Why do some states have no sales tax while you’re filing returns in 45 others? For e-commerce businesses navigating multi-state compliance, understanding Michigan sales tax nexus determines whether you’re collecting legally or building hidden liabilities.

Michigan requires collection once you cross $100,000 in sales or 200 transactions to Michigan customers in the previous calendar year. Either threshold triggers obligations. No physical presence required.

What catches sellers off guard? Amazon storing your inventory in Michigan creates instant nexus, regardless of sales volume. That Romulus fulfillment center just made you a Michigan taxpayer.

At Hands Off Sales Tax (HOST), we’ve managed Michigan nexus analysis and compliance since 1999. Whether you’ve just crossed thresholds or discovered past exposure requiring voluntary disclosure, we eliminate the complexity so you can focus on growth.

What Sales Tax Nexus Means

Nexus is the connection between your business and Michigan that creates tax obligations. Think of it as the trigger point where Michigan gains authority to require collection from your customers.

Multiple types exist: physical presence, economic activity, affiliate relationships, and referral arrangements. Each creates distinct obligations, and you can trigger nexus through any single pathway, or several simultaneously.

Wayfair changed everything. Before 2018, only physical presence mattered. Now, selling enough product into Michigan from anywhere triggers obligations.

Michigan’s Economic Nexus Threshold

Michigan established economic nexus October 1, 2018, immediately following Wayfair. The dual threshold: $100,000 in gross sales OR 200 separate transactions to Michigan customers in the previous calendar year.

Notice that “or.” Hit either threshold, and nexus exists. $105,000 in Michigan sales from 50 transactions? You must collect. $60,000 in sales from 210 transactions? Same obligation.

Michigan measures both thresholds against the previous calendar year. Your 2024 sales determine 2025 nexus status. If you exceed either threshold in 2024, you must register and begin collecting by January 1, 2025, regardless of your 2025 sales volume.

Critical detail: Michigan counts all sales delivered into the state, not just taxable sales. Even tax-exempt products count toward the $100,000 threshold.

Physical Nexus Still Matters

Economic nexus captures remote sellers, but physical nexus remains broader and immediate. Physical presence creates collection obligations regardless of sales volume.

Michigan considers these activities physical nexus:

- Inventory Storage: Warehousing products anywhere in Michigan, including FBA inventory at Amazon fulfillment centers in Romulus, Livonia, or Gaylord

- Employees or Contractors: Sales representatives, installers, or remote workers residing in Michigan

- Office or Retail Space: Any physical business location, even temporary

- Trade Shows and Events: Attending Michigan trade shows where you accept orders or make sales

- Property Ownership: Business equipment, vehicles, or real estate in Michigan

FBA inventory catches many sellers unprepared. Amazon determines where to store inventory, often distributing across multiple states for faster shipping. If Amazon places your products in Michigan fulfillment centers, you’ve established physical nexus even if you’ve never visited the state.

HOST’s nexus analysis examines your complete business footprint, identifying all physical presence factors creating obligations beyond economic thresholds.

Affiliate Nexus and Click-Through Nexus

Michigan recognizes two additional nexus types that catch multi-channel sellers off guard.

Affiliate Nexus exists when your business has relationships with Michigan-based entities performing activities on your behalf. You’re presumed engaged in Michigan retail sales if an affiliated person:

- Sells similar products under the same or similar business name

- Uses your trademarks, service marks, or trade names in Michigan

- Maintains offices, warehouses, or distribution facilities in Michigan to facilitate your sales

- Delivers, installs, or services your products for Michigan customers

Click-Through Nexus triggers when Michigan residents refer customers to you for commission. You establish nexus if:

- Cumulative gross receipts from all Michigan referral partners exceed $10,000 in the previous 12 months, AND

- Your total Michigan sales exceed $50,000 in the previous 12 months

This affects businesses working with Michigan-based bloggers, influencers, or affiliate marketers. That product review site generating referrals? It might create nexus obligations you didn’t anticipate.

