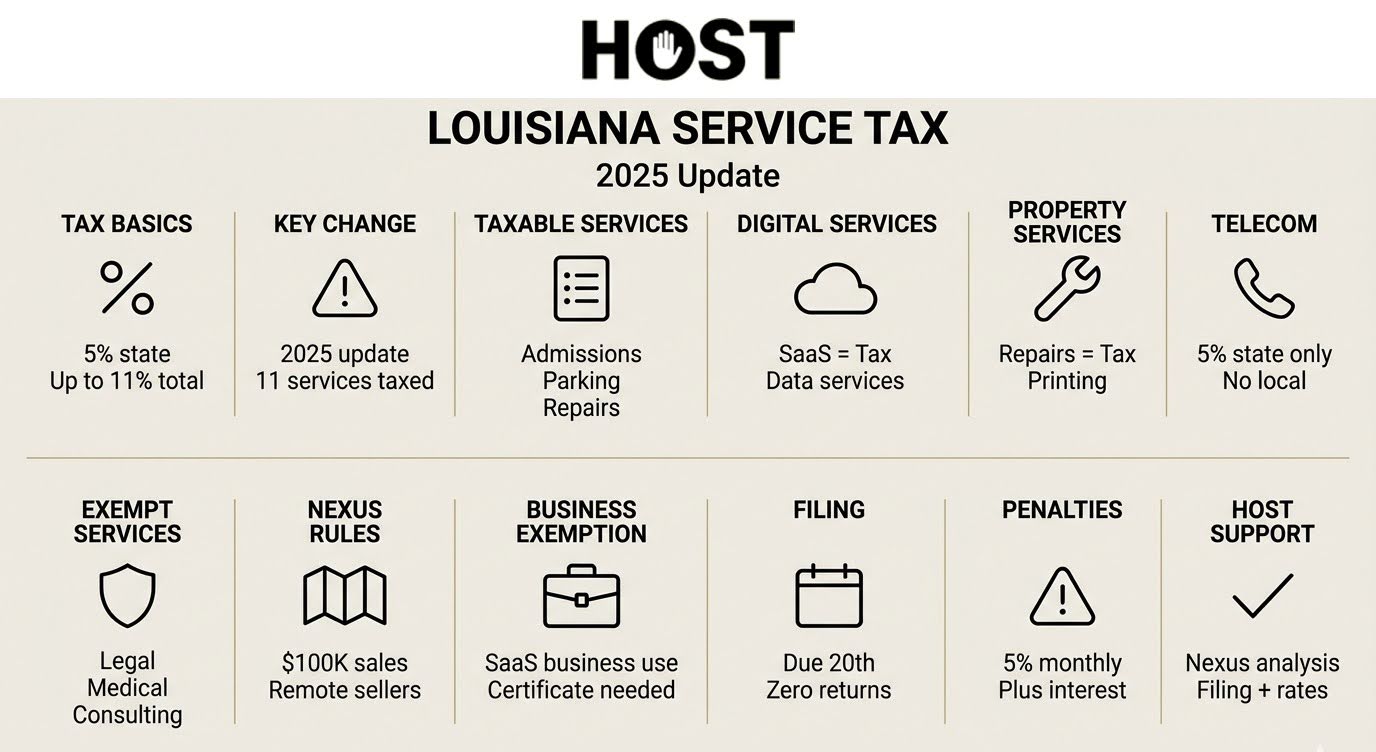

Are services taxable in Louisiana? For most service businesses, the answer is no, but crucial exceptions exist. Louisiana historically taxed goods over services, keeping professional and personal services exempt. That changed dramatically in 2025.

Starting January 1, 2025, Louisiana’s service taxation shifted under Act 11 of the 2024 Third Extraordinary Session. The state now taxes 11 specific service categories at a 5% state rate—plus local taxes in most cases.

Whether you’re a SaaS provider newly subject to tax, a telecommunications company navigating rate changes, or a service business confirming exempt status, knowing Louisiana’s rules prevents costly compliance gaps.

At Hands Off Sales Tax (HOST), we specialize in exactly this complexity. From nexus analysis to automated filings across Louisiana’s 64 parishes, we handle multi-state and multi-parish compliance so you focus on growth.

Louisiana’s Approach to Service Taxation

Louisiana follows a narrow service tax policy. Unlike states that broadly tax services, Louisiana taxes only services explicitly listed in statute. Everything else remains exempt.

