Understanding whether professional services are taxable in California saves businesses from compliance headaches and unexpected penalties. Unlike many states, California doesn’t tax services including professional work like legal, accounting, consulting, and medical services. But exceptions exist that create real obligations for certain labor types.

Whether you’re a consultant expanding into California or an established business reviewing tax obligations, knowing these nuances protects you from costly mistakes. Hands Off Sales Tax (HOST) specializes in navigating these complexities, ensuring businesses collect correctly without the compliance burden.

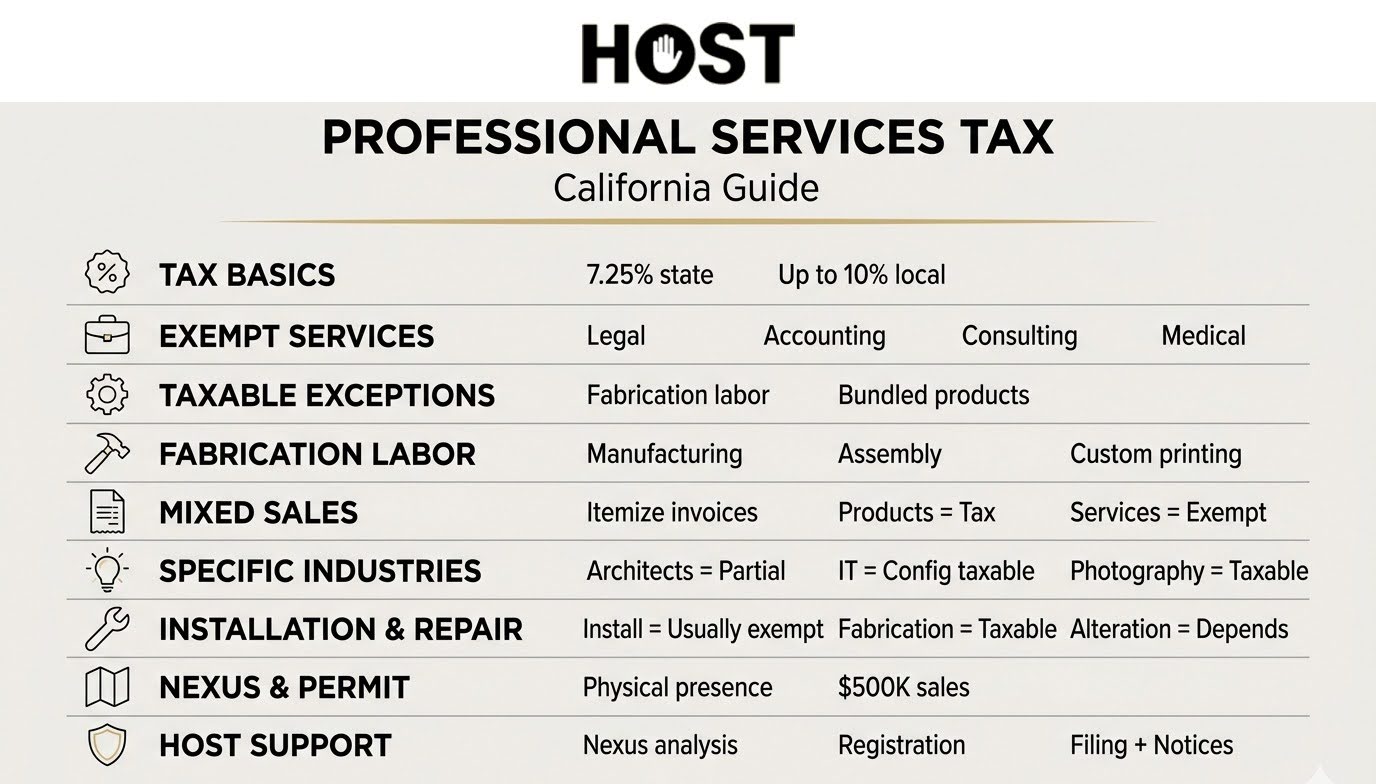

What Makes California’s Service Tax Rules Different

California’s sales tax system focuses on tangible property rather than services. The statewide base is 7.25% (6% state + 1.25% local), with local districts adding taxes that can push combined rates above 10% in some areas.

This makes California fundamentally different from states that broadly tax services. Most pure services remain exempt because they don’t involve transferring tangible property.

