Is there sales tax on rental equipment? The answer shifts with every state line you cross. Equipment rental companies face a patchwork of rules. Some states tax rentals like retail sales, others exempt them entirely, and many apply special rates that depend on what you’re renting, how long you’re renting it, and who’s doing the renting.

Five states skip sales tax altogether: Alaska (at the state level), Delaware, Montana, New Hampshire, and Oregon. But “no sales tax” doesn’t mean “no complications.” Alaska’s 100+ local jurisdictions can impose their own taxes. Oregon hits businesses with a Corporate Activity Tax once revenue crosses $1 million.

For everyone else? It’s complicated.

Hands Off Sales Tax (HOST) specializes in untangling these multi-state knots. We analyze your rental activities, pinpoint where obligations exist, and handle compliance so you can focus on keeping equipment moving instead of decoding tax codes.

What Counts as Rental Equipment for Tax Purposes?

Rental equipment means tangible personal property leased temporarily rather than sold permanently. Construction equipment (excavators, scaffolding, lifts), party supplies (tents, tables, chairs), medical devices (hospital beds, mobility aids), tools, machinery, and audio-visual gear all qualify.

Tax treatment depends on rental duration, equipment type, and customer. Short-term daily rentals often face different rules than multi-year leases. Some states distinguish “true leases” from lease-purchase agreements where ownership eventually transfers.

The rental industry operates across state lines constantly. Equipment moves between job sites, customers operate in multiple jurisdictions, and determining where tax applies gets genuinely messy. A construction company based in Ohio renting equipment for a Texas project faces Texas tax rules, not Ohio’s.

How States Generally Tax Equipment Rentals

Most states treat equipment rentals as taxable transactions. Rent a forklift for $500 per week in a state with 7% sales tax? Your customer pays $535. You collect that $35 and send it to the state.

But “most” leaves plenty of room for exceptions. Equipment rental taxation exists in the majority of states with sales tax. The five states without sales tax. Delaware, Montana, New Hampshire, Oregon, and Alaska (at the state level), create their own wrinkles. Alaska allows over 100 local jurisdictions to tax rentals independently.

The taxability question often hinges on whether the state considers rentals a “service” or a “tangible personal property transaction.” States taxing tangible personal property typically tax its rental. States with narrow tax bases that primarily tax goods but exempt most services often exempt equipment rentals.

State-by-State: Where Rental Equipment Gets Taxed

States That Fully Tax Rentals

California taxes equipment rentals based on rental receipts. Combined state and local rates run 7.25% to 10.75% depending on location. Tax applies where equipment is primarily used.

Texas hits rentals at 6.25% state tax plus up to 2% local, covering construction equipment, tools, and party supplies. Special motor vehicle rental taxes apply to certain heavy machinery.

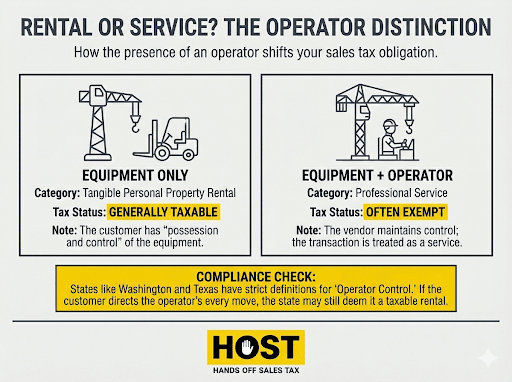

Florida charges 6% state tax plus county surtaxes. New York taxes rentals at 4% state rate plus local rates, but when equipment comes with an operator, it’s treated as a service instead of a rental, changing the tax treatment.

States With Partial Exemptions

Pennsylvania taxes general equipment rentals. Contractors must pay sales tax on rental payments. Pennsylvania’s Building Machinery and Equipment exemption under Act 45 applies to purchases by contractors working for tax-exempt entities, not rentals.

Illinois takes a unique approach, taxing equipment when rental companies acquire it rather than on each rental payment. Once the company pays tax on acquisition, rental receipts to customers often avoid additional tax.

Ohio taxes rentals but provides manufacturing exemptions for equipment used directly in manufacturing. Construction rentals remain taxable unless they qualify under specific manufacturing criteria.

No Sales Tax States

Oregon, Delaware, Montana, and New Hampshire impose no sales tax, making rentals tax-free. However, Oregon’s Corporate Activity Tax kicks in at $1 million in state revenue, creating different compliance obligations.

