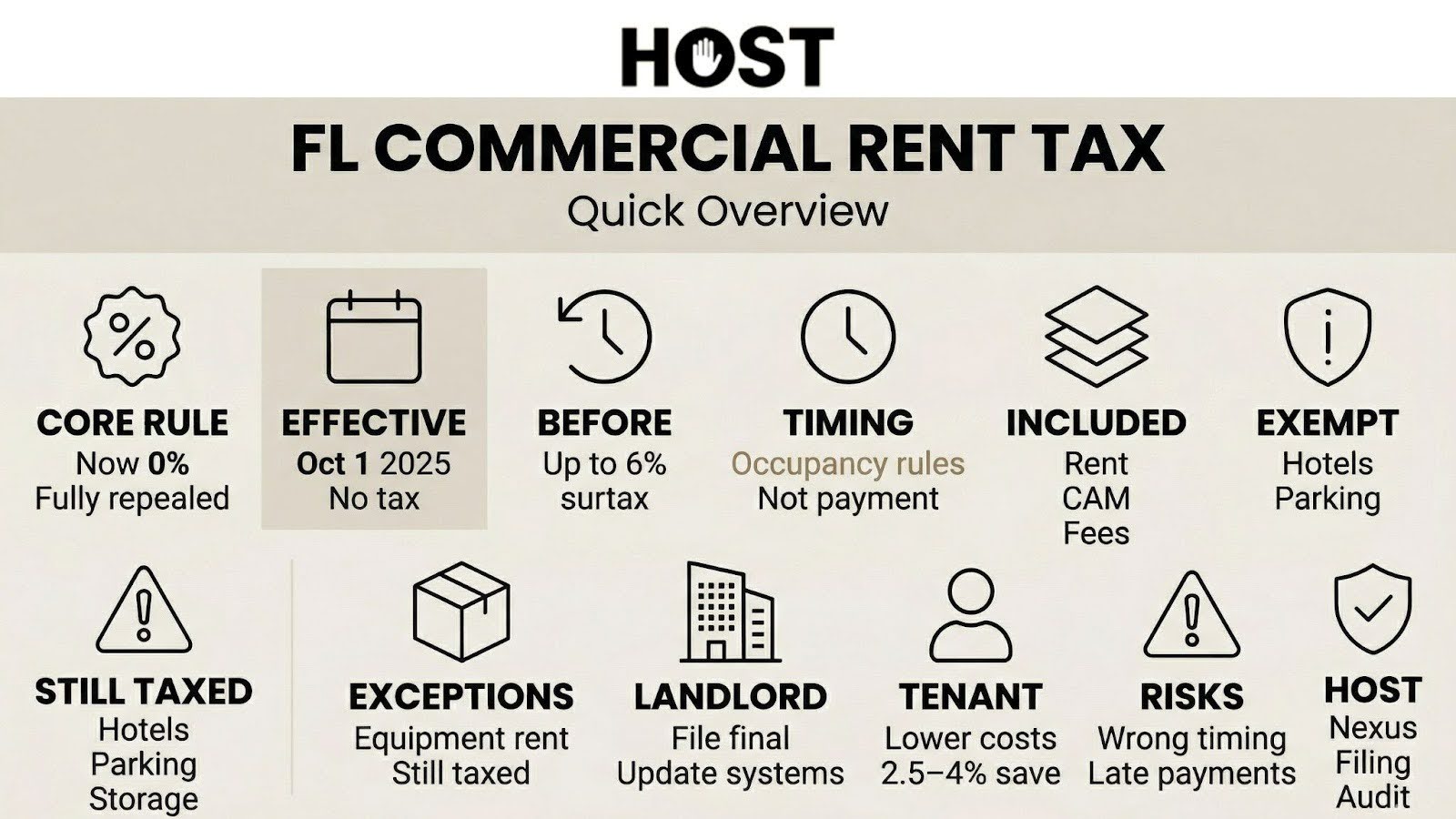

For decades, Florida stood alone as the only state taxing commercial rent. That changed October 1, 2025, when Florida eliminated both state and local sales taxes on commercial lease payments.

Whether you’re a landlord managing office buildings or a tenant leasing warehouse space, understanding this shift matters. From compliance through September 2025 to what remains taxable today, here’s what you need to know.

How Florida’s Commercial Rent Tax Evolved

Florida first imposed sales tax on commercial rent in 1968 at 4%. As the general sales tax climbed to 5%, then 6%, the commercial rent tax followed.