Both affiliate and click-through nexus can be rebutted by demonstrating the activities aren’t significantly associated with your ability to establish or maintain a Michigan market. However, the burden of proof falls on you.

Trailing Nexus: When Obligations Continue

Here’s what sellers miss: nexus doesn’t disappear the moment your sales drop below thresholds.

Michigan enforces trailing nexus. Once established, nexus continues for the remainder of that month plus the following 11 months. You can’t simply stop collecting when sales decline.

Example: You exceed economic nexus thresholds in 2024 and register January 1, 2025. Your 2025 sales drop to $40,000, which is well below the $100,000 threshold. You must continue collecting and filing through all of 2025. Only after an entire calendar year (2025) passes below the threshold can you cease collection on January 1, 2026.

This protects against sellers manipulating collection obligations through strategic sales timing. It also means seasonal businesses experiencing temporary sales spikes face extended obligations beyond their high-volume periods.

When Amazon Collects for You

Michigan’s marketplace facilitator law, effective January 1, 2020, shifts collection responsibility to platforms like Amazon, eBay, Etsy, and Walmart.

When a marketplace facilitator collects Michigan sales tax on your behalf, you generally don’t register or file separately for those marketplace sales. The platform handles calculation, collection, remittance, and reporting.

However, complexity arises with multiple channels. Selling on Amazon (marketplace collects), your Shopify store (you collect), and wholesale to Michigan retailers (potentially exempt) requires tracking which sales create collection obligations.

Key considerations:

- Channel-Specific Registration: You may only need registration for sales through your website, not marketplace sales

- Hybrid Sales Tracking: Separate reporting for marketplace versus direct sales when filing returns

- Physical Nexus Complications: FBA inventory creates physical nexus, potentially requiring registration even when Amazon collects for marketplace sales

The interaction between marketplace facilitator laws and physical nexus creates confusion. Having FBA inventory in Michigan establishes physical nexus, but Amazon collects tax on Amazon sales. Still need to register? The safe answer: yes, for any sales outside the Amazon platform.

What Triggers Registration

Once you’ve established nexus through economic thresholds, physical presence, affiliate relationships, or referral arrangements, Michigan requires registration with the Department of Treasury.

You need a Michigan Treasury Online (MTO) account and must apply for a sales tax license. The application requires:

- Federal Employer Identification Number (FEIN)

- Business structure details (LLC, corporation, sole proprietorship)

- Estimated monthly sales volume

- NAICS code

- Responsible party information

Michigan doesn’t charge registration fees, but processing takes 2-4 weeks. You cannot legally collect Michigan sales tax until receiving your license number.

Alternative Registration Option: Michigan participates in the Streamlined Sales Tax (SST) program. If you’re registering in multiple SST member states, you can complete registration through the SST system rather than MTO. This streamlines multi-state registration and allows you to file Simplified Electronic Returns (SER) across all SST states from a single portal. For businesses with nexus in multiple states, this significantly reduces administrative burden.

Timing matters. The official rule: register by January 1st of the calendar year following the year you exceeded thresholds. Exceed thresholds in 2024, register by January 1, 2025 even if you haven’t made additional Michigan sales yet.

HOST handles Michigan registration completely. Applications, state follow-up, ensuring you receive your license without complications.

