Understanding Indiana sales tax filing frequency is crucial for businesses to ensure compliance, avoid penalties, and maintain smooth operations. The Indiana Department of Revenue (DOR) assigns filing frequencies (monthly, quarterly, or annually) based on a business’s tax liability, making it essential for business owners to stay informed about their obligations.

This guide provides a clear breakdown of Indiana’s filing frequency rules, due dates, and best practices for compliance. Hands Off Sales Tax (HOST) simplifies tax obligations by helping businesses determine the correct filing frequency and manage tax reporting seamlessly.

Understanding Indiana Sales Tax Filing Frequencies

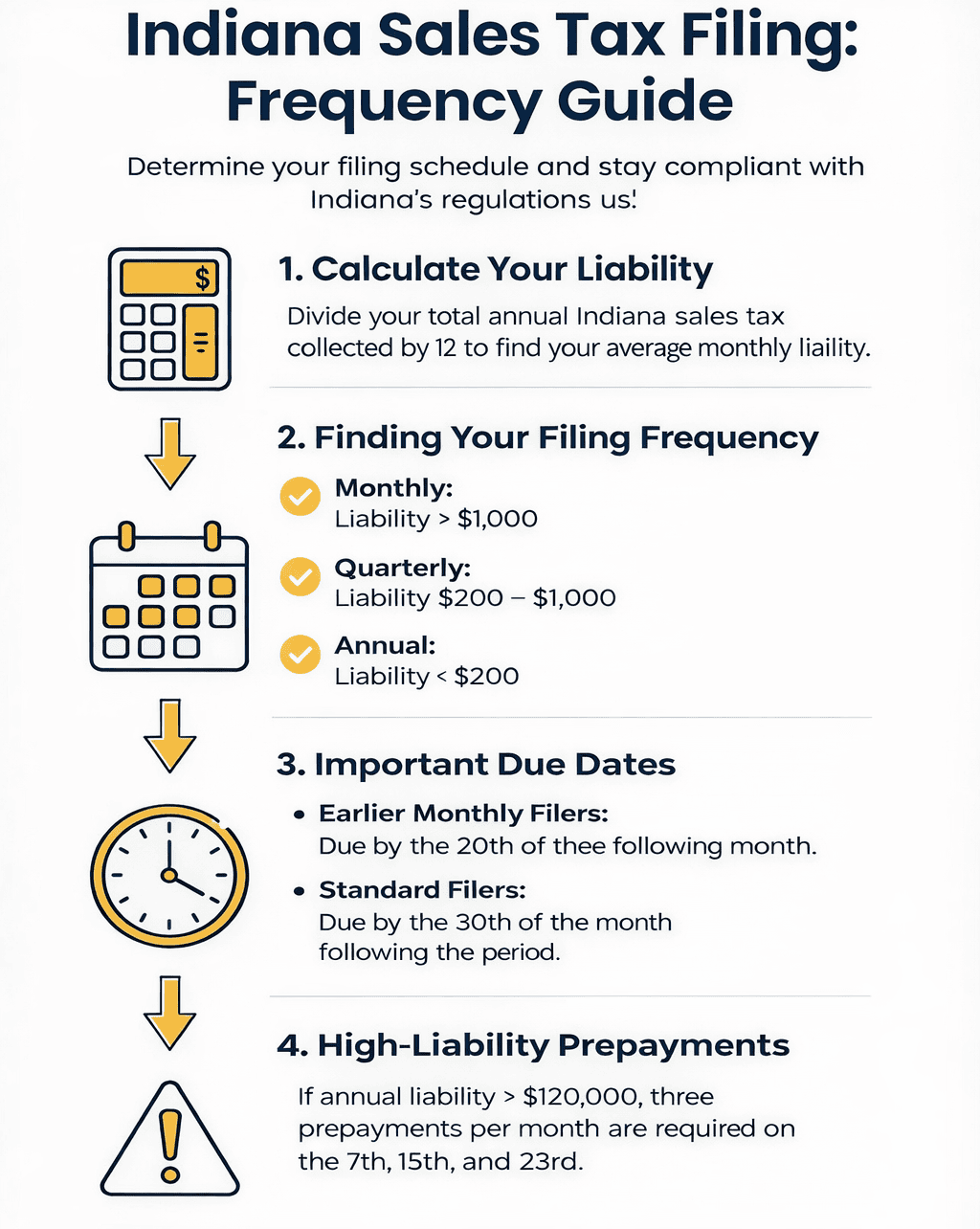

Indiana’s sales tax filing frequencies are based on a business’s average monthly tax liability, categorizing them into monthly, quarterly, or annual filings.

Overview of Filing Frequencies

Monthly Filing: Businesses with an average monthly sales tax liability exceeding $1,000 are required to file returns monthly.

Quarterly Filing: Those with an average monthly liability between $200 and $1,000 must file quarterly returns.

Annual Filing: Businesses with an average monthly liability below $200 are assigned an annual filing frequency.

These assignments ensure the state efficiently collects taxes while accommodating businesses of varying sizes.

Determining Your Business’s Filing Frequency

The Indiana DOR assigns filing frequencies based on your business’s average monthly tax liability.

