Navigating Texas software sales tax can be challenging for businesses selling or purchasing digital products. With different tax rules for prewritten software, custom programs, and Software as a Service (SaaS), understanding taxability is crucial to avoid overpayment or non-compliance. Texas considers software tangible personal property, but exemptions and tax reductions apply in certain cases.

This guide breaks down the taxability of software in Texas, ensuring you stay compliant. For expert assistance, Hands Off Sales Tax (HOST) offers tailored support to help businesses manage software-related sales tax complexities and avoid costly mistakes.

Overview of Texas Sales Tax

In Texas, the state imposes a base sales tax rate of 6.25%. Local jurisdictions including cities, counties, special purpose districts, and transit authorities, can levy additional sales taxes. However, the combined local sales tax rate cannot exceed 2%, resulting in a maximum possible sales tax rate of 8.25% within the state.

For instance, a business located within the city limits of Corpus Christi falls under three local taxing jurisdictions: the city of Corpus Christi, the Corpus Christi Crime Control and Prevention District, and the Corpus Christi Regional Transit Authority. Collectively, these jurisdictions impose a total local sales tax rate of 2%, which, when added to the state’s 6.25%, results in a total sales tax rate of 8.25% for that area.

It’s important to note that local taxing jurisdiction boundaries do not align with U.S. postal ZIP codes. Therefore, businesses should verify the specific tax rates applicable to their locations. The Texas Comptroller’s office provides an online Sales Tax Rate Locator to assist in determining the correct rates by address.

Taxability of Software in Texas

In Texas, the taxability of software hinges on its classification and delivery method.

Tangible Personal Property Classification

Texas classifies computer programs as tangible personal property. Consequently, the sale, lease, or license of software (whether delivered on physical media or electronically) is subject to sales tax. This includes charges associated with the software, such as installation, modification, repair, maintenance, or restoration, regardless of whether these charges are separately stated.