Michigan’s Rate and Sourcing

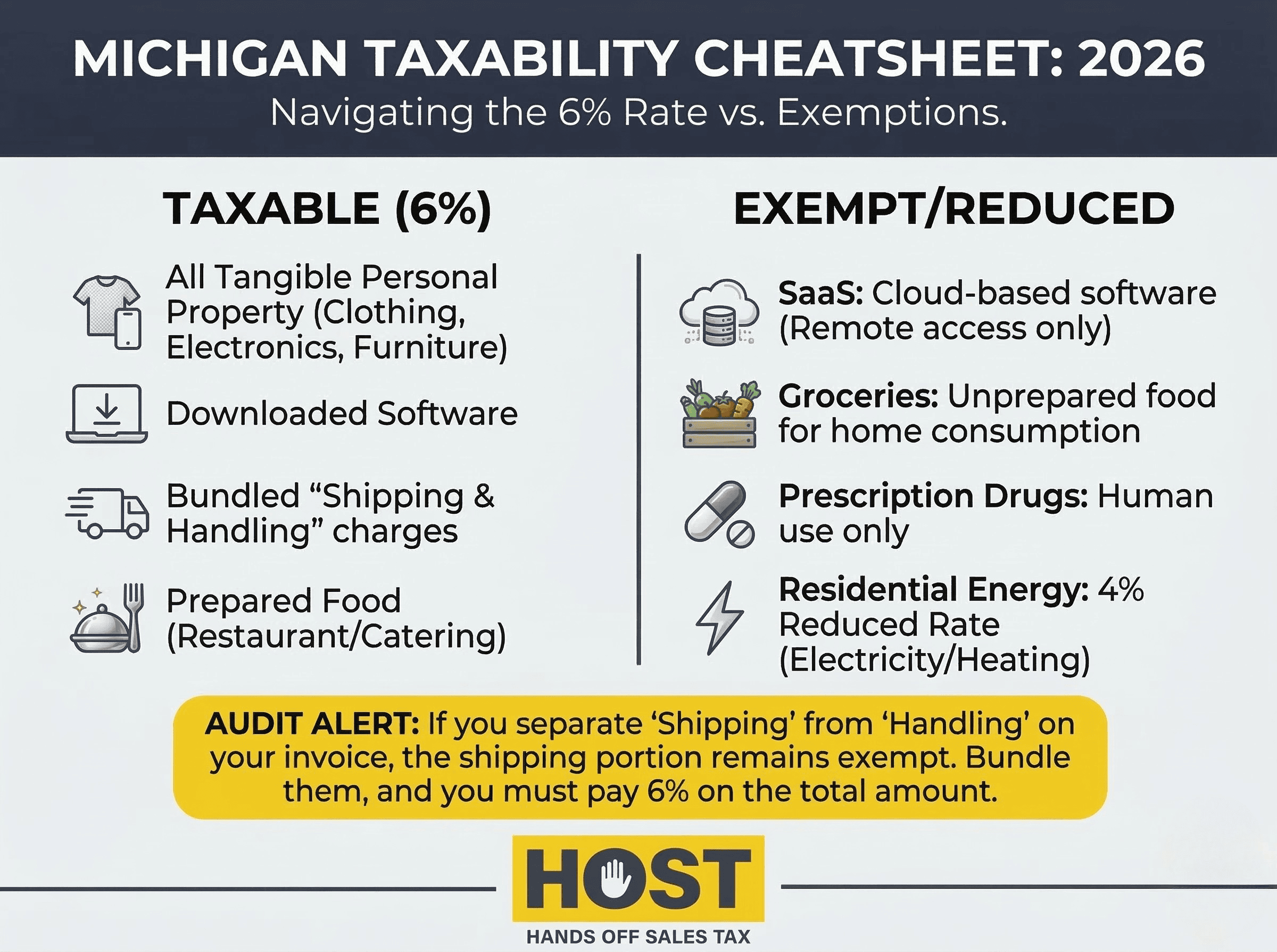

Michigan imposes 6% state sales tax with no local option taxes. This simplicity contrasts sharply with states where combined rates exceed 10%.

Every Michigan sale: exactly 6%. No county add-ons, no city surcharges, no special district taxes.

Exception: Natural or artificial gas, electricity, and home heating fuels for residential use face a reduced 4% rate. If you sell energy products for residential consumption, applying the standard 6% rate creates overcharges.

Michigan uses destination-based sourcing. The rate and rules depend on where the customer receives the product (their shipping address) not your business location.

Product Taxability in Michigan

Most tangible personal property sold in Michigan is taxable at 6%. This includes clothing, electronics, furniture, books, and general merchandise.

