Is sales tax direct or indirect? For e-commerce businesses navigating multi-state compliance, this isn’t academic, it’s the key to understanding why nexus rules exist, why states can hold you liable for uncollected tax, and what obligations you actually carry.

Sales tax is an indirect tax. The consumer pays it, but businesses collect and remit it to government agencies. You’re the intermediary in a three-party transaction you didn’t choose to join.

That’s where Hands Off Sales Tax (HOST) brings clarity. We’ve spent 25+ years managing the complexities of indirect tax compliance so businesses can focus on growth instead of decoding tax classifications.

What Makes a Tax “Direct” vs. “Indirect”?

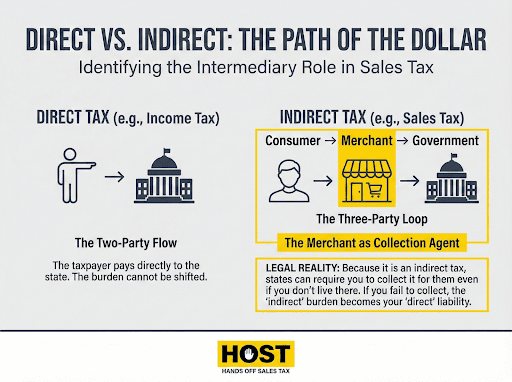

Direct taxes hit the person they’re imposed on. You can’t shift the burden. Income tax? You earn it, you pay it, you file your own return. Property tax works the same way. The owner pays directly to the taxing authority.

Indirect taxes are collected from consumers by an intermediary, then remitted to the government. The business collects but doesn’t bear the economic burden. You’re a collection agent for the state.

When you buy a $100 item with 8% sales tax, you pay $108. The retailer keeps $100 and sends $8 to the state. You bore the burden. The retailer merely facilitated collection.

This intermediary role creates unique compliance obligations. You must register, collect correct amounts, maintain records, file returns, and remit funds, all for a tax you don’t actually pay.

Why This Constitutional Structure Matters

The U.S. Constitution’s distinction between direct and indirect taxes dates to Article I, Section 9. The 16th Amendment (1913) addressed direct income taxes, but indirect taxes like sales tax remained state-controlled, explaining today’s 45-state patchwork where 13,000+ jurisdictions set their own rates.

This framework explains why the U.S. uses sales tax instead of VAT like most developed nations. VAT’s multi-stage collection would require federal coordination that conflicts with states’ rights, creating the compliance complexity businesses face today.

Why Sales Tax Is Classified as Indirect

The Consumer Bears the Economic Burden

Sales tax appears as a separate line item on receipts. This transparency makes the burden explicit—customers pay this tax, not stores.

A household spending $50,000 annually in a jurisdiction with 7% sales tax pays approximately $3,500 over the year. That’s real reduced consumption capacity. Businesses don’t lose purchasing power from sales tax on items they sell, they collect and pass it along.

Businesses Act as Collection Agents

States designate retailers as collection agents, deputizing them to gather revenue on government’s behalf. Instead of collecting small amounts from millions of consumers, states collect aggregated amounts from far fewer businesses.

When you fail to collect where required, you create liability. Often the state holds your business responsible for uncollected tax even when customers didn’t pay it.

Collection Occurs at Point of Transaction

Unlike direct taxes where taxpayers file annual returns, indirect taxes collect automatically at each transaction. For businesses, this means ongoing obligations. Managing thousands of transactions, tracking nexus thresholds across states, and filing monthly or quarterly returns in numerous jurisdictions.

HOST handles this burden through our comprehensive filing services, ensuring every jurisdiction receives correct remittances on time.

Why This Classification Matters for E-Commerce

You’re Responsible Even Though You Don’t Pay

States hold you liable for uncollected tax. If you fail to collect in states where you have nexus, states can assess you for the tax (plus penalties and interest) even though customers were supposed to pay it.

Real Business Scenario: TechGear LLC, a $2M e-commerce seller, believed sales tax was “the state’s problem.” When Texas audited them after three years of uncollected tax, the indirect classification meant Texas held TechGear liable, not their customers.

Assessment: $87,000 in back taxes plus $21,750 in penalties. The indirect nature made the business legally responsible for a tax they thought consumers owed.

Nexus Rules Exist Because It’s Indirect

Economic nexus works because sales tax is indirect. Since tax is levied on consumers (not businesses), states can require remote sellers to collect it as agents of the state where consumers reside.

Currently, 45 states impose sales tax, with most having economic nexus thresholds around $100,000 in annual sales. Notable exceptions include California ($500,000), Texas ($500,000), and New York ($500,000 plus 100 transactions). Connecticut and New York require BOTH revenue and transaction thresholds.

HOST’s nexus analysis service determines exactly where you’ve met thresholds, ensuring you’re collecting in the right jurisdictions.

Administrative Burden Falls on Business

The indirect nature means businesses handle all compliance work for a tax consumers owe. You must monitor sales across jurisdictions, register for permits, calculate correct rates for thousands of jurisdictions, collect appropriate amounts, maintain detailed records, file returns, remit funds on time, and respond to notices and audits.

The average company spends 30+ hours monthly on sales tax compliance. For lean e-commerce operations, this diverts resources from revenue-generating activities.

