Pennsylvania’s sales tax system follows one rule: collect more, file more often. Miss a deadline? 5% penalties per month start stacking immediately, plus interest that compounds daily.

Hands Off Sales Tax (HOST) eliminates the guesswork. We file on time, calculate prepayments correctly, and intercept problems before they reach your desk. For 25 years, we’ve watched businesses struggle with Pennsylvania’s complex filing requirements. Prepayment thresholds that activate without warning, or software miscalculations that create personal liability. Our approach removes those risks entirely.

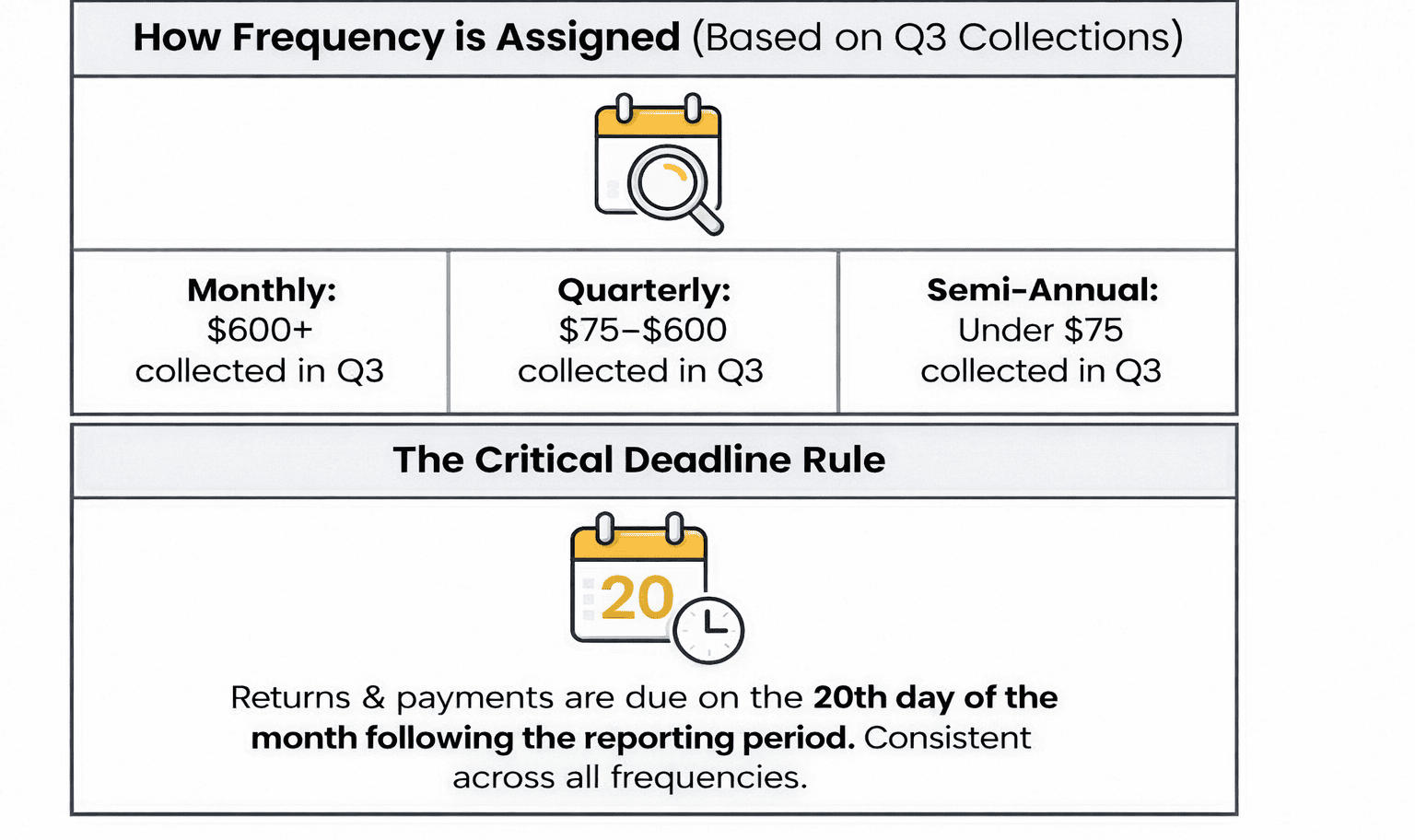

How Pennsylvania Assigns Your Filing Frequency

Every new business starts quarterly filing in April, July, October, and January during year one. This gives new operations breathing room to establish processes without monthly filing pressure. Pennsylvania doesn’t differentiate between businesses during the first year. Whether you collect $500 or $50,000 in sales tax, you’re filing quarterly until the state reviews your actual collection history.

