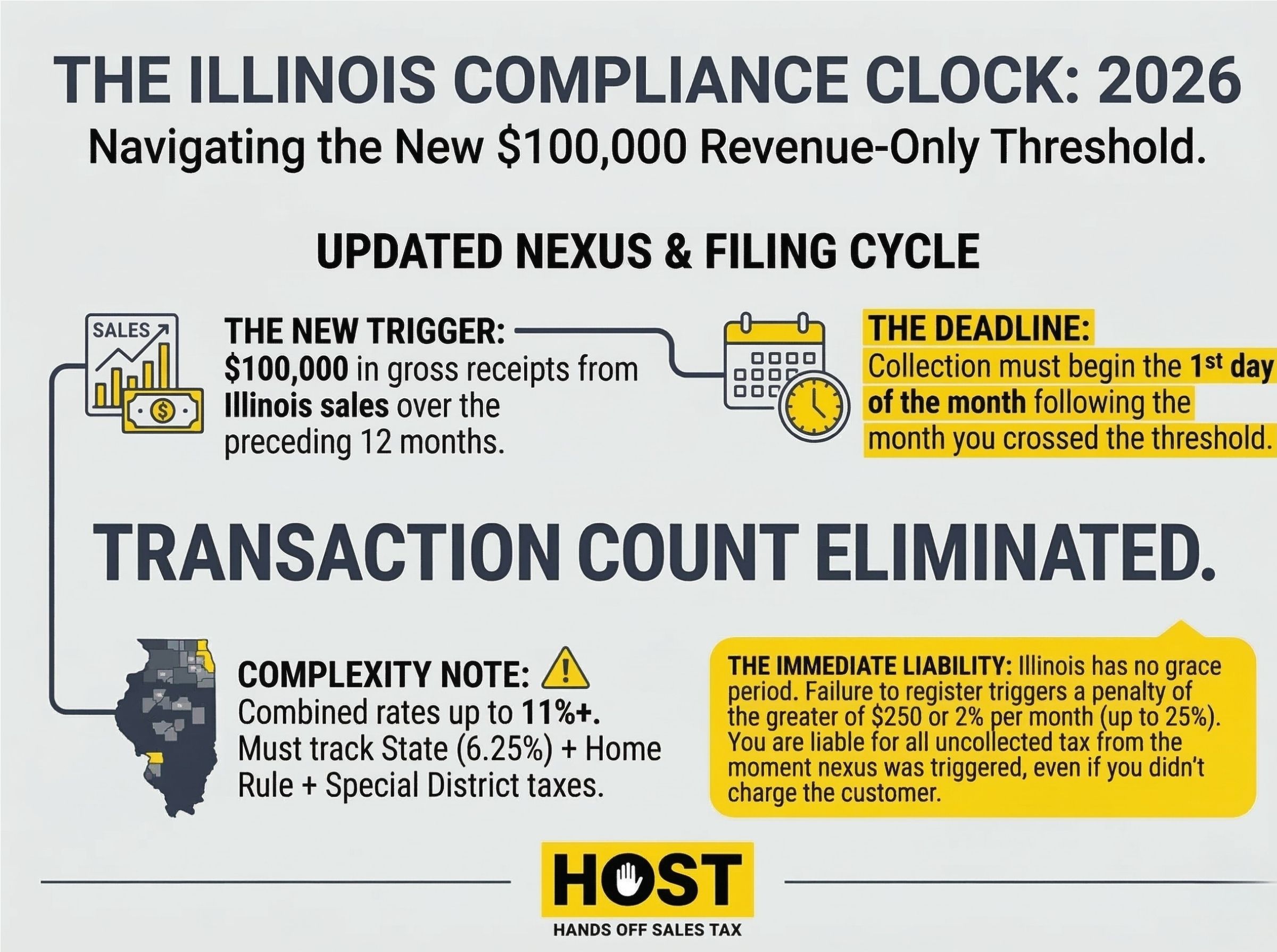

Critical Update: Illinois eliminated its 200-transaction threshold on January 1, 2026.

Economic nexus now triggers on one metric: $100,000 in gross receipts from Illinois sales over the preceding 12 months.

This simplifies compliance significantly. No more counting individual transactions, just monitor total revenue. Businesses with high transaction volumes but lower dollar amounts just caught a break.

Illinois uses quarterly evaluation periods (end of March, June, September, December). You must monitor sales continuously to determine when you cross the threshold.

Once you exceed $100,000, collection obligations begin the first day of the month following the month you crossed. Cross the threshold June 15? You’re collecting July 1. No grace period. No registration delay. Immediate obligation.

The 2026 change means updating your nexus monitoring systems to track gross receipts exclusively, not transaction counts.

Physical Nexus: Any Presence Counts

Physical nexus has no threshold. Any tangible presence creates immediate obligations.

