In 2026, the Florida Department of Revenue (FDOR) has moved toward high-velocity “eAudits,” using sophisticated cross-agency data matching to identify discrepancies in real-time. Whether you are a local retailer or a remote seller reaching Florida customers, compliance is a dynamic target governed by Chapter 212 of the Florida Statutes.

The stakes are higher this year. With the floating interest rate set at 11% for the first half of 2026, a small error can quickly snowball into a significant liability. However, Florida’s legal framework also provides vital protections—from the 60-day preparation window to the Certified Audit Program.

At Hands Off Sales Tax (HOST), we specialize in insulating your business from the stress of FDOR scrutiny. This guide breaks down the 2026 audit lifecycle, providing the “insider” knowledge needed to protect your revenue and ensure your business remains in good standing.

Overview of Sales Tax Audits in Florida

In Florida, the sales tax landscape is aggressively monitored by the Florida Department of Revenue (FDOR). Understanding the purpose and legal scaffolding of an audit is the first step toward safeguarding your business from high-interest liabilities and state-level penalties.

What is a Sales Tax Audit?

A sales tax audit is a comprehensive forensic review of your business’s financial ecosystem. The primary goal is to ensure that the 6% state tax (plus any local surtax) was correctly collected from customers and fully remitted to the state.

The FDOR’s core objectives are three-fold:

- Compliance Enforcement: Verifying that businesses are adhering to the “trust fund” nature of sales tax—money collected from customers belongs to the state from the moment of transaction.

- Revenue Protection: Identifying underreported sales or improper exemptions to recover unpaid state funds.

- Market Fairness: Ensuring a level playing field so that compliant businesses aren’t at a competitive disadvantage against those evading taxes.

The Legal Framework: Chapter 212

Florida’s sales tax authority is derived from Chapter 212 of the Florida Statutes. Navigating an audit requires a technical understanding of four critical sections that auditors use as their primary “playbook.”

1. Section 212.12 – Records and Returns

This section is the foundation of audit preparation. It mandates that every dealer must maintain “suitable” records of all sales and purchases for a minimum of three years.

- The “Burden of Proof”: In Florida, the burden is on the taxpayer, not the state. If you cannot produce an invoice or an exemption certificate, the FDOR legally presumes the transaction is taxable.

- Digital Standards: The FDOR increasingly utilizes “eAudits.” Under this section, your electronic records must be accessible and provided in a format (like Excel or CSV) that allows for automated verification.

2. Section 212.15 – Penalties for Non-Compliance

Failure to remit collected taxes is treated with extreme severity in Florida, often categorized as theft of state funds.

- Standard Penalties: A 10% penalty is typical for negligence. However, if the FDOR suspects willful intent to evade, this can jump to 50% or even 100% of the tax due.

- 2026 Interest Rates: Per TIP #25ADM-03, the floating interest rate for the first half of 2026 is 11%. Unlike penalties, interest is rarely waived and accrues daily.

- Criminal Exposure: Under Section 212.15(2), failing to remit more than $300 in collected tax can be prosecuted as a third-degree felony, punishable by up to 5 years in prison.

3. Section 212.05 – Sales Price and Taxability

Auditors use this section to determine the “taxable base.” A common trap for Florida businesses is the miscalculation of what should be included in the sales price.

- Bundled Services: If you combine a taxable good with a non-taxable service (like delivery or installation) on a single invoice without itemization, the FDOR may tax the entire amount.

- Occasional Sales: While isolated sales are generally exempt, Section 212.05 imposes strict rules on titled items like boats, aircraft, and motor vehicles.

4. Section 212.08 – Statutory Exemptions

This is the most scrutinized area of any audit. Whether you are claiming an exemption for manufacturing, nonprofit status, or resale, the paperwork must be perfect.

- The 90-Day Rule: To be valid, a resale or exemption certificate (like Form DR-13) should ideally be obtained at the time of sale. If missing, you have a limited window to retrieve it before the auditor assesses the tax.

- Specific 2026 Nuance: Auditors are currently focusing on the repeal of commercial rent tax (effective 10/1/25). While rent is no longer taxed, they will meticulously review your 2023–2025 records to ensure compliance before the repeal date.