Calculating Average Monthly Tax Liability

To determine your average monthly tax liability:

- Total Your Annual Taxable Sales: Calculate the total amount of taxable sales your business conducted in Indiana over the past year

- Compute Total Sales Tax Collected: Multiply your total taxable sales by Indiana’s sales tax rate of 7% to find the total sales tax collected

- Calculate the Average Monthly Liability: Divide the total sales tax collected by 12 to determine your average monthly tax liability

Example: If your business collected $24,000 in sales tax over the year:

- Average Monthly Liability: $24,000 ÷ 12 = $2,000

Based on this calculation, your business would be assigned a monthly filing frequency.

Filing Frequency Decision Guide

Use this simple logic to determine your filing status:

Step 1: Calculate your average monthly tax liability using the formula above.

Step 2: Match your liability to the appropriate filing frequency:

- Less than $200/month → Annual filing

- $200 to $1,000/month → Quarterly filing

- More than $1,000/month → Monthly filing

Step 3 (New Businesses): If you have no prior history, the DOR will assign an initial frequency based on your projected sales. Monitor your actual collections and request adjustments if needed.

Step 4 (Mid-Year Changes): If your liability increases or decreases significantly during the year, contact the DOR to discuss potential filing frequency adjustments.

Due Dates and Compliance

Adhering to the correct Indiana sales tax filing frequency and meeting due dates is essential for maintaining compliance and avoiding penalties.

Understanding Earlier Filers vs. Standard Monthly Filers

Indiana has a unique dual due date system for monthly filers:

Earlier Filers: Businesses averaging more than $1,000 per month in sales tax liability during the previous calendar year must file by the 20th day of the month following the tax period.

Standard Monthly Filers: Businesses averaging less than $1,000 per month in sales tax liability during the previous calendar year file by the 30th day of the month following the tax period.

How Earlier Filer Status is Assigned:

- The DOR reviews your previous calendar year’s collections

- If your average monthly liability exceeded $1,000, you’re assigned earlier filer status for the following year

- You’ll receive official notification from the DOR of this designation

Filing Frequency Comparison Table

| Filing Status | Average Monthly Liability | Due Date | Example |

| Earlier Filer (Monthly) | More than $1,000 (prior year) | 20th of following month | January sales due Feb 20 |

| Standard Monthly Filer | Less than $1,000 (prior year) | 30th of following month | January sales due Jan 30 |

| Quarterly Filer | $200 to $1,000 | 30th of month after quarter end | Q1 (Jan-Mar) due April 30 |

| Annual Filer | Less than $200 | 30th of following January | 2024 sales due Jan 30, 2025 |

Important: If a due date falls on a weekend or state holiday, the return is due the next business day.

Quarter-Monthly Prepayment Requirements

For high-liability businesses, Indiana requires additional prepayments throughout the month.

Who Must Make Quarter-Monthly Prepayments:

- Businesses with annual sales tax liability exceeding $120,000 (approximately $10,000+ per month)

- The DOR will notify you if you’re required to participate in this program

How Quarter-Monthly Prepayments Work:

- You must make three prepayments during each month, covering approximately one week of tax liability each

- Prepayment due dates are typically the 7th, 15th, and 23rd of each month

- Each prepayment should equal roughly 25% of your expected monthly liability

- You still file a complete monthly return by your regular due date (20th or 30th of the following month)

Example: If your monthly liability is $12,000:

- First prepayment (due 7th): $3,000

- Second prepayment (due 15th): $3,000

- Third prepayment (due 23rd): $3,000

- Final payment with monthly return: $3,000 (plus any adjustments)

Penalties for Missing Prepayments:

- Each missed or late prepayment incurs a 10% penalty

- Interest accrues from the original due date

- Consistent failure to prepay can result in increased scrutiny from the DOR

Penalties for Late Filing or Payment

Timely filing and payment are crucial to avoid penalties:

- Late Filing: A penalty of 10% of the unpaid tax liability or $5.00, whichever is greater

- Late Payment: A penalty of 10% of the unpaid tax is assessed if the tax is not paid by the due date

- Failure to File After DOR Notification: A penalty of 20% of the unpaid tax liability is imposed

- Fraudulent Intent: A 100% penalty of the unpaid tax

Interest may also accrue on unpaid taxes from the original due date until the tax is paid in full.

Adjusting Filing Frequencies

Fluctuations in your business’s tax liability can necessitate adjustments to your assigned filing frequency.

Changes in Tax Liability

Increased Tax Liability: If your average monthly tax liability surpasses your current filing threshold, the DOR may shift you to a more frequent filing schedule. This could also trigger quarter-monthly prepayment requirements if you exceed $120,000 in annual liability.

Decreased Tax Liability: A significant reduction in tax liability could result in a less frequent filing requirement, potentially reducing your administrative burden.

Requesting a Change

If you believe your assigned filing frequency no longer aligns with your business’s tax activity:

- Contact the DOR: Reach out to the Indiana DOR to discuss your situation

- Provide Documentation: Be prepared to submit records demonstrating the change in your tax liability

- Await Confirmation: The DOR will review your request and notify you of any adjustments

Regularly reviewing your tax liabilities and maintaining open communication with the DOR ensures your filing frequency remains appropriate.