Facilities: Own, lease, or maintain any office, warehouse, or distribution center in Illinois? That’s nexus.

Employees: Full-time, part-time, temporary, or remote employees working from Illinois homes all create nexus. One employee triggers obligations for your entire business.

Inventory: Storing products in Illinois warehouses creates nexus, even third-party fulfillment. Amazon FBA sellers frequently trigger Illinois nexus when Amazon stores their inventory in Illinois fulfillment centers.

Trade Shows: Attending Illinois trade shows or events where you make sales or solicit orders can create nexus, particularly with regular or extended presence.

Affiliates: Illinois-based affiliates, partners, or related businesses that refer customers or assist with sales can trigger nexus under click-through provisions.

Physical nexus demands immediate registration. Any presence, no matter how minimal, creates collection obligations.

Registering for Illinois Sales Tax

Once nexus exists, registration isn’t optional. Illinois requires all businesses with nexus to obtain a Certificate of Registration before making taxable sales.

Navigate to MyTax Illinois, the state’s online portal. You’ll need your business information: legal name, EIN or SSN, business structure, contact details, and NAICS code.

Complete Form REG-1, the Illinois Business Registration Application. This single form handles sales tax registration along with other state obligations. Budget 30-45 minutes if you have all information ready.

Provide estimated monthly Illinois sales. The state uses this to assign your filing frequency: monthly, quarterly, or annually based on volume.

No registration fee applies. Once approved, Illinois issues your Certificate of Registration and Account ID, typically within 1-2 business days for online applications.

When to Register: Before you begin collecting. If you just crossed economic nexus thresholds, register immediately. Delays create liability, meaning you owe tax on all sales after your obligation begins, registered or not.

HOST Handles Registration: Our sales tax registration service manages the entire process across all states where you have nexus. We complete applications, handle follow-up, and ensure you’re properly licensed everywhere required so you can focus on running your business instead of navigating state bureaucracy.

Illinois Rates: State Plus Local Complexity

Illinois charges 6.25% state sales tax. But local jurisdictions add their own taxes, creating combined rates varying significantly across the state.

Combined rates range from 6.25% in jurisdictions with no local tax to over 11% in some Chicago locations. Cook County adds 1.75%. Chicago adds 1.25%. Special districts add more.

Calculating correct sales tax requires address-level precision. Two customers in adjacent zip codes may owe different rates based on exact location within different taxing jurisdictions.

Home Rule Jurisdictions: Illinois has over 100 home rule municipalities with authority to impose additional local taxes and set rates. This creates compliance complexity beyond typical state requirements.

Filing Frequencies: Illinois assigns frequency based on average monthly tax liability:

- Monthly: Over $200/month

- Quarterly: $50-$200/month

- Annual: Under $50/month

New registrants typically start monthly until the state has sufficient data to reassign.

Local Returns: Some home rule jurisdictions require separate local returns beyond your state filing. One Illinois sale might require filing on both the state ST-1 return and a separate municipal return.

HOST’s filing services handle this complexity! State returns, all required local returns, varying deadlines across jurisdictions. Nothing falls through cracks.

Common Illinois Nexus Triggers

Amazon FBA: Storing inventory through FBA or 3PL providers creates physical nexus. Amazon operates multiple Illinois fulfillment centers. When Amazon transfers your inventory to Illinois, nexus triggers immediately.

Marketplace facilitator laws add critical nuance. Amazon collects and remits Illinois tax on FBA marketplace sales. However, you still have nexus for any non-Amazon channels. If you sell through your website, other marketplaces, or wholesale, you must collect Illinois tax on those sales yourself.

Whether FBA inventory creates physical nexus for you depends on how that inventory is used. If it fulfills only marketplace orders where the facilitator collects tax, it doesn’t create physical nexus. If it fulfills your own direct sales or both marketplace and direct sales, it creates physical nexus, triggering broader collection obligations.

This distinction matters for multi-channel sellers. Inventory supporting your Shopify store alongside FBA sales creates nexus differently than inventory exclusively fulfilling Amazon marketplace orders.

Drop Shipping: Drop shipping into Illinois creates nexus if either you or your supplier has Illinois presence.

Remote Employees: Hiring a single remote employee living in Illinois establishes physical nexus. This creates collection obligations on all Illinois sales, not just sales that employee touches.

Trade Shows: Participating in Chicago trade shows or Illinois pop-up events can trigger nexus. Single events may not create permanent nexus, but repeated presence or extended duration increases risk.

The Cost of Non-Compliance

Failing to collect required Illinois tax creates serious consequences. Illinois actively pursues non-compliant remote sellers, particularly those exceeding economic nexus thresholds.

Back Taxes: You owe all uncollected tax from when nexus began. Crossed thresholds two years ago but never registered? You’re liable for two years of back taxes, even though you didn’t collect from customers.

