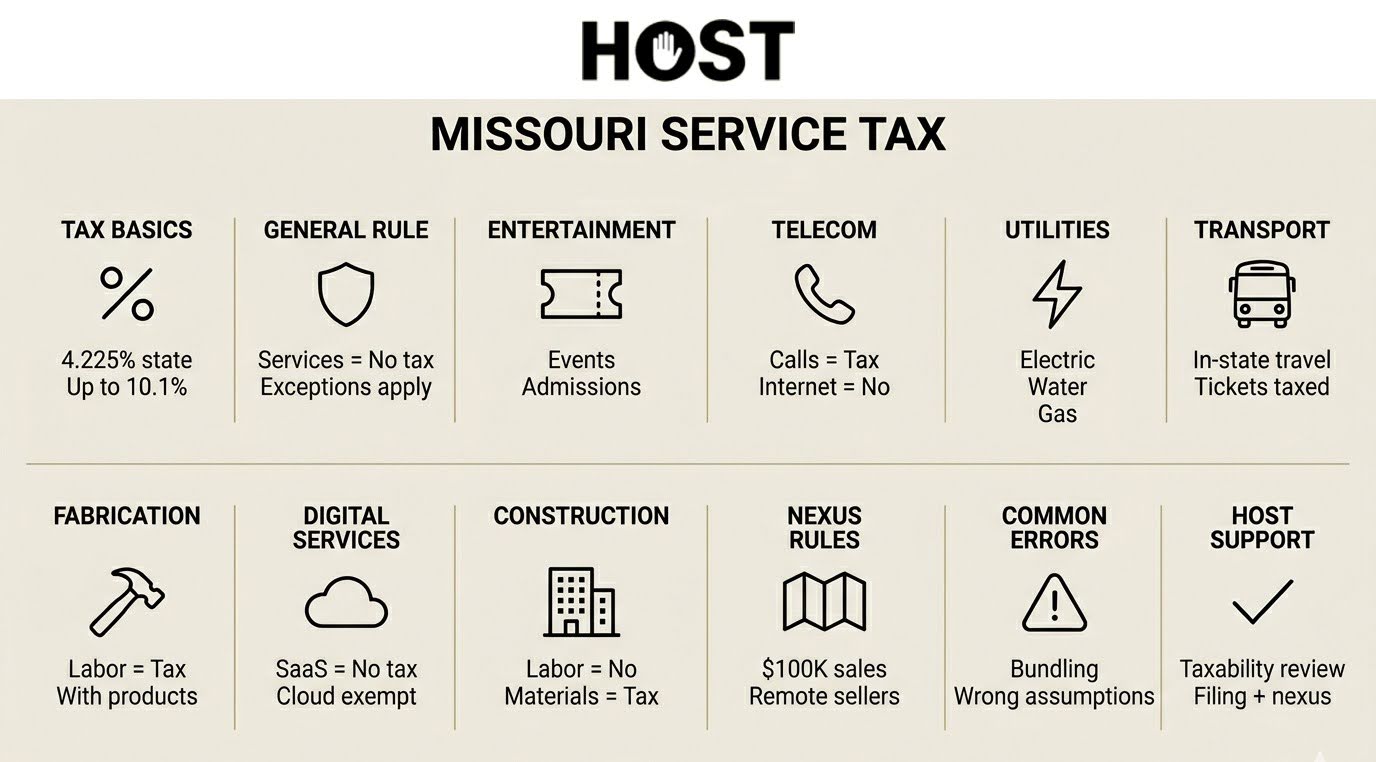

Most services escape Missouri sales tax, but the exceptions trip up businesses constantly. While tangible goods face the standard 4.225% state rate, services live in different territory. Know which ones trigger collection obligations, and you avoid audit surprises.

Missouri’s economic nexus threshold sits at $100,000 in annual sales. Cross it selling taxable services to Missouri customers, and collection starts. Physical presence optional. Entertainment venues, telecom companies, utilities providers: all need clarity on when tax applies.

Hands Off Sales Tax (HOST) specializes in exactly this. We’ve spent 25+ years determining which services trigger obligations, handling registrations across jurisdictions, and managing ongoing filings so compliance doesn’t drain your resources.

Missouri’s Service Tax Rule: Simple Until It Isn’t

Services are generally not taxable in Missouri. Professional services, consulting, advertising, cleaning—all exempt. But specific categories face Missouri’s tax machinery, and combined state and local rates can hit 10.1% in some jurisdictions.

