Understanding physical nexus vs economic nexus determines where your business owes sales tax. Get this wrong, and you’re either over-collecting from customers or under-collecting for states, and both spell trouble. Physical presence once defined everything. Now, your sales volume alone triggers obligations in states you’ve never visited.

For e-commerce sellers managing multi-state operations, nexus rules shape registration requirements, filing obligations, and audit exposure across 45 states. Each jurisdiction applies different thresholds. Cross one state’s economic nexus threshold today, and registration deadlines start immediately.

That’s where Hands Off Sales Tax (HOST) matters. We analyze your footprint, determine exactly where nexus exists, handle registrations across all applicable states, and manage ongoing filings so you stay compliant without sacrificing growth.

What Is Sales Tax Nexus?

Nexus is the connection between your business and a state that gives that state authority to require you to collect and remit sales tax. Without nexus, you have no obligations in that state. With nexus, you must register, collect tax on taxable sales, file returns according to the state’s schedule, and remit collected taxes by their deadlines.

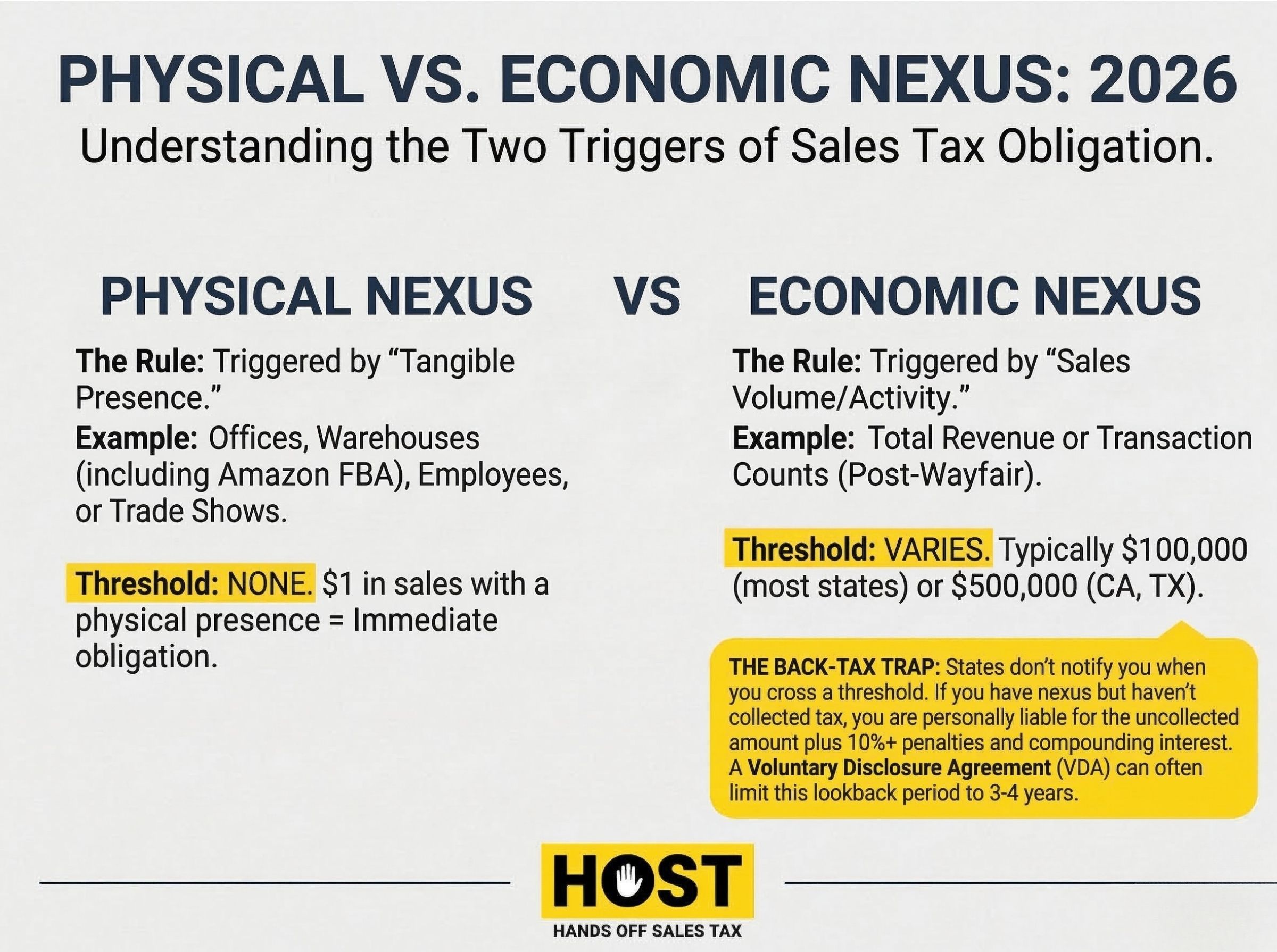

Two primary nexus types exist: physical and economic. Most businesses trigger one or both across multiple states, creating complex compliance obligations that vary by jurisdiction.