Alaska has no statewide tax but permits local taxation. Over 100 municipalities impose local sales taxes from 1% to 7%, and many tax rentals. Companies operating in Alaska must determine obligations jurisdiction by jurisdiction.

How to Calculate Sales Tax on Rental Equipment

The basic calculation is straightforward: Rental Amount × Tax Rate = Tax Due

Example: You rent a forklift for $800 weekly in a jurisdiction with 8.5% combined sales tax. $800 × 0.085 = $68 tax due. Customer pays $868 total.

The challenge is knowing which rate applies where, which customers qualify for exemptions, and how ancillary fees get treated. Address-level accuracy matters when rates vary by city block.

Industry-Specific Considerations

Construction Equipment

Construction equipment like excavators, bulldozers, cranes, scaffolding represents one of the largest rental categories. Most states tax these rentals fully, though treatment varies significantly.

The operator distinction creates a critical tax divide. States like Indiana, Michigan, Washington, and Idaho treat equipment rented with an operator as a service rather than a rental. Services often escape sales tax that rentals face. Rent a crane alone? Taxable. Rent the same crane with an operator? Often exempt. The line between taxable rental and non-taxable service can save (or cost) substantial money.

Medical Equipment

Many states exempt durable medical equipment rentals when prescribed by healthcare providers. Wheelchairs, hospital beds, oxygen equipment, and mobility aids often qualify as medical necessities.

States define “medical equipment” narrowly. A hospital bed prescribed by a doctor typically qualifies. A massage chair marketed for wellness likely doesn’t. Documentation requirements vary. Some states require prescriptions or medical necessity certificates.

Party and Event Equipment

Party rental equipment like tents, tables, chairs, linens, dinnerware, is almost universally taxable. Few states provide exemptions. Some allow exemptions when nonprofits rent equipment for exempt purposes, but rules are strict.

Geographic complications arise frequently. A party rental company in State A renting equipment for a State B event must determine which state’s rules apply, often based on where equipment is delivered and used.

Duration-Based Tax Differences

Many states distinguish short-term rentals from long-term leases. Short-term rentals (daily, weekly, monthly) typically face standard sales tax each period. Long-term leases may qualify for alternative treatment.

Some states treat leases exceeding certain thresholds (often six months or one year) as conditional sales rather than ongoing rentals, changing how and when tax applies.

Understanding these duration distinctions matters for rental companies with diverse offerings: daily tool rentals, monthly equipment leases, and multi-year machinery contracts may all face different tax treatment in the same state.

Common Rental Equipment Tax Mistakes

Misclassifying Long-Term Leases

Many rental businesses treat all transactions identically, collecting sales tax on every payment. However, long-term leases may qualify for different treatment. Failing to distinguish creates either overcollection (irritating customers) or undercollection (triggering audit liability).

Ignoring Delivery Location Rules

Companies often sign contracts at their business location but deliver equipment elsewhere. Most states tax based on where equipment is used, not where contracts are signed. A Pennsylvania rental company delivering to a Maryland job site must collect Maryland tax.

This creates nexus in delivery states. Once you exceed economic nexus thresholds through rental deliveries (typically $100,000 in sales or 200 transactions) registration and collection obligations kick in.

Failing to Track Exemption Certificates

Business customers claim exemptions like resale certificates, manufacturing exemptions, or agricultural exemptions. Accepting certificates without proper validation or retention creates audit risk. States require specific information, and many invalidate improperly completed forms.

Overlooking Local Taxes

State sales tax is just the beginning. Over 11,000 local taxing jurisdictions exist nationwide. Equipment delivered to one city may face different combined rates than equipment delivered five miles away. Address-level tax calculation becomes essential.

Not Understanding Ancillary Fee Treatment

Rental transactions often include charges beyond the base rental rate. Delivery fees, pickup charges, damage waivers, assembly, maintenance. These ancillary fees face different tax treatment depending on the state.

Some states tax delivery charges separately. Others tax them only when mandatory. Damage waivers are taxable in certain jurisdictions, exempt in others. Assembly and disassembly charges create similar confusion. Failing to properly classify these fees leads to either overcollection or audit exposure. The rules aren’t intuitive, and they vary by state.

Why Equipment Rental Companies Need Specialized Help

Equipment rental businesses face distinct compliance challenges. Equipment moves constantly between jurisdictions. Rental durations vary from hours to years. Customer types span individuals, businesses, contractors, and manufacturers, each potentially qualifying for different exemptions.