Each November, Pennsylvania reviews third-quarter collections (July-September) and assigns next year’s frequency based on precise thresholds:

- Monthly filing: $600+ in Q3

- Quarterly filing: $75-$600 in Q3

- Semi-annual filing: Under $75 in Q3

These thresholds represent sales tax collected, not gross sales. A business with $10,000 in Q3 sales at Pennsylvania’s 6% rate collects $600 in tax, hitting the monthly threshold exactly. Understanding this distinction prevents surprises when frequency changes arrive.

No December notification? Don’t assume nothing changed. Log into myPATH and check your account dashboard. The automated notification system fails occasionally, but the frequency change still applies regardless of whether you received official notice. Pennsylvania holds you responsible for checking your status, making myPATH verification essential every December.

Semi-annual filers follow different rules designed to catch seasonal businesses. Pennsylvania examines combined collections from the last half of the previous year plus the first half of the current year. Exceed $300 total, you move to quarterly. Hit $2,400 total and you’re monthly. This extended review period prevents holiday retailers or summer-focused businesses from staying semi-annual when their annual collections actually warrant more frequent filing.

The difference matters significantly. A seasonal business collecting $250 in Q3 stays semi-annual based on that quarter alone. If summer and holiday seasons pushed total annual collections to $2,500, the 12-month review catches it and assigns monthly filing. Pennsylvania designed this specifically to ensure high-volume seasonal operations file appropriately.

Due Dates and Prepayment Requirements

Returns land on the 20th of the month following your reporting period. January collections? Due February 20th. Weekend deadline? You get the next business day. This 20th-day rule applies universally across monthly, quarterly, and semi-annual frequencies. Pennsylvania keeps due dates consistent to simplify compliance.

Pennsylvania tracks compliance patterns meticulously. Skip a zero return and face identical penalties as skipping a $10,000 payment. The state views missing zero returns as equally serious compliance failures because they indicate you’re not monitoring obligations properly. Worse, a history of missed zero returns damages your compliance record during November frequency reviews, potentially triggering audits even when you’ve paid every dollar owed.

Payment Methods Matter

Payments over $1,000 must use Electronic Funds Transfer (EFT) through myPATH. This isn’t optional—it’s a hard requirement. Under $1,000? Pay via ACH debit, ACH credit, or credit card (convenience fees apply for cards, typically 2.35% of payment). Wrong methods trigger compliance violations even when amounts are correct and on time. Pennsylvania’s system flags incorrect payment methods as procedural violations separate from late payment issues.

No internet access? File by phone: 1-800-748-8299. The TeleFile system walks you through reporting gross sales, taxable sales, and tax collected via automated prompts. You’ll need your 8-digit sales tax account number, total sales figures, and bank information for payment. While less common in 2026, TeleFile ensures businesses without reliable internet can maintain compliance.