Common Triggers for a Sales Tax Audit

A sales tax audit in Florida can be initiated for various reasons. Understanding these triggers can help businesses avoid unnecessary scrutiny and maintain compliance.

Quantifying Your Audit Risk

Understanding your actual audit exposure helps prioritize compliance efforts effectively:

Industry-Specific Audit Rates:

- Retail and hospitality sectors experience audit rates of approximately 8-12% annually due to complex exemption scenarios and high transaction volumes

- Construction businesses face audit rates near 10-15%, primarily due to contractor exemption certificate management and varying taxability of services versus materials

- E-commerce and remote sellers see increasing audit attention, with approximately 6-8% audit rates as FDOR focuses on economic nexus compliance post-Wayfair

- Professional services and consulting firms typically experience lower audit rates (3-5%) but face scrutiny when service classifications blur

Threshold Indicators:

The FDOR typically flags businesses when discrepancies exceed specific thresholds:

- Sales variations of 15% or more between reporting periods without documented business changes

- Taxable sales-to-total sales ratios that deviate significantly from industry norms (typically flagged at 20%+ variance)

- Exemption certificate usage exceeding 30% of total transactions without proper documentation

- Consistent filing of zero or minimal tax liability despite substantial gross receipts

- Businesses reporting more than $500,000 in annual sales with disproportionately low tax remittance

Discrepancies in Reported Sales

Why It Triggers Audits:

Significant inconsistencies between reported sales and actual revenue are one of the most common red flags for the Florida Department of Revenue (FDOR).

Common Mismatch Scenarios:

- Gross receipts reported on federal tax returns that substantially exceed sales reported on Florida returns (typical trigger: 10%+ variance)

- Credit card processing statements showing higher transaction volumes than reported taxable sales

- Third-party marketplace reports (Amazon, eBay, etc.) indicating unreported Florida sales

- Bank deposit records inconsistent with reported revenue streams

- Wholesale versus retail transaction misclassifications that understate taxable sales

Importance of Accurate Reporting:

Regularly reconciling financial data across all reporting platforms ensures consistency and reduces the risk of triggering an audit. Implement monthly cross-checks between your accounting system, merchant processing statements, and tax filings.

Industry-Specific Factors

Higher Risk Industries:

Certain industries, like retail, hospitality, and construction, are audited more frequently due to complex tax rules and higher instances of non-compliance. These sectors often deal with exemptions, varying tax rates, or large cash transactions, increasing the likelihood of errors.

Random Selection

Purpose of Random Audits:

To maintain fairness, the FDOR sometimes selects businesses at random for audits. This ensures consistent enforcement of tax laws across all industries, even when no specific discrepancies are evident.

By addressing these common triggers proactively, businesses can reduce their audit risk and strengthen compliance efforts.