Physical Nexus: The Traditional Standard

Physical nexus exists when your business maintains a tangible presence in a state. This includes obvious situations like storefronts or warehouses, but extends to connections that catch businesses by surprise.

What Creates Physical Nexus

Office or Retail Location: Any permanent establishment creates immediate physical nexus.

Warehouse or Inventory Storage: Storing inventory, even temporarily, establishes nexus. This includes third-party fulfillment centers, Amazon FBA warehouses, or consignment arrangements.

Employees or Contractors: Having employees working in a state creates nexus. Independent contractors and sales representatives operating on your behalf also trigger obligations.

Temporary Presence: Attending trade shows, conducting sales presentations, or providing installation services can create nexus depending on duration and frequency.

Affiliate Relationships: Some states enforce “click-through nexus” when you compensate in-state businesses for referrals, even without direct physical presence.

Physical nexus rules existed for decades. The 1992 Supreme Court Quill Corp. v. North Dakota decision established that physical presence was required before states could impose sales tax collection obligations, protecting remote sellers from obligations in states where they had no presence.

This protection gave online retailers a significant price advantage. Customers could buy a $600 couch online tax-free while paying $648 at a local store, prompting brick-and-mortar retailers to challenge the fairness of this marketplace.

This protection lasted until 2018.

Economic Nexus: The Post-Wayfair Reality

The June 21, 2018 South Dakota v. Wayfair Supreme Court decision fundamentally changed sales tax compliance. The Court ruled that physical presence is no longer required. States can require sales tax collection based solely on economic activity within their borders.

This decision enabled states to impose “economic nexus” thresholds. Economic nexus didn’t replace physical nexus, both exist concurrently. Physical presence remains the first consideration when determining obligations. Remote sellers crossing economic thresholds must register, collect, and remit sales tax regardless of physical presence.

How Economic Nexus Works

Economic nexus triggers when your business exceeds a state’s threshold for sales revenue, transaction count, or both during a specified period (typically the current or previous calendar year).

Common Threshold Patterns:

- $100,000 in sales (most states)

- $500,000 in sales (California, Texas)

- 200 transactions (fewer states still use this)

- Combined sales and transaction thresholds

Once you cross a state’s threshold, you’ve established economic nexus. Registration and collection obligations begin either immediately or at the start of the following month or quarter.

When Economic Nexus Starts

Each state defines when obligations begin after crossing thresholds. Some require immediate registration. Colorado gives you 60 days. Louisiana requires registration before making your next sale. While most states offer roughly 30 days to register, collecting sales tax without a permit is illegal in most states and triggers additional penalties.

Monitoring sales by state becomes critical. Cross $100,000 in Minnesota during November, and you need to register, configure your sales tax software for Minnesota rates, begin collecting December 1st, and file your first return by January 20th. States rarely notify businesses when they’ve triggered nexus, so monitoring is your responsibility.

HOST’s nexus analysis service tracks your sales data, identifies exactly when you’ve crossed each threshold, and manages registrations so you remain compliant.

Physical Nexus vs Economic Nexus: Key Differences

Basis: Physical nexus requires tangible presence: offices, employees, inventory. Economic nexus requires only sales volume.

Geographic Reach: Physical nexus is limited. Economic nexus is unlimited. High-volume sellers often have economic nexus in 30+ states while maintaining physical nexus in only 2-3.

Thresholds: Physical nexus has no threshold. Any qualifying presence creates nexus. Economic nexus only triggers after exceeding specific thresholds.

Timeline: Physical nexus obligations begin when presence is established. Economic nexus obligations begin after crossing thresholds, with registration required within state-specific timeframes.

Monitoring: Physical nexus is straightforward. You know where your offices and employees are. Economic nexus requires continuous monitoring of sales data.

Why Both Types Matter for E-Commerce

Most e-commerce businesses eventually trigger both types across multiple states. An online retailer headquartered in Ohio with FBA inventory in five Amazon warehouses has physical nexus in six states. Selling $2 million annually across the U.S.? They likely have economic nexus in 20-30 additional states.

This creates complex obligations:

Registration: Each state requires separate registration with unique forms and processing times.

Collection: Sales tax rates vary by customer location, including state, county, city, and special district taxes across 13,000+ jurisdictions.

Filing: States assign filing frequencies based on tax collected, with different deadlines and requirements.

Remittance: Collected taxes must be remitted according to each state’s schedule.

Missing nexus in even one state creates risk. If you’ve been selling into a state where you have nexus but haven’t collected, you may owe back taxes, penalties, and interest potentially covering multiple years. Getting caught can mean back taxes with interest, penalties starting at 10% of unpaid tax in some states, and costly audits spanning multiple years. States have become increasingly aggressive in pursuing remote sellers since Wayfair.

