What is Suffolk County sales tax, and why does it matter for your business? If you’re selling to customers in Long Island’s eastern reaches, understanding this combined rate structure means the difference between compliant operations and costly audit surprises.

Suffolk County sales tax combines New York State’s 4% base rate with county and local additions, creating an 8.75% total effective March 1, 2025 (increased from 8.625%). For e-commerce sellers, crossing economic nexus thresholds in New York triggers collection obligations, and Suffolk County’s current rate applies to every customer from Montauk to Huntington. Hands Off Sales Tax (HOST) handles nexus analysis, registration, filing, and ongoing compliance so you can focus on growth.

What Is Suffolk County Sales Tax?

Suffolk County sales tax is the combined rate charged on retail transactions within Suffolk County, New York. Located on Long Island’s eastern portion, Suffolk County encompasses towns from Babylon and Huntington in the west to the Hamptons and Montauk in the east—covering approximately 1.5 million residents across 912 square miles.

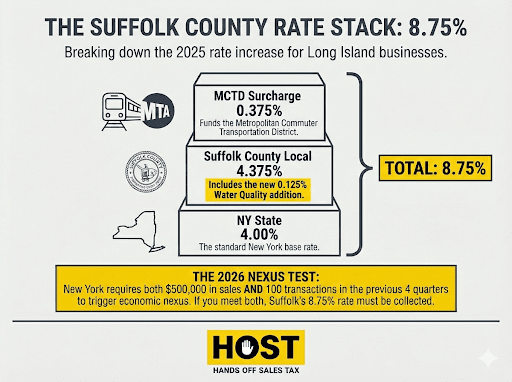

As of March 1, 2025, the total Suffolk County sales tax rate is 8.75%, composed of three layers:

- New York State: 4%

- Suffolk County: 4.375% (increased from 4.25%)

- Metropolitan Commuter Transportation District (MCTD): 0.375%

This combined rate applies uniformly throughout Suffolk County. Unlike some New York counties where individual municipalities add their own sales taxes, Suffolk County maintains a single rate across all towns and villages, you don’t need address-level validation within the county.

The 8.75% rate places Suffolk County among New York’s higher-tax jurisdictions, though it remains below New York City’s 8.875% rate. For context, neighboring Nassau County currently charges 8.625%.

For businesses, every taxable sale to a Suffolk County customer requires collecting $8.75 per $100 of merchandise. On a $1,000 purchase, that’s $87.50 in sales tax remitted to New York State.

Why Did Suffolk County Increase Sales Tax?

Understanding the reason behind the March 2025 increase provides important context for businesses operating in the region. Suffolk County voters overwhelmingly approved Proposition 2 in November 2024 with over 71% support, authorizing the 0.125% sales tax increase to fund critical water quality restoration initiatives.

The additional revenue generates an estimated $49 million annually starting in 2026, totaling $3 billion by 2060. These funds directly support Suffolk County’s Water Quality Restoration Act, addressing decades of nitrogen pollution, protecting vital aquifers, and modernizing wastewater infrastructure throughout the county.

For businesses, this voter-approved increase reflects long-term community investment in environmental sustainability, expanding sewer systems, reducing reliance on aging septic systems, and revitalizing Suffolk County’s bays, harbors, and groundwater. The initiative also unlocks economic development opportunities in downtown districts that have experienced stagnation due to inadequate wastewater infrastructure.

Breaking Down the Combined Rate Structure

New York State Base Rate: 4%

Every New York jurisdiction starts with the 4% state rate, funding statewide programs: education, infrastructure, public safety, healthcare. New York collected approximately $16.8 billion in state sales tax during fiscal year 2023.

The state rate applies to most tangible personal property and certain services. New York exempts groceries, prescription medications, residential utilities, and clothing under $110 per item.

Suffolk County Local Rate: 4.375%

Suffolk County adds 4.375% on top of the state base, funding county services: law enforcement, social services, parks, and roads. On March 1, 2025, Suffolk County increased this rate from 4.25% to 4.375%. The 0.125% increase approved by voters for water quality restoration.

MCTD Surcharge: 0.375%

The Metropolitan Commuter Transportation District (MCTD) surcharge funds the Metropolitan Transportation Authority (MTA), supporting subway, bus, and commuter rail operations. Suffolk County falls within the MCTD because the Long Island Rail Road (LIRR) serves the county extensively.

What Products and Services Are Taxable in Suffolk County?

Understanding what triggers sales tax collection prevents costly mistakes. In Suffolk County, most tangible personal property is taxable at the full 8.75% rate.

Taxable Items:

- Clothing and footwear over $110 per item

- Electronics, furniture, appliances

- Restaurant meals and prepared foods

- Hotel accommodations (subject to 8.75% sales tax PLUS 5.5% county occupancy tax)

- New in 2025: Short-term rental occupancy (under 30 days) is now subject to sales tax, collected by booking services or operators

Exempt Items:

- Groceries (unprepared food for home consumption)

- Prescription medications and residential utilities

- Clothing and footwear under $110 per item

- Residential energy sources and services (these remain at the previous 8.625% rate and were not subject to the March 2025 increase)

Special Rules: Software as a Service (SaaS) is generally taxable in New York when users access software remotely. The clothing exemption creates particular complexity—items under $110 are exempt, but items over $110 are fully taxable on the entire amount.

For e-commerce sellers, product categorization becomes critical. Miscategorizing exempt items as taxable means overcharging customers. Miscategorizing taxable items as exempt creates audit liability.

Economic Nexus and Suffolk County Sales Tax Obligations

Physical presence in Suffolk County isn’t required to trigger collection obligations. New York’s economic nexus law requires remote sellers to collect sales tax once they exceed specific thresholds.