When Prepayments Start

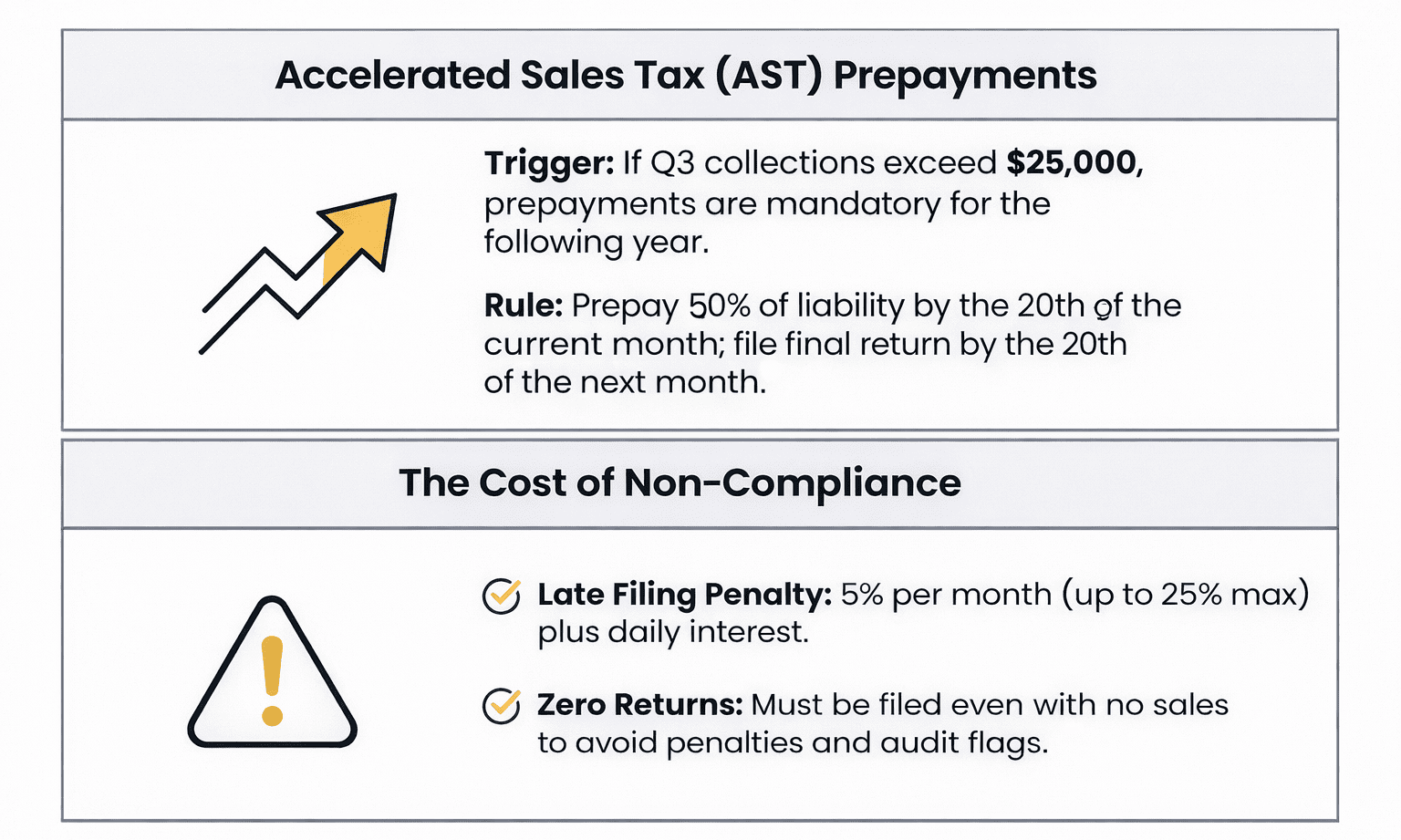

Cross $25,000 in Q3 collections and Accelerated Sales Tax prepayments activate immediately for the following year. Pennsylvania implemented AST to ensure steady revenue flow from high-volume businesses rather than receiving large lump sums quarterly or monthly.

Level 1 ($25,000-$100,000 in Q3): Choose 50% of last year’s same-month liability or 50% of current month estimate. This flexibility helps businesses with fluctuating revenue. Growing businesses can estimate current month liability, while stable operations might prefer the predictability of last year’s figures. You select the method each month. No requirement to use the same approach consistently.

Level 2 ($100,000+ in Q3): Pay 50% of last year’s same-month liability. No estimation option at this volume. Pennsylvania wants certainty and consistent revenue flow from major tax collectors. If last January you collected $15,000 in sales tax, you’re prepaying $7,500 by January 20th regardless of current year performance.

Here’s the critical detail businesses miss: submit prepayments and final returns separately in myPATH. The prepayment goes in by the 20th of the current month. The final return for that month goes in by the 20th of the following month. Combining them creates processing confusion that registers as non-compliance in Pennsylvania’s system, triggering penalty notices even when you’ve paid correctly.

Example: January 2026 collections require a prepayment by January 20th (based on your calculation method) and a final return by February 20th. The final return shows total tax collected minus the prepayment already submitted, resulting in the balance due. If you prepaid $7,500 and collected $14,200 total, your February 20th payment is $6,700.

Extensions Cover Paperwork Only

Form REV-426 grants 30 days for filing extensions. Extensions prevent late-filing penalties but not interest charges on late payment. This distinction costs businesses real money when misunderstood. The 5% monthly late-filing penalty waits if you file the extension, but interest at Pennsylvania’s current rate (announced annually by the Department of Revenue) starts accruing immediately on unpaid balances from the original due date.

Smart businesses use extensions strategically. If you need extra time to reconcile complex transactions or gather exemption certificates but can pay estimated tax on time, file REV-426 and submit payment by the original deadline. You get 30 days to perfect the return details without penalty exposure.