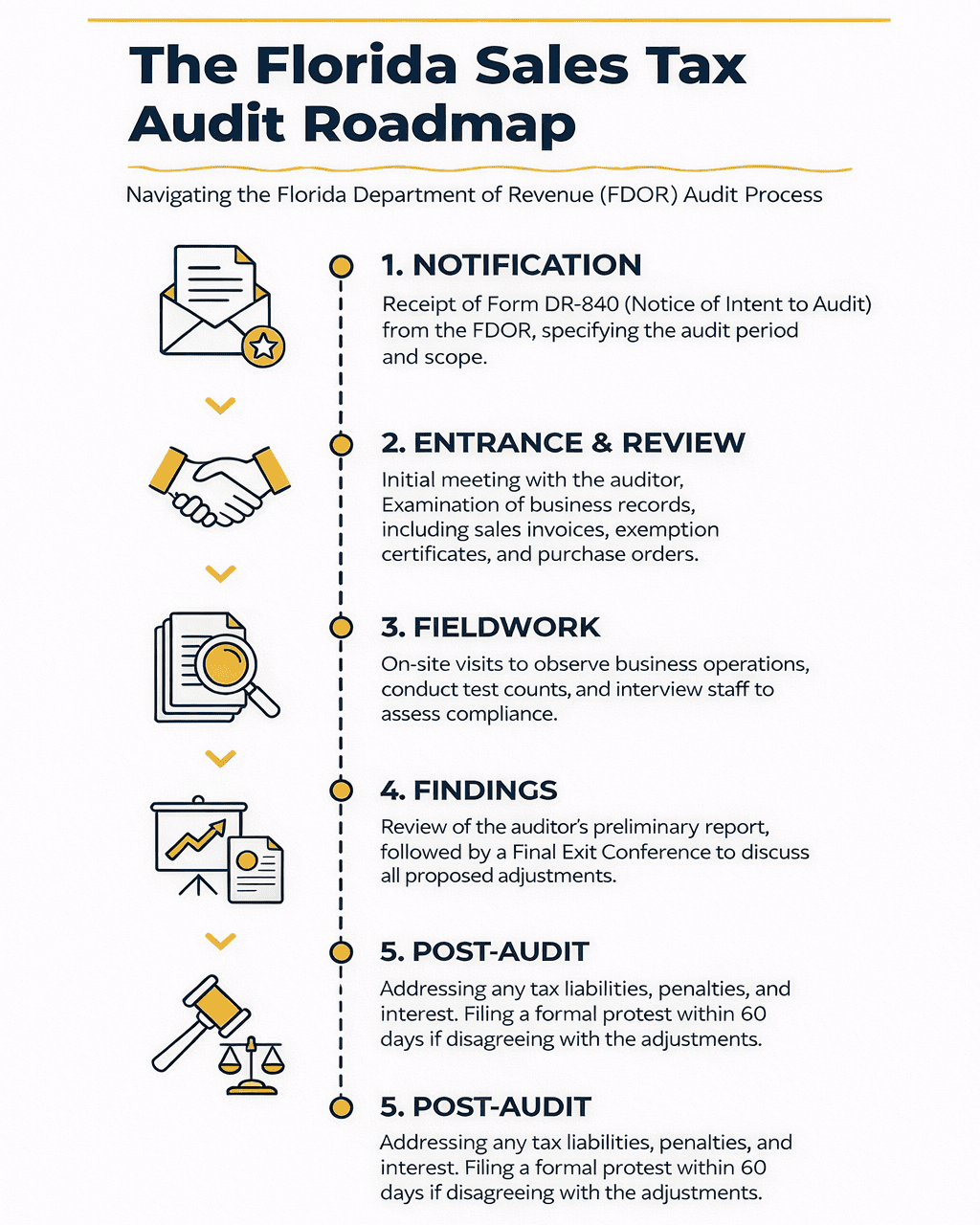

The Florida Sales Tax Audit Process

The Florida sales tax audit process is structured to ensure transparency and compliance. Understanding each phase helps businesses prepare effectively and avoid unnecessary complications.

The Florida sales tax audit process is structured to ensure transparency and compliance. Understanding each phase helps businesses prepare effectively and avoid unnecessary complications.

Notification

Audit Initiation:

The process begins with the Florida Department of Revenue issuing a Notice of Intent to Audit Books and Records (Form DR-840). This document outlines the scope of the audit and the records required.

Preparation Timeline:

Businesses are typically given 60 days to gather and submit the requested documents. Prompt organization is crucial during this phase.

Entrance Conference

Purpose of the Meeting:

The entrance conference introduces the auditor and establishes the audit’s objectives, timeline, and required cooperation.

Key Discussion Points:

- Scope of the audit.

- Documentation requirements.

- Clarifications on any business-specific complexities.

Examination of Records

Records Reviewed:

Commonly audited records include sales invoices, exemption certificates, tax returns, and purchase orders. Electronic records may also be reviewed in an eAudit format.

Importance of Accurate Records:

Disorganized or incomplete records can lead to extended audits or additional penalties.

Fieldwork

On-Site Visits:

Auditors may visit the business location to observe operations and ensure records align with activities.

Staff and management may be interviewed for clarification.

Preliminary Findings

Presentation of Findings:

Auditors present their initial findings and allow businesses to provide additional documentation or explanations to address discrepancies.

Exit Conference

Audit Report Presentation:

In the final meeting, the auditor presents the complete report, outlining assessed taxes, penalties, and interest.

Taxpayer Rights:

Businesses have the right to dispute findings or request clarification on assessments.

By understanding this process, businesses can navigate audits confidently while safeguarding their operations.