Professional services such as accounting, legal advice, consulting, architectural design, and medical care generally escape sales tax. Personal services like haircuts, personal training, and dry cleaning also remain non-taxable.

The distinction? Louisiana taxes specific commercial services that generate entertainment value, provide digital access, or involve tangible property repair.

Louisiana’s Taxable Services (Effective January 1, 2025)

Louisiana’s R.S. 47:301.3 consolidates all taxable services. According to the Louisiana Department of Revenue, there are 11 services subject to state sales tax. The state retained existing taxable services and added 2 new categories (prewritten computer software access services and information services) effective January 1, 2025.

1. Furnishing Sleeping Rooms and Accommodations

Hotels, motels, short-term rentals (including Airbnb), bed and breakfasts, and any establishment providing overnight accommodations to transient guests must collect sales tax. This includes rooms purchased through online travel companies like Expedia and Orbitz, covering the full accommodation charge including booking and service fees.

2. Admissions to Amusement, Entertainment, and Recreational Events

Sales tax applies to admission charges for theaters, concerts, sporting events, amusement parks, museums, and festivals. The tax extends to participation fees: escape rooms, trampoline parks, or any facility charging for recreational access. Even nonprofit organizations must collect sales tax on admission tickets and parking fees unless they qualify for specific exemptions.

3. Storage and Parking Services

Auto hotels, parking lots, and parking garages collecting vehicle storage or parking fees must collect sales tax. This includes short-term parking (hourly or daily) and long-term storage, plus valet services when separately charged.

4. Telecommunications Services

Louisiana imposes a 5% state sales tax on telecommunications services, which is collected at the state level instead of local taxes. Telecommunications includes traditional phone services, Voice over Internet Protocol (VoIP), prepaid calling cards, and text messaging. Mobile phone plans with voice and data are fully taxable.

5. Laundry, Cleaning, Pressing, Alteration, Repair and Dyeing Services

Louisiana taxes laundry and cleaning services broadly: commercial laundry operations, personal dry cleaning, pressing, garment alterations and repairs, and dyeing services. This applies to both business-to-business services (linen services to restaurants) and personal consumer services.

6. Furnishing of Cold Storage Space

Businesses providing refrigerated warehouse space, cold storage facilities for food products, or temperature-controlled storage for pharmaceuticals must collect sales tax on all charges for accessing and using the space.

7. Repairs to Tangible Personal Property

Repair services involving tangible personal property trigger tax: appliance repairs, electronics repairs, vehicle repairs and maintenance, and equipment repairs. The taxable amount includes labor and parts. However, repairs to immovable property (home renovations, building repairs) remain non-taxable. The rule: if it moves, repairs are taxable.

8. Printing and Related Services

Commercial printing services (offset, digital, letterpress, screen printing) are taxable, plus related services like binding, laminating, and finishing when bundled with printing work.

9. Sales of Prepaid Calling Cards

Prepaid phone cards providing predetermined calling time are taxable. A longstanding Louisiana requirement.

10. Prewritten Computer Software Access Services (NEW in 2025)

Software as a Service (SaaS) is now taxable in Louisiana. Prewritten computer software access services include cloud-based software where users access applications remotely: CRM platforms, project management tools, accounting software, email marketing platforms, data storage, and graphic design tools. The tax applies to monthly subscriptions, annual licenses, and usage-based pricing.

11. Information Services (NEW in 2025)

Information services like electronic data retrieval and information delivery are now taxable. This includes research databases, credit reporting services, market research data, legal research platforms (Westlaw, LexisNexis), and business intelligence platforms.

12. Cable Television, Satellite, and Video Programming Services

Cable television, direct-to-home satellite, video programming, and satellite digital audio radio services face a 5% state-only sales tax. Collected instead of local taxes, not in addition to them.

What Services Remain Exempt?

Most service businesses don’t collect Louisiana sales tax. Exempt services include:

Professional Services: Accounting, tax preparation, legal services, architectural design, engineering, medical and dental care, veterinary care, and business consulting remain exempt.

Personal Services: Haircuts, salon services, massage therapy, personal training, and pet grooming remain non-taxable.

Real Estate, Financial, and Educational Services: Real estate commissions, property management, banking fees, investment advisory, insurance premiums, tutoring, and training programs are exempt.

If your service doesn’t appear on the 11 taxable categories, you generally don’t collect Louisiana sales tax.