The key principle: California taxes goods, not expertise.

Are Professional Services Taxable in California?

No. Professional services such as legal, medical, accounting, consulting, and therapy are exempt from California sales tax. When you bill purely for expertise, those charges remain non-taxable.

This covers legal representation, tax preparation, business consulting, medical care, architectural design, and engineering services. Any professional advice billed separately from tangible products.

The exemption applies regardless of billing structure: hourly rates, flat fees, retainers, or project-based pricing all remain tax-exempt for pure professional services.

When Services Become Taxable: The Critical Exceptions

California’s straightforward exemption has two important exceptions: services inseparable from tangible property sales, and fabrication labor.

Services Inseparable from Tangible Property

When a service is so tied to property that it becomes part of the sale, the entire charge becomes taxable. Even itemizing separately won’t help.

For example, machinery requiring calibration as a condition of sale means the calibration fee is taxable. Training bundled with required software purchases? Also taxable.

Fabrication Labor

Fabrication labor like work creating tangible property different from its components, is taxable. This includes manufacturing, producing, processing, or assembling products.

The CDTFA defines fabrication broadly: manufacturing machinery, cutting customer-provided materials, assembling components, altering items to create new products, or custom printing.

Even drilling holes in metal and bending it to create a bracket constitutes taxable fabrication.

The line between taxable fabrication and non-taxable repair often confuses businesses. Altering new garments is taxable because it’s a step in creating a new item. Altering used clothing after purchase is exempt repair labor.

Specific Professional Industries: Where Gray Areas Exist

Some professional services blur the line between pure expertise and tangible deliverables, creating confusion about taxability:

Architects and Engineers: While consulting remains exempt, creating blueprints or construction drawings constitutes taxable fabrication labor because you’re creating tangible property. The intellectual work of designing remains exempt, and the physical deliverable becomes taxable.

IT Consultants and Software Professionals: Strategic technology advice is exempt. Custom software development remains non-taxable. But software configuration, customization bundled with products, or installation crosses into taxable territory when it becomes inseparable from a product sale.

Photography Services: One of the few service types explicitly taxed both digital and physical photographs and related services are subject to California sales tax, making photography a unique exception to California’s service exemption rule.

Marketing and Creative Agencies: Digital-only deliverables (strategy documents, reports sent electronically) remain exempt. Printed materials, promotional items, or tangible marketing collateral become taxable products requiring separate invoicing.

Training and Educational Services: Stand-alone training is exempt. Training bundled inseparably with equipment purchases or software becomes taxable as part of the product sale.

The “true object test” helps determine borderline cases: Is the primary purpose receiving the service or the tangible item? If clients primarily value your expertise rather than the physical deliverable, the service typically remains exempt.

Installation, Repair, and Modification Services

Installation Labor: Generally non-taxable when separately stated. Installing a car stereo generates non-taxable labor charges when itemized. Exception: installation constituting “fabrication on site” becomes taxable.

Repair Labor: Tax doesn’t apply to itemized repair charges like work restoring property to intended use. However, if parts exceed 10% of total charges or are separately stated, parts become taxable while labor may remain exempt.

Alteration: Whether alteration services are taxable depends on the item’s status. Altering new items constitutes fabrication (taxable). Altering previously used items constitutes repair (non-taxable labor, though materials may be taxable if over 10% of total charge).

Mixed Transactions: Products and Services Combined

When you sell both taxable goods and non-taxable services, itemize invoices to clearly separate taxable products from non-taxable services.

A graphic designer selling creative services (non-taxable) and printed materials (taxable product) must separate these charges. Combined without itemization, California may tax the entire transaction.

Clear invoicing protects your business: list products and services separately, show quantities for tangible goods, label service charges clearly, calculate sales tax only on taxable totals, and provide your California Seller’s Permit number.

Nexus and Registration Requirements

Even when services remain non-taxable, businesses selling any taxable products need California seller’s permits.

California requires businesses with nexus to register, collect, and remit sales tax on taxable sales. Physical presence creates nexus immediately. Remote sellers exceeding $500,000 in California sales must register.

Professional service providers who occasionally sell tangible products like training materials, printed guides, or software on physical media need seller’s permits even if 95% of revenue comes from exempt services.