Software Helps but Isn’t Enough

Sales tax automation tools calculate rates and generate filing data, but require proper configuration. Common mistakes include charging tax on wholesale transactions meant for resale, double-taxing when multiple sales channels overlap, treating exempt items as taxable, and missing local district taxes beyond state rates.

HOST offers a Free Sales Tax Software Review to audit your configuration and identify errors before they create problems.

The Marketplace Facilitator Complication

Marketplace facilitator laws, now in all 45 sales tax states, add another layer of indirect tax complexity.

When you sell on Amazon or eBay, the platform collects and remits sales tax on those transactions. But if you also sell direct (your own website), you may still need separate registrations. The platform handles marketplace sales, but you’re responsible for direct sales.

Marketplace sales often count toward your nexus threshold even though the platform collects tax. Your total sales (marketplace plus direct) determine when you cross the $100,000 threshold. Cross it, and you’re required to register and collect on your direct sales.

This split responsibility exemplifies how indirect tax classification creates complex multi-party compliance scenarios.

Why Use Tax Proves the Point

When businesses don’t collect sales tax (no nexus), consumers legally owe “use tax” directly to their state, which is essentially self-reporting and paying sales tax themselves. This makes use tax a direct tax on consumers.

The result? Voluntary compliance rates under 2%. Consumers simply don’t pay taxes they’re supposed to calculate and remit themselves.

This reality drives states’ aggressive economic nexus enforcement. They’ve learned that indirect collection through businesses works, while direct collection from consumers doesn’t. The indirect nature of sales tax isn’t just a classification, it’s the entire enforcement mechanism.

Real-World Implications

State Revenue Stability

Indirect taxes like sales tax generate more reliable revenue than direct taxes. Economic downturns reduce income tax collections as earnings fall, but consumption remains relatively stable. This stability makes sales tax attractive to states, comprising 30-40% of total revenue.

Consumer Behavior Impact

Because indirect taxes feel “optional,” meaning consumers can avoid them by not buying, voters often accept higher rates than they would for direct income taxes. Combined state and local sales tax can exceed 10% in Louisiana, Tennessee, and Arkansas, yet these voters fiercely resist income tax increases.

This psychological distance explains why states prefer indirect taxation. It generates revenue with less political resistance.

Compliance Complexity Drives Professional Services

Because businesses handle obligations for a tax they don’t pay, many outsource compliance entirely. HOST provides end-to-end services such as nexus analysis, registration, filing, notice management, and audit defense, allowing businesses to completely offload sales tax obligations.

We file your returns across all jurisdictions so you stay compliant without spending dozens of hours monthly on unprofitable administrative work.

HOST: Managing Indirect Tax Compliance

Sales tax might be indirect, but the compliance burden on your business is direct. States expect accurate collection, timely filing, and complete records.

What HOST Delivers:

- Nexus Analysis: We determine exactly where you’ve triggered collection obligations across all 45 sales tax states

- Sales Tax Registration: We handle registrations in all required states, managing paperwork and state communications

- Ongoing Filing: We prepare and file returns across all jurisdictions. Monthly, quarterly, annually

- Notice Management: We interpret and respond to state notices, resolving issues before they become penalties

- Audit Defense: We’re your trusted partner in resolving sales tax audits

- Voluntary Disclosure Agreements: We file VDAs to limit lookback periods and abate penalties

We’ve been 100% focused on sales tax since 1999. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

Ready to Hand Off Your Indirect Tax Obligations?

Sales tax is indirect, but the compliance burden on your business is anything but. Every hour spent researching nexus rules, calculating rates, filing returns, or responding to notices is an hour not spent growing revenue.

Contact us today to discuss your sales tax needs or schedule a free consultation. Let us handle the indirect tax complexity so you can focus on direct revenue growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Is sales tax a direct or indirect tax?

Sales tax is an indirect tax. Consumers pay it, but businesses collect it as intermediaries and remit to state and local governments. The business doesn’t bear the economic burden, the consumer does, making it indirect by definition.

What’s the main difference between direct and indirect taxes?

Direct taxes are paid directly by the person or entity they’re imposed on (income tax, property tax). Indirect taxes are collected from consumers by an intermediary business, which remits funds to the government (sales tax, excise tax). The key distinction is whether the taxpayer can shift the burden.

Why does it matter that sales tax is indirect?

The indirect classification explains why businesses must comply with nexus rules even without physical presence, why states can hold businesses liable for uncollected tax, and why administrative burden falls on businesses for a tax consumers owe.

Can states hold my business responsible for sales tax my customers didn’t pay?

Yes. Because you’re designated as a collection agent, states can assess your business for uncollected sales tax in jurisdictions where you have nexus, even if customers were supposed to pay it. This creates significant financial risk.

What’s the relationship between indirect tax and economic nexus?

Economic nexus works because sales tax is indirect. Since tax is levied on consumers (not businesses), states can require remote sellers to collect it as agents of the state where consumers reside. If sales tax were direct, states couldn’t impose obligations on out-of-state businesses without physical presence.

How do marketplace facilitator laws affect my indirect tax obligations?

Even though platforms like Amazon collect tax on marketplace sales, you may still need separate registrations if you also sell direct. Marketplace sales often count toward your nexus threshold, and you’re responsible for collecting tax on all non-marketplace sales once you cross state thresholds.