Taxable Services in Missouri

Entertainment and Admissions

Admission fees and seating at places of amusement, entertainment, recreation, and athletic events are taxable. Concert venues, movie theaters, sporting arenas, amusement parks are all collect tax on ticket sales.

Missouri defines “place of amusement” broadly: any location where amusement activities constitute more than a minimal portion of operations. If entertainment drives your business model, you’re collecting tax.

Telecommunications Services

Local and long-distance telecommunication services face Missouri sales tax. Traditional phone service, wireless plans, VoIP, all taxable.

Missouri courts ruled VoIP calls are taxable telecommunications services, establishing that tax frameworks extend to new voice technologies. Your delivery method doesn’t matter. Voice calls get taxed.

Critical distinction: Internet access and interactive computer services remain exempt. Voice services over internet infrastructure? Taxable. The internet connection itself? Exempt.

Utilities Services

Electricity, water, gas, and sewer services are taxable for residential, commercial, and industrial users. Most utility consumption faces sales tax obligations.

Transportation Services

Intrastate tickets for buses, railroads, airplanes, and licensed motor carriers are taxable. Travel entirely within Missouri triggers tax. Interstate trips beginning or ending outside Missouri generally escape.

Fabrication Labor

Labor to fabricate products sold at retail is taxable. Missouri prevents fabricators from separating labor charges to claim exemption. Fabrication work and materials get taxed together.

Commonly Confused Services

Event planning and coordination: Not taxable. You’re selling expertise, not tangible goods. However, if you sell decorations, linens, or equipment as part of your service, those items face tax.

Consulting services: Exempt across the board: management consulting, IT consulting, marketing strategy. The moment you deliver tangible products (printed reports, USB drives with presentations), those items become taxable.

Catering: The food is taxable as tangible personal property. Your service fee for setup, coordination, and cleanup (if separately stated) isn’t taxable as a service, but most catering packages get taxed entirely.

Fitness and gym memberships: Not taxable. Personal training, yoga instruction, group fitness classes. All exempt services.

Landscaping and lawn care: Service labor isn’t taxable. But if you sell and install plants, mulch, or hardscaping materials, you’re selling tangible property and charging tax.

Web design and digital services: Providing hosted websites or cloud-based solutions? Not taxable. Delivering website files on USB drives or physical media? The tangible delivery method may trigger tax obligations.

Construction Services: Missouri’s Counterintuitive Approach

Missouri handles construction differently than most states. Construction labor is not taxable. Contractors don’t charge clients sales tax on building, repairing, or remodeling work.

Instead, Missouri treats contractors as end consumers of materials. When contractors buy lumber, concrete, or drywall, they pay sales tax because they’re using materials in real property improvements. The materials become part of buildings, so no longer tangible personal property available for resale.

Contractors pay tax going in, clients pay nothing on the completed work. This flips the script from states like Kansas, where commercial remodeling labor often faces tax.

If repair labor on tangible personal property is separately stated, it’s not taxable. But parts and materials used in repairs face tax.

Digital Services and SaaS: Favorable Territory

Missouri provides breathing room for digital services. Software as a Service is not subject to sales tax, per statute 12 CSR 10-109.050.

Cloud-based software, SaaS subscriptions, remotely accessed applications, streaming services, data storage, all exempt. Missouri voters approved a constitutional amendment in November 2016 prohibiting taxation of services not taxed as of January 1, 2015. This constitutional barrier blocks SaaS taxation.

The catch: Bundling matters. SaaS bundled with taxable items such as hardware or downloadable software without separate charges can make the entire package taxable. Invoice itemization protects you.

Prewritten software on physical media (CDs, DVDs, USB drives) remains taxable. Delivery method determines treatment.

When Registration Becomes Mandatory

Physical Nexus

Physical presence creates immediate obligations: offices, warehouses, employees, inventory, or regular business activity in Missouri.

Economic Nexus

Missouri’s economic nexus threshold is $100,000 in gross sales to Missouri customers within the previous or current calendar year. This includes tangible goods and taxable services.

At each calendar quarter’s end, calculate your Missouri sales over the preceding 12 months. Exceed $100,000, and you register within three months following that quarter.

Sales through marketplace facilitators count toward your threshold even when platforms collect tax on your behalf.