Taxpayer Rights and Responsibilities

Understanding your rights and responsibilities during a sales tax audit in Florida is key to navigating the process smoothly. The Florida Department of Revenue (FDOR) ensures transparency and fairness while requiring businesses to fulfill specific obligations.

Rights

Right to Professional and Courteous Treatment:

Taxpayers are entitled to respectful and professional interactions throughout the audit. Auditors are expected to maintain impartiality and adhere to ethical standards.

Right to Confidentiality of Tax Information:

All information provided during the audit is confidential and protected under Florida law. Unauthorized disclosure by auditors is prohibited.

Right to Understand Findings and Appeal:

Taxpayers have the right to receive a detailed explanation of audit findings and appeal any disputed results through proper channels.

Responsibilities

Accurate and Complete Records:

Businesses must maintain and provide comprehensive records, including sales invoices, exemption certificates, and tax returns. Missing or disorganized records can lead to penalties.

Cooperation with Auditor Requests:

Responding promptly to requests for information or clarifications is critical to avoiding delays or additional scrutiny.

Timely Communication:

Businesses are responsible for clear and timely communication with auditors to ensure the process moves forward efficiently.

Adhering to these rights and responsibilities helps protect businesses while fostering a collaborative audit process.

Preparing for a Sales Tax Audit Florida

Preparation is the key to minimizing stress and ensuring a smooth sales tax audit in Florida. By adopting effective practices in record-keeping, internal controls, and staff training, businesses can proactively address potential issues before they arise.

Record-Keeping Best Practices

Maintain Organized and Accessible Records:

Ensure all documents, such as sales invoices, exemption certificates, and tax returns, are properly organized and readily available. This reduces the risk of delays during the audit process.

Regularly Reconcile Sales and Taxes Collected:

Periodic reconciliation between sales reports and tax filings helps identify and correct discrepancies early.

Internal Controls

Accurate Tax Reporting Procedures:

Implement clear procedures for calculating and reporting sales tax to avoid errors. Automating processes can further enhance accuracy.

Conduct Internal Audits:

Periodic internal reviews ensure compliance and help uncover potential issues before an external audit occurs.

Staff Training

Educate Employees on Compliance:

Employees should be trained to understand sales tax laws and maintain accurate documentation. Knowledgeable staff can respond effectively to auditor queries.

By adopting these measures, businesses can reduce their audit risk, streamline the process, and safeguard their operations from penalties and non-compliance issues.

The Certified Audit Program: An Alternative Approach

The Certified Audit Program in Florida offers businesses a proactive and cooperative way to address sales tax compliance. This program, a collaboration between the Florida Department of Revenue (FDOR) and the Florida Institute of Certified Public Accountants (FICPA), encourages voluntary compliance while reducing audit-related stress.

Overview

Purpose and Benefits:

The Certified Audit Program allows businesses to work with an independent Certified Public Accountant (CPA) to conduct a thorough review of their tax compliance. If discrepancies are found, businesses can address them with the FDOR directly, often receiving waivers for penalties and reduced interest.

Eligibility Criteria

Businesses must meet specific criteria, including:

- A history of compliance with Florida tax laws.

- No ongoing audits or investigations at the time of application.

Application Process

Submit an application to the FDOR, which includes:

- A proposal detailing the scope of the audit.

- Agreement to address any findings promptly.

The FDOR will review and approve the application within a specified timeframe.

Conducting a Certified Audit

Taxpayer Responsibilities:

Work closely with the CPA to provide records, clarify discrepancies, and implement corrections.

Interaction with the FDOR:

Once the CPA completes the audit, the FDOR reviews the findings, ensuring compliance and issuing any necessary certifications.

This program fosters transparency and helps businesses resolve tax issues efficiently, avoiding the burdens of a formal audit.

Common Pitfalls and How to Avoid Them

Sales tax compliance is complex, and even small mistakes can lead to costly audits. Identifying common pitfalls and taking corrective measures can safeguard your business.

Misclassification of Taxable and Non-Taxable Sales

Examples and Corrective Measures:

Misclassifying taxable services as exempt or vice versa is a frequent error. For example, certain services like repairs may be taxable while others, like consulting, are exempt. Regularly review Florida’s taxability guidelines to ensure accuracy.

