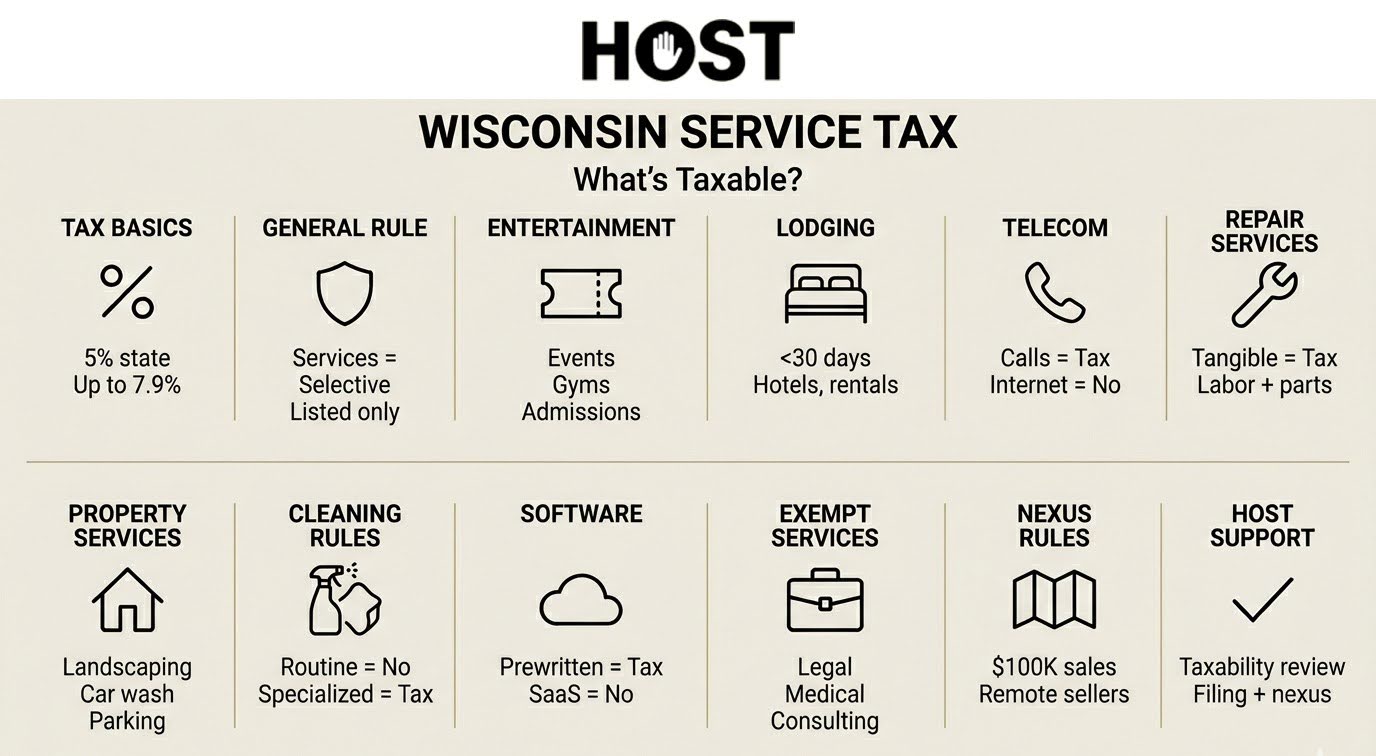

Are services taxable in Wisconsin? Unlike states that cast a wide tax net over most services, Wisconsin picks and chooses. Most professional and personal services remain exempt, while entertainment, lodging, telecommunications, and property-related services face the state’s 5% sales tax.

The distinction matters. Charging tax on exempt services creates refund headaches and frustrated customers. Missing taxable services? That’s back taxes, penalties, and interest. The kind of surprise that keeps business owners up at night.

Hands Off Sales Tax cuts through the complexity. From nexus analysis to multi-jurisdictional filing, we handle Wisconsin’s service tax obligations so you don’t have to.