Key exemptions:

- Groceries: Most food for human consumption purchased for off-premises consumption

- Prescription Medications: Drugs prescribed by licensed physicians

- Manufacturing Equipment: Qualified industrial processing equipment (requires documentation)

Services in Michigan are generally not taxable unless specifically enumerated. However, when services include tangible personal property transfer, the transaction might become taxable.

Software as a Service (SaaS) and digital products present complexity. Michigan generally doesn’t tax cloud-based software access, but downloaded software is taxable. The distinction: if customers receive possession (download), it’s taxable; if they only access remotely (SaaS), it’s not.

Shipping Charges: Separately stated shipping isn’t taxable if the sale itself isn’t taxable. For taxable sales, shipping becomes taxable only if included in product price or not separately stated.

Filing Frequency and Deadlines

Michigan assigns filing frequency based on tax liability:

- Monthly Filers: Businesses remitting more than $720 annually (most active sellers)

- Quarterly Filers: Businesses remitting $45-$720 annually

- Annual Filers: Businesses remitting less than $45 annually (rare for nexus-triggering sellers)

Returns are due by the 20th day of the month following the reporting period. Monthly returns for January sales: due February 20. Quarterly returns for Q1 (January-March): due April 20.

Important: Even monthly and quarterly filers must file an annual reconciliation return by February 28 of the following year using Form 5081. This reconciles estimated payments with actual tax liability for the previous year.

Accelerated Filer Rules: Businesses averaging $720,000+ in annual sales tax must follow accelerated payment schedules. You must prepay 75% of the lesser of the previous month’s liability or the same period from the previous year by the 20th of the current month. Remaining balance due by the 20th of the following month. Electronic payment required.

Michigan requires electronic filing through the MTO portal. The state doesn’t accept paper returns for sales tax.

Late filing penalties: 5% of tax due, plus additional 5% for each month late, up to 25% maximum. Interest accrues at statutory rate from original due date.

Even owing zero tax requires filing returns. Failing to file zeros creates compliance gaps triggering notices or penalties.

HOST manages all Michigan filing deadlines! Monthly, quarterly, or annually, ensuring accurate, timely returns with proper documentation for every period.

Voluntary Disclosure for Past Obligations

Discovered you should have collected Michigan sales tax for the past two years? Voluntary Disclosure Agreements (VDAs) can limit exposure.

Michigan’s VDA program allows businesses to come forward voluntarily, disclosing past obligations in exchange for:

- Limited Lookback Period: Typically 4 years instead of Michigan’s 10-year statute of limitations

- Penalty Waiver: Michigan generally waives penalties for businesses voluntarily disclosing

- Structured Payment Plans: Ability to pay back taxes over time in some cases

The key requirement: you must come forward before Michigan contacts you. Once the state initiates contact through audit letter or notice, VDA benefits disappear.

VDAs particularly benefit businesses that:

- Established nexus through FBA without realizing it

- Crossed economic thresholds but didn’t know requirements

- Operated under incorrect advice about nexus obligations

- Triggered affiliate or click-through nexus unknowingly

HOST prepares and files VDAs with Michigan, negotiating optimal terms while protecting your business from maximum exposure.

Common Michigan Nexus Mistakes

Assuming FBA Doesn’t Create Nexus: The most common error. Amazon distributing your inventory to Michigan fulfillment centers creates physical nexus immediately.

Ignoring Affiliate and Click-Through Nexus: Believing only physical presence and economic activity matter, while Michigan-based referral partners or affiliated entities create separate obligations.

Counting Only Taxable Sales Toward Thresholds: Michigan’s $100,000 threshold includes all sales delivered into the state, regardless of taxability.

Stopping Collection When Sales Drop: Not understanding trailing nexus means sellers incorrectly stop collecting before the required 12-month period passes.

Missing the 4% Residential Energy Rate: Energy product sellers applying the standard 6% rate instead of the 4% residential rate.

Ignoring Annual Reconciliation Requirements: Monthly and quarterly filers missing the February 28 annual return deadline.

Each mistake creates audit exposure, potential back taxes, penalties, and interest. The cumulative effect can devastate small businesses operating on thin margins.

