What triggers a sales tax audit? For e-commerce businesses managing multi-state compliance, the answer isn’t always obvious, but the consequences of missing red flags can be devastating.

Understanding what catches auditors’ attention helps businesses stay compliant and avoid costly examinations. Hands Off Sales Tax (HOST) has defended hundreds of audits over 25+ years, giving us unique insight into exactly what triggers state scrutiny, and how to prevent it.

How State Tax Authorities Select Audit Targets

State revenue departments don’t audit randomly. They use data analytics, third-party reporting, and pattern recognition to identify high-probability non-compliance.

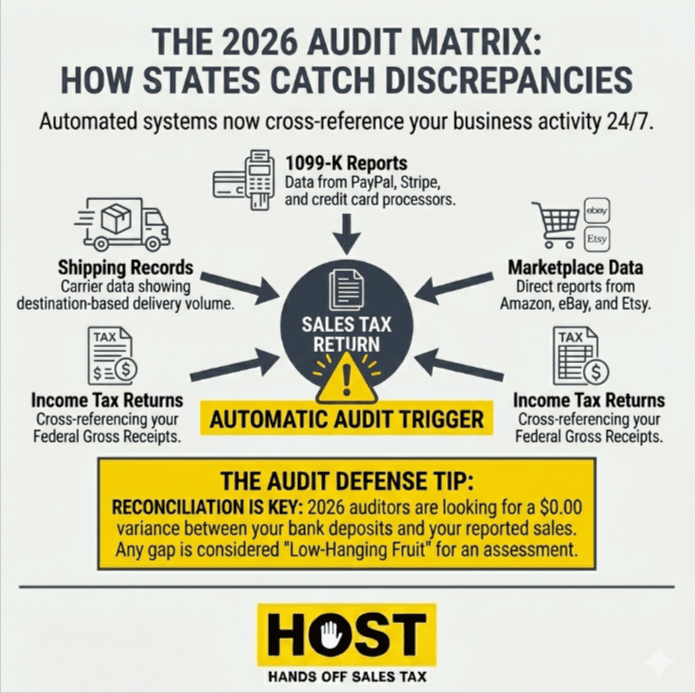

Automated Data Matching Systems

States now cross-reference multiple data sources automatically. Your sales tax returns get compared against marketplace facilitator reports (Amazon, eBay, Shopify), credit card processor data, and shipping records.

When these sources don’t align with your reported sales, the system flags your account. A seller reporting $500,000 annually but showing $2 million in payment processing creates an immediate audit trigger.

Industry-Specific Targeting

E-commerce sellers, SaaS companies, construction contractors, and restaurants consistently rank high on audit target lists. Post-Wayfair, remote sellers became priority targets. States know many businesses struggle with economic nexus compliance across 45+ jurisdictions.

Revenue Shortfall Periods

Audit activity increases dramatically during budget shortfalls. Recent data shows audit rates quadrupling from less than 1% in 2021 to 4% in 2023. Auditors receive performance metrics tied to revenue recovery, creating institutional pressure to identify non-compliance.

Top Red Flags That Trigger Audits

Significant Reporting Discrepancies

The most common trigger: your reported sales don’t match third-party data. This happens when businesses underreport revenue, fail to account for exempt transactions correctly, or report gross instead of taxable sales.

States also cross-reference your sales tax returns against federal income tax returns. When total sales on your federal return don’t align with sales tax filings, it creates an immediate audit flag. These discrepancies trigger automatic review systems designed to catch underreporting.

Even if differences represent legitimate exempt sales, the burden of proof falls on you during audit.

Inconsistent Filing Patterns

Erratic filing behavior signals problems: filing late repeatedly, showing dramatic month-to-month fluctuations without business explanation, or suddenly decreasing reported sales after consistent growth.

States track your filing history over years. When monthly reports drop from $50,000 to $10,000 without nexus termination or business closure, it raises questions.

Zero or Minimal Tax Due Repeatedly

Filing returns showing zero or minimal tax due for extended periods invites examination. While legitimate scenarios exist, states assume most retailers collect some tax.

A restaurant filing zero tax due for six consecutive months despite active operations creates an obvious red flag.

Never Registered Despite Clear Nexus

Operating without registration despite obvious nexus triggers enforcement action. States identify unregistered businesses through business licenses, Amazon seller data, corporate filings, and third-party reporting.

The most common scenario: an e-commerce seller crosses the $100,000 threshold in multiple states but only registers in their home state. Within 12-24 months, notices demanding back taxes arrive.

HOST’s nexus analysis service identifies exactly where you’ve triggered obligations, preventing this costly scenario.