Incomplete or Missing Exemption Certificates

Importance of Certificates:

Failure to retain valid exemption certificates can result in tax assessments for otherwise exempt sales. Use digital tools to organize and track exemption certificates.

Errors in Sales Tax Calculation

Issues and Resources:

Incorrect application of tax rates or misallocations across jurisdictions can trigger audits. Use Florida’s tax rate lookup tool to ensure accuracy.

Failure to Reconcile Sales and Tax Returns

Why It Matters:

Regular reconciliation of sales data with filed tax returns can uncover discrepancies before an audit. Periodic internal audits are also helpful.

Delayed Responses to Auditor Inquiries

Consequences and Tips:

Non-responsiveness can lead to penalties or extended audits. Assign a dedicated contact to handle communication promptly and professionally.

By proactively addressing these pitfalls, businesses can minimize risks and maintain compliance.

Post-Audit Procedures

After a sales tax audit in Florida, understanding and addressing the results is crucial to resolving any discrepancies and minimizing financial impacts. Here’s how to navigate the post-audit process effectively.

Understanding Audit Results

Audit Report Breakdown:

The audit report provides a detailed summary of findings, including assessed taxes, penalties, and interest. Each section highlights discrepancies and areas of non-compliance.

Tip: Review the findings carefully to spot errors or miscalculations. Seek clarification from the auditor if any details seem inaccurate.

How to Interpret Liabilities:

Understand how liabilities were calculated, ensuring assessments align with the records provided. Errors can be disputed through formal channels.

Paying Assessed Taxes, Penalties, and Interest

Payment Methods and Deadlines:

Payments can be made electronically via the FDOR portal to avoid additional penalties or interest.

Installment Plans for Large Balances:

Businesses with substantial liabilities may request an installment plan to spread payments over time. This involves submitting a formal agreement to the FDOR.

Filing an Appeal

Disputing Audit Findings:

If you disagree with the audit results, file a written protest within 60 days of receiving the assessment notice. Include detailed explanations and supporting documentation.

Supporting Documentation:

Strengthen your case with relevant records and justifications. Appeals may progress to administrative hearings or formal litigation if unresolved.

By addressing post-audit procedures promptly, businesses can mitigate financial impacts and ensure compliance moving forward.

Simplify Your Sales Tax Audit with HOST

Facing a sales tax audit in Florida can be overwhelming, but Hands Off Sales Tax (HOST) offers the expertise and support you need to navigate the process smoothly. With years of experience and a client-focused approach, HOST is dedicated to safeguarding your business against tax risks. Whether you’re preparing for an audit or aiming to strengthen compliance, HOST provides the expertise you need.

Audit Defense Services

Comprehensive Representation:

HOST’s audit defense team manages every step of the audit process, from responding to notices to liaising directly with auditors. This minimizes disruptions and ensures your rights are protected.

Error Mitigation:

If discrepancies arise, HOST works to resolve them efficiently, helping reduce penalties and interest.

Proactive Compliance Solutions

Sales Tax Registration: HOST simplifies obtaining and maintaining sales tax permits, ensuring compliance across all jurisdictions.

Automated Sales Tax Filing and Remittance: Filing frequency can vary based on sales volume, adding complexity. HOST automates the filing and remittance process, guaranteeing timely submissions to avoid penalties and maintain compliance.

Nexus Analysis: Identify where your business owes sales tax to avoid unexpected audits.

Voluntary Disclosure Agreements (VDAs): If you have unpaid taxes, HOST can negotiate reduced penalties and interest through voluntary disclosure agreements.

Closing the Compliance Gap with Confidence

Navigating a sales tax audit in Florida requires preparation, clarity, and the right support. By understanding the process, avoiding common pitfalls, and addressing post-audit procedures effectively, businesses can stay compliant and protect their operations from unnecessary penalties.

When it comes to expert assistance, Hands Off Sales Tax (HOST) is your trusted partner. With tailored solutions for audits, compliance, and proactive tax management, HOST takes the burden off your shoulders. Don’t let tax challenges derail your business. Reach out to HOST today for a personalized consultation and ensure your peace of mind.