For over five decades, Florida remained the only state imposing statewide sales tax on commercial leases. This unique burden generated $2.64 billion in fiscal year 2024, substantial revenue for the state, substantial cost for businesses.

The Phase-Down Timeline

Florida systematically reduced the tax starting in 2017:

- 2017: 6% to 5.8%

- 2019: Down to 5.7%

- 2020: Reduced to 5.5%

- December 1, 2023: Cut to 4.5%

- June 1, 2024: Slashed to 2%

- October 1, 2025: Fully repealed

House Bill 7031, signed by Governor Ron DeSantis on June 30, 2025, delivered the final blow. The repeal saves Florida businesses an estimated $2.5 billion annually.

What Changed October 1, 2025

Florida sales tax no longer applies to commercial real property rent or license fees. Both state-level tax and county discretionary surtaxes disappeared.

The elimination covers:

- Office buildings and commercial space

- Retail storefronts and shopping centers

- Warehouses and distribution facilities

- Industrial and manufacturing facilities

- Self-storage units

- Convention and meeting rooms

- Land leases for commercial purposes

- License fees for vending machines, kiosks, and amusement machines

The Critical Timing Rule

Here’s where it gets specific: occupancy period controls, not payment date. Tax applies based on when the tenant occupies the property, regardless of when rent is paid.

Examples:

- September rent paid in October: Tax applies (occupancy predates repeal)

- October rent paid in September: No tax (occupancy begins October 1+)

- Late November payment for August occupancy: Tax applies

This distinction affects reconciliations and adjustments through 2025 and beyond for delayed payments.

What Was Taxable Through September 30, 2025

Before repeal, Florida taxed “total rent charged,” all consideration for using commercial property.

Beyond base rent, this included:

- Common area maintenance (CAM) charges

- Property taxes paid by tenants

- Insurance premiums on behalf of owners

- Property management fees

- Utilities structured as lease components

- Mortgage payments made by tenants

The law included charges “whether or not they can be attributed to the property’s ability to attract customers,” sweeping language that captured everything.

Local Surtaxes Added to the Burden

Florida counties imposed discretionary surtaxes ranging from 0.5% to 2.0% on top of state tax. Combined rates typically hit 3% to 3.5% statewide before June 2024’s reduction.

When state commercial rent tax was repealed, local discretionary surtax was eliminated simultaneously.

What’s Still Taxable: Important Exceptions

The repeal doesn’t cover everything. Several categories remain taxable under separate statutes.

Short-Term Accommodations

Rentals of six months or less remain taxable:

- Hotels and motels

- Vacation rentals

- Airbnb and similar platforms

- Extended-stay accommodations under six months

Vehicle, Boat, and Aircraft Storage

Sales tax continues on:

- Parking or storage for motor vehicles

- Boat docking or storage in marinas

- Aircraft tie-down or storage at airports

These specific categories remain taxable under Florida Statute 212.03, separate from the repealed commercial rent provisions.

Equipment Rentals

Equipment leased to tenants remains subject to Florida’s 6% sales tax. If a warehouse lease includes forklift rental as a separate charge, that equipment portion is taxable even though the warehouse space isn’t.

Landlord Compliance Requirements

Filing Through September 2025

Landlords must file returns for reporting periods through September 2025. Requirements vary by filing frequency:

- Monthly filers: Submit July, August, and September 2025 returns

- Quarterly filers: File Q3 2025 return

- Annual filers: Report only months with taxable rent received

Returns are required each period even if no tax is due. The Florida Department of Revenue automatically updates landlord accounts after receiving final returns.

Late Payments and Adjustments

Tax remains due on any rent for pre-October occupancy, whenever received:

- Late September rent paid in December

- Property tax reconciliations for pre-October periods

- Additional rent charges attributable to earlier occupancy

Landlords must identify occupancy periods accurately when determining tax obligations.

Refund Procedures

Incorrectly collected tax requires a specific process:

- Refund the tenant first

- Then file Form DR-26S requesting state reimbursement

- Maintain documentation for three years

The Department of Revenue won’t reimburse landlords who haven’t first refunded tenants.

System Updates

Landlords should immediately:

- Update billing systems to remove tax for October+ rent

- Review lease language referencing sales tax

- Notify tenants of the change

- Verify year-end reconciliations split correctly

Successor Liability

The Florida Department of Revenue has three years to audit filed returns. Property purchasers should verify sales tax compliance for the preceding three years as part of due diligence.