New York Economic Nexus Thresholds:

- $500,000 in gross receipts from New York sales, AND

- More than 100 transactions to New York customers

- In the current or immediately preceding four sales tax quarters

Both conditions must be met. Once you exceed both thresholds, registration becomes mandatory.

New York’s thresholds are higher than most states (which typically use $100,000 in sales OR 200 transactions). However, New York’s large population means businesses often cross these thresholds without realizing it.

HOST’s nexus analysis service examines your sales data across all states and jurisdictions, identifying exactly where you’ve met thresholds and what registration obligations exist.

How to Register and File in New York

Once nexus exists, registration with the New York State Department of Taxation and Finance becomes mandatory. The process requires obtaining a Certificate of Authority, providing business information, and determining your filing frequency based on expected tax liability.

Filing deadlines in New York fall on the 20th of the month following the reporting period. Quarterly filers must file by April 20, July 20, October 20, and January 20.

Penalties for late filing are significant: 10% of tax due for returns filed within 60 days, increasing to 30% for returns filed more than 60 days late. Interest accrues at New York’s statutory rate.

HOST handles the entire registration and filing process. From initial Certificate of Authority applications to ongoing filings across all your nexus states.

Common Suffolk County Sales Tax Mistakes

Mistake 1: Collecting Outdated Rates Since March 1, 2025, Suffolk County’s rate has been 8.75%, not 8.625%. Businesses still collecting at the old rate are undercollecting, creating audit liability. On $100,000 in sales, that’s $125 in uncollected tax you’ll owe the state.

Mistake 2: Applying Wrong Rates to Special Categories The $110 clothing exemption threshold confuses sellers. Items under $110 are exempt, but items over $110 are fully taxable on the entire amount. Residential energy sources remain at 8.625%, not 8.75%.

Mistake 3: Missing New 2025 Requirements Short-term rental operators must now collect sales tax on occupancy under 30 days. Hospitality businesses must collect both the 8.75% sales tax AND the separate 5.5% hotel occupancy tax.

Mistake 4: Ignoring Contractor Provisions Pre-existing lump sum construction contracts signed before December 17, 2024 may qualify for credits on the 0.125% rate difference. Contractors should track purchases accordingly and request refunds where applicable.

HOST: Your Partner for New York Sales Tax Compliance

Managing sales tax obligations across New York’s 62 counties creates complexity that drains time without generating revenue. Suffolk County represents just one piece of a larger compliance puzzle.

What HOST Delivers:

Nexus Analysis: We determine precisely where you’ve met New York’s $500,000 and 100-transaction thresholds, along with nexus in all other states.

Sales Tax Registration: We handle your New York Certificate of Authority application, managing all paperwork and state communications.

Sales Tax Filing: We prepare and file your New York returns, ensuring the 20th-of-the-month deadlines are always met.

Rate Management: We ensure your systems collect Suffolk County’s current 8.75% rate without manual updates.

Notice Management: When New York sends confusing notices, we interpret and respond appropriately to resolve issues before they escalate.

Audit Defense: If New York selects you for audit, we’re your trusted partner throughout the process.

Software Optimization: We review your TaxJar, Avalara, or other automation tools to identify costly mistakes.

We’ve been 100% focused on sales tax since 1999. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise-level expertise to e-commerce sellers of all sizes.

Ready to Simplify Suffolk County Sales Tax Compliance?

Understanding what Suffolk County sales tax is and how New York’s combined rate structure works is the first step. Implementing compliant collection, managing registration, filing on time, and responding to notices requires ongoing attention that diverts focus from revenue-generating activities.

Whether you’re crossing New York’s economic nexus thresholds, expanding into new states, or overwhelmed by managing compliance across dozens of jurisdictions, the right sales tax partner eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss your New York sales tax needs or schedule a free consultation. Let us handle the tax so you can focus on sales.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the sales tax rate in Suffolk County, New York?

The Suffolk County sales tax rate is 8.75% as of March 1, 2025, composed of New York State’s 4% rate, Suffolk County’s 4.375% local rate, and the 0.375% MCTD surcharge. This rate applies uniformly throughout the county, with exceptions for residential energy sources which remain at 8.625%.

Do I need to collect Suffolk County sales tax if I don’t have a physical location there?

Yes, if you’ve exceeded New York’s economic nexus thresholds: $500,000 in gross receipts from New York sales AND more than 100 transactions to New York customers in the current or preceding four sales tax quarters. Physical presence is not required.

Are clothing items taxed in Suffolk County?

Clothing and footwear under $110 per item are exempt from sales tax in Suffolk County. Items priced at $110 or above are fully taxable at the 8.75% rate on the entire purchase amount.

Why did Suffolk County increase its sales tax rate?

Suffolk County voters approved a 0.125% sales tax increase in November 2024 (Proposition 2) to fund the Water Quality Restoration Act. The increase generates $49 million annually for clean water infrastructure, sewer expansion, and addressing nitrogen pollution—a $3 billion investment through 2060.

What’s the difference between hotel occupancy tax and sales tax in Suffolk County?

Hotels in Suffolk County must collect both the 8.75% sales tax AND a separate 5.5% county occupancy tax on room rentals, totaling 14.25% in taxes on lodging. Short-term rentals under 30 days are now also subject to sales tax as of March 2025.

Does Suffolk County have different rates in different towns?

No. Suffolk County maintains a uniform 8.75% rate across all towns and villages within the county, simplifying compliance. You don’t need address-level validation within Suffolk County to determine the correct rate.