Common Nexus Scenarios That Surprise Businesses

Amazon FBA Creates Physical Nexus Everywhere They Store Your Inventory

Amazon distributes your inventory across their fulfillment network. You ship products to one warehouse, but Amazon moves them to 5-10 facilities nationwide. Each location creates physical nexus.

Many FBA sellers discover years later they’ve had nexus in a dozen states but never collected tax. States pursue back taxes aggressively.

Remote Employees Trigger Physical Nexus

Hiring a remote customer service representative in Florida while your business operates from New York creates physical nexus in Florida. A contractor running Facebook ads from Texas creates nexus there.

Crossing Economic Nexus Mid-Year Creates Immediate Obligations

You launched an aggressive campaign in Q3. Sales jumped 300%. Suddenly you’ve crossed thresholds in 15 states you weren’t monitoring. Each state has different registration deadlines.

Failing to register immediately can mean you owe tax you didn’t collect, leading to paying out of pocket plus penalties.

How to Determine Where You Have Nexus

Conduct a Comprehensive Nexus Study

Analyze your complete footprint: offices, warehouses, employees, contractors, inventory locations, and any temporary presence.

Pull sales data by state for current and prior calendar years. Compare against each state’s economic nexus thresholds. Identify everywhere you’ve exceeded limits.

Document everything. States may challenge your determination during audits.

Monitor Ongoing Changes

Nexus isn’t static. Opening a warehouse creates physical nexus. Growing sales crosses new thresholds. Hiring remote employees adds states. Monthly monitoring prevents surprises.

Consider Voluntary Disclosure Agreements

If you discover nexus after already owing back taxes, Voluntary Disclosure Agreements (VDAs) can limit lookback periods and abate penalties. Most states offer VDA programs that significantly reduce liability compared to audits.

HOST’s VDA services help businesses come forward voluntarily, negotiate favorable terms, and resolve past obligations with minimal penalties.

HOST: Your Partner for Nexus Compliance

Determining where nexus exists is just the beginning. Registration, collection setup, ongoing filings, and notice management create constant operational burden.

What HOST Delivers

Nexus Analysis: We analyze your complete footprint (physical presence and sales data) to determine exactly where you have nexus obligations across all 45 sales tax states.

Sales Tax Registration: We handle registrations in every applicable state, managing paperwork, follow-up, and state communications.

Sales Tax Filing: We file your returns monthly, quarterly, or annually based on each state’s requirements, keeping everything current.

Sales Tax Software Integration: We optimize your TaxJar, Avalara, or other automation tools to calculate rates correctly and prevent costly errors.

Notice Management: We interpret and respond to state notices, protecting you from penalties while resolving problems efficiently.

Audit Defense: We’re your trusted partner in resolving audits, organizing documentation, and defending your position.

We’ve focused exclusively on sales tax for over 25 years. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce businesses of all sizes.

Ready to Get Nexus Right?

Understanding physical nexus vs economic nexus determines where you owe sales tax. Getting it wrong means either missing obligations that create audit risk or over-collecting unnecessarily.

Whether you’re trying to determine where nexus exists, overwhelmed by multi-state registration requirements, or uncertain whether your current setup covers all obligations, professional guidance eliminates guesswork and prevents costly mistakes.

At HOST, we combine deep nexus expertise with 25+ years of specialized experience. You handle the sales, we handle the tax.

Contact HOST today to discuss your nexus situation or schedule a free consultation. Let us determine exactly where you have obligations and manage compliance across every state.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What’s the difference between physical nexus and economic nexus?

Physical nexus requires tangible presence in a state. Offices, warehouses, employees, or inventory. Economic nexus requires only sales volume exceeding state-specific thresholds, typically $100,000-$500,000 annually, with no physical presence necessary.

Do I need to collect sales tax in states where I only have economic nexus?

Yes. Once you exceed a state’s economic nexus threshold, you must register for a sales tax permit and begin collecting tax from customers in that state, regardless of physical presence.

How do I know if I’ve crossed economic nexus thresholds?

Track your sales by state monthly or quarterly. Compare totals against each state’s threshold. Most use $100,000 in sales, though California and Texas require $500,000. Once you exceed a state’s threshold during the current or prior calendar year, you’ve established nexus.

Does having inventory in Amazon FBA warehouses create nexus?

Yes. Amazon distributes inventory across multiple fulfillment centers nationwide. Each location where they store your products creates physical nexus in that state, requiring registration and collection.

What happens if I discover I’ve had nexus but haven’t been collecting?

You may owe back taxes, penalties, and interest. Voluntary Disclosure Agreements (VDAs) allow you to come forward, limit lookback periods (often to 3-4 years instead of unlimited), and significantly reduce penalties compared to audits or enforcement actions.

Can I have nexus in a state where I’ve never visited?

Absolutely. Economic nexus means you can have sales tax obligations in states you’ve never physically visited, based solely on sales volume to customers in those states. This is the primary impact of the 2018 Wayfair decision.