Tracking where equipment is used, which tax rates apply, when long-term lease rules activate, and which customers qualify for exemptions demands specialized expertise.

Many equipment rental companies operate in 20 or 30+ states. Each requires separate registration, ongoing filings, and jurisdiction-specific knowledge. The administrative burden quickly overwhelms internal resources.

State auditors scrutinize rental businesses carefully. Transactions are frequent, dollar amounts are high, and exemption certificate usage is common, creating multiple audit exposure points.

HOST: Equipment Rental Tax Compliance Made Simple

At Hands Off Sales Tax, we’ve spent over 25 years helping businesses navigate multi-state compliance. Equipment rental companies benefit from our specialized expertise in sourcing rules, exemption management, and industry-specific tax treatment.

What HOST Delivers:

Nexus Analysis: We analyze your rental footprint to determine where delivery activity, storage locations, or other factors created collection obligations. Equipment rental nexus goes beyond sales thresholds. Physical presence through storage yards or delivery vehicles triggers obligations regardless of sales volume.

Sales Tax Registration: We handle registrations in every applicable state and local jurisdiction, managing applications, follow-up communications, and ongoing filing requirements.

Ongoing Filings: We prepare and file returns monthly, quarterly, or annually in every jurisdiction based on their specific requirements and your sales volume. This includes state returns, local returns, and special district returns. You’ll never miss a deadline.

Exemption Certificate Management: We help implement systems to collect, validate, and retain exemption certificates. During audits, proper documentation is your primary defense.

Software Configuration: Equipment rental software often integrates with tax calculation tools. We review and optimize these configurations. Our Free Sales Tax Software Review identifies costly errors before they become audit issues.

Audit Defense: When state auditors question your rental tax treatment, exemption certificates, or sourcing decisions, we advocate. Organizing documentation, communicating with auditors, and defending your positions.

Through our parent company TaxMatrix, we’ve helped North America’s largest equipment rental companies manage compliance. Now we bring that enterprise expertise to small and mid-sized rental businesses.

Take Equipment Rental Tax Off Your Plate

Equipment rental taxation varies dramatically by state, equipment type, rental duration, and customer use. Managing compliance across jurisdictions while running your rental operation diverts time, creates stress, and exposes you to audit risk.

Professional tax management eliminates guesswork, prevents costly mistakes, and lets you focus on keeping equipment moving.

Whether you’re expanding into new states, concerned about exemption certificate validity, or overwhelmed by filing obligations, HOST provides the specialized expertise equipment rental companies need.

Ready to simplify compliance? Contact us today to discuss your multi-state obligations or schedule a free consultation. We’ll handle the tax so you can focus on growing your rental business.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book—many principles apply to equipment rental businesses navigating multi-state compliance.

Frequently Asked Questions

Is equipment rental subject to sales tax in most states?

Yes, most states treat equipment rentals as taxable transactions similar to retail sales. However, significant exceptions exist, and specific equipment categories often qualify for exemptions based on industry use or rental duration.

How do I know which state’s sales tax applies to my equipment rental?

Generally, sales tax applies where equipment is delivered and used, not where rental contracts are signed or where your business is located. If you deliver equipment to a Texas job site, Texas tax rules apply regardless of where your company is based.

Are construction equipment rentals taxed differently than other equipment?

Tax treatment varies significantly by state. Some states treat construction rentals like any other rental. Others provide special treatment depending on the customer type, project type, or whether an operator accompanies the equipment.

Do long-term equipment leases face the same tax treatment as short-term rentals?

Not necessarily. Many states distinguish between short-term rentals and long-term leases, sometimes treating leases exceeding six months or one year as conditional sales rather than ongoing rentals, significantly changing tax calculation and timing.

What happens if I collect the wrong amount of sales tax on equipment rentals?

Undercollecting creates audit liability. You remain responsible for unpaid tax plus penalties and interest. Overcollecting irritates customers and may require refunds. Either mistake creates administrative burden and relationship damage, making accurate calculation essential.

How do exemption certificates work for equipment rental customers?

Business customers may provide exemption certificates claiming the rental qualifies for resale, manufacturing, agricultural, or other statutory exemptions. You must collect, validate, and retain these certificates properly. During audits, invalid certificates mean you owe the uncollected tax.