Louisiana’s 2025 Sales Tax Changes

Louisiana implemented sweeping changes effective January 1, 2025:

State Rate Increased to 5%: Louisiana’s rate increased from 4.45% to 5%, remaining at 5% through December 31, 2029, then reducing to 4.75% on January 1, 2030.

Combined Rates Exceed 10%: With local parish and municipal taxes, Louisiana now has combined rates from 5% to over 11%. Louisiana has the highest combined state and average local sales tax rate nationally at 10.11%.

Digital Products Now Taxable: Act 10 expanded Louisiana’s sales tax to digital audiovisual works, digital audio, digital books, digital games, and digital codes.

Nexus: When You Must Collect Louisiana Sales Tax

Nexus is the connection triggering tax obligations. Two types create nexus:

Physical Nexus: Maintaining an office, employing people, storing inventory (including through fulfillment services), or providing services at Louisiana customer locations creates physical nexus.

Economic Nexus: Remote sellers must collect Louisiana sales tax once they exceed $100,000 in Louisiana sales during the current or previous calendar year. Once you exceed $100,000, register within 30 days and begin collecting within 60 days. This threshold applies identically to service businesses—if your SaaS company sells $100,000+ to Louisiana customers, you have nexus.

HOST’s nexus analysis service determines exactly where you’ve triggered obligations across all parishes.

Business-Use Exemptions: How to Avoid Tax on SaaS Purchases

Louisiana offers a business-use exemption for digital products and SaaS purchased exclusively for commercial purposes. If you’re buying project management software, accounting platforms, or data storage for business operations you don’t pay sales tax, but you must document it properly.

Who Qualifies: Businesses purchasing SaaS or digital products used solely for business operations, not personal use or resale to consumers.

Documentation Requirements: Provide your vendor with a completed exemption certificate specifying business use. Keep records proving commercial application: business email domain, company credit card, business address.

Common Mistakes: Using personal email for business SaaS (creates audit risk), mixing personal and business use on same subscription (makes entire purchase taxable), failing to provide exemption certificate upfront (you’ll pay tax and struggle to recover it).

Healthcare providers also receive exemptions for SaaS used to store/transmit healthcare information or diagnose/treat medical conditions.

Handling Mixed Service Bundles

What happens when you sell taxable and exempt services together? Louisiana applies a “dominant purpose” rule: if the primary purpose is taxable, the entire bundle is taxable.

Example 1: You provide consulting (exempt) plus SaaS access (taxable) in one package. If the SaaS is the dominant component (the main reason customers buy) the entire fee is taxable.

Example 2: HVAC companies selling repair services (taxable) bundled with annual maintenance contracts. The repair portion is clearly taxable; determine if maintenance also constitutes “repairs to tangible personal property.”

Best Practice: Separately state exempt and taxable services on invoices when possible. This creates clear documentation and may reduce your taxable base.

Filing Requirements

Louisiana assigns filing frequency monthly, quarterly, or annually based on tax liability. Returns are due by the 20th day of the month following the reporting period. Louisiana requires filing even with zero sales.

Penalties: 5% of tax due monthly for late filing (max 25%), 0.5% monthly for late payment (max 25%), plus 4.5% annual interest. A $1,000 liability filed one month late triggers a $50 penalty plus interest.

Vendor’s Compensation: Louisiana allows businesses to retain 1.05% of tax collected, capped at $750 monthly (reduced from $1,500), only when filed and paid timely.

Common Mistakes Service Businesses Make

Assuming All Services Are Exempt: The biggest error is assuming exempt status without verifying Louisiana’s rules. SaaS providers often discover taxable status only after Louisiana notices uncollected tax.

Charging the Wrong Rate: Louisiana’s destination-based sourcing means rates depend on customer location. Using your business location’s rate creates underpayment or overpayment.

Ignoring Economic Nexus: Remote service providers often ignore economic nexus. Louisiana’s $100,000 threshold is easily crossed by successful SaaS businesses. If you sold $120,000 in subscriptions to Louisiana customers in 2024 but never registered, you’ve been operating non-compliant since crossing the threshold.

Failing to File Zero Returns: Louisiana requires filing even with no sales. Many skip filing during slow periods, triggering penalties.

Misunderstanding Business-Use Exemptions: SaaS vendors often incorrectly collect tax from business customers who qualify for exemptions, or fail to collect exemption certificates, creating audit exposure for both parties.