The Rewards and Risks

Pennsylvania balances incentives with consequences. Timely filers save money, late filers face escalating costs.

File On Time, Save Money

Timely filers get discounts that compound quickly:

- Monthly: Lesser of $25 or 1%

- Quarterly: Lesser of $75 or 1%

- Semi-annual: Lesser of $150 or 1%

The calculation matters. A monthly filer collecting $3,000 in sales tax gets $25 (since 1% would be $30, but the cap is $25). A monthly filer collecting $2,000 gets $20 (since 1% of $2,000 is less than the $25 cap). These discounts aren’t automatic—you claim them on your return when filing on time.

A business collecting $50,000 monthly saves $500 annually just for hitting deadlines. That’s $300 in capped discounts ($25 × 12 months). Over five years, that’s $2,500 in savings simply from punctual filing. For businesses filing quarterly with similar collection volumes, the savings are less frequent but equally valuable: $300 annually ($75 × 4 quarters).

File Late, Pay Dearly

Pennsylvania charges 5% per month, maxing at 25%, plus daily interest. The penalty calculates on unpaid tax, not gross sales. A $10,000 late payment becomes $10,500 after one month (5% penalty), $11,000 after two months (10% penalty), progressing to $12,500 after five months when you hit the 25% cap. Daily interest compounds on top of this throughout the entire period.

The minimum penalty is $5. Even if your late payment was only $50, you owe at least $5 in penalties. This catches semi-annual filers with very small obligations who assume minimal tax means minimal consequences.

Beyond financial costs, late filings damage your compliance profile. Pennsylvania reviews filing history when assigning frequency changes, conducting audits, and evaluating Voluntary Disclosure Agreement applications. Clean filing history signals reliable compliance; late filing patterns signal risk, triggering closer scrutiny across all interactions with the Department of Revenue.

Common Traps That Catch Good Businesses

Frequency Confusion: Your Q3 liability jumped from $550 to $650 after strong summer sales. Did you catch the November notification moving you from quarterly to monthly? The notification arrives during holiday chaos, and suddenly you’re three months behind in January without realizing the change occurred. By the time you discover it in March, you owe three months of penalties plus interest on each missed filing.

Prepayment Blindness: Fast growth is exciting until it crosses $25,000 in Q3 collections. AST Level 1 requirements activate immediately for the following year. Miss that first January prepayment because you didn’t realize the threshold triggered, and penalties accumulate before you notice. You might see the filing requirement but miss the additional prepayment obligation that now precedes each filing.

Local Rate Gaps: Your software applies Pennsylvania’s 6% statewide rate but misses Philadelphia’s additional 2% local tax. You’re personally liable for that missing 2%. The same trap exists in Allegheny County, where the combined rate should be 7% (6% state + 1% local), not 6%. These local rates apply to the delivery address for remote sellers, not your business location. A Pittsburgh business selling to a Philadelphia customer must collect 8%, not 7%.

The personal liability aspect shocks businesses, regardless of software failures. If your system miscalculates for six months, collecting 6% on Philadelphia sales instead of 8%, you personally owe the state that missing 2% on every transaction, which is potentially tens of thousands of dollars—plus penalties and interest. The customer already paid and received their goods; you can’t retroactively collect more tax. The shortfall comes from your pocket.

HOST Solution: We monitor frequency changes automatically with redundant systems that catch notifications before they slip through: prepayments without your involvement, calculating correct amounts and submitting them before deadlines. We ensure correct rate calculations for every jurisdiction, validating delivery addresses against Pennsylvania’s local tax database before processing transactions. Learn more about our filing services.

Why Businesses Choose HOST

Good businesses face bad consequences over filing mistakes that weren’t mistakes at all. Just predictable traps the system sets. Growth triggers new thresholds during vacation season when finance teams are understaffed. Prepayment requirements catch businesses unprepared because the notification was buried. Software providers update rate tables but miss local jurisdiction changes, creating liability exposure you discover during audits.

We eliminate those moments through continuous liability tracking that monitors your collections against every threshold, not just monthly totals; but Q3 isolations, 12-month rolling averages for semi-annual filers, and prepayment triggers. Accurate filing means validating those numbers against 67 Pennsylvania counties and two special local tax jurisdictions, ensuring every transaction calculates correctly before you claim it on a return.

Proactive prepayment management removes the calculation burden entirely. We determine which level applies, select the optimal calculation method for your situation, submit prepayments separately from returns, and reconcile everything on final filings. Problem interception happens before Pennsylvania sends notices. We catch frequency changes before you do, identify rate calculation errors before returns file, and resolve discrepancies before they become penalties.

