Can you deduct sales tax as a business expense? Sometimes, but IRS rules create complexity that catches even seasoned business owners off guard. Sales tax you collect from customers never qualifies as a deduction. Sales tax you pay on business purchases often does, but it’s embedded within larger expense categories rather than claimed separately.

Understanding which sales tax qualifies, how to document it correctly, and when deductions actually reduce your tax liability requires navigating rules that shift based on business structure, purchase type, and state jurisdiction.

From nexus obligations across 45+ states to multi-jurisdictional compliance, sales tax creates layers of complexity for growing businesses. Hands Off Sales Tax (HOST) manages the operational burden: registration, filing, notices, audits, so you can focus on maximizing legitimate deductions rather than drowning in compliance details.

Sales Tax Collected: Never Deductible

Here’s the critical rule: sales tax you collect from customers is never a deductible business expense. The IRS treats collected sales tax as a liability, not income or expense.

When you collect $100 in sales tax from customers, you don’t report it as business income. It flows straight through your books as a liability: money you owe to state and local governments. You’re a collection agent, not earning revenue.

This means you can’t deduct it. Attempting to deduct collected sales tax creates red flags for audits since you never included it in taxable income.

Many business owners get confused by cash flow timing. You might collect sales tax in January but not remit it until February’s filing deadline. During that window, the cash sits in your bank account, making it feel like your money. It’s not. It’s a liability from day one.

Best practice: Maintain separate accounting for collected sales tax using liability accounts in QuickBooks, Xero, or your accounting software.

Sales Tax You Pay: Embedded in Your Expenses

Sales tax you pay on business purchases often qualifies as a deductible expense,but almost never as a separate standalone deduction. The IRS requires you to include sales tax paid as part of the cost basis for the underlying expense.

When It’s Deductible: Real-World Examples

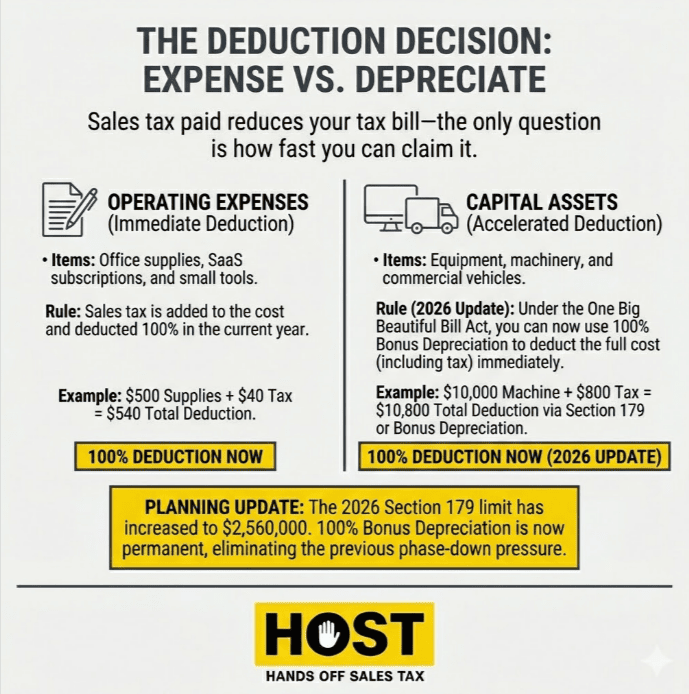

Office Supplies and Operating Expenses: Purchase $500 in office supplies plus $40 sales tax? Your deductible office supply expense is $540 total. The sales tax is embedded in the supply cost.

Equipment and Machinery: Here’s where understanding the math matters. Say you purchase a $10,000 computer system with $800 sales tax, creating an $10,800 total cost. You depreciate that full $10,800 over the equipment’s useful life. Or, use Section 179 to deduct the complete $10,800 immediately. At a 24% tax rate, that $800 in sales tax translates to $192 in federal tax savings—either this year via Section 179, or spread over the depreciation period. The sales tax doesn’t disappear; it reduces your taxable income just like the equipment cost itself.

Inventory Purchases for E-Commerce Sellers: This is where many online retailers miss opportunities. When you purchase $50,000 in inventory plus $4,000 sales tax, that complete $54,000 becomes your cost of goods sold when the inventory sells. The sales tax flows through your income statement as part of COGS, reducing taxable profit dollar-for-dollar. For product sellers, properly tracking sales tax paid on inventory purchases directly impacts your bottom line.

Business Services: Sales tax paid on software subscriptions, consulting, repairs gets included in the service expense. A $1,200 software license with $96 sales tax becomes a $1,296 deductible software expense.

When It’s Not Deductible

Personal Purchases: Sales tax paid on personal items never qualifies, even if you’re self-employed. The IRS draws clear lines between business and personal expenses.