Types of Software and Their Tax Implications

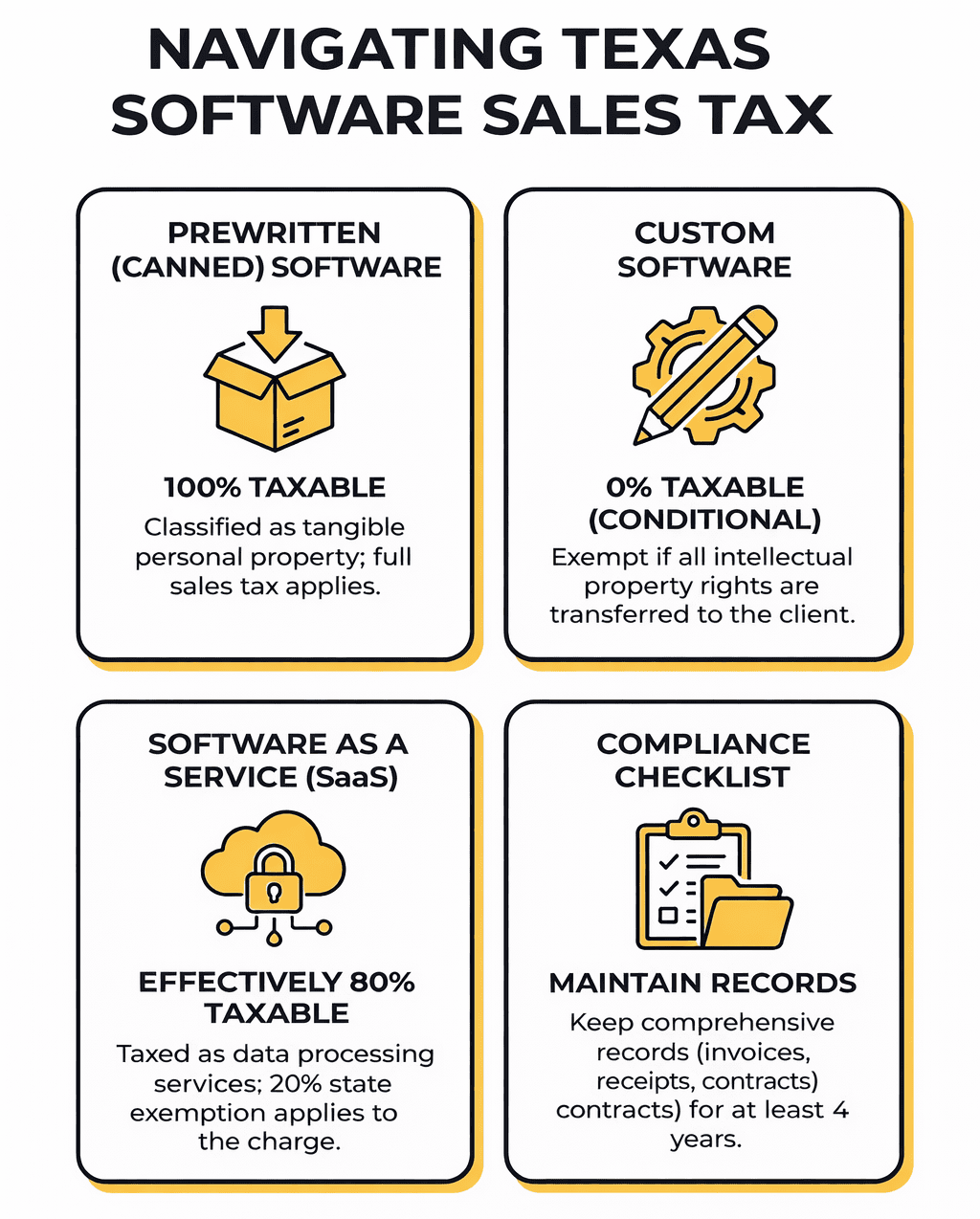

Prewritten (Canned) Software

Standardized software, commonly known as prewritten or “canned” software, is taxable in Texas. This applies to both physical and electronic deliveries.

Custom Software

Custom software developed specifically for a client may be exempt from sales tax if certain conditions are met. For instance, if all rights to the program are transferred to the customer, the transaction may qualify as non-taxable contract programming services. However, if the developer retains rights or uses the software for other clients, the exemption may not apply.

Software as a Service (SaaS)

In Texas, SaaS is treated as a taxable data processing service. Notably, Texas provides a 20% exemption on charges for data processing services, effectively taxing only 80% of the service charge. This means that businesses offering SaaS should apply sales tax to 80% of their service fees.

Understanding these distinctions is crucial for businesses to ensure compliance with Texas sales tax regulations and to avoid potential penalties.

Software Taxability Decision Framework

Determining whether your software is taxable in Texas requires analyzing several factors. Use this framework to classify your product:

Step 1: Identify the Software Type

Is the software prewritten (off-the-shelf)?

- Yes → Taxable (go to Step 4)

- No → Continue to Step 2

Is it custom-developed for a specific client?

- Yes → Continue to Step 2

- No → It’s likely SaaS (go to Step 3)

Step 2: Custom Software Analysis

For custom software to be non-taxable, all of these must be true:

✓ All intellectual property rights transfer to the customer

✓ The developer cannot reuse the code for other clients

✓ The contract explicitly states complete rights transfer

✓ No licenses or ongoing usage rights are retained by the developer

Missing even one requirement? → The software becomes taxable

Common disqualifiers:

- Developer retains any usage rights

- Software includes reusable components

- Similar software sold to other clients

- License agreement instead of full rights transfer

Step 3: SaaS Classification

Software delivered as a service (accessed remotely, not downloaded) is taxable as data processing in Texas.

Taxable at 80% of the fee (20% exemption applies)

This includes:

- Cloud-based applications

- Subscription software access

- Hosted software platforms

- Web-based tools and services

Step 4: Delivery Method Matters

Physical media (CD, USB)? → Fully taxable

Electronic download? → Fully taxable

Cloud access only? → Taxable as data processing (80% of fee)

Quick Reference Table

| Software Type | Taxability | Rate Applied |

| Prewritten/Off-the-shelf | Taxable | 100% of price |

| Custom (all rights transferred) | Not taxable | 0% |

| Custom (partial rights retained) | Taxable | 100% of price |

| SaaS/Cloud access | Taxable as data processing | 80% of price (20% exempt) |

| Software maintenance | Taxable | Same as underlying software |

| Installation services | Taxable | Same as underlying software |

Understanding SaaS Taxability in Texas

Texas’s treatment of SaaS creates confusion for many businesses. Software as a Service is taxable when it involves “data processing services” like the processing, storage, retrieval, or manipulation of information.