Penalties: Illinois imposes penalties for late registration, late filing, and late payment. Failure to register penalty: the greater of $250 or 2% per month, up to 25%. Late payment penalties add 2% monthly.

Interest: Illinois charges interest on all unpaid tax from original due dates. Rates fluctuate but typically range 3-5% annually.

Audits: The state can audit records for 3.5 years standard or longer for suspected fraud. Audits require extensive documentation and can uncover additional issues beyond initial scope.

The financial impact compounds fast. Owing $50,000 in back taxes might mean $12,500 in penalties plus interest, creating total liability exceeding $65,000.

Voluntary Disclosure: Limiting Exposure

Discovered you should have been collecting Illinois tax but weren’t? A Voluntary Disclosure Agreement (VDA) can limit exposure.

Illinois VDAs allow voluntary disclosure before the state contacts you. In exchange, the state typically limits lookback to 4 years and often waives penalties, though you’ll still owe tax and interest.

The VDA process requires calculating past Illinois sales, estimating uncollected tax, and negotiating with Illinois Department of Revenue. You must commit to registering and remaining compliant forward.

When VDAs Make Sense: If you’ve been selling into Illinois for years without collecting, accumulated liability can be substantial. A properly negotiated VDA can save tens of thousands in penalties and reduce lookback exposure.

HOST’s VDA Services: We handle voluntary disclosures with states including Illinois. Our team analyzes exposure, prepares documentation, negotiates with authorities, and structures agreements minimizing liability while bringing you into compliance.

HOST: Your Illinois Compliance Partner

Illinois sales tax demands precision. Combined rates, home rule jurisdictions, varying filing frequencies, and aggressive enforcement create complexity pulling focus from growth.

What HOST Delivers:

Nexus Analysis: We analyze your sales footprint to determine exactly where you’ve triggered Illinois nexus and when obligations began.

Registration: We handle Illinois registration completely: Form REG-1, Department of Revenue follow-up, Certificate of Registration before you begin collecting.

Ongoing Filings: We file Illinois ST-1 returns monthly, quarterly, or annually based on assigned frequency, plus all required home rule local returns.

Software Optimization: We audit your TaxJar, Avalara, or other tools ensuring correct Illinois rate calculations across all local jurisdictions.

Notice Management: Illinois notices require quick response. We interpret what the state wants, prepare documentation, respond within deadlines.

Audit Defense: If Illinois audits your compliance, we’re your partner throughout organizing records, preparing responses, and working to minimize liability.

We’ve been 100% focused on sales tax since 1999. That’s 25 years managing compliance so you keep hands on your business. Through parent company TaxMatrix, we’ve served North America’s largest companies. Now we bring that expertise to e-commerce sellers of all sizes.

You handle the sales, we handle the tax.

Ready for Illinois Compliance?

Illinois nexus creates obligations that can’t be ignored. Whether you just crossed the $100,000 threshold, discovered Illinois inventory creating physical nexus, or realized you should have been collecting for months, action now limits exposure and prevents compounding penalties.

Professional help eliminates guesswork. Every hour researching Illinois regulations, calculating local rates, or preparing returns is an hour not growing revenue. The right partner handles complexity while you focus on what you do best.

Contact HOST today to discuss Illinois compliance or schedule a free consultation. Let us determine your nexus status, handle registration and filings, and ensure correct collection across all Illinois jurisdictions.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What triggers Illinois sales tax nexus for remote sellers?

Update: As of January 1, 2026, Illinois eliminated the 200-transaction threshold. Economic nexus now triggers when you exceed $100,000 in sales to Illinois customers in the preceding 12 months. Physical nexus triggers through any tangible presence including employees, inventory, or facilities.

When must I start collecting Illinois sales tax?

You must begin collecting the first day of the month following the month you exceeded the $100,000 threshold. Physical nexus obligations begin immediately when presence is established.

Does Amazon collect Illinois tax for FBA sellers?

Amazon collects and remits Illinois tax on sales through their marketplace. However, if you sell through other channels (your website, other marketplaces, wholesale), you must collect Illinois tax on those sales yourself since Amazon FBA creates physical nexus.

What are penalties for not collecting Illinois tax?

Illinois imposes the greater of $250 or 2% per month (up to 25%) for failure to register, plus 2% monthly late payment penalties, plus interest on all unpaid tax. Back taxes are owed from when nexus began, even if you never collected from customers.

How often must I file Illinois returns?

Filing frequency depends on average monthly tax liability. Monthly filers average over $200/month, quarterly filers $50-$200/month, annual filers under $50/month. Illinois assigns frequency based on reported sales.

Can I resolve past Illinois obligations without full penalties?

Yes, through a Voluntary Disclosure Agreement (VDA). Illinois VDAs typically limit lookback to 4 years and may waive penalties in exchange for voluntary compliance and payment of tax plus interest. Professional negotiation optimizes terms.