Resale Certificate Exempt Purchases: When you use exemption certificates to buy inventory without paying sales tax, there’s no sales tax to deduct. You collect sales tax from end customers instead. Understanding when to use resale certificates helps you avoid paying tax unnecessarily! A better outcome than deducting tax you shouldn’t have paid in the first place.

Meals and Entertainment: While business meals are partially deductible (typically 50%), sales tax paid on those meals follows the same limitation.

Use Tax: The Hidden Obligation Most Businesses Miss

Here’s what competitors won’t tell you: even when you don’t pay sales tax, you might still owe tax, and potentially deduct it.

Use tax is the mirror image of sales tax. When you purchase items from out-of-state vendors who don’t collect your state’s sales tax, you typically owe use tax directly to your home state. This happens frequently with online purchases, equipment bought from vendors without nexus in your state, or inventory sourced from out-of-state wholesalers.

Example: You purchase $10,000 in equipment from an Oregon vendor (no sales tax state). They don’t collect tax, but your California business owes California use tax on that purchase. You report and pay the use tax directly to California, then include it in your equipment’s depreciable basis. Just like sales tax.

Most businesses overlook use tax entirely, creating audit liability. Others pay it but forget to include it in their deductible expense basis. Either mistake costs you money. HOST’s nexus analysis doesn’t simply identify where you should collect sales tax, we flag use tax obligations you might be missing.

The Personal Tax Election: Sales Tax vs. Income Tax

Individual taxpayers face a choice when itemizing deductions on Schedule A: deduct state and local income taxes paid OR state and local sales taxes paid, but not both.

For most business owners, this personal tax decision favors deducting income taxes since they’re typically higher. However, individuals in states without income tax (Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, Wyoming, and New Hampshire) benefit from electing the sales tax deduction.

The 2017 Tax Cuts and Jobs Act originally capped the combined state and local tax (SALT) deduction at $10,000. However, on July 4, 2025, the One Big Beautiful Bill Act increased this cap to $40,000 for taxpayers with modified adjusted gross income under $500,000. The cap phases down for incomes above this threshold and reverts to $10,000 in 2030.

For your business entity: This election is irrelevant. Business expenses flow through normal expense categories with sales tax embedded. C corporations are not subject to the SALT deduction cap.

How Business Structure Affects Sales Tax Deductibility

Your business legal structure determines exactly how sales tax deductions flow through to your taxable income, but the principle remains consistent: sales tax paid on legitimate business purchases reduces taxable income as part of the underlying expense, not as a separate line item.

Sole Proprietorships: Sales tax gets included in expense categories on Schedule C. Office supply purchases include sales tax in line 18. Equipment purchases include sales tax on the depreciable basis.

Partnerships, LLCs, and S Corporations: Sales tax flows through expense categories, then passes through to partners or shareholders on Schedule K-1 with sales tax embedded throughout.

C Corporations: Sales tax paid reduces corporate taxable income directly as part of expense categories on Form 1120, without SALT deduction caps.

E-Commerce Sellers: Special Considerations Post-Wayfair

The 2018 Wayfair decision changed everything for online sellers. Once you cross economic nexus thresholds (typically $100,000 in sales or 200 transactions), you must register and collect sales tax in that state.

Here’s what most articles miss: registering in multiple states affects your deduction strategy. When you’re registered in 15 states, you’re potentially paying sales tax on business purchases in all 15 states. Each state’s sales tax paid flows into your deductible expenses. This compounds across jurisdictions.

Marketplace Facilitators Change the Calculation: If you sell through Amazon, Etsy, or other platforms, they collect and remit sales tax on your behalf in most states. This simplifies collection but doesn’t eliminate your obligation to track sales tax you pay on business purchases in those states.

Inventory Sourcing Strategy: Many e-commerce sellers source inventory from wholesalers in multiple states. Providing valid resale certificates to those wholesalers eliminates sales tax on inventory purchases, creating zero deductible sales tax, but also zero unnecessary tax paid. Understanding when you’re the end user (pay sales tax, then deduct it) versus reselling (use exemption certificate, collect from customers) prevents overpaying.

HOST’s nexus analysis determines exactly where your business has triggered obligations across all 45 sales tax states, ensuring you’re positioned to maximize legitimate deductions while staying compliant.

Documentation: Your Audit Defense

The IRS requires substantiation for all business expense deductions. When sales tax is embedded in those expenses, your documentation must support both the underlying purchase and the tax paid.

Keep all receipts showing the purchase amount, sales tax charged, date, vendor, and description. Digital copies work, photograph receipts immediately or use receipt-scanning apps.

