Do contractors charge sales tax on labor in Washington State? The answer hinges on what you’re actually doing. Installing tangible property? That labor’s taxable. Improving real estate? Different story entirely.

For contractors expanding into Washington (or locals navigating the labyrinth) this distinction isn’t academic. It’s the difference between pricing correctly and facing audit assessments that make your quarterly estimates look like pocket change.

Hands Off Sales Tax (HOST) specializes in untangling Washington’s peculiar approach to contractor taxation while managing compliance across all 45+ sales tax states. From nexus analysis to automated filings, we handle the complexity so you can focus on the work that actually generates revenue.

Washington’s Fundamental Rule: Labor Is Usually Taxable

Washington operates under a principle that surprises contractors from other states: labor charges are generally taxable when they’re part of a retail sale involving tangible personal property.

The Washington Department of Revenue views most construction, installation, and repair activities as retail transactions subject to the state’s 6.5% sales tax rate (plus local taxes that can push combined rates to 10.6% in some jurisdictions). Unlike states where pure labor separates cleanly from materials, Washington often treats the entire transaction: labor, materials, overhead. Profit as a single taxable retail sale.

This stems from how Washington defines “retail sale” in RCW 82.04.050. The statute explicitly includes “the installing, repairing, cleaning, altering, imprinting, or improving of tangible personal property.” When you install materials, the labor becomes inseparable from the taxable transaction.

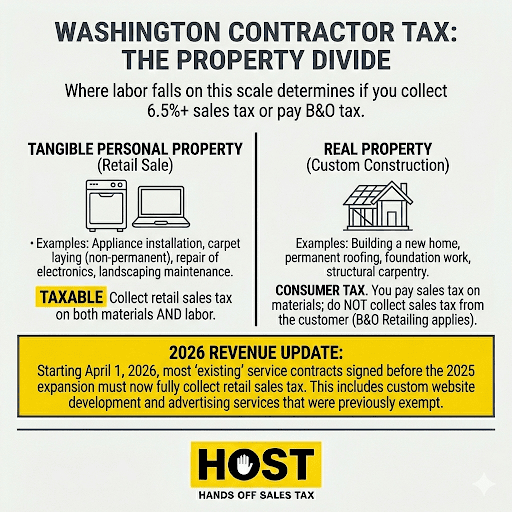

The Critical Question: Real Property or Tangible Property?

Washington’s treatment pivots on one distinction: Are you improving real property or installing tangible personal property?

Real property improvements receive different tax treatment. Construction, repair, or improvement work that becomes permanently affixed to land or buildings typically operates under B&O (Business & Occupation) tax rather than retail sales tax on the customer transaction.

Tangible personal property installations trigger retail sales tax. If you’re installing something that remains personal property, even if attached temporarily or semi-permanently, the entire charge including labor becomes taxable.

Consider these scenarios:

- Installing carpet: When sold and installed as a package, the entire charge including labor faces retail sales tax

- Installing a built-in dishwasher: Taxable retail sale with labor included

- Repairing a refrigerator: Labor charges are taxable alongside parts

Construction Contractors vs. Retail Contractors

Washington distinguishes between two contractor types:

Construction contractors working on real property improvements like building structures, pouring foundations, installing permanently affixed roofing, don’t charge sales tax to customers. Instead, they pay retail sales tax on materials they purchase and report revenue under B&O tax. HOST’s sales tax registration services help contractors determine which business activities require registration and handle applications across all applicable jurisdictions.

Retail contractors installing tangible personal property must collect retail sales tax from customers on the entire charge. Materials plus labor. This includes appliance installers, certain flooring contractors, security system installers, and others whose work doesn’t constitute real property improvement.

When Contractor Labor Is Taxable

Repair and Maintenance Services

Repair services involving tangible personal property are almost always taxable. If you’re fixing, maintaining, or restoring an item of tangible personal property, the labor charges plus any parts face retail sales tax.

Common taxable scenarios:

- Appliance repair: Refrigerators, washers, dryers, ovens, labor is taxable

- Computer repair: Hardware repairs and installations trigger sales tax on labor

- Vehicle repair: Auto mechanics charge sales tax on labor (with limited exceptions for farm vehicles)

- Furniture repair: Reupholstering, refinishing, or fixing furniture includes taxable labor

This catches many service providers by surprise, especially those operating in multiple states where the same work might be tax-free.

Installation Services

Installation labor is taxable when you’re installing tangible personal property for customers. The transaction combines the property and installation into a single retail sale.

Taxable installations include:

- Home theater systems: TVs, speakers, equipment, entire charge is taxable

- Security systems: Cameras, sensors, monitoring equipment trigger sales tax on labor

- Window treatments: Blinds, shades, shutters installed as tangible personal property

- Flooring installation: When sold retail with installation, labor becomes part of taxable sale

- Landscaping services: Lawn maintenance, planting, design work, all subject to retail sales tax

Even if a customer provides their own materials, the labor to install those materials remains a taxable service. The contractor charges sales tax on the labor-only amount.