If You Just Discovered You Should Be Collecting

Realizing you’ve been selling taxable services without collecting Louisiana sales tax? You’re not alone. The 2025 expansion caught many businesses unprepared.

Your Situation: You’ve been providing SaaS, repair services, or other taxable services to Louisiana customers for months (or years) without collecting sales tax. Maybe you didn’t know the rules changed, or you misunderstood nexus requirements.

Your Exposure: Louisiana can assess back taxes for up to 4 years, plus 5% monthly late filing penalties (max 25%), 0.5% monthly late payment penalties (max 25%), and 4.5% annual interest. If you’ve collected $50,000 in untaxed revenue, you could owe $5,000+ in back taxes plus penalties exceeding $2,500.

Your Solution: Voluntary Disclosure Agreements limit lookback periods (typically 3 years vs. 4), often abate 100% of penalties, and let you come forward anonymously before Louisiana discovers the issue. The sooner you act, the better your outcome.

Timeline Example: If you started selling taxable SaaS January 2025 and it’s now February 2026, a VDA filed today limits exposure to 12-13 months of back taxes with no penalties, versus waiting until Louisiana contacts you in 2027 with a 24+ month assessment plus full penalties.

HOST: Your Partner for Louisiana Service Tax Compliance

Whether you’re a newly-taxable SaaS provider, a telecommunications company adjusting to rate changes, or confirming exempt status, professional guidance prevents costly mistakes.

What HOST Delivers:

Nexus Analysis: We analyze your Louisiana footprint to determine exactly where you’ve triggered obligations across parishes and municipalities.

Sales Tax Registration: We handle registration with Louisiana and every applicable jurisdiction.

Automated Filing: We prepare and file Louisiana returns monthly, quarterly, or annually, handling state and local filings.

Rate Calculation: We determine correct tax rates for every transaction based on precise customer location.

Notice Management: When Louisiana sends confusing notices, we interpret and respond on your behalf.

Audit Defense: We’re your trusted partner in resolving sales tax audits, organizing documentation and defending your position.

Voluntary Disclosure Agreements: If you discover past obligations, we file VDAs to limit lookback periods and negotiate penalty abatement.

We’ve been 100% focused on sales tax since 1999. Over 25 years managing compliance. Founded by Mike Espenshade, serving North America’s largest companies, we bring enterprise expertise to service businesses of all sizes.

Ready to Simplify Louisiana Compliance?

Louisiana’s 2025 service tax expansion caught many businesses unprepared. Professional sales tax management eliminates guesswork, prevents penalties, and frees your team to focus on growth.

Contact HOST today to discuss your Louisiana service tax obligations. Whether you need full-service compliance or strategic guidance, we’re ready to help.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Are professional services taxable in Louisiana?

No. Professional services like accounting, legal advice, consulting, architectural design, and medical services remain exempt. Louisiana only taxes the 11 specific service categories listed in R.S. 47:301.3.

Is SaaS taxable in Louisiana?

Yes. Effective January 1, 2025, Louisiana taxes SaaS as “prewritten computer software access services” at the 5% state rate plus applicable local taxes. This includes cloud-based platforms, subscription software, and remotely accessed applications.

What is Louisiana’s sales tax rate on services?

Louisiana charges a 5% state rate on taxable services (effective January 1, 2025), plus local parish and municipal taxes varying by location. Combined rates range from 5% to over 11%. Telecommunications services are taxed at 5% state-only with no local additions.

Do I need to collect Louisiana sales tax if I’m located out of state?

Yes, if you exceed $100,000 in Louisiana sales during the current or previous calendar year. This economic nexus threshold applies regardless of physical presence. Register within 30 days and begin collecting within 60 days of exceeding the threshold.

How do I register for Louisiana sales tax?

Register through the Louisiana Department of Revenue’s GeauxBiz portal at www.geauxbiz.com. Registration requires your FEIN, business structure details, NAICS code, and service description. Registration is free.

What happens if I don’t collect sales tax on taxable services in Louisiana?

Louisiana holds businesses liable for uncollected tax. You’ll owe back taxes, 5% monthly penalties (up to 25%), 0.5% monthly late payment penalties (up to 25%), and 4.5% annual interest. Voluntary disclosure agreements can limit lookback periods and reduce penalties if you come forward before Louisiana discovers the issue.