Wisconsin’s Selective Service Tax Approach

Wisconsin imposes 5% state sales tax on designated services only. A “positive list” approach that exempts everything unless explicitly taxable under Wisconsin Statutes Chapter 77.

As of 2024, 68 of Wisconsin’s 72 counties add 0.5%. Milwaukee County charges 0.9%, and the City of Milwaukee tacks on 2%. Combined rates range from 5% to 7.9%.

Here’s the catch: tax applies based on customer location, not your business address. That telecommunications company serving Milwaukee collects 7.9%. Same company, different county? Could be 5%.

What Gets Taxed: Service by Service

Entertainment and Recreation

Whether you’re selling single tickets or gym memberships, admission to concerts, sporting events, theaters, amusement parks, golf courses, and fitness centers triggers tax. Coin-operated arcade games and rides also count.

Lodging

Any rental under one continuous month is taxable: hotels, motels, B&Bs, vacation rentals. That 30-day mark isn’t negotiable. Day 29? Taxable. Day 31? Exempt.

Interestingly, hotels are considered consumers of the telecommunications they provide to guests. They pay tax buying internet service, but don’t collect when passing costs to customers.

Telecommunications

Phone services like landline, mobile, VoIP are all taxable. That includes voicemail, call forwarding, caller ID. Cable and satellite TV too. Message recording services like answering services and security monitoring get taxed.

But internet access? Exempt since July 1, 2020.

Repair and Property Services

Fixing tangible personal property is taxable. Auto repair, appliance service, electronics. Labor and parts both get taxed.

Construction creates confusion. Real property construction stays exempt. Repairing tangible property gets taxed. Installing a new HVAC system during construction? Exempt. Repairing the existing one? Taxable.

Landscaping, lawn maintenance, planting all face tax. But here’s where it gets weird: rough grading for construction is exempt while fine grading is taxable. Lawn mowing? Taxable. Snow removal? Exempt.

Custom fabrication, printing, boat storage, parking, photography, and car washes all make the taxable list.

Cleaning Services: The Split: Routine janitorial services sweeping offices? Exempt. But specialized cleaning of tangible property such as carpet cleaning, industrial equipment detailing, pressure washing gets taxed. The line separates ongoing maintenance from creating a clean product.

Service Contracts

Maintenance agreements, warranties, and service contracts (including software maintenance contracts) are taxable. Sell equipment with a three-year maintenance plan? You’re collecting tax on the entire contract value upfront.

What Stays Exempt

Professional services dodge Wisconsin sales tax entirely. Accounting, legal, consulting, engineering, architecture. All exempt.

Medical care, dental services, therapy. Exempt.

Educational services, training, classes. Exempt (though training materials sold separately might be taxable).

Banking, insurance, investment advisory. Exempt.

Data processing services where you process client data stay non-taxable. This distinction matters for SaaS providers.

Haircuts, salon services, massage, spa treatments. Exempt (unless you’re selling products alongside).

Real property construction, building additions, improvements. Exempt for the contractor, though they pay use tax on materials.

Software and Digital Products: The Fine Print

Prewritten software is taxable whether downloaded or delivered on physical media. Off-the-shelf programs, standardized applications. If it’s canned software, it’s taxed.

Custom software developed for a single customer? Exempt.

SaaS is generally non-taxable when treated as data processing. Customers access software remotely without possession transfer. Wisconsin clarified this January 1, 2025: remotely accessed software without possession transfer avoids taxation.

Certain digital goods like e-books, music, movies get taxed.

When Collection Becomes Mandatory

Economic Nexus: Remote sellers exceeding $100,000 in gross Wisconsin sales current or previous year must collect. That includes both taxable and non-taxable sales. No transaction count to track.

Physical Nexus: Offices, employees, inventory, property in Wisconsin creates nexus requiring collection.