High Exemption Certificate Usage

Claiming large percentages of exempt sales without proper documentation attracts scrutiny. Auditors specifically examine whether certificates are complete, current, and match the claimed exemption type.

Missing signatures, expired certificates, or certificates from ineligible buyers result in assessed tax on those transactions plus penalties.

Operating in High-Audit States

Geographic location matters significantly. California, New York, Texas, Illinois, Pennsylvania, Florida, and New Jersey maintain large audit divisions and sophisticated data systems.

California alone employs over 1,000 auditors focused on sales tax. Understanding your state’s audit intensity helps calibrate compliance investment.

High Initial Reports After Late Registration

Registering late with high initial tax amounts signals to states that you crossed nexus thresholds much earlier. When your first return shows $10,000 in collected tax, auditors immediately calculate backward, wondering if you collected that much in month one, how much did you owe over the previous year?

This pattern triggers automatic audit flags designed to recover back taxes from the period between when you should have registered and when you actually did. States specifically target this scenario because it represents clear revenue loss.

Vendor or Customer Audit by Association

When your vendor or customer gets audited, you’re often next. States conduct “whipsaw audits” which examine the entire business network connected to an audited company.

During a customer’s audit, auditors review your invoices. If exemption certificates are missing or improper, they contact you directly. When large companies get audited, states systematically audit all their suppliers and clients, creating cascading examination waves.

This trigger sits completely outside your control, making documentation even more critical.

Never Reporting Use Tax

Businesses that never report use tax on returns raise immediate red flags. Use tax applies to out-of-state purchases where no sales tax was collected: equipment, furniture, software, supplies purchased from vendors who didn’t charge tax.

Auditors call this “low-hanging fruit” because most businesses neglect it entirely. Zero use tax reported year after year suggests either perfect compliance (unlikely) or complete ignorance of the obligation (probable).

Business Closure or Dissolution

Closing locations, dissolving the business, or declaring bankruptcy triggers immediate audit action. States want to collect before the business disappears and assets get distributed.

These “exit audits” often receive priority handling because the window for collection is closing. Even businesses that maintained perfect compliance face scrutiny during closure.

Post-Wayfair Compliance Gaps

The 2018 Wayfair decision fundamentally changed sales tax compliance. States implemented economic nexus laws requiring collection once you exceed thresholds that are typically $100,000 in sales or 200 transactions annually.

Crossing Thresholds Without Registration

The most common post-Wayfair violation: exceeding thresholds without registering. States receive marketplace facilitator reports showing your sales volume. When data shows you crossed $100,000 but you’re not registered, audit notices follow.

Incorrect State Sourcing

Origin-based sourcing (charging your home state’s rate to all customers) worked pre-Wayfair but violates current rules. Destination-based sourcing requires calculating tax based on customer location across 11,000+ jurisdictions.

HOST’s Free Sales Tax Software Review identifies configuration errors before they become audit issues.

Marketplace Sales Confusion

When filing returns, you must exclude marketplace-facilitated sales to avoid reporting the same revenue twice. Auditors frequently see sellers report total sales including Amazon transactions, while Amazon separately reports the same transactions. This appears as underremittance and triggers examination.

How Software Errors Create Audit Exposure

Sales tax automation tools calculate rates, but misconfiguration creates systematic errors affecting thousands of transactions.

Incorrectly configured software may charge tax on exempt products like groceries, prescription medications, manufacturing equipment. While this generates excess revenue for states, it signals overall system problems and incomplete exemption documentation.

Missing local taxes creates underremittance. States receive local tax reports from processors showing customer locations. When your remittance doesn’t include local components, it signals calculation problems.

Warning Signs You’re at Risk

Rapid Business Growth

Dramatic year-over-year revenue increases attract attention because they create compliance gap opportunities. If your business grew from $500,000 to $2 million annually, ensure your nexus coverage, registration status, and software configuration scaled accordingly.

Nexus Questionnaires and Pre-Audit Letters

States send compliance questionnaires probing your sales activity before launching full audits. These seemingly harmless letters request detailed information about your operations, nexus triggers, and sales volumes.

Ignoring these questionnaires or responding inaccurately often triggers formal audits. Many businesses dismiss them as low-priority, but they’re actually the state’s way of building an audit case. Treat nexus questionnaires as seriously as audit notices.

Previous Audit History

Once audited, you face higher probability of future examination. States revisit businesses with prior compliance issues within 3-5 years.

Operating Without Professional Guidance

Businesses attempting DIY sales tax compliance face significantly higher audit rates. The complexity of multi-state obligations, constantly changing laws, and jurisdictional variations make professional management essential.

HOST has defended hundreds of audits over 25+ years. We know exactly what auditors look for, how to organize documentation, and how to resolve examinations while minimizing assessed liabilities.