The key question: Does the installed item become real property? Permanently affixed and losing its identity as personal property, or does it remain tangible personal property? If it remains personal property, installation labor is taxable.

Fabrication and Manufacturing

Custom fabrication where you’re creating tangible personal property for a customer creates retail sales tax obligations. The labor to fabricate, along with materials, becomes part of the taxable retail price.

When Contractor Labor May Be Exempt

Real Property Construction

Labor charges for real property construction or improvement typically don’t get charged to customers as retail sales tax. The contractor pays sales tax when purchasing materials and reports the transaction under B&O tax.

Real property improvements include building construction, roofing permanently affixed to structures, concrete foundations and driveways, and structural carpentry that becomes part of real property.

Public Works and Government Construction

Public road construction for federal, county, or city governments receives exemption from retail sales tax. Contractors working on public roads, bridges, or highways owned by municipal corporations don’t collect sales tax from government clients.

However, construction for the State of Washington itself remains subject to retail sales tax. An important distinction. Federal government construction projects also receive different tax treatment under government contracting rules.

Contractors on these projects pay sales tax when purchasing materials as consumers, but the overall transaction structure differs from standard retail construction.

Speculative Builders: The Major Exception

Speculative builders construct buildings on land they own with intent to sell the finished property. Unlike custom contractors, speculative builders don’t charge retail sales tax to the final buyer.

Instead, the builder operates as the consumer. Paying sales tax on all materials and subcontractor services when purchased. The final sale of the completed property falls under Real Estate Excise Tax (REET), not retail sales tax.

This distinction matters tremendously for tax treatment. A custom contractor building on a client’s land collects retail sales tax on the full contract price. A speculative builder constructing on their own land pays tax upfront on inputs but doesn’t collect from the buyer.

Professional Services Without Tangible Property Transfer

Pure professional services that don’t involve selling, installing, or transferring tangible personal property may avoid sales tax. However, this exemption is narrow in Washington.

The moment tangible personal property enters the transaction. Even digital goods in some cases, Washington’s retail sales tax likely applies.

The Materials vs. Labor Breakdown Trap

Many contractors separately state materials and labor on invoices, hoping to exempt the labor portion. This strategy fails in Washington when you’re engaged in retail sales of tangible personal property.

Washington’s administrative guidance makes clear that when labor is part of a retail sale, you cannot separately state it to avoid taxation. The entire charge: materials, labor, overhead, profit becomes the taxable retail selling price.

Separating charges for internal accounting or customer transparency is acceptable, but both components remain taxable when the transaction qualifies as retail sale of tangible personal property.

Contract Price Presumption

Washington law presumes any contract price doesn’t include sales tax unless explicitly stated otherwise. If your contract is silent on tax treatment, you must add the applicable sales tax on top of the agreed price. This makes clear contract language about tax treatment essential for both parties.

How Reseller Permits Work

Contractors performing custom construction can purchase materials that become permanent parts of the building without paying sales tax upfront. By providing suppliers with a reseller permit.

The contractor then collects retail sales tax from the customer on the total contract price, including those materials. This prevents double taxation while ensuring tax gets collected at the retail level.

Reseller permits are free, valid for two years, and issued specifically to businesses making wholesale purchases. Contractors cannot use reseller permits to purchase consumable supplies, tools, equipment, or items not incorporated into the customer’s project—those purchases require paying sales tax.

Prime Contractor vs. Subcontractor Tax Collection

Understanding who collects tax matters in multi-tier projects:

Prime contractors (hired directly by property owners) collect retail sales tax from customers on the total contract price, including amounts paid to subcontractors.

Subcontractors don’t charge sales tax to prime contractors. Instead, they provide the prime contractor with a reseller permit, documenting that their work is for resale as part of the larger retail project. The subcontractor reports the transaction under wholesaling B&O tax classification.

This hierarchy prevents double taxation while ensuring the state collects retail sales tax once from the end customer.

Audit Risks and Common Mistakes

Washington’s Department of Revenue actively audits contractors. Common deficiencies include:

Underreporting taxable labor: Treating labor as exempt when it’s actually part of a taxable retail transaction

Incorrectly claiming exemptions: Assuming work qualifies as real property improvement when it involves tangible personal property installation

Missing local taxes: Washington has approximately 186 local taxing jurisdictions with varying rates. Collecting state tax but missing local components triggers liabilities. Proper address-level validation and comprehensive filing services ensure you’re calculating and remitting all required taxes.

Inconsistent treatment: Taxing some jobs but not others with similar characteristics raises red flags

The penalties bite hard. Washington imposes interest on unpaid tax, penalties up to 29% for negligence, and potential criminal prosecution for intentional evasion.

Multi-State Contractors: Why Washington Is Different

If you operate across state lines, Washington’s approach stands out:

Most states exempt pure labor: Many jurisdictions tax materials but exempt labor charges when separately stated. Washington takes the opposite approach for retail transactions.