Taxable SaaS examples:

- Project management tools (Asana, Monday.com)

- CRM platforms (Salesforce, HubSpot)

- Accounting software accessed online (QuickBooks Online)

Pure SaaS Access

When customers only access software through a web browser without downloading:

Taxability: 80% of the subscription fee is taxable (20% exemption applies)

Example: A business pays $1,000/month for CRM access.

- Taxable amount: $800

- At 8.25% rate: $66 in sales tax

- Total charge: $1,066

SaaS with Training or Downloadable Components

Training bundled with SaaS is taxable as part of the overall service package. When SaaS includes downloadable software, the entire package may become fully taxable.

Best practice: Separate pricing for cloud access and downloadable components when possible, and document training as a distinct professional service when applicable.

The 20% Data Processing Exemption Explained

Texas offers a 20% exemption on data processing services, but applying it correctly is critical.

When the Exemption Applies

The 20% exemption applies to charges for processing information, maintaining databases, entering and retrieving data, word processing, payroll services, and data storage, including most SaaS products.

How to Show It on Invoices

Correct approach:

Monthly SaaS Subscription: $1,000.00

Sales Tax (8.25% on 80%): $66.00

Total: $1,066.00

Common Mistakes

Mistake #1: Applying the exemption to prewritten software downloads (100% taxable)

Mistake #2: Exempting 20% of ALL charges including setup fees (may be fully taxable)

Mistake #3: No documentation of how exemption was calculated

Mistake #4: Inconsistent application across customers

Data Processing and Information Services

In Texas, data processing services encompass activities involving information handling. According to the Texas Administrative Code, this includes word processing, payroll and business accounting, and computerized data storage or manipulation. Examples include entering inventory data, maintaining employee records, and preparing payroll.

SaaS is classified under data processing services in Texas, meaning businesses providing SaaS offer taxable data processing services with the 20% exemption applied.

Contract Programming Services

In Texas, contract programming services refer to creating custom software where the programmer transfers all rights to the client, including all intellectual property rights.

Tax Treatment

Non-Taxable Service: Such contract programming services are generally non-taxable in Texas because the transaction is viewed as a service rather than the sale of tangible personal property.

Critical Contract Language Requirements

For custom software to qualify as non-taxable, your contract must include:

- Explicit rights transfer: “All rights, title, and interest in the software, including all intellectual property rights, are hereby transferred to Client.”

- No retained rights: “Developer retains no rights to use, modify, distribute, or license the software to any other party.”

- Work-for-hire designation: “This software is developed as a work made for hire, and Client shall be deemed the author and sole owner.”

Contract Red Flags

These provisions make your software taxable:

❌ “Client is granted a license to use the software”

❌ “Developer may incorporate similar functionality in other projects”

❌ “Developer retains ownership of underlying code”

❌ “Annual license renewal required”

Documentation Best Practices

Maintain signed contracts, document the custom nature of development, preserve communications showing client-specific customization, and keep proof that no other clients use the same code.

Exemptions and Exclusions

In Texas, certain exemptions and exclusions apply to software sales, allowing businesses to optimize their tax obligations.

Resale Certificates

Businesses purchasing software with the intent to resell can utilize a resale certificate to avoid paying sales tax at the point of purchase. By providing a properly completed Form 01-339, Texas Sales and Use Tax Resale Certificate, the buyer certifies that the software is for resale purposes.

Important: If the purchaser uses the software instead of reselling it, they become liable for the sales tax.

Common resale certificate misuse that triggers audits:

❌ Using certificates for internal software (software you use in your business is not for resale)

❌ Reselling to end users without collecting tax (you must collect tax when you resell)

❌ Expired or incomplete certificates (keep current, fully completed certificates on file)

❌ Accepting certificates from non-Texas buyers (out-of-state buyers need different documentation)

Interstate Commerce Considerations

When selling software to out-of-state customers, Texas-based sellers generally are not required to collect Texas sales tax, provided the software is delivered electronically and the seller does not have a physical presence in the customer’s state.

However, if the seller has a significant presence, or “nexus,” in the customer’s state, they may be obligated to collect that state’s sales tax. It’s essential for businesses to understand the specific tax laws of each state they operate in to ensure compliance.

Critical nexus triggers for software companies:

- Physical office or employees in the state

- Inventory or servers in the state

- Regular travel to the state for sales or service

- Exceeding economic nexus thresholds ($100,000 in sales or 200 transactions in most states)

- Affiliate relationships in the state

- Drop-shipping arrangements involving the state

By leveraging resale certificates appropriately and understanding interstate commerce tax obligations, businesses can effectively manage their tax responsibilities related to software transactions.