Tenant Considerations

Cost Savings

Eliminating 2% state tax plus local surtaxes saves approximately 2.5% to 4% on total rent expenses. For a business paying $100,000 monthly rent, that’s $2,000 to $4,000 saved each month.

Lease Review

Tenants should:

- Confirm October+ rent excludes sales tax

- Understand late payment implications for pre-October periods

- Review year-end CAM reconciliations for proper period splits

Capital Reallocation

Savings enable businesses to redirect capital toward:

- Employee compensation

- Infrastructure improvements

- Business expansion

- Equipment purchases

The $2.5 billion in annual savings creates significant growth opportunities statewide.

Why Florida Eliminated the Tax

National Competitiveness

Florida was the only state with statewide commercial rent tax, creating competitive disadvantage when businesses evaluated relocations.

Economic development professionals consistently cited the tax as a barrier, particularly for out-of-state businesses surprised by unexpected lease-related tax burdens.

Business Community Advocacy

Organizations including Florida Realtors and Florida Tax Watch lobbied for years. The gradual reduction from 2017 through 2024 reflected increasing legislative recognition of economic impact.

Revenue Growth Despite Rate Cuts

Despite rate reductions, revenue continued growing through economic expansion and in-migration, demonstrating Florida’s economy could sustain eventual full repeal without devastating state finances.

Sales Tax Beyond Commercial Rent

While commercial rent tax is eliminated, Florida businesses navigate numerous other obligations.

General Sales Tax

Florida imposes 6% state sales tax on tangible personal property and many services. Counties add surtaxes from 0.5% to 2%, creating combined rates of 6.5% to 8%.

Multi-State Complexity

For businesses operating across state lines, Florida represents one piece of a complex puzzle. Economic nexus thresholds, varying exemptions, and different filing frequencies create substantial administrative burden.

How Hands Off Sales Tax Helps

At Hands Off Sales Tax (HOST), we’ve focused exclusively on sales tax since 1999. Over 25 years navigating Florida’s evolving tax landscape, including commercial rent tax through its entire lifecycle.

Comprehensive Services

Nexus Analysis: We determine where your business has triggered obligations across Florida and other states, ensuring compliant collection without over-collecting.

Sales Tax Registration: We handle registrations with the Florida Department of Revenue and other jurisdictions, managing paperwork and communications.

Ongoing Filing: We prepare and file returns on your required schedule monthly, quarterly, or annually, including all local jurisdictions.

Notice Response: Received a Florida Department of Revenue letter? We interpret it, determine appropriate response, and handle communications.

Audit Defense: If you face audit, we organize documentation, prepare responses, and defend your position to minimize liability.

Voluntary Disclosure Agreements: Discovered past obligations? We negotiate VDAs to limit lookback periods and abate penalties.

Why Businesses Choose HOST

Through our parent company TaxMatrix, we’ve managed sales tax for North America’s largest corporations. We bring enterprise-level expertise to small and mid-sized businesses navigating Florida’s requirements.

You handle the sales, we handle the tax.

Get Florida Sales Tax Compliance Right

Florida’s commercial rent tax repeal represents historic savings, but doesn’t eliminate other sales tax obligations.

Whether ensuring general sales tax compliance, managing nexus across Florida locations, or expanding into new states, the right partner makes compliance seamless.

Ready to go completely hands-off with sales tax? Contact HOST today to discuss your sales tax needs.

Frequently Asked Questions

Is Florida commercial rent still taxed after October 1, 2025?

No. Florida fully repealed both state and local sales tax on commercial rent effective October 1, 2025. Lease payments for occupancy beginning on or after that date aren’t subject to tax.

What if I paid September rent in October? Do I owe tax?

Yes. Tax applies based on occupancy period, not payment date. September occupancy remains taxable even if paid in October or later.

Are short-term rentals affected by the repeal?

No. Short-term rentals of six months or less remain taxable under separate provisions. The repeal only applies to commercial leases under Florida Statute Section 212.031.

Do I still file returns if I only rent commercial property?

Landlords must file final returns for periods through September 2025. After filing, the Florida Department of Revenue automatically updates accounts. No separate closure action required.

Does the repeal apply to parking garages and boat storage?

No. Tax continues on parking/storage for vehicles, boat docking/storage, and aircraft tie-down/storage. These rentals are taxed under separate statutes unaffected by commercial rent tax repeal.

How much will Florida businesses save from the repeal?

Commercial tenants will save an estimated $2.5 billion annually from eliminating state and local taxes on commercial rent. Individual savings depend on rent amounts and previous local surtax rates. Most tenants save 2.5% to 4% of total rent expenses.