Sales Tax Rates: State Plus Local Complexity

Missouri’s 4.225% state rate applies uniformly. Local jurisdictions add 0% to 5.875%, creating combined rates reaching 10.1% in some locations.

St. Louis sees combined rates between 9.68% and 11.68% depending on specific addresses. Kansas City averages 8.99%. Rates vary within single ZIP codes based on city limits and special districts.

For businesses providing taxable services across Missouri, address-level precision matters.

Common Compliance Mistakes

Assuming blanket exemption: Missouri’s general rule (services aren’t taxable) creates false security. Telecommunications providers or entertainment venues discover their taxable status during audits triggering back taxes, penalties, and interest.

Not understanding when services become products: The line blurs when services create deliverable products. Web designers providing hosted websites? Not taxable. Web designers delivering website files on USB drives? The USB drive (and potentially the files) may trigger tax obligations.

Bundling without itemization: Mixing taxable telecommunications with nontaxable internet access on single-line invoices often taxes the entire charge. Separate line items document which portions face obligations.

Ignoring economic nexus monitoring: Service businesses operating remotely often skip Missouri sales tracking until determination letters arrive. By then, retroactive collection, interest, and penalties accumulate.

Misapplying construction rules: Businesses unfamiliar with Missouri’s unique treatment charge tax when they shouldn’t, or skip tax on materials when required. Both create problems.

How HOST Simplifies Service Taxability

Service taxability shifts dramatically state-to-state. Missouri exempts what Kansas taxes. Telecommunications rules differ in Illinois. Managing multi-state compliance demands specialized expertise.

What HOST Delivers

Nexus Analysis: We examine your service offerings and sales footprint to determine precisely where you’ve triggered obligations, economic or physical in Missouri and elsewhere.

Service Taxability Research: Our team identifies which services are taxable in each state where you have nexus, accounting for industry rules, bundling issues, and state variations.

Registration Management: We handle sales tax permits with Missouri and all required states, managing paperwork and state communications.

Automated Filing: HOST prepares and files returns across jurisdictions monthly, quarterly, annually including state, local, and special district filings.

Audit Defense: When Missouri issues audit notices, we organize documentation, respond to examiners, and defend positions to minimize liability.

Software Integration: We review your automation tools (TaxJar, Avalara, others) ensuring correct service taxability settings, preventing calculation errors.

We’ve focused exclusively on sales tax for 25+ years. That expertise helps businesses navigate compliance so they focus on growth instead of tax codes.

Take the Guesswork Out of Service Taxability

Determining which services trigger Missouri obligations shouldn’t require legal expertise. Entertainment, telecommunications, utilities, or any other category. Clear answers prevent audit exposure and customer confusion.

For multi-state operations, complexity multiplies exponentially. Each jurisdiction applies different rules, exemptions, thresholds. Getting it wrong with back taxes, penalties, interest, audit costs exceeds the investment in proper compliance.

HOST combines technical expertise with transparent communication and personalized support. You get clear answers about service taxability, accurate registration and filing, and ongoing compliance management without tracking 13,000+ U.S. tax jurisdictions.

When you’re ready to ensure service compliance in Missouri and beyond, we’re ready to handle the complexity. Contact HOST today to discuss your taxability questions and discover how we take sales tax off your plate.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Are professional services like accounting or legal services taxable in Missouri?

No. Professional services including accounting, legal, consulting, and advertising aren’t subject to Missouri sales tax. The state’s general rule is services aren’t taxable unless specifically listed as exceptions.

Is SaaS (Software as a Service) taxable in Missouri?

No. Missouri doesn’t tax SaaS or cloud-based software subscriptions. A constitutional amendment passed in 2016 prevents taxing services not taxed as of January 1, 2015, effectively blocking SaaS taxation.

Do contractors charge sales tax on construction labor in Missouri?

No. Construction labor isn’t taxable in Missouri. However, contractors pay sales tax when purchasing materials because Missouri treats them as end consumers of construction materials.

Are telecommunications services taxable in Missouri?

Yes. Local and long-distance services, including VoIP, are taxable in Missouri. Internet access remains exempt, but voice calling services face tax obligations.

What is Missouri’s economic nexus threshold for service businesses?

Missouri’s economic nexus threshold is $100,000 in gross sales to Missouri customers within the previous or current calendar year. This applies to tangible goods and taxable services.

Are utilities taxable in Missouri?

Yes. Sales of electricity, water, gas, and sewer services are taxable in Missouri for domestic, commercial, and industrial users.