Compliance and Best Practices

Maintaining compliance with Texas software sales tax regulations requires diligent record-keeping and staying informed about tax law changes.

Record-Keeping

Businesses must retain comprehensive records of all software sales and purchases for at least four years. This includes invoices, receipts, contracts, and any related documents. Such records are essential for accurate tax reporting and are crucial during audits.

If the Texas Comptroller’s office initiates an audit, it’s advisable to keep all pertinent records until the audit concludes, even if it extends beyond the standard four-year period.

Essential records to maintain:

- Sales invoices showing tax calculations

- Contracts (especially for custom software claiming exemptions)

- Resale certificates from customers

- Documentation of software type and delivery method

- Records of the 20% data processing exemption application

- Correspondence with customers about taxability

- Vendor invoices for software purchases

Staying Informed

Tax laws, especially those concerning software and digital products, can evolve. To remain compliant:

Regularly Consult Official Resources: The Texas Comptroller’s website offers updates on sales tax regulations, publications, and announcements.

Subscribe to Updates: The Tax Policy News newsletter provides insights into recent legislative changes, policy updates, and procedural modifications.

By maintaining detailed records and staying informed through reliable sources, businesses can navigate Texas’s software sales tax landscape more effectively and avoid potential compliance issues.

Audit Risk Indicators for Software Businesses

The Texas Comptroller targets specific patterns when auditing software companies:

High-Risk Audit Triggers

- SaaS Misclassification

- Reporting zero taxable sales despite offering SaaS products

- Classifying all SaaS as exempt rather than applying the 80% taxable rule

- Inconsistently applying data processing treatment

Audit prevention: Document your SaaS taxability analysis and consistently apply the 20% exemption.

- Overuse of Resale Certificates

- High percentage of sales claimed as resale (>30-40% is unusual)

- Accepting resale certificates from end-user customers

- Missing or incomplete certificates on file

Audit prevention: Verify customers are legitimate resellers and maintain complete, current certificates.

- Incorrect Nexus Assumptions

- Not collecting tax on Texas sales despite having Texas nexus

- Assuming cloud-based delivery creates no nexus

- Ignoring economic nexus thresholds

Texas economic nexus threshold: $500,000 in Texas sales in the preceding 12 months

- Custom Software Documentation Gaps

- Contract language doesn’t clearly transfer all rights

- Multiple customers use “custom” software with similar features

- No documentation of custom specifications

- Inconsistent Tax Treatment

- Different tax treatment for similar products

- No written policy on tax classification

- Manual calculations without supporting methodology

What To Do If Selected for Audit

- Don’t panic – audits are routine and manageable with proper preparation

- Engage a sales tax professional immediately (like HOST)

- Gather all requested documentation promptly and completely

- Don’t volunteer information beyond what’s requested

- Review your exposure across all states, not just Texas

- Consider a Voluntary Disclosure Agreement if you discover other compliance gaps

HOST provides comprehensive audit defense services, managing communications with tax authorities and working to minimize your liability.

Common Pitfalls and How to Avoid Them

Navigating Texas’s sales tax regulations for software can be challenging. Businesses often encounter common pitfalls:

Misclassification of Software

Prewritten Software: Both physical and electronically delivered prewritten software are taxable as tangible personal property in Texas.

Custom Software: If a developer creates custom software and transfers all rights to the client, this service is generally non-taxable. However, retaining any rights renders the transaction taxable.

To avoid misclassification, thoroughly understand the distinctions between software types and ensure accurate categorization.

Overlooking Data Processing Exemptions

Texas imposes sales tax on data processing services with a 20% exemption, meaning only 80% of the total charge is taxable. Failing to apply this exemption leads to overpayment. Ensure you correctly apply the 20% exemption to eligible data processing services.

Improper Use of Resale Certificates

Accepting incomplete or invalid resale certificates, or accepting them from end users (not resellers), creates significant audit risk.

Best practices:

- Verify the customer is a registered reseller

- Ensure Form 01-339 is completely filled out

- Keep certificates on file for at least four years

Bundling Issues

When software is bundled with hardware, maintenance, or services, the entire package may become taxable.

Solution: Separately state and price each component when possible, and document the distinct nature of services.

Simplifying Texas Software Sales Tax Compliance with HOST

Navigating Texas software sales tax can be complex, with varying tax rules for prewritten software, SaaS, data processing services, and exemptions. Misclassifications, overlooked exemptions, or incorrect filings can lead to overpayment or costly penalties.