Separate business and personal purchases completely. Dedicated business credit cards create clear documentation trails.

Maintain exemption certificates for purchases where you didn’t pay sales tax due to resale or manufacturing exemptions.

Retain records for at least three years from the filing date. Many states reach back four years for sales tax audits.

HOST’s audit defense services include organizing documentation and defending your position when state or local authorities question obligations.

Common Mistakes That Trigger Audits

Trying to Deduct Collected Sales Tax: This is the biggest red flag. Since collected sales tax is never included in revenue, deducting it creates artificial losses that immediately attract IRS attention.

Missing Sales Tax in Asset Capitalization: Capitalizing only the purchase price and expensing sales tax separately violates IRS rules. Sales tax must be included in the asset’s depreciable basis.

Claiming Personal Sales Tax as Business Expense: Self-employed individuals sometimes blur lines between personal and business purchases. This is an instant audit trigger.

Double-Counting: Including sales tax in expense categories (correct) but also claiming a separate sales tax deduction on personal returns (incorrect).

Poor Documentation: Missing receipts or commingled personal-business purchases give the IRS grounds to disallow deductions entirely.

Strategic Tax Planning: Timing Your Deductions

Year-End Equipment Purchases: Buying equipment before December 31 captures the deduction (including sales tax) in the current tax year. With Section 179 expensing, you can deduct up to $1,220,000 (2025 limit) immediately, including all sales tax paid.

Sales Tax Holiday Coordination: Some states offer sales tax holidays on specific purchases. Timing major equipment acquisitions during these windows eliminates sales tax, meaning nothing to deduct; but also nothing to pay. For large purchases, the elimination beats the deduction.

Use Tax Catch-Up: If you’ve been missing use tax obligations, addressing them through voluntary disclosure limits lookback periods and penalties while creating legitimate deductions you’ve been missing.

HOST offers a Free Sales Tax Software Review to identify whether you’re overpaying sales tax on purchases that should be exempt, eliminating unnecessary costs is much better than deducting them later.

HOST: Your Partner for Sales Tax Compliance

Sales tax compliance extends far beyond understanding deductibility. Managing multi-state obligations, tracking nexus thresholds, handling registrations, filing returns, and responding to notices consumes time that generates zero revenue.

What HOST Delivers:

- Nexus Analysis: We analyze your sales footprint to determine where you’ve met economic or physical nexus thresholds

- Sales Tax Registration: We handle registrations in all required states, managing paperwork and state communications

- Automated Filing: We file your returns across all jurisdictions. Monthly, quarterly, annually

- Notice Management: We interpret and respond to state notices, protecting you from penalties

- Audit Defense: We organize documentation and defend your position when tax authorities come knocking

- Software Optimization: We review your TaxJar, Avalara, or other automation tools

We’ve been 100% focused on sales tax since 1999. Co-founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

Ready to Simplify Sales Tax Compliance?

Understanding sales tax deductibility helps you maximize legitimate tax benefits while avoiding costly mistakes. But the deduction strategy represents just one piece of comprehensive sales tax management.

At HOST, we combine deep technical expertise with 25+ years of specialized experience. When you’re ready to take sales tax off your plate and ensure compliant operations, we’re ready to help.

Contact HOST today to discuss your compliance needs and discover how we handle the complexity so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Can I deduct sales tax I collect from customers?

No. Sales tax collected from customers is a liability, not income or expense. Since you never report it as income, you cannot deduct it as an expense. Attempting this creates immediate audit red flags.

How do I deduct sales tax I pay on business purchases?

Include sales tax paid as part of the underlying expense category. Office supplies purchased for $500 plus $40 sales tax becomes a $540 office supply expense. Equipment purchases include sales tax in the capitalized cost, which you depreciate over time or expense immediately via Section 179.

What is use tax and do I need to worry about it?

Use tax applies when you purchase items from out-of-state vendors who don’t collect your state’s sales tax. You owe use tax directly to your home state and can include it in your deductible expense basis. Most businesses overlook use tax entirely, creating audit liability.

Does business structure affect sales tax deductibility?

Business structure determines how deductions flow through to taxable income, but the principle remains consistent: sales tax paid on legitimate business purchases reduces taxable income as part of the underlying expense.

How does selling on Amazon or Etsy affect my sales tax deductions?

Marketplace facilitators collect sales tax on your behalf, but this doesn’t affect sales tax you pay on business purchases. You still deduct sales tax paid on inventory, equipment, and supplies by including it in the expense cost.

Should I use resale certificates or just deduct the sales tax I pay?

Use resale certificates when buying inventory for resale. This eliminates sales tax entirely, which is better than paying it and deducting it later. Only pay sales tax on items you’ll use in your business (equipment, supplies), not items you’ll resell.