The Complication: A telecommunications company serving Wisconsin remotely needs to register once hitting $100K. A consulting firm providing exempt services may exceed $100,000 without triggering collection, unless they also sell taxable service contracts.

HOST’s nexus analysis examines your complete sales footprint, identifying exactly where you’ve triggered obligations based on economic thresholds, physical presence, or affiliate relationships.

Common Compliance Traps

The Manufacturing Principle: Services that create or manufacture products face taxation. A carpenter building custom furniture? Creating a product? Taxable. A consultant providing strategic advice? Pure service. Exempt. Understanding this distinction prevents misclassification.

Bundled Services: Single invoice for taxable and nontaxable services? Wisconsin taxes the entire amount unless you separately state charges. That consulting project including taxable software installation? Break out the line items or everything gets taxed.

Construction vs. Repair: The line between exempt construction and taxable repair causes frequent errors. Installing cabinets during new construction? Exempt. Replacing existing cabinets? Taxable.

Software Misclassification: Treating SaaS as taxable prewritten software or failing to tax actual downloads creates gaps. The possession transfer test determines everything.

Service Contract Timing: Maintenance agreements trigger immediate tax on the full contract value, even for multi-year terms. Missing this creates use tax liabilities.

Shipping Charges: Taxable products make shipping taxable too. Shipping mixed orders? Allocate costs. Only the portion for taxable items gets taxed.

Wrong Rate, Wrong Place: Using your business location’s rate instead of the customer’s location leads to under-collection or over-collection.

How HOST Simplifies Wisconsin Service Tax

Wisconsin’s selective service tax creates ongoing complexity. Monitoring nexus, classifying services, calculating location-based rates, filing across jurisdictions.

Nexus Analysis: We examine sales by state and service type, determining exactly where you’ve triggered Wisconsin’s $100,000 threshold or physical presence obligations.

Service Classification: Through consultation, HOST clarifies which offerings face taxation under Wisconsin’s rules.

Registration: We handle Wisconsin Department of Revenue registration, obtaining permits and establishing required accounts.

Multi-Jurisdictional Filing: Wisconsin requires separate state and local reporting. HOST manages monthly, quarterly, or annual returns based on your volume.

Software Integration: We review and optimize TaxJar and Avalara configurations, ensuring correct service tax calculations by location.

Audit Defense: When Wisconsin DOR audits arrive, HOST manages communications, organizes documentation, and defends classifications.

We’ve focused exclusively on sales tax for over 25 years. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

Your Next Step

Wisconsin’s selective approach benefits most service providers, but taxable categories demand careful compliance. Misclassifying services, missing local requirements, or overlooking nexus creates audit exposure.

For telecommunications providers, entertainment venues, lodging operators, repair services, and other Wisconsin service businesses, professional management eliminates guesswork and prevents costly mistakes.

Contact us today to discuss your Wisconsin sales tax needs or schedule a free consultation.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Are most services taxable in Wisconsin?

No. Most services remain exempt. Wisconsin taxes specific categories like entertainment, lodging, telecommunications, and property repair while exempting professional, medical, educational, and most business services.

What is Wisconsin’s sales tax rate on services?

5% state tax, with most counties adding 0.5% and Milwaukee imposing higher local rates. Combined rates typically range from 5% to 7.9%.

Is SaaS taxable in Wisconsin?

Generally no. SaaS is treated as exempt data processing when customers access software remotely without possession transfer. However, downloaded prewritten software is taxable.

Do I collect Wisconsin service tax as an out-of-state provider?

Yes, if you exceed $100,000 in gross Wisconsin sales during the current or previous year, you must register and collect sales tax on taxable services provided to Wisconsin customers.

Are professional services like consulting and accounting taxable?

No. Professional services including accounting, legal, consulting, and engineering are not subject to Wisconsin sales tax.

How do I know if my specific service is taxable?

Consult Wisconsin Department of Revenue Publication 201 for detailed service tax guidance, or schedule a consultation with HOST for personalized classification help.