Complete Coverage

- Nexus Analysis – We determine exactly where Pennsylvania and other states require collection based on your physical presence, economic activity, and sales patterns across all channels

- Registration Services – We handle myPATH setup, complete PA-100 enterprise registration, obtain your 8-digit sales tax account number, and manage all state paperwork including the 5-year renewal requirement

- Automated Filing – We submit returns monthly, quarterly, or semi-annually with zero input required from you, adapting automatically when Pennsylvania changes your frequency

- Prepayment Management – We calculate and submit AST Level 1 and Level 2 payments before deadlines, selecting optimal calculation methods and tracking prepayments through final return reconciliation

- Audit Defense – We represent you during Pennsylvania reviews, organize documentation, respond to information requests, and negotiate assessments to minimize liability

Take Pennsylvania Sales Tax Off Your Plate

Every hour researching filing frequencies or calculating prepayments is an hour not spent growing revenue. HOST eliminates that trade-off entirely. While you focus on sales, marketing, product development, and customer service, we handle the compliance burden that generates zero revenue but creates unlimited liability exposure when mismanaged.

Pennsylvania’s complex prepayment structure, local rate calculations, and frequency change tracking represent exactly the type of specialized compliance work we’ve perfected over two and a half decades. Your business gets enterprise-level expertise without enterprise-level overhead or long-term contracts.

We’ve seen every Pennsylvania filing scenario: seasonal businesses bouncing between frequencies, rapid growth triggering prepayment requirements mid-year, software migrations that disrupted rate calculations, local rate changes that created retroactive liability, and audit notices questioning three years of filings. This experience means we anticipate problems before they develop and resolve issues before they cost you money.

Schedule a consultation to discuss your specific situation. We’ll review your current filing frequency, verify your rate calculations, identify any exposure from past periods, and outline exactly how we’d manage Pennsylvania compliance going forward.

Download our guide on the 10 most expensive sales tax mistakes e-commerce sellers make, including several Pennsylvania-specific traps that catch even experienced finance teams.

Frequently Asked Questions

When does Pennsylvania change my filing frequency?

Every November, based on third-quarter collections (July-September). Collected $600+ in Q3? Expect monthly filing next year. Between $75-$600? You remain quarterly. Under $75? Semi-annual. Pennsylvania examines the 12-month period covering the last half of the previous year plus the first half of the current year. Check your myPATH dashboard if notification doesn’t arrive by mid-December, as the automated system occasionally fails to generate notices.

What triggers Accelerated Sales Tax prepayments?

Third-quarter collections exceeding $25,000 trigger AST requirements for the following calendar year. You’ll pay 50% of estimated liability by the 20th of each month (either based on last year’s same month or current month estimate for Level 1; last year’s same month only for Level 2), then file your complete return by the 20th of the following month showing total tax collected minus prepayment already submitted.

Do filing discounts actually matter?

Absolutely. A business filing monthly with $50,000 monthly collections saves $300 annually through capped discounts ($25 per month × 12 months). The actual savings can be higher if some months qualify for the full 1% before hitting the $25 cap. That’s real money that compounds as you grow—$1,500 saved over five years simply from punctual filing. Quarterly filers with similar volumes save $300 annually ($75 × 4 quarters).

What happens if I file three days late?

Pennsylvania charges 5% of unpaid tax immediately as a late filing penalty. There’s no grace period. “Just a few days” still costs you the full 5% for that month, plus daily interest charges. Beyond the financial cost, late filing triggers closer scrutiny during November frequency reviews and can flag your account for audit selection. The Department of Revenue views filing patterns as compliance indicators, so even one late filing damages your profile.

How do I fix errors on filed returns?

File amended returns using Form REV-1170 through myPATH. You may owe additional tax plus interest calculated from the original due date. Address errors quickly—Pennsylvania’s 4-year record retention requirement means mistakes surface during audits, and voluntary correction before audit discovery generally results in more favorable treatment. You can claim a refund for overrepayment, though the state takes 60-90 days to process refund requests.

Can HOST really eliminate all the hassle?

Yes. We monitor your thresholds continuously against all frequency triggers, calculate prepayments using optimal methods for your situation, file every return accurately on time, and handle all state communications including notices, frequency change confirmations, and audit information requests. You receive monthly summaries showing exactly what we filed, what we paid, and what your current obligations look like for the period ahead. No surprises, no missed deadlines, no personal liability exposure.Contact us today to get started..