Real vs. personal property line: The distinction determining taxability in Washington receives different treatment elsewhere. What qualifies as real property improvement in one state might be taxable retail installation in Washington.

Tax on contractors vs. customers: Some states tax contractors as consumers of materials (similar to Washington’s construction contractor treatment). Others tax the customer on the full retail transaction. Washington uses both approaches depending on transaction type.

Rate complexity: Washington’s local sales tax adds complexity. Approximately 186 local taxing jurisdictions create rate variations requiring address-level accuracy.

For businesses expanding into Washington, understanding these differences prevents costly mistakes. The nexus analysis services HOST provides identify exactly where you have obligations and ensure correct treatment in each jurisdiction.

What E-Commerce Businesses Need to Know

While this focuses on traditional contractor services, e-commerce businesses selling products requiring installation face similar questions.

If you sell and install products like furniture, appliances, or equipment in Washington, the entire transaction including installation labor is taxable. You cannot separately state installation labor to avoid taxation.

Understanding how Washington treats your specific business model requires analysis of whether you’re selling tangible personal property or services, whether tangible property becomes real property upon installation, your nexus status based on sales thresholds or physical presence, and how to source transactions under Washington’s destination-based system.

Complex situations often benefit from professional guidance. HOST’s sales tax consultation services provide 15, 30, or 60-minute sessions to discuss your specific scenarios and receive strategic compliance recommendations.

HOST specializes in multi-state compliance for businesses operating across jurisdictions with varying rules. We analyze your business model, determine obligations in each state, and manage ongoing compliance so you can focus on growth.

HOST: Your Partner for Washington Contractor Tax Compliance

Sales tax compliance for contractors operating in Washington (or across multiple states) creates operational complexity that diverts attention from core business. Understanding labor taxability, tracking local rate changes, managing exemption certificates, and responding to notices consumes hours that generate no revenue.

What HOST Delivers:

Nexus Analysis: We analyze your Washington operations and multi-state footprint to determine exactly where you have sales tax obligations. Identifying both obvious and hidden nexus triggers

Sales Tax Registration: We handle registration with Washington and other states where you’ve triggered nexus, managing paperwork and communications

Accurate Rate Determination: We ensure you’re collecting the correct combination of state and local taxes based on customer location in Washington’s approximately 186 jurisdictions

Automated Filing: We prepare and file returns monthly, quarterly, or annually across all states—including Washington’s complex local returns

Exemption Certificate Management: We implement systems to properly capture, verify, and retain exemption certificates from customers claiming exempt status

Notice Management: We interpret and respond to Washington Department of Revenue notices, protecting you from penalties while resolving issues efficiently

Audit Defense: When Washington initiates an audit, we serve as your trusted partner organizing documentation, defending positions, and negotiating resolutions

Software Configuration: We review and optimize your sales tax automation tools to calculate Washington’s complex local rates correctly

We’ve focused exclusively on sales tax for over 25 years. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to contractors and e-commerce sellers of all sizes.

You handle the work, we handle the tax.

Ready to Get Washington Contractor Tax Right?

Whether you’re expanding into Washington, an e-commerce business offering installation services, or a multi-state operation struggling with varying state rules, understanding labor taxability prevents costly mistakes.

Washington’s aggressive enforcement, complex local rates, and unique treatment of contractor labor make compliance challenging. Professional management eliminates guesswork and ensures you’re collecting correctly without diverting focus from revenue-generating activities.

Contact HOST today to discuss your compliance needs and discover how we handle the complexity so you can focus on growth.

Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Do contractors charge sales tax on labor in Washington State?

It depends on the work type. Installing, repairing, or fabricating tangible personal property as a retail transaction means labor charges are taxable alongside materials. Performing real property construction or improvement means you don’t charge sales tax to customers but instead pay tax on materials you purchase.

What’s the difference between construction contractors and retail contractors in Washington?

Construction contractors work on real property improvements (buildings, structures permanently affixed to land, etc.) and don’t charge sales tax to customers. Retail contractors install or repair tangible personal property and must collect sales tax on the entire charge including labor.

Can I separately state labor and materials to avoid Washington sales tax?

No. When you’re engaged in retail sale of tangible personal property, Washington treats the entire charge: materials, labor, overhead, profit, as taxable retail selling price. Separately stating components doesn’t change tax treatment.

Is appliance repair labor taxable in Washington?

Yes. Repair services involving tangible personal property, including appliance repair, face retail sales tax on both parts and labor charges.

How do I know if my installation work is real property or tangible personal property?

The determination depends on whether the installed item becomes permanently affixed to real estate and loses its identity as personal property. Built-in appliances, hardwired systems, and items that become structural components may qualify as real property improvements, while items remaining readily removable typically stay tangible personal property. Specific facts of each installation determine treatment.

What happens if I don’t charge sales tax on labor in Washington when I should?

Washington can assess back taxes for uncollected amounts, plus interest and penalties up to 29%. In audits, you bear the burden of proving exemptions apply. Without documentation, auditors presume charges are taxable. Professional compliance management prevents these costly mistakes.