Hands Off Sales Tax (HOST) provides expert solutions to help businesses stay compliant while minimizing tax liabilities.

Expert Software Sales Tax Review

Many businesses use tax software like TaxJar or Avalara. However, they may be unknowingly overpaying sales tax due to misclassified transactions or incorrect software settings.

HOST offers a free sales tax software review, ensuring your tax settings are optimized for compliance and cost efficiency.

Comprehensive Tax Compliance Services

Sales Tax Filings & Remittance – HOST manages the complexities of filing, ensuring accurate and timely submissions.

Audit Defense – If your business faces an audit, HOST provides expert representation and strategic guidance.

Nexus Analysis – HOST determines where your business has tax obligations, helping you register in the right jurisdictions.

Resale Certificate Management – Assistance in properly documenting resale transactions to prevent unnecessary tax charges.

With HOST’s specialized knowledge of Texas software sales tax laws, businesses can confidently navigate compliance while reducing financial risks.

Ensure Compliance and Avoid Overpaying Sales Tax

Understanding Texas software sales tax is essential for businesses to stay compliant and avoid unnecessary costs. From prewritten and custom software to SaaS and data processing services, different tax treatments can impact your bottom line.

Misclassification, overlooking exemptions, or failing to apply the 20% data processing deduction can lead to overpayment or penalties.

Hands Off Sales Tax (HOST) simplifies the process by offering expert sales tax guidance, software reviews, and compliance solutions.

Don’t leave your tax obligations to chance—schedule a consultation with HOST today and ensure your business is tax-compliant and cost-efficient.

Frequently Asked Questions

Is all software taxable in Texas?

Not necessarily. Prewritten software (whether downloaded or on physical media) is fully taxable. Custom software where all rights transfer to the customer is non-taxable. SaaS is taxable as data processing, but only 80% of the charge (a 20% exemption applies).

How does the 20% data processing exemption work for SaaS?

When you charge $1,000 for SaaS, only $800 is subject to sales tax. You apply the exemption by calculating tax on 80% of your fee. This exemption applies specifically to data processing services, which includes most SaaS products.

What makes custom software non-taxable in Texas?

For custom software to be non-taxable, ALL intellectual property rights must transfer to the customer, the developer cannot retain any rights to reuse the code, and the contract must explicitly state this complete transfer. If any rights are retained or the software can be used for other clients, it becomes taxable.

Do I need to collect Texas sales tax on software sold to out-of-state customers?

Generally, no. If the software is delivered electronically and you have no physical presence in the customer’s state. However, you may need to collect that state’s sales tax if you have nexus there. Each state has different rules, so multi-state sellers should conduct a nexus analysis.

What’s the difference between taxing prewritten software and SaaS?

Prewritten software (downloaded or on physical media) is 100% taxable. SaaS (cloud-accessed software) is taxable as a data processing service with a 20% exemption, so only 80% of the charge is taxable. The delivery method and access model determine which treatment applies.

Can I use a resale certificate when purchasing software for my business?

Only if you’re genuinely purchasing the software to resell it to customers. You cannot use a resale certificate for software you’ll use internally in your business operations. Misusing resale certificates is a common audit trigger.

What documentation do I need for custom software exemptions?

You need a contract explicitly stating that all rights transfer to the customer, no rights are retained by the developer, and the software is custom-built exclusively for that customer. Maintain project documentation, specifications, and delivery records showing the custom nature of the work.

What should I do if I discover I’ve been misclassifying software?

Contact a sales tax professional immediately (like HOST) to assess your exposure. Consider filing amended returns for recent periods or pursuing a Voluntary Disclosure Agreement (VDA) to limit lookback periods and potentially reduce penalties. Don’t wait. The Texas Comptroller may discover the issue first during an audit.

Are software maintenance and support services taxable?

Yes, if they’re related to taxable software. Maintenance, updates, and support for prewritten software are taxable. For SaaS, ongoing support is typically included in the data processing service charge (taxable at 80%). For non-taxable custom software, maintenance may also be non-taxable if structured correctly.

How often does Texas audit software companies?

While audit frequency varies, software companies face higher scrutiny due to common classification issues. Red flags include significant sales with minimal tax collected, overuse of resale certificates, and SaaS misclassification. Proper documentation and consistent tax treatment significantly reduce audit risk.