Utilizing INTIME for Efficient Filing

The Indiana Taxpayer Information Management Engine (INTIME) is the DOR’s online portal for efficient sales tax management.

Benefits of INTIME

- 24/7 Access: File returns, make payments, and manage tax accounts at any time

- Secure Communication: Directly message DOR customer service within the portal

- Electronic Record-Keeping: Access and store tax documents electronically

- Account Management: Update business information and manage multiple locations seamlessly

Registration and Navigation

Create an Account:

- Visit the INTIME portal

- Click on “New to INTIME? Sign up”

- Select “Business” to manage business tax accounts

- Provide your FEIN and legal business name

- Validate your account using a recent Letter ID from the DOR

- Create a username and password to complete registration

By leveraging INTIME’s comprehensive features, businesses can ensure timely and accurate sales tax filings.

Best Practices for Compliance

Maintaining compliance with Indiana’s sales tax regulations requires diligent record-keeping and staying informed.

Record-Keeping

The Indiana DOR mandates that businesses retain all pertinent sales records, including invoices, receipts, and financial statements, for at least three years. This documentation supports the figures reported on tax returns and is crucial during audits.

Staying Informed

Tax laws and filing requirements can change. Regularly consulting the Indiana DOR’s Sales Tax Information Bulletins provides insights into current regulations. Additionally, subscribing to the DOR’s updates ensures timely information delivery.

Given the complexities of tax compliance, partnering with professionals can be beneficial. HOST’s sales tax services offer expertise in managing sales tax obligations, allowing you to focus on your core business activities.

Simplify Indiana Sales Tax Compliance with HOST

Managing Indiana sales tax filing frequency can be complex, with different due dates, changing tax liabilities, and evolving regulations. Hands Off Sales Tax (HOST) provides expert guidance to ensure businesses stay compliant while minimizing administrative burdens.

Filing Frequency Assessment & Adjustments

HOST helps businesses determine the correct filing frequency: monthly, quarterly, or annually, based on their tax liabilities. If your tax obligations fluctuate, HOST assists in filing requests with the DOR to modify your assigned frequency.

Accurate Sales Tax Filings & Payment Management

With HOST, businesses can streamline their sales tax processes by:

- Preparing and filing accurate Indiana ST-103 Sales Tax Returns on time

- Managing quarter-monthly prepayments for high-liability businesses

- Maintaining organized records to avoid compliance issues and penalties

Audit Support & Compliance Monitoring

In case of an audit, HOST provides expert audit defense services, ensuring your business is prepared with proper documentation and responses. Additionally, HOST keeps you updated on tax law changes, preventing compliance risks before they arise.

Stay Compliant and Avoid Sales Tax Pitfalls

Understanding and adhering to Indiana sales tax filing frequency is essential for keeping your business compliant and avoiding unnecessary penalties. Whether you file monthly, quarterly, or annually, or need to manage quarter-monthly prepayments, timely and accurate reporting is key to preventing costly errors.

Staying informed about tax law changes and leveraging tools like INTIME can simplify compliance, but managing these tasks can be overwhelming. That’s where Hands Off Sales Tax (HOST) comes in. From filing frequency assessments to audit support, HOST ensures your business stays compliant without the hassle.

Contact HOST today for expert guidance and a stress-free tax solution!

Frequently Asked Questions

What is the difference between an “earlier filer” and a standard monthly filer in Indiana?

Earlier filers are businesses that averaged more than $1,000 per month in sales tax liability during the previous calendar year and must file by the 20th of the following month. Standard monthly filers averaged less than $1,000 per month and file by the 30th. The DOR assigns this status annually based on your prior year’s collections.

How do I know which filing frequency applies to my business?

Calculate your average monthly tax liability by dividing your total annual sales tax collected by 12. If it’s less than $200, you file annually. Between $200-$1,000, you file quarterly. Over $1,000, you file monthly. The DOR will officially notify you of your assigned frequency.

What are quarter-monthly prepayments and do I need to make them?

Quarter-monthly prepayments are required for businesses with annual sales tax liability exceeding $120,000 (roughly $10,000+ per month). You must make three prepayments during each month (typically on the 7th, 15th, and 23rd), each covering approximately 25% of your monthly liability, plus file a regular monthly return.

What happens if I miss a quarter-monthly prepayment deadline?

Each missed or late quarter-monthly prepayment incurs a 10% penalty, plus interest from the original due date. Consistent failure to make prepayments can result in increased scrutiny from the Indiana DOR.

Can my filing frequency change during the year?

Yes. If your tax liability increases or decreases significantly, you can contact the DOR to request a filing frequency adjustment. The DOR may also proactively change your frequency based on reviewing your collections. You’ll receive official notification of any changes.

How can HOST help my business with Indiana sales tax filing?

HOST provides comprehensive Indiana sales tax services, including determining your correct filing frequency, managing quarter-monthly prepayments, filing accurate returns on time, maintaining organized records, handling DOR notices, and providing audit defense. We take the complexity out of Indiana sales tax compliance so you can focus on running your business.