Filing Requirements and Penalties

Filing frequency depends on tax liability: monthly (over $1,000 monthly collected), quarterly ($601-$1,000 monthly), or annually ($600 or less monthly).

Penalties:

- Late filing: up to 10% of tax due, plus interest

- Failure to remit collected tax: 40% penalty on unremitted amounts

- Collection Cost Recovery Fees for delinquent accounts

A business collecting $5,000 monthly but failing to remit faces potential $2,000 penalties monthly plus interest, turning administrative oversights into financial crises.

Common Mistakes Professional Service Providers Make

Misclassifying Fabrication Labor: Believing all labor is exempt leads to underreporting when work creates new tangible property. Blueprint creation, sign design, and custom manufacturing generate taxable fabrication labor.

Bundling Without Itemization: Combining taxable products with non-taxable services under single charges creates presumption that entire amounts are taxable.

Ignoring Materials Thresholds: When repair services include materials exceeding 10% of total charges, those materials become taxable even when labor remains exempt.

Missing Economic Nexus: Professional service providers expanding into product sales often miss the $500,000 threshold, discovering multi-year back-tax liabilities.

Using Generic Invoicing: Vague descriptions like “professional services and supplies” provide insufficient documentation during audits. Specific line items prove exempt status.

Failing to Obtain Resale Certificates: When providing services to clients who resell your work, proper resale certificates make the transaction non-taxable. Missing certificates mean you’ll pay tax on B2B transactions that should be exempt.

Why Businesses Choose Professional Sales Tax Management

California’s nuanced service taxability rules create compliance challenges. When should you consider expert help?

- You provide both professional services and sell products or materials

- Your work involves fabrication, assembly, or creating tangible property

- You’ve expanded into California and need nexus analysis

- You’re unsure whether specific services or bundled offerings are taxable

- You’ve received CDTFA notices questioning past filings

HOST specializes in California sales tax compliance through comprehensive services:

Nexus Analysis: We analyze your California sales footprint to determine precisely where obligations exist: from physical presence, economic activity, or specific service types.

Sales Tax Registration: We handle CDTFA registration paperwork and follow-up, ensuring proper licensing for all required activities.

Ongoing Filing Services: We prepare and file returns monthly, quarterly, or annually, managing the entire process so you stay compliant.

Software Review: We audit existing configurations to identify costly mistakes like overtaxing exempt services, missing required taxes, or double-taxing due to system overlaps.

Notice Management: We interpret and respond to CDTFA notices, handling communications and resolving issues efficiently.

Audit Defense: If the CDTFA initiates an audit, we organize documentation, explain positions, and work to minimize liability.

With over 25 years focused exclusively on sales tax, HOST has helped businesses from solo consultants to multi-state enterprises navigate California’s requirements.

Next Steps: Ensuring Compliance Without the Headache

Professional services in California remain largely exempt, but exceptions around fabrication labor, bundled products, and mixed transactions create real compliance obligations. Understanding where your specific services fall protects you from penalties while ensuring correct customer billing.

Contact HOST today to discuss your California sales tax situation. Our team provides clarity on taxability questions, handles registrations and filings, and ensures compliance across all California jurisdictions.

Ready to get sales tax off your plate? Schedule a free consultation or grab our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book to learn common pitfalls.

Frequently Asked Questions

Are professional services taxable in California?

No. Professional services such as legal, medical, accounting, and consulting work are exempt from California sales tax. These services don’t involve transferring tangible property.

What kinds of services are taxable in California?

Services tied to creating, producing, or fabricating tangible goods are taxable. This includes manufacturing labor, custom printing, and fabrication services.

Do I charge sales tax if I provide both products and services?

Yes, but only on the taxable product portion. Itemize invoices clearly to separate taxable goods from non-taxable professional services.

How do I know if my labor is considered fabrication?

Fabrication labor creates tangible property different in form or function from its components. If your work produces new items or constitutes a step in creating new products, it’s taxable fabrication.

What happens if I fail to file sales tax on time in California?

Penalties of up to 10% apply, plus interest charges. Businesses failing to remit collected tax face 40% penalties. Delinquent accounts may also face Collection Cost Recovery Fees.

Do I need a California seller’s permit if I only provide services?

If your services are purely professional and never involve selling tangible products or taxable labor, you don’t need a permit. However, if you sell any taxable items, materials, or perform fabrication work, you must register regardless of how small that portion of your business is.