How to Reduce Your Audit Risk

Maintain Complete Exemption Certificate Files

Every exempt transaction requires valid documentation: customer signature, business license number, expiration date, and specific exemption type. Missing documentation on 5% of claimed exempt sales results in assessed tax on 100% during audit.

Conduct Regular Nexus Reviews

HOST’s nexus analysis service monitors your sales across all states, alerting you when approaching thresholds and handling registration when you cross them.

Reconcile Third-Party Reports

Compare internal sales data against marketplace reports, payment processor statements, and shipping records quarterly. Identifying discrepancies before states do allows for correction through amended returns rather than audit assessments.

Keep Detailed Records

Maintain transaction-level records for at least four years. This includes invoices, exemption certificates, shipping documentation, and evidence supporting tax calculation decisions.

Document significant business changes affecting reporting: seasonal patterns, wholesale channel launches, or geographic expansion. When auditors see explanations for reporting variations, it reduces suspicion.

What to Do If You Receive an Audit Notice

Act Quickly

Audit notices include response deadlines, which are typically 30 days. Missing deadlines results in automatic assessments based on state estimates, which are always higher than reality.

Contact Professionals Immediately

Sales tax audits are technical proceedings with significant financial consequences. HOST’s audit defense service manages the entire process: organizing documentation, communicating with auditors, identifying assessment errors, and negotiating resolution.

Gather Requested Documentation

Auditors request transaction records, exemption certificates, general ledgers, bank statements, and software reports. Incomplete documentation appears like non-compliance even when you collected tax correctly.

Consider Voluntary Disclosure

If audits uncover obligations in states where you never registered, voluntary disclosure agreements (VDAs) can limit lookback periods and abate penalties. Rather than facing full statutory lookback (typically 3-4 years), VDAs often limit exposure to 12-36 months with no penalties.

HOST: Your Partner in Audit Prevention and Defense

Sales tax audits drain time, resources, and capital. Prevention through proper systems delivers far better ROI than reactive defense.

What HOST Delivers:

Nexus Analysis: We monitor your sales footprint, identifying exactly where you’ve triggered obligations and handling registration proactively

Sales Tax Filings: We prepare and file returns in all jurisdictions monthly, quarterly, and annually which eliminates filing pattern red flags

Software Optimization: Our Free Sales Tax Software Review identifies configuration errors creating compliance gaps

Exemption Certificate Management: We help implement proper documentation systems ensuring every exempt transaction has supporting certificates

Audit Defense: We manage the entire process: organizing documentation, communicating with auditors, and negotiating favorable resolution

Voluntary Disclosure: We file VDAs strategically to limit lookback periods and abate penalties

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate compliance while minimizing audit risk. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

Stay Ahead of State Scrutiny

Understanding what triggers sales tax audits helps you recognize vulnerabilities before states initiate examination. From inconsistent reporting to post-Wayfair nexus gaps, most audit triggers are preventable through proper systems and professional management.

State tax authorities have sophisticated analytics identifying non-compliance faster than ever. Waiting until you receive an audit notice means facing back taxes, penalties, interest, and significant disruption.

Whether you’re managing nexus across multiple states, scaling rapidly, or want peace of mind that your compliance is solid, the right partner makes all the difference. At HOST, we combine deep technical expertise with 25+ years of specialized experience, transparent communication, and personalized support.

When you’re ready to eliminate audit risk and ensure bulletproof compliance, we’re ready to help. Contact HOST today to discuss your compliance needs or schedule a free consultation.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the most common trigger for sales tax audits?

Reporting discrepancies between your sales tax returns and third-party data (marketplace reports, payment processors, shipping records) trigger the majority of audits. States automatically flag accounts when these sources don’t align.

How far back can states audit my sales tax records?

Most states have a three to four-year statute of limitations. However, if fraud or no filing is suspected, some states can look back six years or more.

Will using sales tax software prevent audits?

Software helps calculate correct rates and track nexus, but misconfiguration actually creates audit triggers: overtaxing exempt items, missing local taxes, or double-taxing due to multi-channel sales.

Do small businesses get audited less frequently?

Not necessarily. Small businesses get audited when data shows specific red flags: inconsistent reporting, operating without registration despite nexus, or industry-specific non-compliance patterns.

What should I do if I’ve been collecting sales tax incorrectly?

Contact a sales tax professional immediately. Voluntary disclosure agreements can limit lookback periods and abate penalties when you proactively address compliance gaps.

Can I represent myself during a sales tax audit?

You can, but professional representation dramatically improves outcomes. Specialists understand what documentation satisfies auditors, how to challenge incorrect assessments, and when to negotiate liability reductions. The cost of representation typically saves multiples in reduced assessments.