HOST: Your Michigan Nexus Partner

Michigan sales tax compliance requires understanding economic thresholds, physical presence rules, affiliate relationships, click-through nexus, marketplace facilitator complications, trailing nexus periods, and product-specific taxability. Managing it internally diverts time from growth while risking costly errors.

What HOST Delivers for Michigan Compliance:

- Nexus Analysis: We examine your Michigan sales, FBA inventory locations, affiliate relationships, and referral arrangements to determine exactly when you triggered nexus

- Sales Tax Registration: We complete your Michigan Treasury application (including SST registration if beneficial), handle follow-up, and ensure you receive your license

- Monthly/Quarterly Filing: We prepare and file all Michigan returns, including zero returns and annual reconciliation, maintaining perfect compliance

- Taxability Review: We determine correct tax treatment for your specific products under Michigan law, including the 4% residential energy rate

- Notice Response: We interpret and respond to Michigan Treasury notices, resolving issues before they escalate

- Audit Defense: We represent your business in Michigan audits, organizing documentation and defending your position

- VDA Preparation: We file voluntary disclosures to limit lookback and eliminate penalties for past obligations

Co-founded in 1999 by Mike Espenshade, HOST has focused exclusively on sales tax for over 25 years. Through parent company TaxMatrix, we’ve served North America’s largest companies. Now we bring that expertise to e-commerce sellers of all sizes.

You handle the sales, we handle the tax.

Ready to Get Michigan Compliant?

Michigan sales tax nexus creates obligations through multiple pathways: economic thresholds, physical presence, affiliate relationships, and referral arrangements. Whether crossing economic thresholds for the first time, managing FBA inventory complications, discovering affiliate nexus exposure, or learning about past obligations requiring VDA resolution, the right partner ensures compliant operations without draining your time.

At HOST, we combine deep Michigan expertise with 25+ years of specialized experience, transparent communication, and personalized support. Every aspect of Michigan compliance from comprehensive nexus analysis through monthly filing becomes our responsibility, freeing you to focus on growing your business.

When you’re ready to eliminate Michigan sales tax complexity, we’re ready to help. Contact HOST today to discuss your Michigan nexus situation and discover how we handle the compliance so you can concentrate on sales.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the Michigan sales tax nexus threshold for remote sellers?

Michigan requires remote sellers to collect sales tax once they exceed $100,000 in gross sales or 200 separate transactions to Michigan customers in the previous calendar year. Either threshold creates nexus, so you don’t need to meet both. If you exceed thresholds in 2024, you must register and begin collecting by January 1, 2025.

Does FBA inventory in Michigan create nexus?

Yes. If Amazon stores your inventory in Michigan fulfillment centers, you’ve established physical nexus regardless of sales volume. This creates immediate collection obligations for all Michigan sales, including those outside Amazon.

What is click-through nexus in Michigan?

Click-through nexus triggers when Michigan residents refer customers to you for commission, and your cumulative gross receipts from all Michigan referral partners exceed $10,000 in the previous 12 months while your total Michigan sales exceed $50,000. This affects businesses working with Michigan-based bloggers, influencers, or affiliate marketers.

How long does Michigan nexus last after my sales drop below thresholds?

Michigan enforces trailing nexus. Once established, nexus continues for the remainder of that month plus the following 11 months. You must continue collecting and filing until an entire calendar year passes in which you don’t meet either threshold. Only then can you cease collection.

When do marketplace facilitators collect Michigan sales tax for me?

Marketplace facilitators like Amazon, eBay, and Etsy collect and remit Michigan sales tax for transactions processed through their platforms. However, this doesn’t cover sales through your own website, wholesale transactions, or other direct channels. You must collect for those separately.

What happens if I’ve been selling to Michigan without collecting tax?

You’ve created back-tax liability for uncollected amounts, plus penalties and interest. Michigan’s Voluntary Disclosure Agreement program can limit the lookback period to 4 years and waive penalties if you come forward before the state contacts you. HOST prepares VDAs to minimize exposure and structure favorable terms.